Low Melting Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.52 Billion |

| Market Size (2031) | USD 3.46 Billion |

| Growth Rate (2026 - 2031) | 6.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

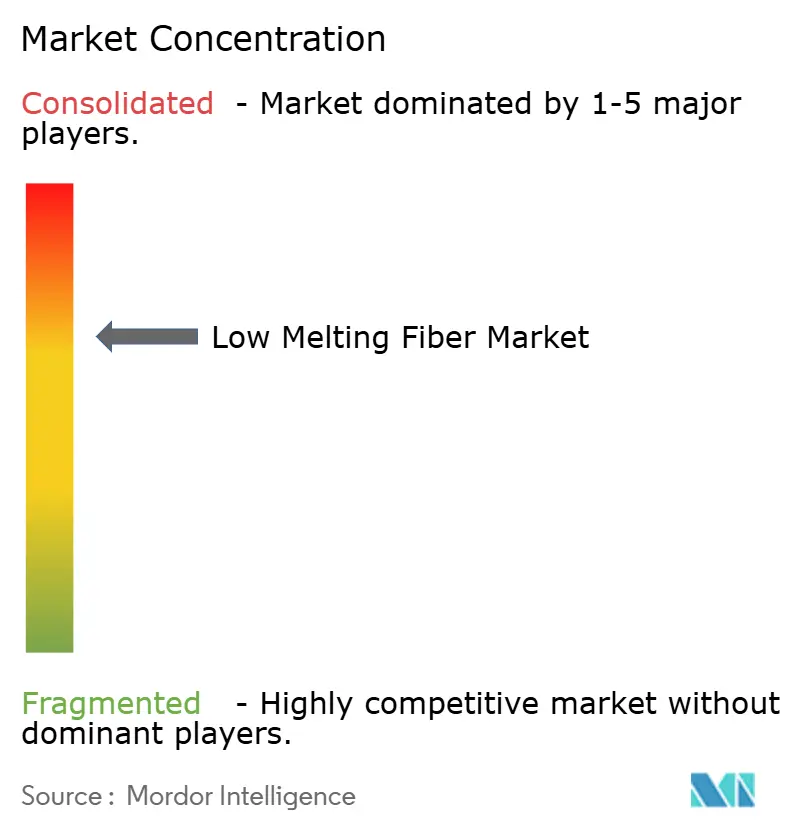

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Melting Fiber Market Analysis by Mordor Intelligence

The Low Melting Fiber Market size is expected to grow from USD 2.36 billion in 2025 to USD 2.52 billion in 2026 and is forecast to reach USD 3.46 billion by 2031 at 6.57% CAGR over 2026-2031. In Vietnam and Thailand, the expansion of mattress manufacturing hubs is driving growth. Electric-vehicle battery packs are undergoing acoustic insulation retrofits, while functional sportswear supply chains are adopting solvent-free lamination lines. Islands-in-sea fiber architectures are reshaping lightweight composites, and bio-based sheath polymers are paving the way for compostable hygiene products. Chemically recycled PET feedstocks are providing a buffer against fluctuations in crude-oil prices. Regulatory changes, such as U.S. antidumping duties on low-melt PSF from Korea and Taiwan, and the European Union's plastic-pellet-loss rule, are increasing compliance costs. However, these changes are advantageous for integrated producers with upstream containment assets. Feedstock volatility remains a significant concern; recent spikes in PTA and MEG prices have compressed melt margins. In response, producers are diversifying their sourcing, securing forward contracts, and co-investing in depolymerization ventures to ensure a steady supply of recycled inputs.

Key Report Takeaways

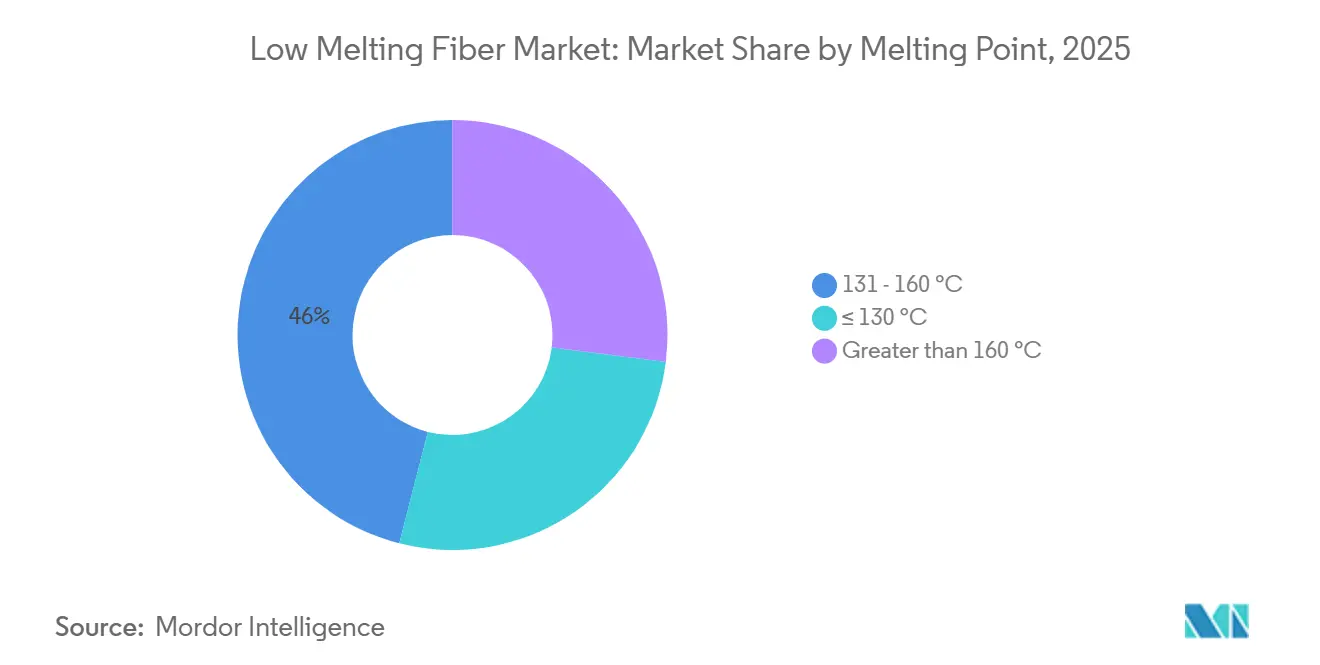

- By melting point, 131–160 °C grades led with 46.02% of the Low Melting Fiber market share in 2025, while ≤130 °C grades are projected to expand at a 6.72% CAGR from 2026 to 2031.

- By structure type, core-sheath fibers commanded 65.36% share in 2025; islands-in-sea architectures are expected to post a 6.88% CAGR over 2026-2031.

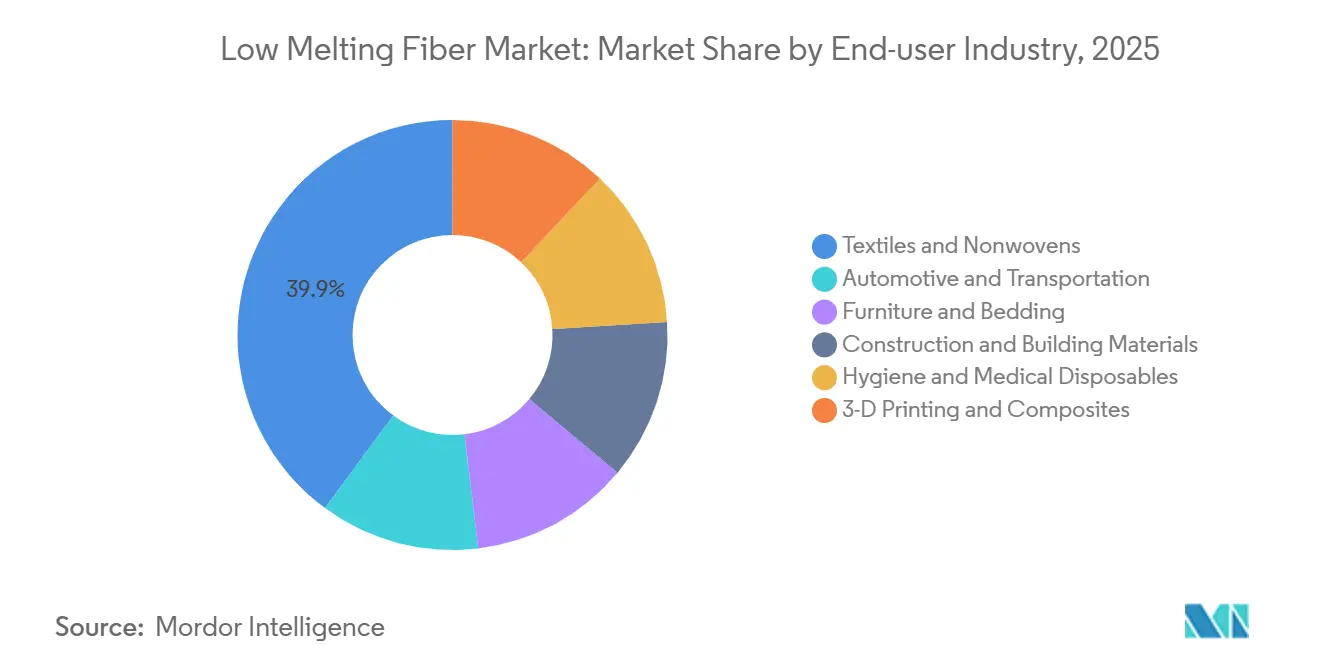

- By end-user industry, textiles and nonwovens absorbed 39.89% demand in 2025, whereas hygiene and medical disposables are forecast to grow at a 7.02% CAGR from 2026 to 2031.

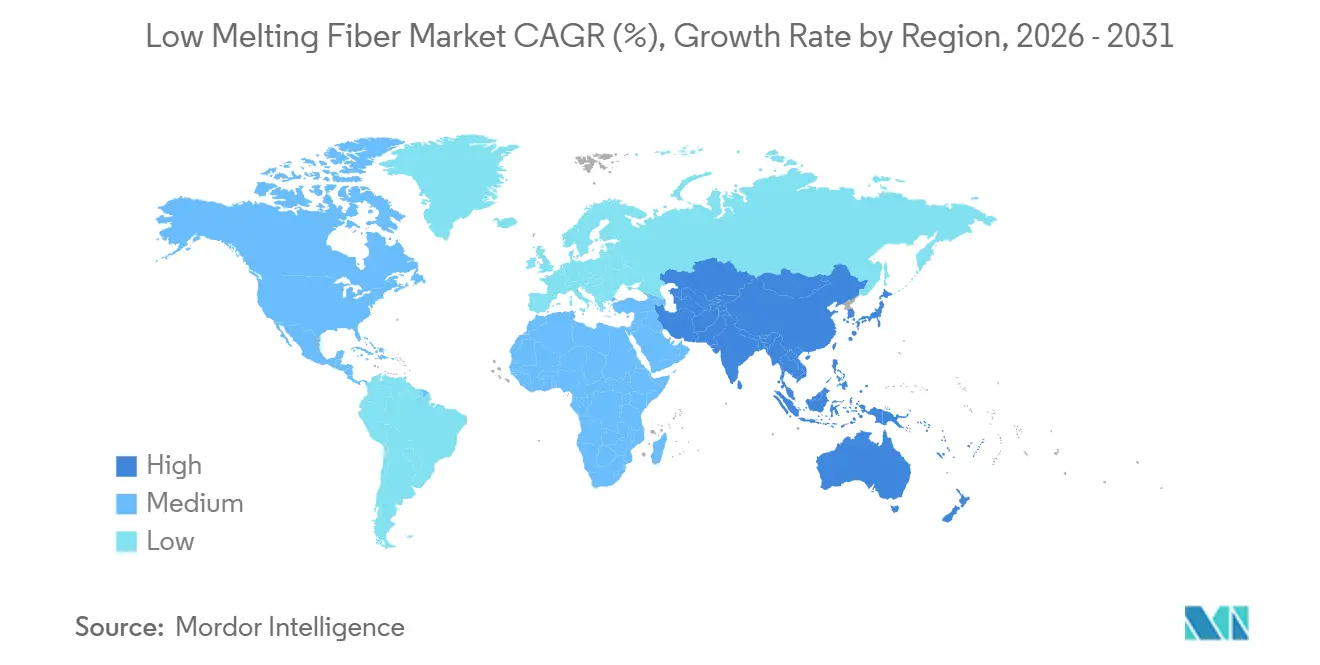

- By geography, Asia-Pacific captured 51.37% revenue share in 2025, and the region is set to advance at a 6.77% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low Melting Fiber Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for eco-friendly and sustainable thermal-bond fibers | +1.2% | Global, with early adoption in the EU and North America | Medium term (2–4 years) |

| Expansion of mattress and bedding manufacturing footprints | +0.9% | Asia-Pacific core (Vietnam, Thailand, China), spill-over to South America | Short term (≤2 years) |

| Growth in automotive acoustic and thermal-insulation applications | +1.4% | Global, concentrated in APAC (China, Japan, South Korea) and North America | Medium term (2–4 years) |

| Shift toward solvent-free hot-melt lamination in functional sportswear | +0.8% | Global, led by the EU and North America, brands sourcing from ASEAN | Short term (≤2 years) |

| Emergence of 3D-printed fiber preforms for lightweight composites | +0.5% | North America and EU (aerospace, automotive R&D hubs) | Long term (≥4 years) |

| Surging interest in biodegradable LMF grades for EV-battery thermal pads | +0.7% | APAC (China, Japan, South Korea) and the EU | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Eco-Friendly and Sustainable Thermal-Bond Fibers

Brand commitments to carbon reduction have accelerated the shift from virgin polyester to both chemically recycled and plant-based alternatives. Indorama Ventures and Jiaren Chemical Recycling have been producing textile-recycled PET that maintains virgin-grade molecular weight, allowing for a low-melt bicomponent extrusion without compromising strength[1]Indorama Ventures, “Fibers business and Jiaren Chemical Recycling form joint venture,” indoramaventures.com. Fiberpartner’s PolyPlant BICO, a bicomponent fiber with a 130 °C sheath made from PLA, boasts 100% bio-based thermal bonding. It meets the OEKO-TEX Class 1 Annex 6 standard and is aimed at hygiene products, where compostability and skin safety are paramount. The EU's Circular Textiles Strategy mandates ecodesign regulations and digital passports, pushing demand toward suppliers with the ISCC Plus mass-balance certification[2]European Commission, “EU Strategy for Sustainable and Circular Textiles,” europa.eu. Oriental Shenghong, with its recycled-polyester unit and a direct-spinning method from bottle to yarn, has emerged as a traceable, low-carbon feedstock provider. Its specialty grades cater to renowned brands such as Nike and Uniqlo.

Expansion of Mattress and Bedding Manufacturing Footprints

In a bid to evade U.S. Section 301 tariffs, mattress orders that once headed to China are now finding their way to factories in Vietnam and Thailand. This pivot has spurred a surge in demand for low-melt PSF in the region, a material frequently utilized in quilted covers and as filling for pillows. In a calculated maneuver, PVChem inked a pact in July 2025 with VNPOLY, directing recycled PET chips into the country's POY production lines. This effort is further strengthened by an upcoming bottle-recycling facility in Nghi Son, boasting a significant capacity, set to commence operations later this year. This integrated approach significantly reduces Vietnam's long-standing reliance on imported staple fiber, a dependency that was once pronounced. Additionally, mattress OEMs are now prioritizing shorter lead times and flexible denier counts. This evolution has created opportunities for local converters, enabling them to compete successfully by providing shipping costs that are lower than those of their Chinese rivals.

Growth in Automotive Acoustic and Thermal-Insulation Applications

Recent trials revealed that aerogel-fiber composites, using low-melt PET binders, excelled in conductivity and surpassed other materials in sound absorption. Electric vehicle battery packs now demand insulation capable of enduring temperatures over 800 °C, all while maintaining a weight under 1.5 kg/m². In 2025, Indorama Ventures unveiled its Reicofil high-loft bicomponent line in Mocksville, United States, producing ultra-soft automotive interiors that meet noise-reduction benchmarks. The market is now categorizing fibers by their applications: the cabin, under-hood, and battery zones. Grades rated for temperatures up to 130 °C are confined to interiors, while the demand for high-temperature applications has shifted toward ceramic and basalt solutions.

Shift Toward Solvent-Free Hot-Melt Lamination in Functional Sportswear

Outdoor brands are phasing out solvent adhesives in response to enforced VOC caps. SikaMelt 600, a polyurethane hot melt, bonds at temperatures between 110 and 140 °C. It not only bonds breathable membranes but also adheres to Bluesign limits. Collano adhesives, activating at 80 °C, bond with aramid and UHMWPE fabrics, maintaining stability up to 230 °C. This stability feature facilitates energy-efficient lamination on sensitive substrates. In Vietnam, integrated knit-to-laminate plants have adopted solvent-free lines, catering to major brands such as Nike and The North Face. However, the premium price of bio-PU presents challenges for its widespread adoption in the mass-market apparel industry. Indorama Ventures, signaling a significant industry shift, partnered with a consortium to supply CO₂-based para-xylene fibers to The North Face in Japan, emphasizing a commitment to verified low-carbon inputs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs and PTA/MEG feedstock volatility | -1.1% | Global, acute in South Asia and China | Short term (≤2 years) |

| Intense competition from conventional binders (adhesive powders, PP fibers) | -0.6% | Global, concentrated in cost-sensitive hygiene and construction segments | Medium term (2–4 years) |

| Microplastic shedding restrictions on synthetic nonwovens (EU proposal) | -0.4% | EU, potential spill-over to North America and APAC | Long term (≥4 years) |

| US anti-dumping duties on Korean and Taiwanese low-melt PSF | -0.5% | North America, indirect impact on global pricing | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Production Costs and PTA/MEG Feedstock Volatility

In March 2026, the prices of PTA and MEG in India surged before declining. This fluctuation compelled filament makers to increase their prices. A tightening in spot MEG availability emerged as Middle-East supply lines faced delays, while Chinese producers prioritized domestic demands. In commoditized segments, buyers shift to polypropylene when polyester premiums exceed a specific threshold, reducing the pass-through effect. Although Chinese semi-depolymerization projects promise significant energy savings, their high capital requirements limit immediate implementation.

Intense Competition from Conventional Binders and U.S. Duties

Budget diapers and construction panels are increasingly opting for adhesive powders and PVA binders as cost-effective sticking solutions. In the United States, the authorities have imposed antidumping duties on low-melt PSF imports from Korea, while imports from other countries face even steeper rates. This pricing strategy is encouraging buyers to shift toward domestic sources or those aligned with the USMCA agreement. Concurrently, synthetic fiber manufacturers in the European Union are preparing for potential design changes and mandatory factory pre-washing, as the bloc's draft microplastic regulations have increased their production costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Melting Point: Mid-Range Grades Balance Processability and Stability

In 2025, the market saw the 131-160 °C band dominate, capturing 46.02% of the demand. Its appeal was largely due to its smooth flow during calendering and its resilience in Asia-Pacific warehouses, where it avoided sticking. Ultra-low-melt grades, set at or below 130 °C, are projected to expand at a 6.72% CAGR during the forecast period of 2026–2031. Their rising popularity is attributed to their pivotal role in PLA-based fibers, ensuring seamless bonding for hygiene pads and compostable mailers. In contrast, high-melt grades, surpassing 160 °C, are primarily used in melt-blown filter media and select under-hood components. However, they are losing market share to ceramic fibers, particularly in battery-adjacent applications. The market for low-melting fibers, especially in the mid-range band, is poised for significant growth. With the European Union's pellet-loss regulations taking effect in December 2025, major plants are now adopting dust capture systems. This transition favors integrated players with on-site containment solutions. In a calculated move, Far Eastern New Century is channeling investments into boosting elastic recovery at low-melt points, targeting the lucrative margins in sportswear and compression hosiery.

Emerging trends underscore a heightened focus on recycling; circular-design invoices now highlight melt temperatures, streamlining future separations. In Europe, discerning core buyers are willing to pay a premium for mid-range fiber lots accompanied by a "passport" – a quality assurance – over those from unverified sources.

By Structure Type: Islands-in-Sea Architectures Gain Pace in Composites

In 2025, core-sheath lines, attuned to cards, air-through ovens, and lamination towers, captured a commanding 65.36% market share. Meanwhile, output from islands-in-sea is projected to grow at a 6.88% CAGR during the forecast period of 2026–2031, driven by the aerospace industry's shift toward ultrafine microfibers for their suede-like panels. Toray's Alcantara, utilizing sea-island conjugate spinning, effectively dissolves the "sea" polymer, revealing micro-filaments that are half the width of a human hair. This advanced innovation commands a premium in the luxury car market. Although the capital-intensive nature and complex spinneret designs create barriers for new entrants, the increased surface area in natural-fiber composites enhances resin wet-out, significantly reducing environmental impact. The market for Low Melting Fiber, with a specific focus on islands-in-sea fibers, is expected to expand. Additionally, Indorama Ventures' 2025 investment in U.S. high-loft underscores the commitment of established players to increase core-sheath capacity, particularly for hygiene fluff, which is currently operating at over 85% utilization.

By End-User Industry: Hygiene and Medical Disposables Lead Growth

In 2025, the demand for textiles and nonwovens, primarily quilted fillers, wipe substrates, and diaper cores, accounted for 39.89% of the market. Hygiene and medical disposables, driven by aging demographics in Japan and South Korea and pandemic-driven mandates for single-use items, are projected to experience the fastest growth, with a CAGR of 7.02% during the forecast period of 2026–2031. PLA staple fiber, known for its adhesive-free bonding and compliance with skin testing, has been incorporated into diaper topsheets. While automotive interior liners continue to grow steadily, they are losing a portion of their high-temperature market share to basalt mats, particularly those used near EV batteries. In the Asia-Pacific region, the local demand for PSF, primarily for furniture and bedding applications, is surging and is further supported by tariff diversions from China. Although construction insulation remains a niche market, it is notable that mineral wool outperforms polyester in both R-value and fire ratings, all while maintaining a comparable cost.

Geography Analysis

In 2025, the Asia-Pacific region dominated the Low Melting Fiber market, capturing a substantial 51.37% share. Projections indicate the region will sustain a robust 6.77% CAGR through the forecast period of 2026–2031. China, anchored at the forefront, boasts significant filament lines at Oriental Shenghong. Starting in Q4 2026, Vietnam’s Nghi Son rPET complex will bolster local supply loops by providing recycled chips to VNPOLY POY extruders. Even with feedstock price fluctuations in March 2026 leading to price hikes in India, the annual demand remains strong, attracting new players to the low-melt market.

North America finds itself contending with antidumping levies, specifically duties on imports of Korean PSF. Consequently, buyers are pivoting towards domestic U.S. production and converters in Mexico. Indorama Ventures’ Mocksville line not only streamlines transit times for hygiene OEMs but also secures a position in the automotive interior sector.

Europe is preparing for a December 2025 deadline, focusing on pellet-loss compliance and the rollout of digital passports that require melt-point disclosures. Both Germany and Italy are showing a willingness to pay a premium for ISCC-certified, chemically recycled low-melt products. While South America and the Middle-East and Africa play relatively minor roles, Brazil's expanding footprint in hygiene pads and Saudi Arabia's significant infrastructure investments are driving demand for carpet backings and HVAC insulation.

Competitive Landscape

The low-melting fiber market is moderately consolidated. Indorama Ventures, via its depolymerization joint venture, secured a commitment for recycled PET feedstock, aligning with apparel brands targeting Scope 3 emissions-reductions. In the meantime, niche players eSUN and Fiberpartner, focusing on biodegradable PLA fibers, are successfully commanding price premiums in the hygiene and compostable packaging markets.

Establishing a greenfield bicomponent line requires significant capital and can face OEM approval delays of up to 36 months, complicating swift market entry. However, competition is intensifying: sustainable adhesive chemistries, capable of achieving lap-shear strength on steel and offering catalytic recyclability, threaten to overshadow thermal-bond fibers in specific electronics encapsulation niches.

Low Melting Fiber Industry Leaders

Sichuan Huvis

Toray Advanced Materials Korea

NAN YA PLASTICS CORPORATION

Far Eastern New Century Corporation

Taekwang Industrial Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Huvis introduced an eco-friendly low melting fiber for sustainable textiles. The company developed this fiber as part of its environmental sustainability initiatives in textile manufacturing.

- August 2024: UNIFI, Inc. expanded its REPREVE portfolio with two new textile waste-based products using low melt fiber: a white-dyeable filament yarn and ThermaLoop insulation material. This development aligns with UNIFI's strategy to advance textile-to-textile recycling and circular manufacturing solutions.

Global Low Melting Fiber Market Report Scope

Low-melting fiber is defined as a specialized bicomponent synthetic fiber that functions as a thermal binder. It melts at lower temperatures to fuse with other fibers, such as standard PET, without requiring adhesives. Low-melting fiber offers high bonding strength, elasticity, and dimensional stability, enabling an eco-friendly, glue-free manufacturing process for nonwovens and composites.

The market is segmented by melting point, structure type, end-user industry, and geography. By melting point, the market is segmented into ≤ 130 °C, 131 - 160 °C, and greater than 160 °C. By structure type, the market is segmented into core-sheath, side-by-side, and islands-in-sea. By end-user industry, the market is segmented into textiles and nonwovens, automotive and transportation, furniture and bedding, construction and building materials, hygiene and medical disposables, and 3-D printing and composites. The report also covers the market size and forecasts for the market in 19 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| ≤ 130 °C |

| 131 - 160 °C |

| Greater than 160 °C |

| Core-Sheath |

| Side-by-Side |

| Islands-in-Sea |

| Textiles and Nonwovens |

| Automotive and Transportation |

| Furniture and Bedding |

| Construction and Building Materials |

| Hygiene and Medical Disposables |

| 3-D Printing and Composites |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Melting Point | ≤ 130 °C | |

| 131 - 160 °C | ||

| Greater than 160 °C | ||

| By Structure Type | Core-Sheath | |

| Side-by-Side | ||

| Islands-in-Sea | ||

| By End-user Industry | Textiles and Nonwovens | |

| Automotive and Transportation | ||

| Furniture and Bedding | ||

| Construction and Building Materials | ||

| Hygiene and Medical Disposables | ||

| 3-D Printing and Composites | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast CAGR for Low Melting Fiber between 2026 and 2031?

The market is forecast to rise from USD 2.52 billion in 2026 to USD 3.46 billion by 2031, reflecting a 6.57% CAGR.

Which region holds the largest Low Melting Fiber demand?

Asia-Pacific accounted for 51.37% of 2025 revenue and remains the fastest-expanding region, registering a CAGR of 6.77% from 2026 to 2031.

Which melting-point segment dominates Low Melting Fiber sales?

Grades in the 131-160 °C range held 46.02% share in 2025 because they balance processing ease and stability.

Why are hygiene and medical disposables a key growth area?

Aging populations in Japan and South Korea and post-pandemic safety norms are driving a 7.02% CAGR in this segment from 2026 to 2031.

Page last updated on: