Bulletproof Glass Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

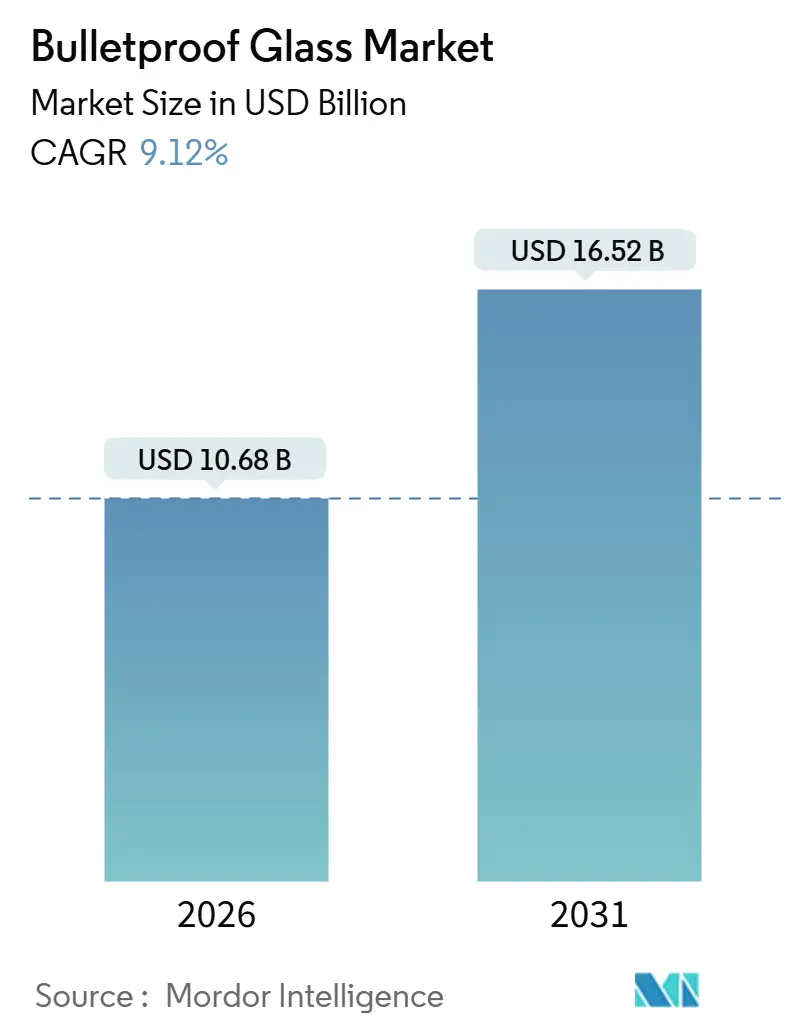

| Market Size (2026) | USD 10.68 Billion |

| Market Size (2031) | USD 16.52 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

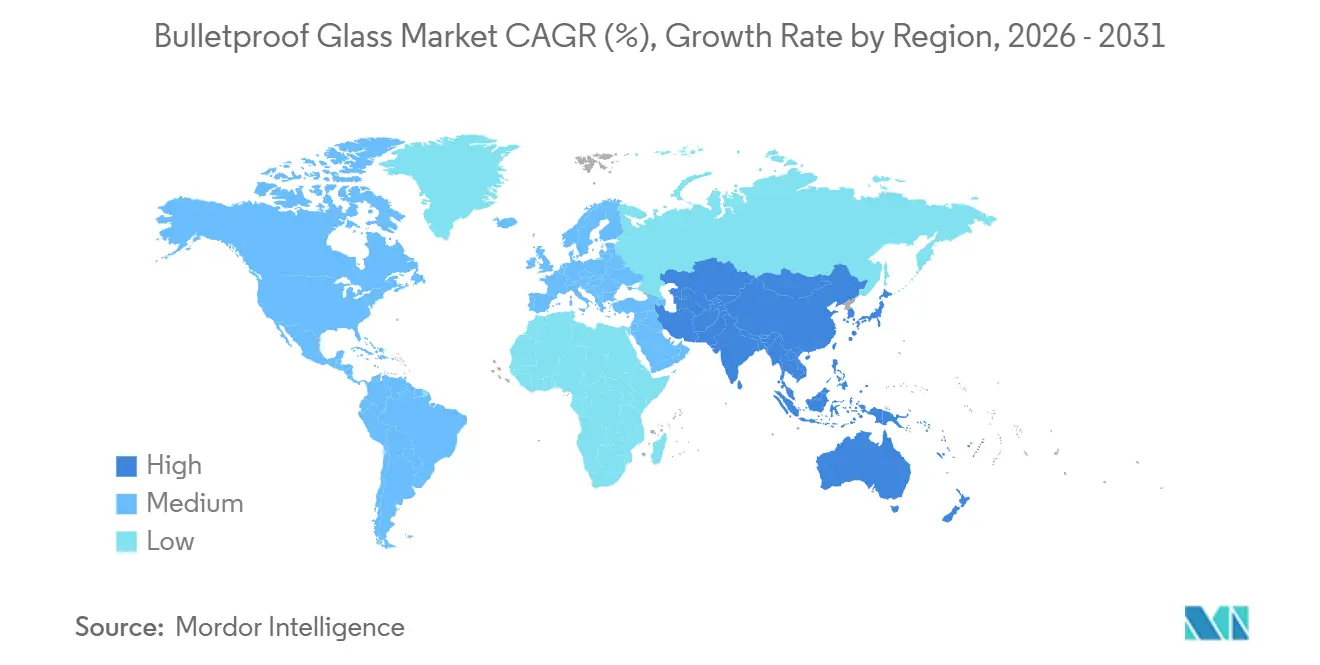

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bulletproof Glass Market Analysis by Mordor Intelligence

The Bulletproof Glass Market size is estimated at USD 10.68 billion in 2026, and is expected to reach USD 16.52 billion by 2031, at a CAGR of 9.12% during the forecast period (2026-2031). Rising defense modernization, climate-resilient construction mandates, and the electrification of armored vehicles are reinforcing demand, while polymer-ceramic hybrids promise meaningful weight savings. Solid acrylic dominated 2025 volumes because of its optical clarity and cost advantage, yet customer preference is shifting toward polycarbonate and glass-clad polycarbonate that deliver multi-hit protection with lighter laminates. Automakers are embedding ballistic glazing at the factory level to capture margin, and public-sector buyers are aligning safety and sustainability targets by specifying recycled-content laminates. The bulletproof glass market is therefore transitioning from reactive procurement toward proactive infrastructure hardening and mobility integration.

Key Report Takeaways

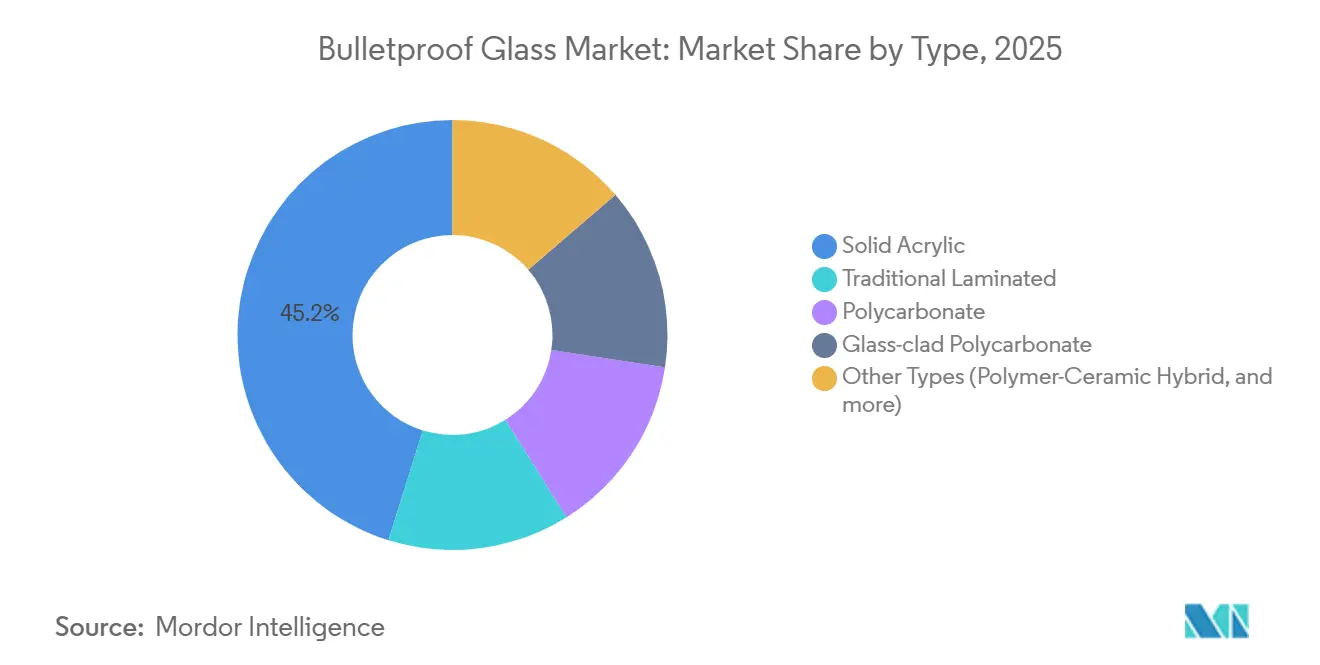

- By type, Solid Acrylic led with 45.19% of the bulletproof glass market share in 2025, while Polycarbonate is forecast to expand at a 10.21% CAGR to 2031.

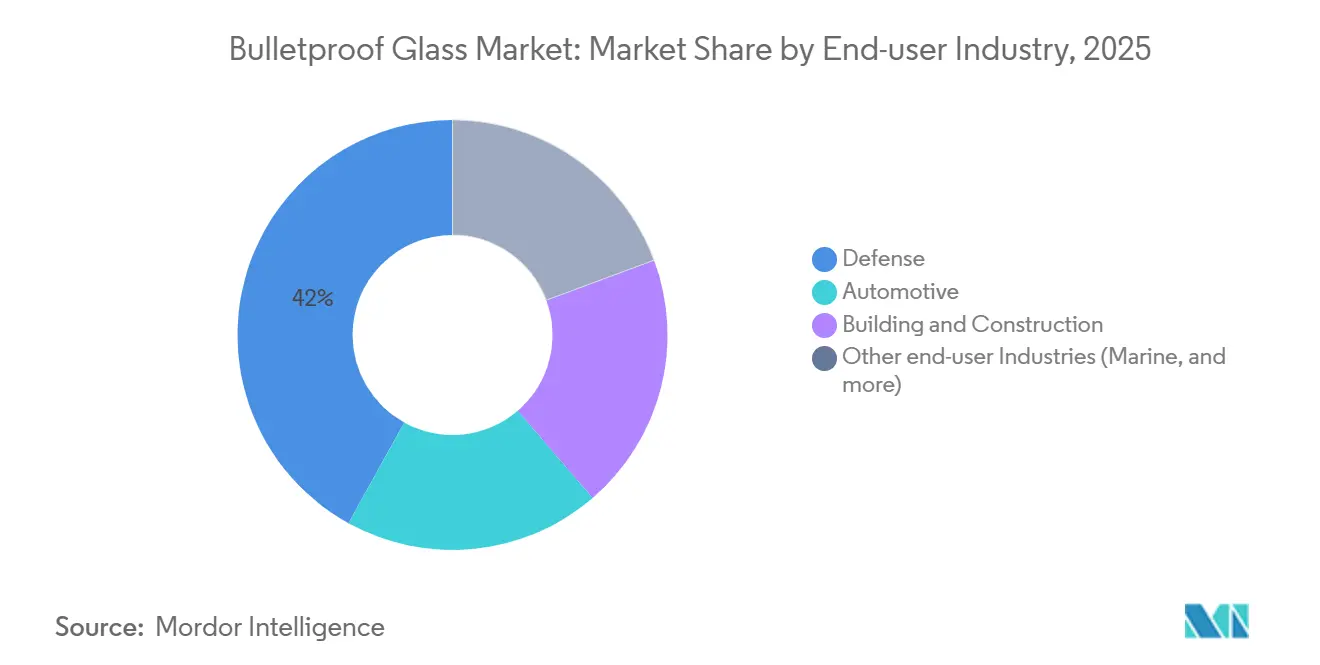

- By end-user industry, the Defense segment held 41.97% of the bulletproof glass market share in 2025, whereas the Automotive segment records the fastest CAGR at 11.92% through 2031.

- By geography, North America accounted for 39.18% of the bulletproof glass market size in 2025, yet Asia Pacific is projected to grow at a 12.17% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bulletproof Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global defense and homeland-security spending | +2.8% | North America, Europe, Middle East | Medium term (2-4 years) |

| Increasing infrastructure development in high-risk urban areas | +2.1% | China, India, Middle East, South America | Long term (≥ 4 years) |

| Growing utilization in luxury and armored vehicles | +1.9% | North America, Europe, Saudi Arabia, UAE | Short term (≤ 2 years) |

| Mandatory ballistic-facade codes in climate-resilient buildings | +1.5% | United States, Europe, China | Long term (≥ 4 years) |

| Rising demand for multi-threat transparent armor in electric public-transport fleets | +0.9% | China, India, United States | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Defense and Homeland-Security Spending

Transparent-armor budgets are climbing as militaries favor survivability upgrades over new platforms. The US Army allocated USD 108 million in fiscal 2026 for its Vehicle Protection System, prioritizing retrofit kits that lighten legacy fleets[1]U.S. Department of the Army, “Fiscal Year 2026 Budget Highlights,” army.mil. The FBI issued a USD 45 million tender in 2025 for NIJ Level III shields and panels. The UK Ministry of Defence’s GBP 76 million framework, awarded in November 2025, focuses on VR7–VR9 civilian-profile vehicles. Weight limits in electric drivetrains are pushing the adoption of glass-clad polycarbonate and polymer-ceramic hybrids, with the US Navy SBIR funding lightweight laminates that cut mass by 25% against STANAG 4569 Level 3a threats.

Increasing Infrastructure Development in High-Risk Urban Areas

Megacities are embedding ballistic glazing in curtain walls to satisfy insurance and public-safety requirements. China’s JGJ 113-2015 mandates laminated safety glass in high-footfall buildings, and Shanghai extends the rule to façades taller than 24 m[2]Ministry of Housing and Urban-Rural Development of China, “JGJ 113-2015,” mohurd.gov.cn. India’s Central Reserve Police Force specifies bulletproof vehicles for Z and Z Special protectees, driving retrofits of sedans and SUVs. In the United States, FEMA’s ASCE 7-22 tornado provisions and ASTM impact tests now overlap with ballistic standards, allowing a single laminate to meet windborne-debris and small-arms threats.

Growing Utilization in Luxury and Armored Vehicles

OEMs are bundling factory armor to retain value. BMW launched the i7 Protection in 2024, the first electric sedan verified to VPAM VR10, integrating 1,750 kg of armor while maintaining a 236-mile range. General Motors Defense unveiled the Suburban Shield in 2025 to serve diplomatic fleets. The US State Department widened its USD 400 million armored-EV contract beyond Tesla, prompting Ford and Rivian to lock in ballistic-glass supply. Middle-East VIP buyers routinely request VR7–VR9 protection, sustaining demand for lighter polycarbonate laminates.

Mandatory Ballistic-Facade Codes in Climate-Resilient Buildings

Government funding ties safe-room projects to stricter glazing rules. FEMA P-361 requires tornado-missile resistance, and ICC 500-2023 is compulsory for federally backed community shelters. The DoD’s UFC 4-010-01 bans fragment-retention films and stipulates a minimum of 6 mm polycarbonate or laminated glass on new federal buildings. Europe is harmonizing EN 1063 ballistic and EN 13124 blast standards, enabling single-product compliance. These codes trigger retrofits of pre-2020 facilities, boosting replacement demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High raw-material and processing costs | −1.4% | Europe, North America | Short term (≤ 2 years) |

| Limited availability of skilled installers | −0.8% | North America, Europe, Asia-Pacific cities | Medium term (2-4 years) |

| Energy-intensive manufacturing process | −0.6% | Europe, North America, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Raw-Material and Processing Costs

Polycarbonate spot prices ranged from USD 2,810 / t in North America to USD 1,810 / t in China for optical grades in 2025, while BPA-free resins carry a 12–18% premium. Autoclave bonding consumes up to 200 kWh / m², and TPU bonding adds 10–15% more energy. Recycled cullet cuts float-glass energy by 25%, but the post-consumer supply is limited outside Europe.

Limited Availability of Skilled Installers

AGMT certification demands 7,500 hours of field practice and quadrennial renewal, creating a lag between demand spikes and workforce supply. Improper edge sealing can reduce ballistic performance by up to 30%. Robotics trimmed lay-up errors but requires USD 0.5–1.5 million per line, limiting uptake by smaller glaziers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polycarbonate Gains on Weight-Critical Applications

Solid acrylic held 45.19% of 2025 demand due to 92% light transmission and lower raw material cost. Polycarbonate is forecast to grow 10.21% annually through 2031 as defense and automotive buyers prioritize lighter, multi-hit laminates. Laminated glass remains prevalent in building façades that need blast retention, although its 40–60 kg/m² weight and interlayer aging limit use in mobile platforms. Glass-clad polycarbonate balances clarity and toughness but carries a 15–20% cost premium. Polymer-ceramic hybrids, including spinel and AlON strike faces, currently contribute under 5% of volume yet deliver 20–30% thickness savings, signaling future diffusion into automotive and aerospace fleets.

Demand for polycarbonate underscores the bulletproof glass market transition toward materials that reduce vehicle payload penalties without compromising NIJ Level III or VPAM VR7 standards. The bulletproof glass market size for polycarbonate laminates is projected to outpace acrylic by late-decade as factory-armored EVs and lightweight retrofit kits gain traction. Emerging TPU nanocomposites further lift spall strength by 34% compared with baseline TPU, extending service life and lowering replacement costs.

By End-User Industry: Automotive Outpaces Defense on EV Integration

Defense accounted for 41.97% of 2025 consumption, supported by multi-year military programs, yet growth remains single-digit amid budget plateaus. Automotive is set to advance at 11.92% CAGR through 2031 as OEMs like BMW and General Motors install ballistic packages at the assembly line to capture premium pricing. The bulletproof glass market share for factory-armored EVs is rising after the US State Department opened its USD 400 million contract to all domestic brands. Building and construction contribute roughly one-quarter of demand, anchored by FEMA and Chinese façade regulations.

Beyond core segments, marine, aerospace, and public transit consume niche volumes but grow double digits as they validate polymer-ceramic hybrids in weight-sensitive settings. The bulletproof glass industry is therefore broadening from defense-centric procurement to diversified mobility and infrastructure applications.

Geography Analysis

North America led the bulletproof glass market with 39.18% share in 2025 as US federal demand, including a USD 108 million Vehicle Protection System budget and a USD 45 million FBI tender, buoyed volumes. FEMA’s dual-threat glazing rules are aligning disaster-resilient and ballistic requirements, allowing suppliers to amortize certification costs across construction and defense projects. The broadened State Department EV framework has catalyzed domestic supply chains, while Canada and Mexico add incremental automotive retrofits.

Asia-Pacific is the fastest-growing region at a 12.17% CAGR. China enforces JGJ 113-2015, fueling laminated façade upgrades across megacities, and Fuyao Glass committed USD 400 million to Illinois, plus CNY 9.1 billion to new domestic float lines aimed at new-energy-vehicle glazing. India’s 200-person VIP protection roster sustains armored-SUV retrofits. Japan and South Korea invest in transparent-ceramic R&D that promises 20–30% weight savings for next-generation infantry vehicles.

In Europe, the UK’s GBP 76 million protected vehicle framework prioritizes low-profile electric SUVs. AGC’s January 2025 acquisition of SGT Germany and its October 2025 photovoltaic-glass recycling pilot illustrate incumbent moves toward vertical integration and lower-carbon float furnaces. EU ETS carbon pricing pressures margins yet accelerates recycled-content laminates. Saudi Arabia, UAE, and Brazil round out global pockets investing in ballistic façades for government and commercial assets.

Competitive Landscape

The bulletproof glass market is moderately concentrated. Process innovation is eclipsing scale as a differentiator. Saint-Gobain patented a sapphire-glass-polycarbonate laminate achieving 85% light transmission at 72.78 kg/m², aiming at electric-vehicle and aerospace niches. NxLite debuted low-emissivity coatings on polycarbonate that halve the weight versus glass while passing ASTM impact tests. Installer bottlenecks and energy costs invite disruption. Robotic bonding lines reduce labor needs but demand heavy capex, motivating smaller entrants to offer modular, pre-certified panels.

Bulletproof Glass Industry Leaders

Saint-Gobain

Guardian Industries

AGC Inc.

SCHOTT

Nippon Sheet Glass Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Fuyao Glass Industry Group Co., Ltd., announced a USD 400 million expansion of its Decatur, Illinois, float-glass facility to boost the supply of high-quality automotive glazing to US OEMs. The expansion will enhance the broader North American bulletproof glass supply chain through improved raw material availability.

- April 2025: The University of Oulu in Finland inaugurated its 6G test centre, offering testing services to corporate clients. Tambest, a Finnish glass processing factory, became the inaugural client. During the initial tests, various bulletproof glasses, designed to shield against signal interference, were evaluated. The test outcomes helped in refining the product.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the bulletproof glass market as the annual value of newly-manufactured transparent armor panels formed from layered glass and polymer sheets that resist specified ballistic threats across security levels 1-8. These panels are supplied to OEM vehicle makers, building façade contractors, financial institutions, and defense agencies.

Scope Exclusion: Retro-fit films, opaque composite armor, and post-installation maintenance services lie outside our valuation.

Segmentation Overview

- By Type

- Solid Acrylic

- Traditional Laminated

- Polycarbonate

- Glass-clad Polycarbonate

- Other Types (Polymer-Ceramic Hybrid, and more)

- By End-user Industry

- Automotive

- Building and Construction

- Defense

- Other End-user Industries (Marine, and more)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We subsequently interviewed ballistic-testing laboratory managers, procurement heads at armored-vehicle assemblers across North America, Europe, and the Gulf, and facility planners for high-risk government buildings in Asia-Pacific. Their insights refined price-thickness curves, clarified capacity utilization swings, and validated regional demand pockets that secondary sources could not quantify.

Desk Research

Mordor analysts first mapped the industry using open data from sources such as the Small Arms Survey, SIPRI military-expenditure tables, U.S. Harmonized Tariff Schedule import lines for laminated safety glass, and construction permit filings captured by Dodge Data & Analytics. Trade association papers from the International Association for Safety & Security Glass and academic journals covering polymer interlayers helped us frame failure-mode criteria. Company disclosures on armored limousine output, together with D&B Hoovers financials, grounded revenue share estimates. This list is illustrative only; many additional public and paid references were reviewed before numbers were finalized.

Market-Sizing & Forecasting

Top-down modeling begins with global output of laminated safety glass and transparent armor, reconstructed from production and customs data, then apportioned to end uses through verified penetration ratios. Supplier roll-ups of polycarbonate sheet shipments and sampled average-selling-price × volume checks offer bottom-up cross-tests that temper totals. Key variables like defense budget allocation to protected vehicles, luxury-SUV production, rate of new bank branch openings, and Class 3+ building code adoptions feed a multivariate regression that projects demand to 2030. Scenario analysis captures upside from lightweight nano-laminates and downside from budget freezes. Data gaps, for instance on clandestine military retrofits, are bridged using regional analogs vetted with subject-matter experts.

Data Validation & Update Cycle

Outputs pass three layers of review: variance checks against historical trade flows, peer challenge within the analyst team, and a sign-off by a senior reviewer. The model refreshes each year; interim updates trigger when exchange-rate shifts, regulatory changes, or plant-capacity announcements would move totals by more than three percent.

Why Mordor's Bulletproof Glass Baseline Earns Trust

Estimates from different publishers often diverge because each chooses distinct security levels, regional cut-offs, and base years.

Our disciplined scope selection, yearly refresh, and dual-angle modeling create a dependable midpoint that decision-makers can audit.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.45 B (2025) | Mordor Intelligence | - |

| USD 9.30 B (2023) | Global Consultancy A | Older base year and omission of construction glazing |

| USD 8.80 B (2024) | Industry Journal B | Limited MENA coverage and reliance on public-company revenues only |

| USD 7.37 B (2022) | Regional Consultancy C | Narrow security level scope and static FX rates |

The comparison shows that when differing years, scopes, and data inputs are normalized, Mordor's 2025 figure sits logically between lower-scope counts and aggressive long-tail projections, giving users a balanced, transparent baseline they can replicate and defend in board-room discussions.

Key Questions Answered in the Report

What is the 2026 value of the bulletproof glass market?

The bulletproof glass market size stands at USD 10.68 billion in 2026.

How fast will global demand grow through 2031?

Market revenue is forecast to expand at a 9.12% CAGR between 2026 and 2031.

Which product type is growing the quickest?

Polycarbonate laminates are advancing at a 10.21% annual rate through 2031 as buyers seek lighter, multi-hit solutions.

Which end-user will add the most incremental volume?

Automotive leads growth, with an 11.92% CAGR thanks to factory-integrated armored electric vehicles.

Why is Asia-Pacific the fastest-growing region?

China’s façade mandates and India’s VIP-protection fleet are driving a 12.17% regional CAGR.

Page last updated on: