Lignin Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

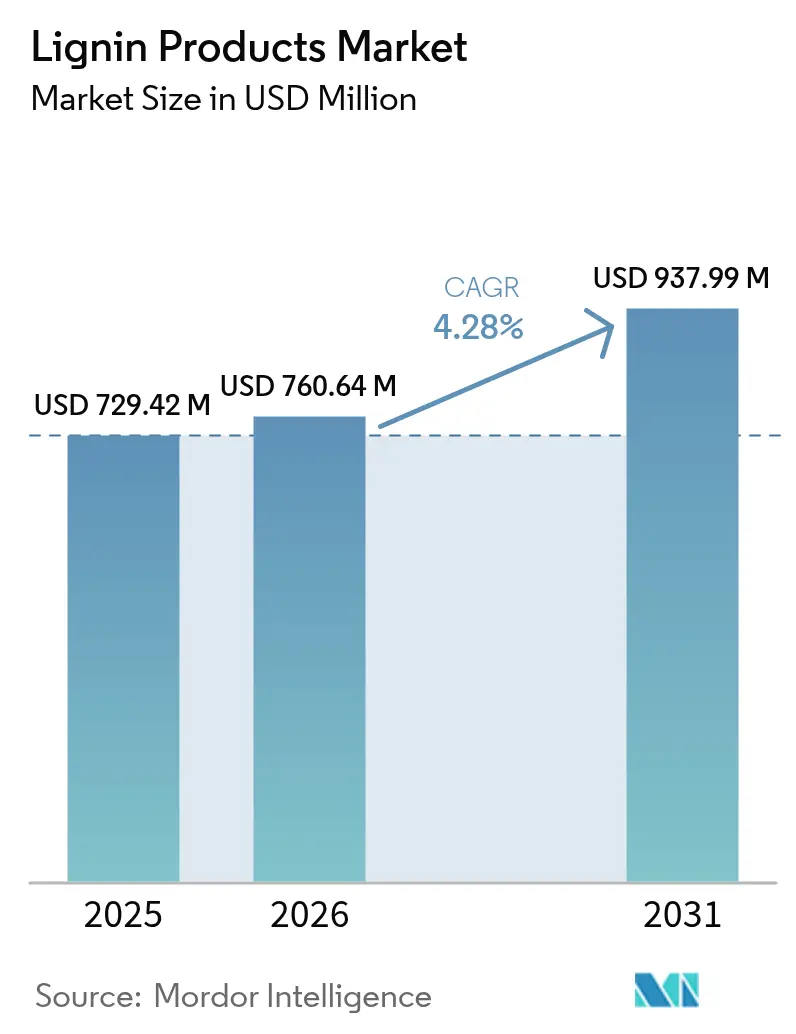

| Market Size (2026) | USD 760.64 Million |

| Market Size (2031) | USD 937.99 Million |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lignin Products Market Analysis by Mordor Intelligence

The Lignin Products market size is expected to grow from USD 729.42 million in 2025 to USD 760.64 million in 2026 and is forecast to reach USD 937.99 million by 2031 at 4.28% CAGR over 2026-2031. Performance gains stem from rising demand for low-carbon construction chemicals, stricter sustainability regulations across mature economies, and continuing breakthroughs in bioconversion pathways that open high-value outlets for lignin‐based aromatics. The shift from waste-stream disposal toward value-added biorefinery integration reinforces pricing power, especially for high-purity grades supplied to the pharmaceutical and electronics value chains. Europe preserves first-mover advantage thanks to long-standing pulp-mill infrastructure, while North America records the fastest growth on the back of cellulosic ethanol mandates and automotive lightweighting programs. Competitive intensity remains moderate, with integrated pulp producers leveraging scale to protect margins against smaller specialty processors

Key Report Takeaways

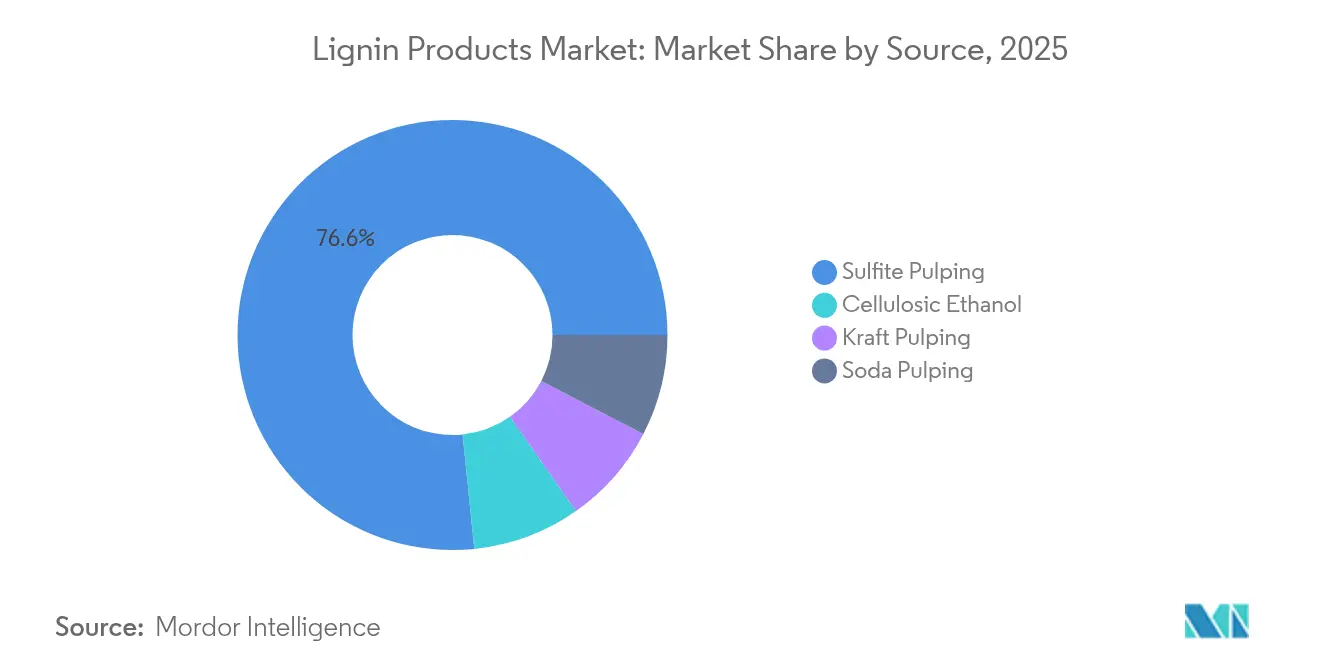

- By source, sulfite pulping led with 76.62% lignin products market share in 2025; cellulosic ethanol posted the highest projected 4.95% CAGR through 2031.

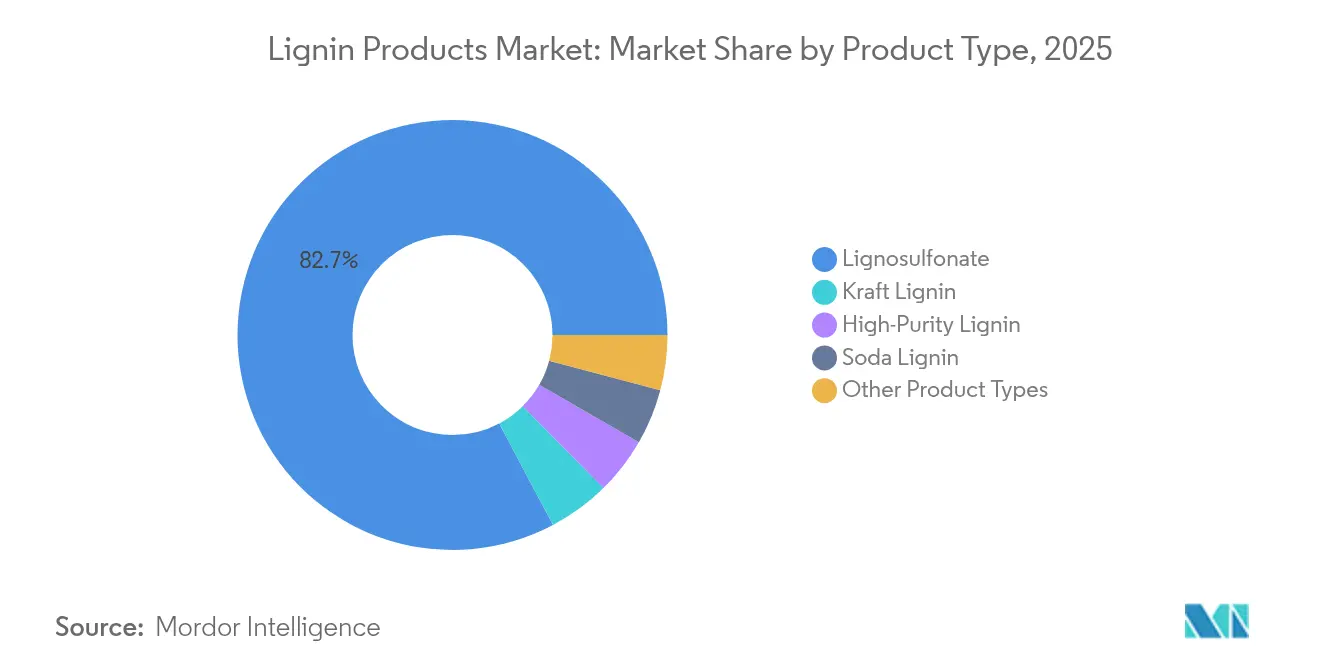

- By product type, lignosulfonate accounted for 82.74% of the lignin products market size in 2025, while kraft lignin is poised to expand at a 5.29% CAGR to 2031.

- By application, dispersants held 30.44% revenue share in 2025; concrete additives are forecast to grow at a 5.31% CAGR to 2031.

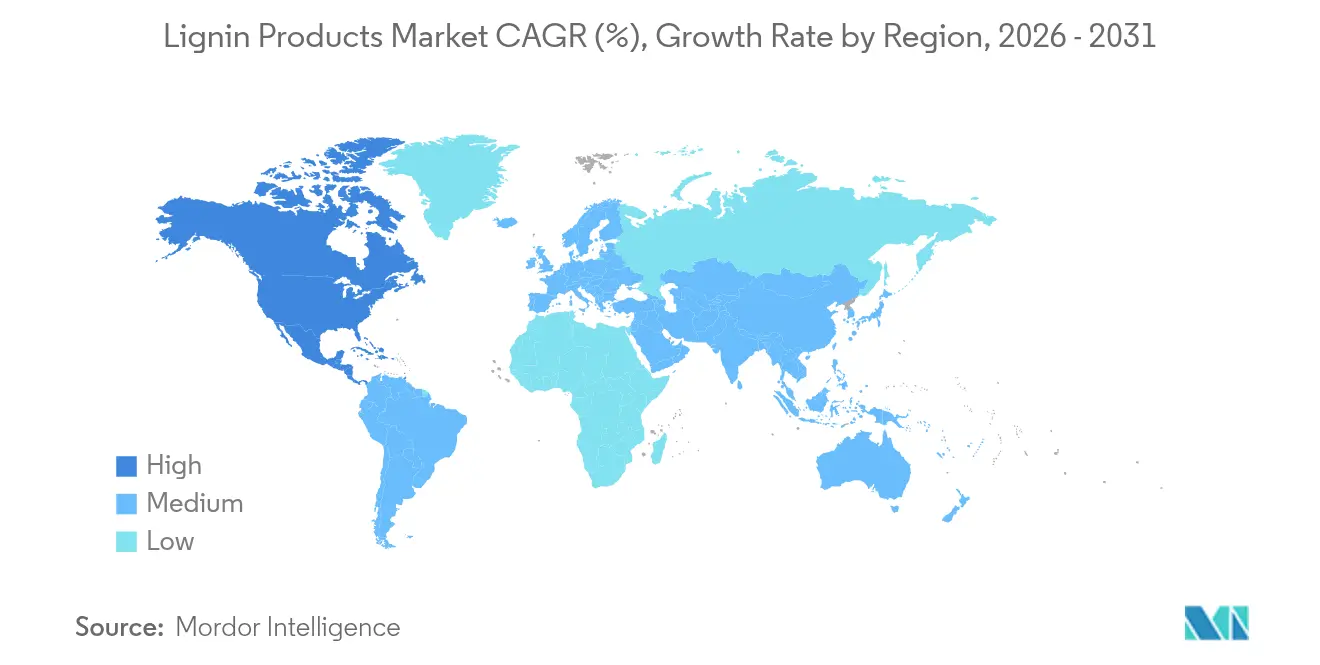

- By geography, Europe captured 33.55% share of the lignin products market in 2025, whereas North America is projected to register the highest 5.08% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lignin Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for High-Performance Concrete Admixtures | +1.8% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Uptake of Lignin-Based Feed Binders in Animal Nutrition | +1.2% | Europe and North America core, expanding to APAC | Long term (≥ 4 years) |

| Valorisation of Pulp-Mill Side-Streams for Circular Revenue | +0.8% | Nordic countries, North America, Brazil | Short term (≤ 2 years) |

| Breakthrough Lignin-To-Vanillin Bioconversion Routes | +0.6% | Europe and North America, pilot projects in Asia | Long term (≥ 4 years) |

| Automotive Push for Lignin-Derived Bio-Carbon Fibre | +0.5% | Germany, Japan, United States automotive clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High-Performance Concrete Admixtures

Infrastructure expansion across Asia-Pacific and Latin America raises the need for superplasticizers that improve flow while lowering cement consumption. Lignin-based admixtures reduce water-cement ratios, boosting compressive strength by 15-20% and cutting cement use by 8-12%[1]Xinyu Li, “Performance of Lignin-Based Superplasticizers,” Cement and Concrete Research, scientific.net . Construction firms pursuing LEED certification favor these bio-based solutions because they lower embodied carbon in high-rise and transportation projects. Green-building codes in China and India now endorse natural admixtures, providing a regulatory pull that accelerates commercialization. Producers scale up capacity to keep pace with large metro and highway contracts that specify performance concrete. Steady gains in smart-city investments anticipate durable demand for lignin superplasticizers through the medium term.

Uptake of Lignin-Based Feed Binders in Animal Nutrition

European regulations that restrict antibiotic growth promoters have moved feed formulators toward lignosulfonate binders. Studies show 25-30% better pellet durability versus molasses systems, translating into lower feed dust and reduced transport losses. Specific lignin fractions exhibit prebiotic activity that enhances ruminant gut microbiota, allowing feed companies to price at a premium. Danish and Dutch manufacturers report 12-15% logistics cost savings after sourcing local lignin derivatives from regional pulp mills. North American producers adopt similar strategies as large integrators target antibiotic-free supply chains. The long-term outlook remains strong as Asia-Pacific livestock operators shift toward higher-value protein and require efficiency gains in compound feed.

Valorisation of Pulp-Mill Side-Streams for Circular Revenue

Pulp producers, under pressure from tighter emission standards and fiber cost inflation, increasingly monetize lignin streams. Recovery systems yield 8-12% incremental revenue per ton of pulp, turning a legacy waste into a profit center. Equipment suppliers offer retrofits that achieve 85-90% recovery with minimal energy penalty, giving mills processing over 500,000 tons annual capacity three-to-four-year payback periods. Nordic operators lead adoption, but installations in Brazil and Canada quickly follow as carbon-pricing schemes raise disposal costs. Captive lignin output feeds on-site boilers, reducing fossil fuel demand and improving mill energy balance. Combined with renewable-power credits, the circular model supports financial resilience in the volatile pulp sector.

Breakthrough Lignin-to-Vanillin Bioconversion Routes

Enzymatic pathways now deliver 15-20% vanillin yields from kraft lignin, fivefold higher than legacy oxidation. The process eliminates aggressive chemicals and runs 60–80 °C cooler, slashing energy use and generating higher-purity output. Pilot plants in Finland, France, and the United States demonstrate 40-50% lower unit cost than petroleum routes. Rising global vanilla demand at an 8–10% clip strengthens the business case, and food companies keen on natural labels contract early offtake volumes. Regulatory bodies accept lignin-origin vanillin as “natural flavor,” widening the addressable market. Commercial-scale facilities are scheduled for start-up by 2027, signaling meaningful supply additions in the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quality Variability Across Extraction Processes | -0.7% | Global, particularly affecting emerging market producers | Short term (≤ 2 years) |

| Competition from Sugar-Derived Bio-Aromatics | -0.4% | North America and Europe, where sugar processing is established | Medium term (2-4 years) |

| Lack of International Lignin Product Standards | -0.3% | Global, with strongest impact on cross-border trade | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Quality Variability Across Extraction Processes

Differences in sulfur content and molecular weight between kraft, sulfite, and soda lignin complicate procurement for users that require consistent specifications. Sulfite variants carry 20-30% higher sulfur, impacting resin cure kinetics and demanding tailored processing protocols[2]Mark Johnson, “Quality Variability in Technical Lignins,” Industrial & Engineering Chemistry Research, acs.org . Downstream firms maintain parallel inventories and dual qualification programs, inflating supply-chain spending by 8-12%. Smaller mills rarely possess analytical labs to certify each batch, restricting market access to low-margin outlets. Near-term uncertainty remains until shared testing standards emerge and cloud-based traceability platforms mature. Quality harmonization is therefore pivotal for broader adoption in specialty segments.

Competition from Sugar-Derived Bio-Aromatics

Fermentation platforms converting glucose to vanillin, phenol, and other aromatics achieve 99.5% purity, outclassing lignin-based products that generally reach 95–97%. Pharmaceutical and premium flavor markets pay 15-20% extra for the higher consistency. Brazil and India leverage existing cane and corn sucrose streams, enabling continuous supply at industrial scale. As sugar prices stay subdued, the cost gap narrows, pressuring lignin players in high-value chemical niches. To defend share, lignin producers invest in purification innovations and co-product valorization. The medium-term outlook hinges on parity in purity and price.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Sulfite Pulping Dominates Despite Cellulosic Growth

The lignin products market size linked to sulfite pulping totaled the bulk of global value, securing 76.62% in 2025 on the back of abundant volumes and well-known performance in dispersants. Cellulosic ethanol plants offer much smaller but higher-margin flows, and their 4.95% CAGR makes them the most dynamic source category to 2031. Production incentives under the U.S. Renewable Fuel Standard and EU RED-II encourage biorefineries to integrate lignin separation units, adding revenue equal to 12-15% of ethanol sales. Sulfite operators, chiefly in Europe and China, defend position by optimizing recovery yields and launching tailor-made grades for concrete and feed. Soda pulping keeps niche importance in India and Southeast Asia, processing agricultural residues into low-ash lignin for regional textile chemicals.

Cellulosic ethanol lignin typically displays lower ash and narrower molecular-weight distribution than kraft material, granting it a premium in specialty polymers. Pilot users in automotive composites value the predictable rheology that aids continuous fiber spinning. As ethanol producers scale capacity, supply of this high-quality lignin grows, tightening integration between biofuel and specialty chemical chains. Although sulfite volumes dwarf other sources, competitive dynamics hinge on value per ton rather than tonnage alone, especially as carbon revenue streams influence profitability.

By Product Type: Kraft Lignin Gains Despite Lignosulfonate Leadership

Lignosulfonate controlled 82.74% of 2025 value due to entrenched applications in concrete, feed, and dust suppression, benefiting from water solubility that eases blending. Kraft lignin expansion at a 5.29% CAGR derives from severe interest in carbon fibre precursors and bio-based resins. High-purity fractions, though costly to make, open doors in electronics and pharma intermediates where metal content must stay below strict thresholds. Soda lignin meets regional demand for dispersants in pulp and paper mills that process agri-residue, especially in China and Vietnam.

Growth strategies rest on purification technology. Stora Enso’s Sunila line adopts membrane and ion-exchange polishing, pushing kraft lignin to pharmaceutical grade. Ingevity and Valmet develop fractionation know-how to tailor molecular-weight cuts, delivering better compatibility in epoxy systems. Lignosulfonate producers focus on specialty concrete admixtures that satisfy ASTM C494 and European EN 934 standards. Competitive advantage shifts from bulk cost to property consistency, enabling differentiated pricing and lower sensitivity to commodity cycles.

By Application: Concrete Additives Drive Growth Beyond Dispersant Dominance

Dispersants accounted for 30.44% share in 2025 thanks to lignosulfonate’s long history in dye, pesticide, and gypsum slurry formulations. Concrete additives, however, register the quickest 5.31% CAGR as governments fund megaprojects and green-building codes proliferate. Lignin superplasticizers reduce cement content by up to 20%, an attractive attribute when cement production faces carbon taxes. Animal feed demand gains from antibiotic restrictions, while resins benefit from consumer electronics assembly lines seeking formaldehyde-free adhesives.

Specification driven markets demand precise molecular-weight windows and low heavy-metal counts. Producers employ ultrafiltration to remove ash that can hinder concrete set time and feed palatability. For resins, lignin reacts with epoxides to replace bisphenol-A partially, offering safer profiles aligned with consumer product regulations. The diversification across multiple downstream uses insulates suppliers from cyclical swings in any single sector, supporting steady revenue streams through 2031.

Geography Analysis

Europe held 33.55% of global value in 2025 because integrated forest industries and strict climate policies foster early lignin valorization. Pulp mills in Finland and Sweden retrofit extraction lines to capture new revenue, while German concrete and automotive sectors absorb steady volumes. REACH chemicals regulation nudges formulators toward bio-derived inputs, improving demand visibility. Horizon Europe research grants accelerate pilot deployments in vanillin and carbon-fibre, solidifying the region’s innovation leadership.

North America posts the fastest 5.08% CAGR through 2031 as federal cellulosic fuel mandates widen lignin supply and automotive lightweighting efforts raise the bar on sustainable composites. The lignin products market size for concrete admixtures climbs in the United States on the back of the Bipartisan Infrastructure Law, which modernizes bridges and transit. Canadian forestry companies leverage abundant boreal resources to diversify beyond pulp into specialty lignin, supported by provincial carbon-pricing mechanisms that favor low-emission materials. Mexico’s construction boom also creates room for admixture imports, rounding out continental demand.

Asia-Pacific stands at an earlier adoption curve yet offers vast upside. China’s rapid urbanization elevates concrete consumption, and state standards begin to recognize lignin superplasticizers. India scales soda pulping for agri-residue, producing cost-competitive lignin for local feed and dye dispersants. Japan exploits lignin’s aromatic backbone in electronics resins, while South Korea includes lignin-based chemicals in green-procurement lists. Ongoing ASEAN infrastructure initiatives and growing meat production foster multipronged demand, though standards harmonization will be critical for cross-border trade.

Competitive Landscape

Market structure remains moderately fragmented because integrated pulp giants coexist with agile biotech startups. Borregaard, Stora Enso, and Suzano exploit scale and secure wood supply while investing heavily in fractionation technology that upgrades lignin for pharmaceutical and advanced-material targets. Mid-tier players like Ingevity and RYAM focus on kraft-lignin derivatives for carbon-fibre and epoxy resins, employing proprietary molecular-weight control to carve niches.

Technology collaboration defines strategy. Borregaard’s alliance with Archer Daniels Midland opens North American feed markets, combining biochemical skillsets with distribution muscle. Valmet supplies turnkey extraction systems, securing installed-base service revenue and cross-selling opportunities. Patent activity climbed 35% in 2024, reflecting intense R&D in enzymatic depolymerization, vanillin synthesis, and electrospinning of lignin fibres. Specialty processors differentiate through low-metal content, sulfur control, and tailored functionality that address high-margin sectors like electronics solder masks and pharmaceutical excipients.

Capital deployment patterns reveal a pivot from bulk capacity toward downstream integration. Stora Enso’s EUR 50 million Sunila expansion raises high-purity output by 40%, enabling entry into medical-grade polymers. RYAM’s Temiscaming upgrade adds 25,000 tons annual kraft lignin, designed for stringent composite applications. Fragmentation persists because small mills continue supplying commoditized lignosulfonate to tradable markets, yet rising quality expectations may spur consolidation as buyers gravitate to certified vendors.

Lignin Products Industry Leaders

Borregaard AS

Ingevity

Stora Enso

Sappi Ltd

RYAM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Metsä Group developed Metsä LigO, a lignin product developed at its Äänekoski demo plant. This product, derived from the pulp process, aims to replace fossil-based chemicals in concrete production.

- September 2024: UPM Biochemicals partnered with Södra to advance lignin-based solutions. UPM will become a key customer for Södra's large-scale kraft lignin facility, set to begin operations in 2027, promoting bio-based alternatives over fossil-based materials.

Global Lignin Products Market Report Scope

Lignin is a biodegradable polymer/polymer blend naturally found in the cell walls of almost all dry plants. Lignin products are being used as replacements for fossil-based products. Lignin exhibits dispersing, binding, and chelating properties that are exploited for various applications including concrete additives, animal feed, resins, plastics, carbon fiber, etc., that serve major industries such as automotive, construction, agrochemicals, etc.

The Lignin Products Market is segmented by source, product type, application, and geography. By source, the market is segmented into cellulosic ethanol, kraft pulping, sulfite pulping, and soda pulping. By product type, the market is segmented into lignosulfonate, kraft lignin, high-purity lignin, soda lignin (alkali lignin), and other product types. By application, the market is segmented into current applications (concrete additive, animal feed, dispersant, resins, and other current applications (binding agents, emulsion stabilizers, and dust control agents)) and upcoming applications (vanillin, activated carbon, carbon fibers, plastics/polymers, phenol and derivatives, and other applications. The report also covers market size and forecasts for lignin products market in 13 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of value (USD).

| Sulfite Pulping |

| Cellulosic Ethanol |

| Kraft Pulping |

| Soda Pulping |

| Lignosulfonate |

| Kraft Lignin |

| High-Purity Lignin |

| Soda Lignin |

| Other Product Types |

| Dispersant |

| Concrete Additive |

| Animal Feed |

| Resins |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Sulfite Pulping | |

| Cellulosic Ethanol | ||

| Kraft Pulping | ||

| Soda Pulping | ||

| By Product Type | Lignosulfonate | |

| Kraft Lignin | ||

| High-Purity Lignin | ||

| Soda Lignin | ||

| Other Product Types | ||

| By Application | Dispersant | |

| Concrete Additive | ||

| Animal Feed | ||

| Resins | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected global value of lignin products by 2031?

The market is forecast to reach USD 937.99 million by 2031, rising at a 4.28% CAGR.

Which region currently holds the largest share of lignin product demand?

Europe leads with a 33.55% share thanks to established pulp‐mill infrastructure and stringent sustainability rules.

Which application is expanding the fastest in the next five years?

Concrete additives show the highest growth, advancing at a 5.31% CAGR as green-building codes encourage low-carbon superplasticizers.

How are cellulosic ethanol plants influencing lignin supply?

They recover high-purity lignin as a co-product, adding 12-15% extra revenue per ton of ethanol and growing at a 4.95% CAGR through 2031.

Page last updated on: