Cutaneous Lupus Erythematosus Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

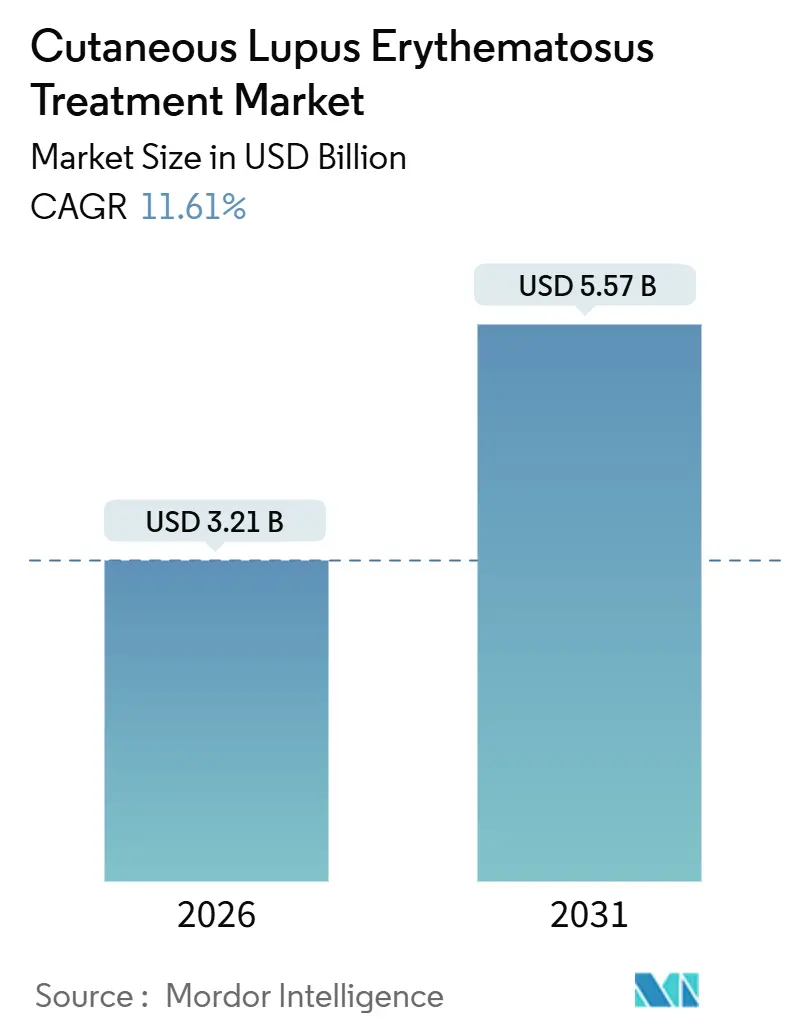

| Market Size (2026) | USD 3.21 Billion |

| Market Size (2031) | USD 5.57 Billion |

| Growth Rate (2026 - 2031) | 11.61% CAGR |

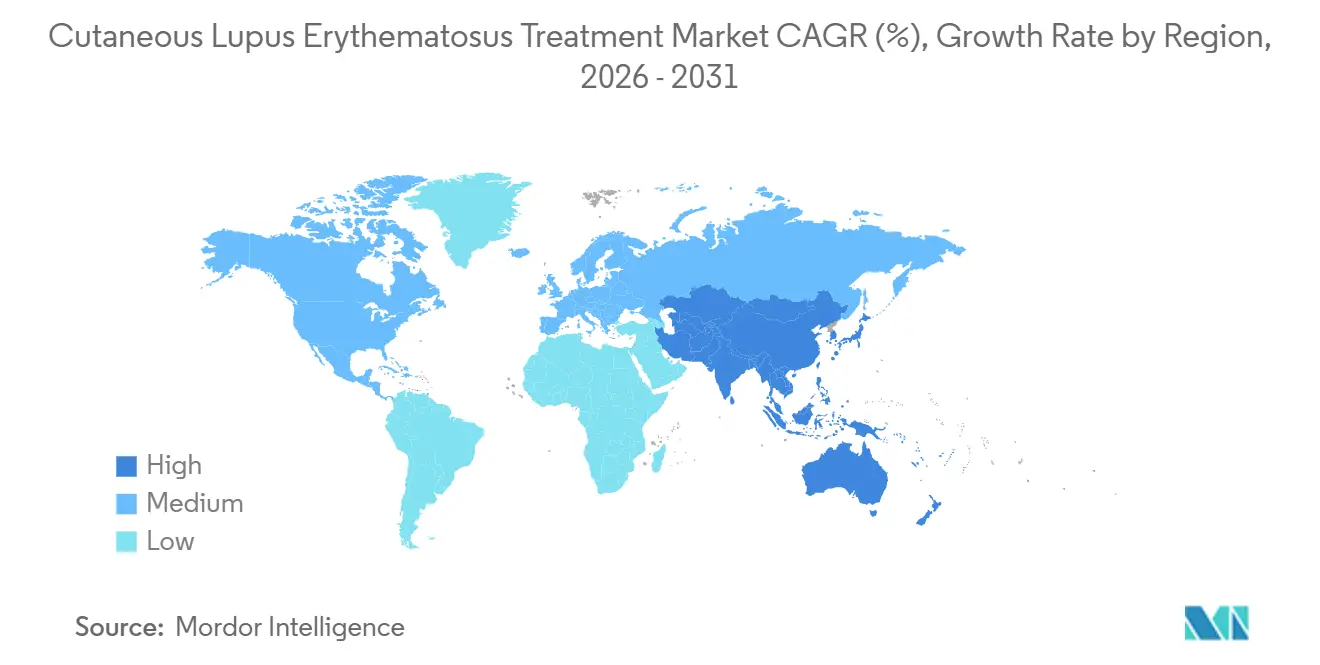

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

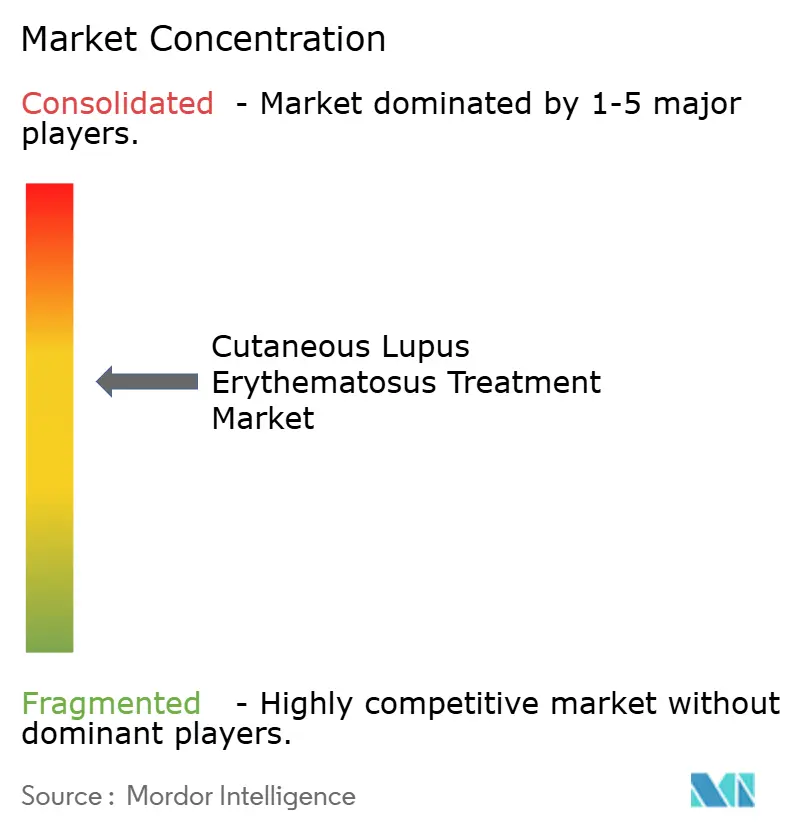

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cutaneous Lupus Erythematosus Treatment Market Analysis by Mordor Intelligence

The Cutaneous Lupus Erythematosus Treatment Market size is estimated at USD 3.21 billion in 2026, and is expected to reach USD 5.57 billion by 2031, at a CAGR of 11.61% during the forecast period (2026-2031).

Regulatory momentum for type I interferon-blocking biologics, the arrival of low-cost generic antimalarials in price-sensitive regions, and the use of AI-enabled CLASI scoring in pivotal trials together shorten approval cycles and underpin the expansion. Steroid-phobia is shifting prescribing toward corticosteroid-sparing regimens that combine antimalarials with topical immunomodulators, thereby widening the addressable patient pool. Competitive intensity is rising as BDCA2- and CD40L-targeting antibodies read out positive Phase 3 data, while Chinese developers secure fast-track status for TYK2 and molecular-glue candidates. Hospitals still dominate biologic dispensing, yet teledermatology-linked e-pharmacies are scaling rapidly in markets with reliable broadband and payer reimbursement parity guidance. Payers in Europe and Asia require real-world corticosteroid-sparing evidence before granting broad biologic coverage, tempering uptake outside high-income segments.

Key Report Takeaways

- By treatment type, antimalarials held 32.55% of the cutaneous lupus erythematosus treatment market share in 2025; biologics and targeted therapies are forecast to grow at a 15.25% CAGR through 2031.

- By disease subtype, chronic CLE accounted for 42.53% of demand in 2025, while subacute CLE is advancing at a 12.85% CAGR to 2031.

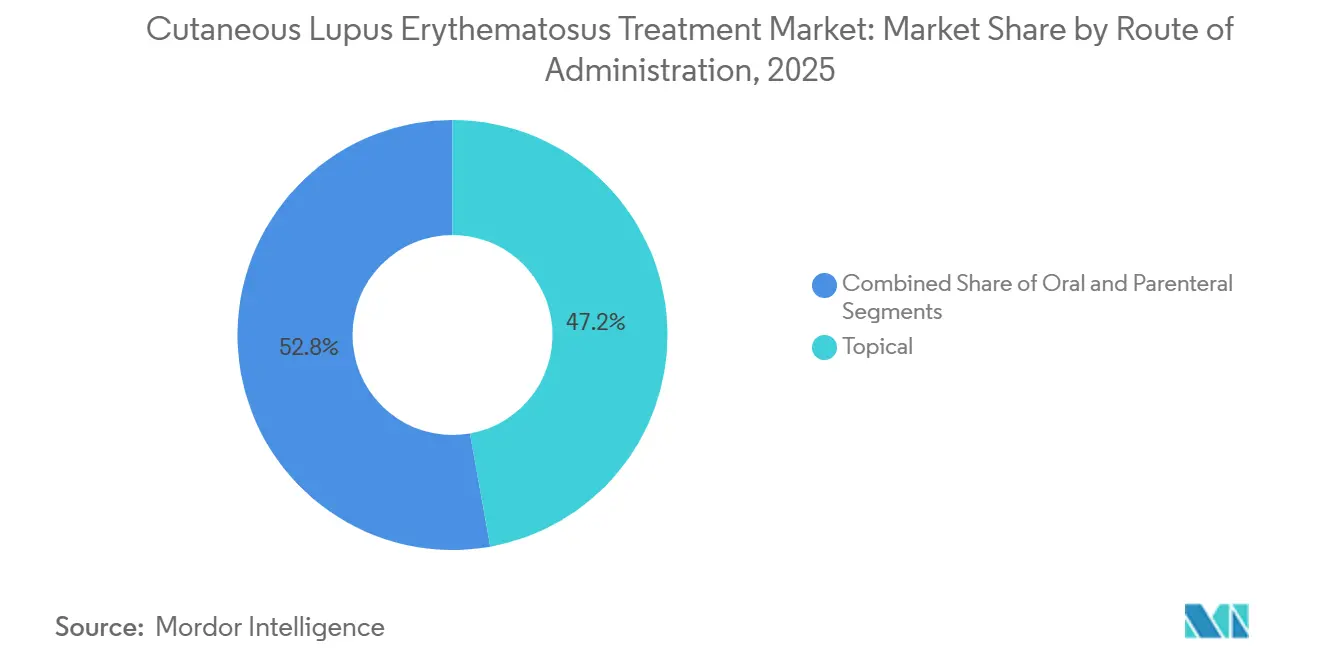

- By route of administration, topical formulations captured 47.23% of the cutaneous lupus erythematosus treatment market size in 2025 and parenteral delivery is set to expand at a 14.55% CAGR through 2031.

- By distribution channel, hospital pharmacies accounted for 43.33% demand in 2025; online / e-pharmacy channels will post a 15.55% CAGR to 2031.

- By geography, North America generated 38.25% of 2025 revenue; Asia-Pacific is projected to post a 12.21% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cutaneous Lupus Erythematosus Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CLE prevalence & earlier diagnosis | +2.3% | North America, Europe | Medium term (2-4 years) |

| Uptake of biologic therapies | +3.1% | North America, Europe, APAC urban | Long term (≥4 years) |

| Generics boost for hydroxychloroquine & topicals | +1.8% | APAC, South America, MEA | Short term (≤2 years) |

| Teledermatology accelerates access | +1.5% | North America, Europe, select APAC | Medium term (2-4 years) |

| AI-enabled CLASI scoring in trials | +1.2% | Global | Long term (≥4 years) |

| Rare-disease incentives fuel pipelines | +1.7% | North America, Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising CLE Prevalence & Earlier Diagnosis

United States surveillance recorded a prevalence of 108.9 per 100,000 population in 2025, yet dermatologists believe under-diagnosis persists, especially in primary care[1]Centers for Disease Control and Prevention, “Lupus Detailed Facts,” cdc.gov. Awareness campaigns by the Lupus Foundation and the American Academy of Dermatology train clinicians to recognize malar rash and discoid lesions sooner, raising treatment eligibility for mild cases. Mandatory 800 × 600-pixel image standards in AAD teledermatology guidance cut wait times for specialist review from weeks to days. Earlier capture of subacute phenotypes pivots demand to oral antimalarials and topical agents, delaying systemic escalation. Medium-term gains center on the United States and Western Europe, where reimbursement parity for virtual visits took effect in 2025. Collectively, these factors add 2.3 percentage points to the forecast CAGR.

Uptake of Biologic Therapies

A December 2025 CHMP positive opinion for subcutaneous anifrolumab widened administration options beyond infusion and primes the molecule for home or clinic injection. The LAVENDER trial evaluates anifrolumab in chronic and subacute CLE with CLASI-70 as the primary endpoint; success would grant the first FDA-approved CLE biologic indication. Real-world data from a Tufts-Brigham cohort showed a mean 18-point CLASI-A drop at 6 months in refractory patients. Belimumab demonstrates mucocutaneous benefit in pooled SLE analyses, though a CLE-specific label remains pending. High U.S. and EU price tags of USD 30,000-50,000 annually mean uptake concentrates in insured segments, but the clinical value proposition adds 3.1 percentage points to CAGR forecasts.

Generics Boost for HCQ & Topicals in EMs

IPCA sells HCQS 200 mg at INR 66.52 per 10 tablets (USD 0.80) in India, an order of magnitude cheaper than North American brands. China and India placed hydroxychloroquine and chloroquine on essential medicine lists, guaranteeing hospital procurement and rural distribution. Low-cost topical corticosteroids likewise enter public formularies, strengthening first-line adherence where biologics are unaffordable. These dynamics raise near-term growth by 1.8 percentage points in APAC, South America and MEA.

Teledermatology Accelerates Access

AAD’s 2025 framework granted payment parity for asynchronous and live video consults. Rural patients now send lesion images that dermatologists grade remotely, accelerating CLASI-based therapy adjustments without travel. Platforms integrate AI triage tools that flag urgent cases, further lifting specialist throughput. North America and Europe lead adoption thanks to broadband penetration and payer mandates. The channel expansion contributes 1.5 percentage points to medium-term CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologic cost & patchy reimbursement | -2.5% | APAC, South America, MEA | Medium term (2-4 years) |

| Safety-driven limits (ocular, JAK) | -1.8% | North America, Europe | Short term (≤2 years) |

| API shortages for quinacrine/thalidomide | -0.9% | North America, Europe | Short term (≤2 years) |

| Steroid-phobia curbs aggressive therapy | -1.3% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Biologic Cost & Patchy Reimbursement

Annual prices of USD 30,000-50,000 for anifrolumab or belimumab strain health budgets outside high-income economies. HTA bodies such as NICE reject coverage unless cost-effectiveness ratios fall below EUR 50,000 per QALY, a hurdle difficult to clear given CLE’s low mortality impact. Only Japan and South Korea routinely reimburse biologics in APAC; China’s provincial formularies remain inconsistent. Consequently, penetration outside private-pay segments drags medium-term CAGR by 2.5 percentage points.

Safety-Driven Usage Limits

Hydroxychloroquine carries a boxed warning for irreversible retinal toxicity, mandating annual OCT and visual-field testing that adds monitoring cost and reduces adherence[2]U.S. Food and Drug Administration, “Plaquenil Label,” fda.gov. In 2023 the FDA and EMA placed class-wide warnings on JAK inhibitors for cardiovascular and malignancy risks, sharply curtailing off-label CLE experimentation. Topical JAK creams face local immunosuppression caveats, restricting chronic use. Collectively, safety concerns lower short-term growth by 1.8 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Biologics Outpace Legacy Antimalarials

Antimalarials held 32.55% of cutaneous lupus erythematosus treatment market share in 2025, anchored by hydroxychloroquine’s first-line status. However, regulatory greenlights for subcutaneous anifrolumab and positive BDCA2 data propel biologics toward a 15.25% CAGR through 2031. Clinicians increasingly reserve systemic corticosteroids for flares, aligning with EULAR 2023 and ACR 2025 guidelines that promote steroid-sparing regimens.

The cutaneous lupus erythematosus treatment market size tied to biologics is forecast to rise markedly as orphan-drug exclusivity underpins premium pricing. Conversely, immunosuppressants such as methotrexate serve as bridge therapy but gradually lose share to targeted agents. Niche drugs like quinacrine and thalidomide remain constrained by API shortages and teratogenicity risk.

By Disease Subtype: Chronic CLE Dominates, Subacute Accelerates

Chronic CLE generated 42.53% of segment demand in 2025 due to its high prevalence and scarring risk that drives lengthy therapy. Earlier tele-diagnosis now captures subacute cases sooner, enabling antimalarial initiation that restricts progression. Subacute CLE therefore posts a 12.85% CAGR to 2031, the fastest within subtype splits.

Cutaneous lupus erythematosus treatment market size gains for subacute disease draw investor attention to trials such as LAVENDER, which intentionally excludes acute systemic flares to maximize endpoint consistency. Regional treatment algorithms vary: China prioritizes topical-first approaches to limit systemic exposure, while Western protocols escalate more quickly to oral therapy.

By Route of Administration: Parenteral Gains on Subcutaneous Shift

Topical agents retained 47.23% of market revenue in 2025 due to widespread corticosteroid and calcineurin use. Yet parenteral modalities will grow at a 14.55% CAGR thanks to autoinjector versions of anifrolumab that reduce infusion-center dependence.

Parenteral share of cutaneous lupus erythematosus treatment market size rises further in rural areas where home injection mitigates travel burden. Oral antimalarials persist as an accessible middle step but face adherence challenges tied to ocular monitoring. Topical JAK inhibitors remain investigational, potentially inserting a targeted topical alternative once long-term safety data mature[3]LEO Pharma, “2024 Six-Month Interim Report,” leo-pharma.com.

By Distribution Channel: E-Pharmacy Emerges

Hospital pharmacies currently dominate biologic dispensing, yet telemedicine-linked e-pharmacies are scaling quickly wherever regulators permit direct-to-patient shipping. Specialty clinics maintain a core role in diagnosis and initial prescribing, but virtual follow-up and home delivery increasingly displace in-person refills.

Although precise cutaneous lupus erythematosus treatment market share metrics for each channel vary by country, the directional trend shows e-pharmacy eroding hospital share in North America and parts of Europe. Regulatory fragmentation in India and China tempers acceleration, but harmonization initiatives are underway.

Geography Analysis

North America contributed 38.25% of 2025 revenue on the back of Medicare Part D coverage for hydroxychloroquine and commercial insurer reimbursement for anifrolumab. Academic centers in Boston, Los Angeles and Toronto anchor CLE trial activity, keeping provider awareness high. Uptake of biologic autoinjectors is set to expand further as specialty-pharmacy networks streamline prior authorization and shipment, though payer step-therapy rules still require antimalarial failure first.

Asia-Pacific is projected to record a 12.21% CAGR through 2031, the fastest across regions. China’s NMPA cleared InnoCare’s TYK2 inhibitor ICP-488 and Kangpu’s molecular-glue KPG-818 for CLE-related trials in 2025, signaling policy support for home-grown innovation. Meanwhile, India’s bulk procurement of USD 0.80 hydroxychloroquine packs widens access in public hospitals. Japan and South Korea maintain universal biologic coverage, allowing rapid diffusion once local safety data accrue.

Europe grows more slowly due to stringent HTA hurdles, yet the EMA’s centralized orphan-drug pathway accelerates approvals once cost-effectiveness is demonstrated. Germany and France have begun conditional reimbursement tied to post-marketing corticosteroid-sparing data. Eastern European markets lean heavily on generics, delaying biologic uptake.

Middle East, Africa and South America remain nascent but see spot growth in urban private hospitals in São Paulo, Buenos Aires, Dubai and Johannesburg. Brazil’s ANVISA recently shortened review timelines for rare-disease therapies, while Argentina’s currency volatility hampers biologic imports. Medical tourists from MEA increasingly source treatment in India and Thailand where costs are lower, creating a shadow flow of demand outside conventional channel tracking.

Competitive Landscape

The arena is moderately concentrated, with top global firms controlling biologic portfolios and fragmented generics populating antimalarials. Biogen’s litifilimab and dapirolizumab pegol posted positive Phase 3 data in 2024, potentially giving the company first-mover advantage in CLE-specific biologics. AstraZeneca and GSK leverage SLE-approved molecules for off-label CLE use while racing to secure formal indications via LAVENDER and other trials.

Chinese contenders InnoCare and Kangpu exploit lower trial costs and expedited NMPA review to advance TYK2 and molecular-glue mechanisms, respectively, aiming to leapfrog Western incumbents in APAC markets. Technology adoption is a differentiator: sponsors deploying AI-enabled CLASI scoring compress development timelines and gain regulatory goodwill.

Strategic moves in 2025-2026 include Johnson & Johnson’s USD 1.25 billion purchase of Yellow Jersey Therapeutics to acquire a bispecific IL-4Rα/IL-31 antibody, underscoring the appetite for multi-pathway dermatology assets. LEO Pharma and Arcutis meanwhile position topical JAK and PDE4 inhibitors as future corticosteroid-sparers, eyeing label expansion into CLE once safety dossiers mature.

Cutaneous Lupus Erythematosus Treatment Industry Leaders

GSK plc

AstraZeneca plc

Biogen Inc.

LEO Pharma A/S

Sun Pharmaceutical Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: InnoCare gained NMPA clearance for Phase 2 testing of TYK2 inhibitor ICP-488 in CLE, the first APAC-originated TYK2 program to reach this stage.

- May 2025: Merck reported positive data for enpatoran, an oral TLR7/8 inhibitor, showing clinically meaningful rash reduction in CLE/SLE patients.

Global Cutaneous Lupus Erythematosus Treatment Market Report Scope

As per the scope of the report, Cutaneous Lupus Erythematosus (CLE) is a form of lupus erythematosus that primarily affects the skin. It is characterized by photosensitive skin lesions that can appear as discoid plaques, erythema, or rash, often on sun-exposed areas. CLE may occur independently or as part of systemic lupus erythematosus (SLE). The condition involves immune-mediated inflammation of the skin, and its management typically includes sun protection, topical therapies, and sometimes systemic medications.

The segmentation of the cutaneous lupus erythematosus treatment market is categorized by treatment type, disease subtype, route of administration, distribution channel, and geography. By treatment type, the market includes topical corticosteroids, topical calcineurin inhibitors, antimalarial drugs, immunosuppressants, biologics and targeted therapies, and other treatment types. By disease subtype, it is segmented into acute CLE (ACLE), subacute CLE (SCLE), and chronic CLE (CCLE). By route of administration, the market is divided into topical, oral, and parenteral. By distribution channel, it comprises hospital pharmacies, specialty clinics and dermatology clinics, online or e-pharmacy channels, and other channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Topical Corticosteroids |

| Topical Calcineurin Inhibitors |

| Antimalarial Drugs |

| Immunosuppressants |

| Biologics & Targeted Therapies |

| Other Treatment Types |

| Acute CLE (ACLE) |

| Subacute CLE (SCLE) |

| Chronic CLE - (CCLE) |

| Topical |

| Oral |

| Parenteral |

| Hospital Pharmacies |

| Specialty Clinics and Dermatology Clinics |

| Online / E-Pharmacy Channels |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Topical Corticosteroids | |

| Topical Calcineurin Inhibitors | ||

| Antimalarial Drugs | ||

| Immunosuppressants | ||

| Biologics & Targeted Therapies | ||

| Other Treatment Types | ||

| By Disease Subtype | Acute CLE (ACLE) | |

| Subacute CLE (SCLE) | ||

| Chronic CLE - (CCLE) | ||

| By Route of Administration | Topical | |

| Oral | ||

| Parenteral | ||

| By Distribution Channel | Hospital Pharmacies | |

| Specialty Clinics and Dermatology Clinics | ||

| Online / E-Pharmacy Channels | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the cutaneous lupus erythematosus treatment market?

The market is valued at USD 3.21 billion in 2026.

How fast is the market expected to grow through 2031?

It is projected to advance at an 11.61% CAGR, reaching USD 5.57 billion.

Which therapy class is expanding the quickest?

Biologics and targeted small molecules are forecast to grow at a 15.25% CAGR as regulatory approvals widen.

Why is Asia-Pacific growth outpacing other regions?

Rapid NMPA approvals, expanding public formularies and low-cost generics drive a 12.21% CAGR in Asia-Pacific.

What safety issues limit certain treatments?

Retinal toxicity with hydroxychloroquine and cardiovascular and malignancy risks with JAK inhibitors constrain broader use.

How are teledermatology platforms influencing care?

Payment-parity rules and high-resolution imaging let specialists diagnose and monitor CLE remotely, accelerating early antimalarial use.

Page last updated on: