Lyocell Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

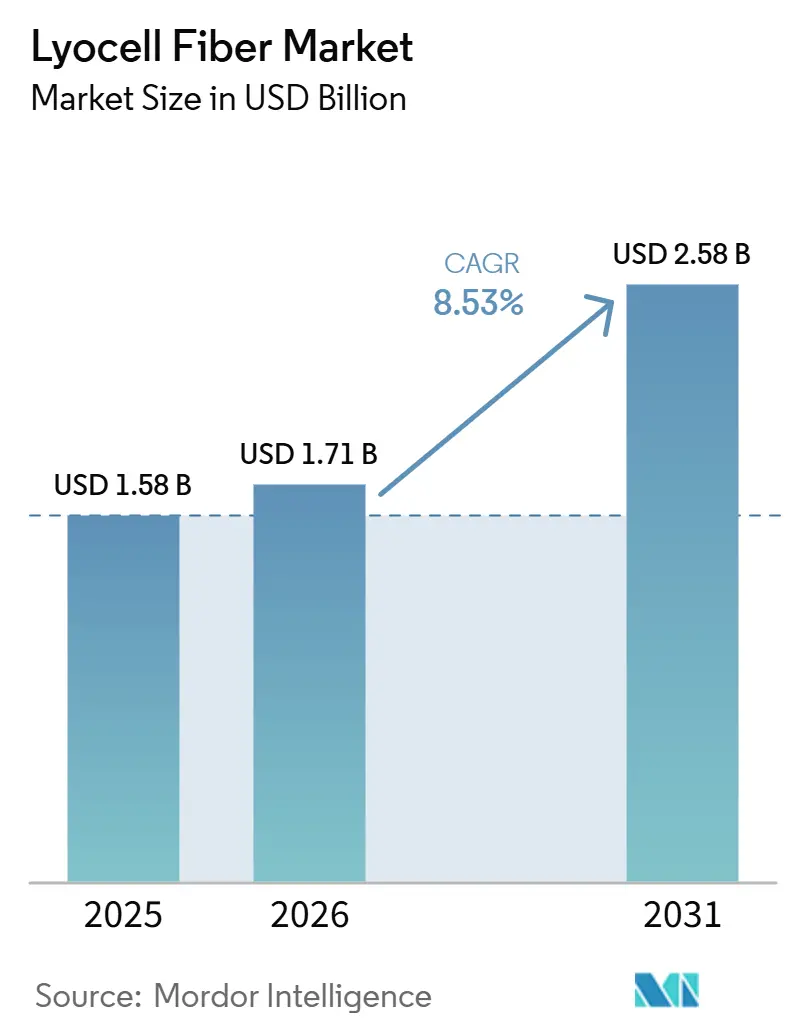

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.58 Billion |

| Growth Rate (2026 - 2031) | 8.53% CAGR |

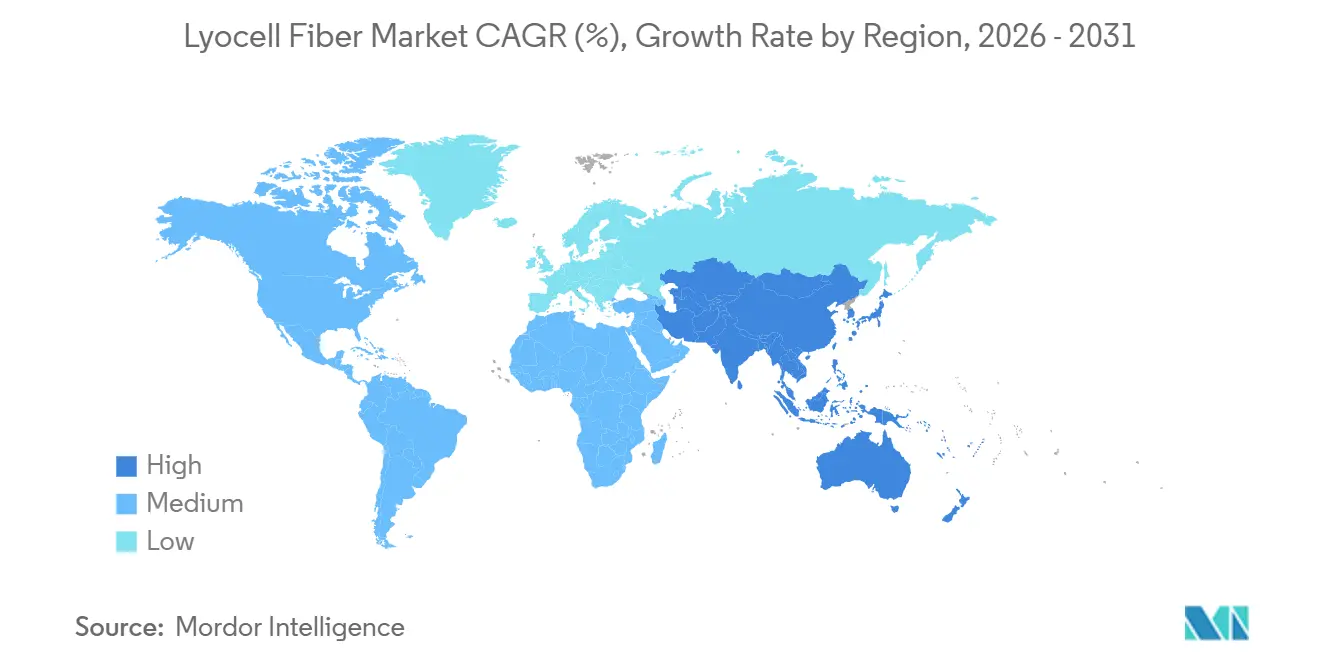

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lyocell Fiber Market Analysis by Mordor Intelligence

The Lyocell Fiber Market size is expected to increase from USD 1.58 billion in 2025 to USD 1.71 billion in 2026 and reach USD 2.58 billion by 2031, growing at a CAGR of 8.53% over 2026-2031. Demand is rising as fashion and hygiene brands transition from petroleum-based synthetics and water-intensive cotton to closed-loop cellulosic fibers. At the same time, carbon-border regulations and extended-producer-responsibility schemes are providing financial incentives for adopting low-impact materials. Staple lyocell continues to lead in volume, but filament grades are growing rapidly as activewear, medical nonwovens, and technical applications demand moisture management and high tensile strength. Asia-Pacific remains the leader in capacity and exports due to significant investments in China, while Europe and North America drive premium demand through strict sustainability standards. Producers that integrate scale, vertical pulp operations, and advanced recycling technologies are achieving cost advantages and stronger margins.

Key Report Takeaways

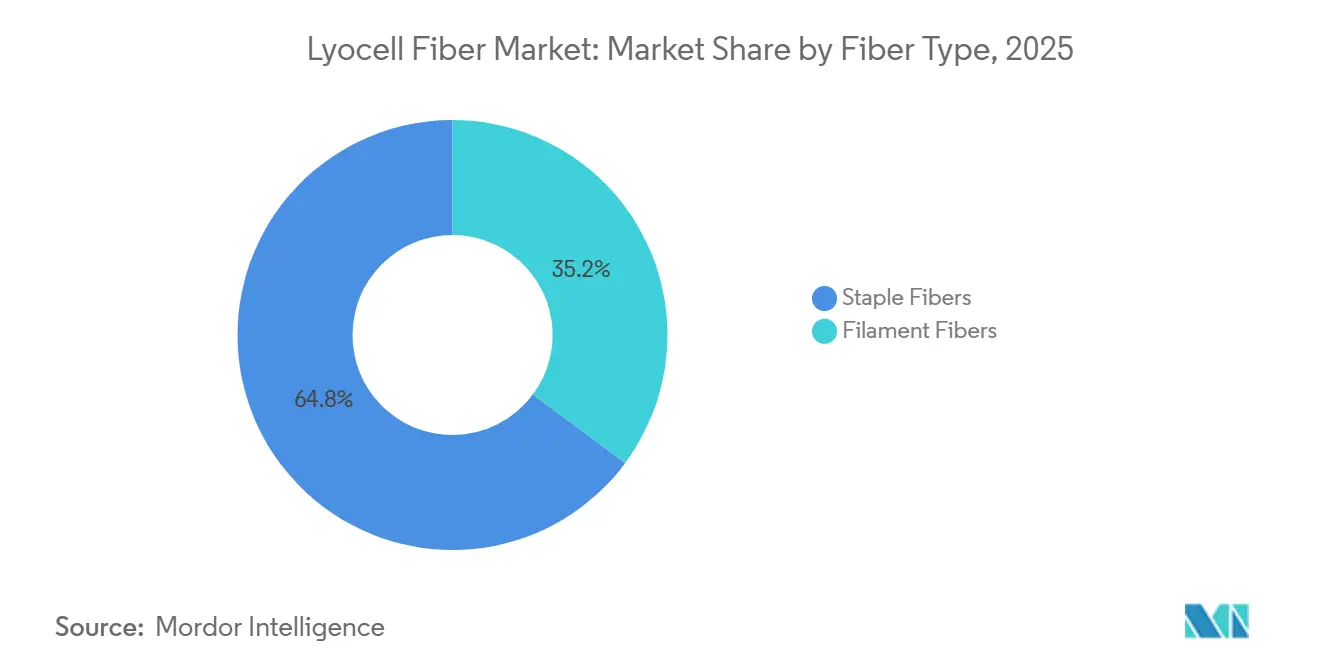

- By fiber type, staple fibers held 64.84% of the lyocell fiber market share in 2025, whereas filament fibers are projected to grow at a 9.02% CAGR through 2031.

- By process type, conventional lyocell captured 78.78% of the lyocell fiber market share in 2025, while closed-loop/next-gen lyocell is advancing at a 9.30% CAGR through 2031.

- By application, apparel led with 59.68% of the lyocell fiber market share in 2025, while medical and hygiene products are forecast to post the fastest growth at a 9.80% CAGR through 2031.

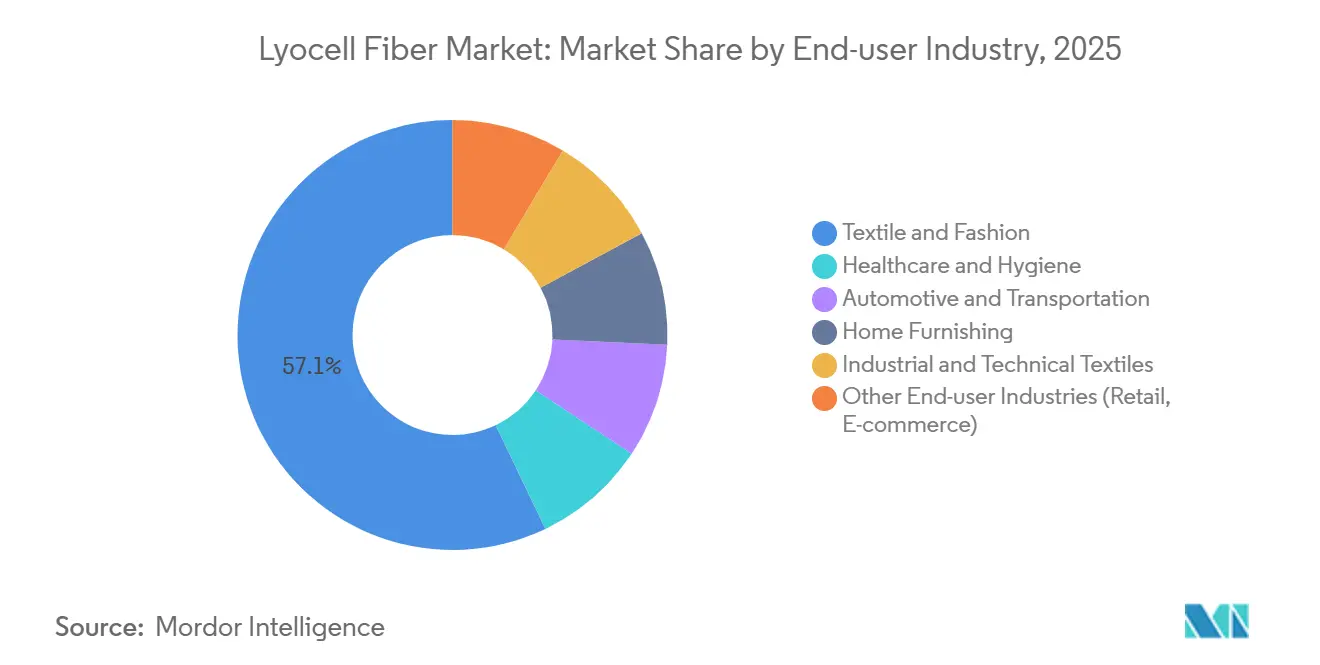

- By end-user industry, textile and fashion led with 57.11% of the lyocell fiber market share in 2025, while healthcare and hygiene is forecast to post the fastest growth at a 10.03% CAGR through 2031.

- By geography, Asia-Pacific accounted for 45.59% of the lyocell fiber market share in 2025 and is on track for a 9.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lyocell Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for sustainable and biodegradable fibers | +1.8% | Global, with peak adoption in Europe and North America | Medium term (2-4 years) |

| Increasing usage in apparel and home textiles | +1.5% | Asia-Pacific core, spillover to Europe and North America | Short term (≤ 2 years) |

| Expansion of eco-friendly collections by fashion brands | +1.2% | Europe and North America, expanding to Asia-Pacific | Medium term (2-4 years) |

| High moisture-absorption and strength enabling performance wear | +0.9% | North America and Europe for activewear; Asia-Pacific for technical textiles | Medium term (2-4 years) |

| Carbon-border taxes accelerating low-impact fibers | +1.0% | Europe (CBAM implementation); potential spillover to North America and Asia-Pacific | Long term (≥ 4 years) |

| Textile-to-textile chemical recycling streams favoring lyocell | +1.3% | Europe and China leading; North America emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Sustainable and Biodegradable Fibers

Brands are increasingly promoting lyocell as a substitute for polyester, prioritizing its biodegradability and lower carbon footprint over cost concerns. Global retailers have pledged to transition to 100% preferred fibers by 2030, with in-house collections launched in 2025-2026, incorporating mechanically recovered cotton waste with virgin lyocell to meet circularity objectives. Independent laboratory studies published in 2025 revealed that 100% lyocell nonwovens disintegrated 83% within 35 days under aerobic soil conditions, achieving complete biodegradation in 55 days, significantly faster than cellulose acetate and recycled polyester. The European Union’s Single-Use Plastics Directive is driving consistent demand for plastic-free wipes, while life-cycle analyses show up to 42% lower cradle-to-gate CO₂ emissions compared to traditional spunlace formulations. These developments establish a stable demand base, protecting volumes from fluctuations in the apparel market.

Increasing Usage in Apparel and Home Textiles

Apparel and bedding remain the largest consumers of lyocell, but demand is shifting from premium linens to mass-market denim and casual basics. A slub-effect lyocell yarn, introduced in 2025, enables denim manufacturers to replicate the irregular textures associated with cotton while maintaining superior moisture management. Collaborations between bio-based elastane suppliers and lyocell producers resulted in active-stretch collections showcased at major trade shows in late 2025, signaling broader adoption in athleisure. Hospitality chains are specifying lyocell-rich sheets to enhance guest comfort, with internal audits reporting improved occupancy rates following bedding upgrades. The combination of comfort, aesthetics, and verified sustainability is enabling lyocell to penetrate price-sensitive mid-tier categories.

High Moisture-Absorption and Strength Enabling Performance Wear

Lyocell’s combination of tensile strength and moisture transport properties makes it a viable alternative to polyester and nylon in performance wear when blended with compatible biopolymers. In 2025, new products combining continuous-filament lyocell with biodegradable co-polyesters were launched, offering stretch and recovery without relying on petroleum-based spandex[1]Lenzing AG, “Product Portfolio – TENCEL,” Lenzing, lenzing.com. Laboratory tests confirmed that lyocell nonwovens match the tensile strength of recycled polyester in needle-punched structures, with thermal bonding further enhancing consolidation. The performance-wear segment is strategically important, as consumers replace activewear more frequently than casualwear, driving volume growth and supporting the expansion of the lyocell fiber market.

Carbon-Border Taxes Accelerating Low-Impact Fibers

The European Union’s Carbon Border Adjustment Mechanism (CBAM), which began phased enforcement in 2026, is expected to include textiles by 2028, increasing costs for coal-powered polyester imports. Scenario analyses suggest that carbon levies could raise landed costs for high-emission synthetic fabrics by up to 25%, reducing their price competitiveness. Lyocell suppliers highlight closed-loop recovery rates exceeding 99.8% and increasing reliance on renewable energy, positioning the fiber as CBAM-ready[2]European Commission, “Carbon Border Adjustment Mechanism Explained,” Europa, europa.eu. Brands with significant sourcing from Asia are already increasing lyocell orders to mitigate future compliance costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs vs. cotton and polyester | -1.1% | Global, with acute pressure in price-sensitive Asia-Pacific markets | Short term (≤ 2 years) |

| Complex chemical recovery and manufacturing process | -0.6% | Emerging markets lacking technical expertise; limited impact in established hubs | Medium term (2-4 years) |

| Competition from other regenerated cellulose fibers | -0.5% | Asia-Pacific and Europe where viscose/modal capacity is high | Short term (≤ 2 years) |

| Volatile dissolving-pulp supply due to biorefinery demand | -0.9% | Global, with acute impact in regions reliant on imported pulp (Asia-Pacific, North America) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Production Costs vs. Cotton and Polyester

Establishing a greenfield lyocell facility requires an investment of approximately USD 300 million, which is double the cost of viscose and four times that of polyester on a per-ton basis. The need for solvent recovery systems and high-purity N-methylmorpholine N-oxide (NMMO) increases operational expenses. Additionally, energy price spikes in Europe eroded margins, leading to the insolvency of a specialty fiber mill in 2024. Without carbon pricing to account for environmental externalities, lyocell faces challenges in displacing polyester in price-sensitive segments, limiting its short-term market penetration.

Complex Chemical Recovery and Manufacturing Process

Lyocell production requires precise solvent management to achieve recovery rates exceeding 99% for NMMO. Emerging markets often lack the necessary engineering expertise and wastewater infrastructure for safe operations, increasing compliance risks. The high capital investment required for closed-loop technology deters smaller entrants, with most capacity expansions occurring in China, where engineering capabilities and government incentives align to support growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fiber Type: Staple Strength with Emerging Filament Upside

Staple fibers accounted for 64.84% of the lyocell fiber market share in 2025, primarily due to their compatibility with cotton-spinning systems and widespread application in apparel, bed linens, and wipes. Filament fibers are projected to grow at a 9.02% CAGR through 2031, surpassing staple fibers in growth rate, as they are valued in sportswear and technical textiles for their pilling resistance and sheen.

Staple fibers are expected to maintain revenue leadership as mills can blend them with cotton or recycled polyester without requiring new equipment. However, continuous filament lyocell commands higher prices in luxury apparel and automotive interiors, indicating a shift in value even as tonnage growth remains slower. Producers capable of supplying both formats can maximize profitability and mitigate risks associated with commoditization in staple grades.

By Process Type: Closed-Loop Economics Take Center Stage

Conventional lyocell held a 78.78% revenue share in 2025, while closed-loop or next-generation lyocell is anticipated to grow at a 9.30% CAGR through 2031. Facilities recovering over 99.8% of solvents reduce operating costs by approximately 10% and provide verified low-carbon credentials, making them preferred by leading apparel brands.

Chemical recycling now integrates 30% recycled pulp into new lyocell production lines, reducing wood demand and aligning with proposed recycled-content quotas in Europe. Producers delaying investment in these technologies risk margin pressures as buyers increasingly prefer mills offering recycled-content products with traceable supply chains.

By Application: Hygiene Surges Ahead of Apparel

Apparel accounted for 59.68% of revenue in 2025, but medical and hygiene applications are projected to grow at a 9.80% CAGR through 2031. Legislative bans on plastic-based wipes and the demand for skin-friendly fibers are driving nonwoven mills to adopt lyocell blends that disperse in wastewater and biodegrade in soil.

The market for lyocell fibers in hygiene applications is expected to grow steadily as fine-denier "Dry" variants gain traction in diapers and feminine hygiene products. While apparel applications will continue to grow, their pace will be slower due to the cost competitiveness of cotton and the dominance of polyester in fast-fashion basics, barring the introduction of carbon surcharges.

By End-user Industry: Healthcare and Hygiene Lead Growth

The textile and fashion industry held a 57.11% market share in 2025, but healthcare and hygiene applications are forecast to grow at a 10.03% CAGR through 2031. European hospitals are increasingly specifying biodegradable drapes and wipes, while multinational consumer goods companies introduced compostable baby wipes in 2025 using lyocell blends.

Automotive and industrial applications are also expanding as OEMs seek lighter, sustainable materials. The lyocell fiber market could benefit further if suppliers secure flame-retardant and abrasion-resistant certifications, enabling access to premium, long-term contracts in these sectors.

Geography Analysis

Asia-Pacific dominated with 45.59% share in 2025 and is forecast to rise at a 9.67% CAGR through 2031. China is adding a 600,000 tpa plant, which will further boost its exports. Domestic operating rates of approximately 85% in 2024 indicate healthy utilization, while export growth of 48.7% between January and November 2025 highlights cost competitiveness compared to European mills.

Europe consumes premium lyocell because of strict eco-design rules, but is losing production capacity after a German specialty mill announced closure by March 2026. The gap invites Asian suppliers to capture higher-margin European demand, provided they document low carbon footprints to satisfy CBAM audits.

North America represents roughly one-quarter of global consumption yet relies heavily on imports. California's producer-responsibility law, effective July 2026, and state-level chemical restrictions are encouraging retailers to shift toward biodegradable fibers, supporting stable demand growth despite limited domestic supply.

South America and the Middle-East and Africa remain small but show double-digit growth potential. Brazil's eucalyptus feedstock advantage could attract future downstream investments, while Turkish mills are incorporating lyocell into export-oriented apparel to meet European sustainability requirements.

Competitive Landscape

The top five suppliers controlled the majority of global capacity in 2025, indicating a moderately concentrated market. However, technological advancements are driving significant disruption. Leading companies are pursuing large-scale projects to reduce unit costs, while challengers focus on recycled feedstock and innovative solvents.

One major producer commissioned twin 75,000 tpa lines in 2025, increasing its total capacity to 400,000 tpa. Another company opened a cotton-waste pulp mill in 2024 and plans to scale to 60,000 tpa by 2027, aiming to offer recycled-content lyocell at prices below virgin pulp grades. European incumbent Lenzing is differentiating through product innovation, including slub-effect yarns for denim, hydrophobic grades for diapers, and acquiring majority control of a next-generation cellulose technology firm in 2026.

Entry barriers are increasing due to the high capital requirements of closed-loop plants, which need sophisticated solvent recovery systems and investments exceeding USD 300 million. Rising energy costs and competition from low-cost Asian producers have already forced one European specialty mill into insolvency, suggesting further consolidation as inefficient assets exit the market.

Lyocell Fiber Industry Leaders

Aditya Birla Yarn

Lenzing AG

Sateri

Tangshan Sanyou Xingda Chemical Fiber Co., Ltd.

Kelheim Fibres GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lenzing AG expanded the production of VEOCEL lyocell fibers at its Prachinburi, Thailand, facility. This marked the first instance of producing nonwoven-grade fibers in Asia, enabling the production of specialty nonwoven-grade fibers specifically for the Asian market.

- October 2025: Lenzing AG introduced TENCEL Lyocell - HV100 featuring Variocut technology, which enabled controlled variations in fiber length (10–28 mm) within the bale. This deliberate variation produced a unique, irregular texture similar to natural fibers such as cotton or linen.

Global Lyocell Fiber Market Report Scope

Lyocell is a sustainable, semi-synthetic cellulose fiber produced from wood pulp, commonly eucalyptus, through a closed-loop solvent spinning process that minimizes environmental impact. It is valued for its softness, breathability, strength, and biodegradability, making it a popular choice for clothing and bedding. With its high moisture absorption, lyocell is often regarded as an environmentally friendly alternative to cotton or conventional rayon.

The Lyocell Fiber Market is segmented into fiber type, process type, application, end-user industry, and geography. By fiber type, the market is segmented into staple fibers and filament fibers. By process type, the market is segmented into conventional lyocell and closed-loop/next-gen lyocell. By application, the market is segmented into apparel, home textiles, medical and hygiene products, industrial, and other applications (packaging, personal care). By end-user industry, the market is segmented into textile and fashion, healthcare and hygiene, automotive and transportation, home furnishing, industrial and technical textiles, and other end-user industries (retail, e-commerce). The report also covers the market size and forecasts for lyocell fiber in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Staple Fibers |

| Filament Fibers |

| Conventional Lyocell |

| Closed-loop/Next-gen Lyocell |

| Apparel |

| Home Textiles |

| Medical and Hygiene Products |

| Industrial |

| Other Applications (Packaging, Personal Care) |

| Textile and Fashion |

| Healthcare and Hygiene |

| Automotive and Transportation |

| Home Furnishing |

| Industrial and Technical Textiles |

| Other End-user Industries (Retail, E-commerce) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Fiber Type | Staple Fibers | |

| Filament Fibers | ||

| By Process Type | Conventional Lyocell | |

| Closed-loop/Next-gen Lyocell | ||

| By Application | Apparel | |

| Home Textiles | ||

| Medical and Hygiene Products | ||

| Industrial | ||

| Other Applications (Packaging, Personal Care) | ||

| By End-user Industry | Textile and Fashion | |

| Healthcare and Hygiene | ||

| Automotive and Transportation | ||

| Home Furnishing | ||

| Industrial and Technical Textiles | ||

| Other End-user Industries (Retail, E-commerce) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the lyocell fiber market?

The lyocell fiber market size stands at USD 1.71 billion in 2026 and is forecast to reach USD 2.58 billion by 2031.

Which end-user industry is growing fastest?

The healthcare and hygiene industry is expected to expand at a 10.03% CAGR from 2026 to 2031.

Why did staple fibers dominate revenue in 2025?

Staple fibers integrate easily with existing cotton-spinning equipment, keeping conversion costs low.

How do closed-loop processes benefit Lyocell producers?

They recover more than 99.8% of solvent, cut operating costs by about 10%, and help brands meet circularity targets.

Page last updated on: