Lighting As A Service (LaaS) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.01 Billion |

| Market Size (2031) | USD 4.01 Billion |

| Growth Rate (2026 - 2031) | 31.64% CAGR |

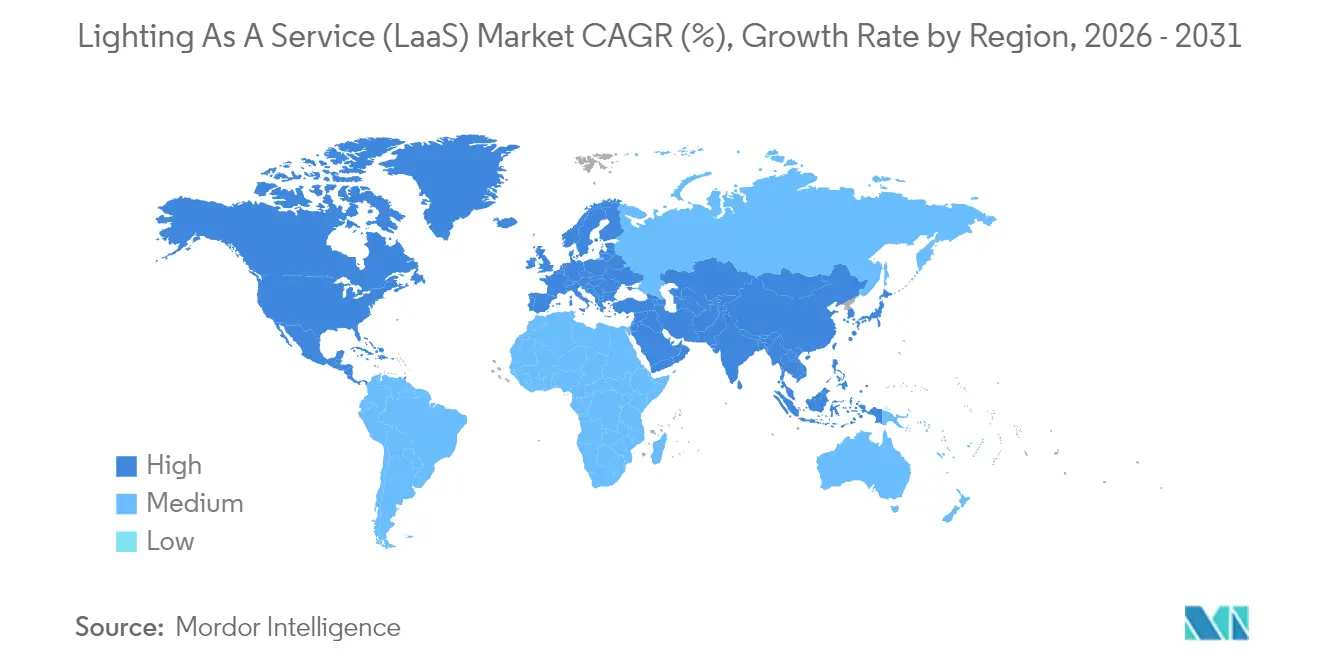

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lighting As A Service (LaaS) Market Analysis by Mordor Intelligence

Lighting As A Service market size in 2026 is estimated at USD 1.01 billion, growing from 2025 value of USD 0.77 billion with 2031 projections showing USD 4.01 billion, growing at 31.64% CAGR over 2026-2031.

This acceleration stems from a structural pivot away from capital-intensive fixture purchases toward subscription models that offload financing, technology, and maintenance risks onto specialized providers. Municipal smart-city budgets, stricter energy-efficiency regulations, and persistent corporate net-zero pledges are synchronizing to elevate service adoption. Hardware cost deflation and the rising ability to embed AI-driven controls inside luminaires are enlarging addressable opportunity pools, while bond-backed OPEX financing keeps projects off municipal balance sheets. Competitive intensity is shifting from luminaire manufacturing to analytics-enabled performance guarantees, transforming lighting grids into data-driven platforms.

Key Report Takeaways

- By installation type, indoor deployments held 69.92% of the Lighting as a Service market share in 2025, whereas outdoor projects are projected to expand at a 37.6% CAGR to 2031.

- By component, luminaires and controls captured a 59.10% revenue share in 2025; software and analytics are expected to grow at a 41.2% CAGR through 2031.

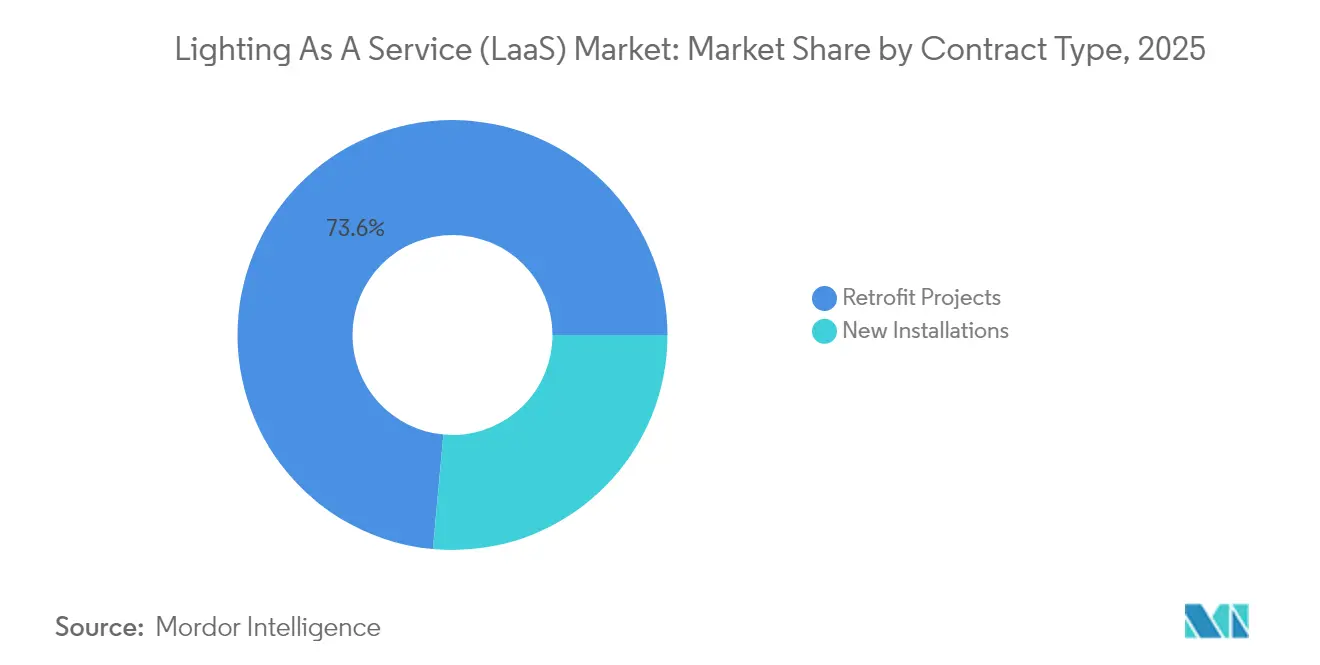

- By contract type, retrofit projects accounted for 73.55% of the Lighting as a Service market size in 2025, while new installations are projected to record the highest CAGR of 42.1% from 2025 to 2031.

- By end-user, commercial facilities led with 47.85% revenue share in 2025; municipal projects are advancing at a 38.2% CAGR through 2031.

- By geography, North America commanded a 44.12% share in 2025, but the Asia-Pacific region is on track for the fastest growth, with a 43.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lighting As A Service (LaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government energy-efficiency mandates | +8.20% | Global, with strongest impact in North America and EU | Medium term (2-4 years) |

| Declining LED & sensor costs | +6.80% | Global, with accelerated adoption in APAC and emerging markets | Short term (≤ 2 years) |

| Corporate net-zero & ESG targets | +5.40% | North America & EU core, expanding to APAC corporate sectors | Long term (≥ 4 years) |

| IoT-enabled smart-building retrofits | +4.90% | Global urban centers, concentrated in smart city initiatives | Medium term (2-4 years) |

| Green-bond financing for lighting OPEX models | +3.70% | North America and EU municipal markets, emerging in APAC | Long term (≥ 4 years) |

| AI-driven lighting-as-a-platform upsell potential | +2.80% | North America and EU commercial sectors, selective APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Energy-Efficiency Mandates

New rules, such as the U.S. Department of Energy’s 120 lumens-per-watt standard, effective July 2028, trigger widespread fixture obsolescence, positioning service contracts as a compliance shortcut that avoids heavy upfront cap-ex. Municipal utilities in California invested USD 223 million in 2022 efficiency programs, with lighting accounting for 34% of the gross annual savings, underscoring the urgency of purchasing. Because service providers assume replacement and regulatory risk, cities and corporates pivot toward outcome-based agreements that guarantee standards alignment while delivering measurable carbon-cutting baselines.(1)U.S. Department of Energy, “Final Rule: Energy Conservation Standards for General Service Lamps,” energy.gov

Declining LED & Sensor Costs

LED package prices have fallen sharply, enabling service providers to offer subscriptions at prices below those of incumbent utilities while maintaining their margins. With LED units already accounting for 70% of global shipments in 2024 and projected to reach 87% by 2030, a secondary replacement demand of 5.8 billion lamps emerges, boosting recurring revenue prospects. Connected luminaires reduce energy consumption by up to 80% when sensor-guided dimming is combined with native LED efficiency, enhancing the service value proposition.(2)Semiconductor Today, “LED Lamp Prices Continue to Fall,” semiconductortoday.com

Corporate Net-Zero & ESG Targets

Enterprises under Scope 2 disclosure pressure often prefer outsourcing their lighting assets to vendors that certify their energy and carbon performance. Signify reports that 65% of its 2025 sales are tied to climate-positive products, signaling a buyer preference for partners that couple hardware with verifiable sustainability metrics. Service contracts integrate lighting OPEX into ESG budgets and supply data for annual sustainability filings, accelerating board-level approvals for portfolio-wide retrofits.

IoT-Enabled Smart-Building Retrofits

Lighting grids are evolving into sensor backbones for occupancy analytics, indoor air quality alerts, and asset tracking. Studies indicate an average power reduction of 36.8 kW when autonomous controls optimize brightness against real-time occupancy. The added operational intelligence, unavailable through basic LED replacements, differentiates full-scope service offers and justifies multi-year managed contracts.(3)MDPI, “Smart Building Lighting Control for Energy Savings,” mdpi.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total contract cost vs. cap-ex purchase | -4.60% | Global, with strongest impact in price-sensitive emerging markets | Short term (≤ 2 years) |

| Utility rebate uncertainty | -3.80% | North America and EU markets with established rebate programs | Medium term (2-4 years) |

| Cyber-security concerns in connected luminaires | -2.90% | Global enterprise and government sectors | Medium term (2-4 years) |

| Limited LaaS awareness in mid-sized enterprises | -2.10% | Global, concentrated in mid-market commercial segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Total Contract Cost vs. Cap-Ex Purchase

Monthly fees can appear burdensome when compared with spot purchases, despite LEDs consuming 75% less power and lasting 25 times longer than incandescent fixtures. Organisations possessing strong cash reserves often decide to self-finance equipment to capture full savings, especially in economies prone to currency swings that inflate service premiums. Providers need to emphasize guaranteed uptime, refresh cycles, and performance warranties to offset sticker shock.

Utility Rebate Uncertainty

Rebate pools, such as Austin Energy’s USD 420-per-kW program, regularly reach funding ceilings, forcing providers to hedge their offers or risk margin erosion. In California, public utilities allocated USD 159 million to efficiency programs in 2021; however, lighting eligibility rules shifted for the next fiscal year, clouding ROI modeling. This volatility slows sales and lengthens contract negotiations, particularly for mid-scale retrofits dependent on incentive stacking.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Installation Type: Indoor Dominance Drives Service Standardization

Indoor projects accounted for 69.92% of the Lighting as a Service market in 2025, reflecting abundant demand in offices, logistics hubs, and manufacturing facilities where standardized ceiling grids reduce engineering variance and simplify service pricing. Providers bundle predictive maintenance and future technology upgrades into contracts, ensuring clients avoid stranded assets as control protocols evolve. Energy code tightening across North America and the EU intensifies the focus on indoor environments, while AI-driven occupancy analytics unlock new revenue opportunities per square foot. Outdoor implementations are scaling quickly at a 37.6% CAGR thanks to municipal smart-street programs; poles now support cameras, 5G small cells, and environmental sensors. Washington D.C.’s USD 309 million concession validates the economics by pairing 50% energy savings with revenue-sharing from data services, an example that is being mirrored in Miami-Dade’s USD 211.7 million multi-sensor rollout. These projects demonstrate how lighting poles evolve into digital urban infrastructure, signaling a deeper level of municipal engagement for Lighting as a Service market teams.

Outdoor’s expansion prompts vendors to refine ruggedized hardware, adaptive dimming algorithms, and financial structures, such as public-private partnerships, that align with 15-year debt amortization schedules. The segment’s growth also stimulates ancillary markets for security analytics, parking management, and air-quality monitoring. As more cities re-tender legacy fixtures, providers with turnkey design-build-finance-maintain packages gain commercial leverage. Indoor environments will remain volume leaders, but the higher per-node revenue and public-sector tenures of outdoor solutions will balance overall portfolio risk for top vendors within the Lighting as a Service market.

By Component: Software Analytics Emerge as Growth Engine

Hardware still accounts for 59.10% of 2025 revenue, yet software and analytics are racing ahead at a 41.2% CAGR through 2031, transforming data insights into the new competitive frontier for the Lighting as a Service industry. Energy dashboards, predictive failure alerts, and integration APIs embed lighting networks inside broader building-management stacks. The Lighting as a Service market size tied to analytics unlocks performance-based billing, allowing providers to monetize kilowatt-hour savings and productivity improvements rather than billing strictly per luminaire. AI-enabled optimisation now delivers up to 26% incremental energy cut on top of LED gains across multi-tenant offices.

Service modules covering asset financing, preventive maintenance, and luminaire recycling continue to underpin vendor cash flows. However, margin expansion also arises from proprietary algorithms that refine light-level tuning based on time-of-day, occupancy, and daylight harvesting inputs. Platforms that maintain open-protocol interoperability outpace closed ecosystems by facilitating seamless integration of third-party sensors and HVAC systems. The differentiation shift forces legacy manufacturers to invest in software talent or acquire SaaS-native firms to protect their installed bases. Customers benefit through lifecycle cost transparency and feature extensibility, reinforcing stickiness inside the Lighting as a Service market.

By Contract Type: Retrofit Projects Lead Market Maturity

Retrofit programmes captured 73.55% of the revenue in 2025 because they deliver immediate energy savings and regulatory compliance for facilities equipped with fluorescent or high-intensity discharge fixtures. Clear pre-retrofit baselines allow providers to model return profiles precisely, aligning payment schedules with verified savings in Lighting. The Lighting as a Service market size tied to retrofits is expected to peak as the first LED cohort, installed a decade ago, approaches end-of-life, between 2025 and 2028, driving a secondary replacement wave projected to represent 78% of LED demand.

New installations, expanding at the fastest rate of 42.1% CAGR, predicate their appeal on embedding service contracts from day one. Developers treat Lighting as a package within holistic smart-building concessions, bundling HVAC, security, and sensor grids for unified command and control platforms. This design-build-operate model shortens sales cycles because financing closes alongside property construction loans. It also accelerates software adoption because systems launch on modern IP networks rather than retrofit legacy wiring. Providers that can integrate BIM data and digitize lighting handoffs possess a crucial edge in the Lighting as a Service market.

By End User: Municipal Sector Accelerates Smart-City Integration

Commercial real estate led 2025 revenue with 47.85% share, bolstered by corporations aligning ESG roadmaps with operational cost cuts. Portfolio owners of logistics centres and retail chains leverage multi-site contracts to average payback over larger energy footprints. Yet municipal entities show the sharpest 38.2% CAGR through 2031 by tapping OPEX-friendly concession models. India’s programme, which replaced 29.5 million streetlamps, demonstrates how aggregated procurement unlocks supplier scale and delivers 48.42 billion kWh of yearly savings, making the Lighting as a Service market contract politically attractive.

Municipal customers also value data-rich poles that host traffic sensors, public Wi-Fi, and environmental monitoring, converting lighting grids into revenue-sharing civic assets. Industrial plants and residential complexes emerge as smaller but promising verticals; each requires tailored SLAs addressing harsh ambient conditions or strata-committee decision dynamics. Vendor segmentation strategies that tailor financial terms and service levels by vertical will dictate share gains throughout the Lighting as a Service market forecast period.

Geography Analysis

North America held a 44.12% share in 2025, driven by mature public-private partnership frameworks and rebate portfolios that reduce payback horizons. Washington D.C.’s USD 309 million street-lighting overhaul illustrates how city governments achieve 50% energy cuts while upgrading poles for surveillance and 5G backhaul. Federal efficiency rules mandating 120 lumens per watt by 2028 inject urgency into school, airport, and roadway retrofits. Utility incentives such as Austin Energy’s USD 420-per-kW credits further sweeten contract economics.

The Asia-Pacific region posts the fastest 43.9% CAGR, undergirded by high-density urbanization and state-engineered smart-city budgets. India’s Street Lighting National Program already retrofitted 29.5 million fixtures, translating into 39.30 million tonnes of annual CO₂ abatement. China’s multi-city digital-twin demonstrations and projects, such as the PHP 2.105 billion Bacolod Super City initiative, amplify the regional appetite for large-scale Lighting as a Service market convergence, Including Lighting, connectivity, and e-governance.

Europe’s market follows a stable replacement rhythm anchored to stringent climate legislation and aging sodium-vapor networks. Copenhagen switched 18,800 streetlights to LED, saving 55% of energy and eliminating 3,200 tons of CO₂ each year, while installing a remote-monitoring platform that future-proofs the poles for environmental sensors. Providers compete primarily on service-level adherence and cybersecurity credentials, as EU directives focus on data protection. Emerging regions in the Middle East, Africa, and South America display uneven but rising interest, where multilateral lenders and export-credit agencies bridge financing gaps, lighting the way for nascent Lighting as a Service market penetration.

Competitive Landscape

The field displays moderate fragmentation but rapid consolidation among incumbents transitioning from manufacturing to outcome-centric service portfolios. Acuity Brands’ USD 1.215 billion QSC acquisition enhances its Intelligent Spaces Group by introducing audio-visual controls that expand the platform's scope beyond illumination. Siemens’ planned takeover of Altair Engineering, slated to absorb the Toggled LED brand, signals heightened integration of lighting with wider building-automation stacks. These moves underscore a race to bundle controls, analytics, and financing within single-vendor propositions, which are viewed favourably by risk-averse buyers.

Technology leadership now rests on open-architecture software that secures IEC 62443 compliance, interoperates with HVAC and access control, and scales AI modules without vendor lock-in. Signify attaining DEKRA cybersecurity validation for Interact illustrates rising baseline expectations, pushing smaller providers toward partnerships or niche vertical focus. White-space opportunities remain in mid-market enterprises that perceive LaaS as complex; nimble specialists simplifying deployment may rapidly accumulate market share. Hardware commoditization means brand differentiation migrates to algorithmic energy optimization and lifecycle assurance—strategic pivot points defining future winners within the Lighting as a Service market.

M&A appetite remains high as diversified distributors, such as Wesco, and private-equity groups sharpen their supply-chain depth and regional channel span. Price competition persists in commodity fixtures, yet the total bundled contract value rises because software and data analytics layers expand ticket size. Vendors with integrated finance arms or access to green-bond pools enjoy lower capital costs, creating defensive moats and heightening the likelihood of further consolidation waves.

Lighting As A Service (LaaS) Industry Leaders

Every Watt Matters

Lumenix

Stouch Lighting

LEDVANCE GmbH

Signify Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Acuity Brands completed its acquisition of QSC for $1.215 billion, adding $535 million in revenue and expanding its cloud-managed building platform capabilities.

- January 2025: Signify formed a 60%-controlled venture with Gila Al Tawakol Electric to open an Egyptian factory producing LED lamps for Europe, Africa, and the Middle East.

- December 2024: Siemens has agreed to acquire Altair Engineering for $10.6 billion, incorporating Altair's Toggled LED lighting portfolio into its building automation offerings.

- November 2024: Wesco International this week announced it has entered a definitive agreement to acquire Ascent LLC., a provider of data center facility management services, for a cash-free, debt-free purchase price of $185 million.

Global Lighting As A Service (LaaS) Market Report Scope

The lighting-as-a-service market studies the business model where the customer does not buy its lighting equipment. Rather it enters a multilayer contract that stipulates a flat fee for the lighting needs. The lighting player provides the lamps, luminaries, and controls and, in some cases, can also offer additional services, such as data analysis and financing arrangements. Separate installation companies install the lighting system and receive a fee from the lighting company for maintaining that equipment over the life of the contract. The study further covers the market growth by different end-users and their impact on the regions around the world.

| Indoor |

| Outdoor |

| Luminaires and Controls |

| Software and Analytics |

| Services (Maintenance, Financing) |

| Retrofit Projects |

| New Installations |

| Commercial |

| Municipal |

| Industrial |

| Residential |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Installation Type | Indoor | |

| Outdoor | ||

| By Component | Luminaires and Controls | |

| Software and Analytics | ||

| Services (Maintenance, Financing) | ||

| By Contract Type | Retrofit Projects | |

| New Installations | ||

| By End User | Commercial | |

| Municipal | ||

| Industrial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Lighting as a Service market in 2026?

The Lighting as a Service market size stood at USD 1.01 billion in 2026 and is forecast to climb rapidly through 2031.

What CAGR is forecast for Lighting as a Service solutions?

Market value is projected to rise at a 31.64% CAGR between 2026 and 2031 on the strength of energy-efficiency regulations and smart-city spending.

Which end-user segment is growing fastest?

Municipal projects lead growth at a 38.2% CAGR because cities prefer long-tenor service contracts that modernize infrastructure without capital outlay.

Which geographic region will add the most incremental revenue?

Asia-Pacific shows the steepest 43.9% CAGR owing to large-scale urbanization programs and government-driven LED streetlight schemes.

Why are software and analytics critical in LaaS contracts?

Software layers optimise energy use, predict failures, and supply ESG reporting data, enabling vendors to charge performance-based fees beyond fixture supply.

What is the biggest barrier to adoption among mid-sized enterprises?

Limited awareness of service benefits and confusion over total contract cost versus cap-ex purchase delay decision-making, though education campaigns are starting to narrow the gap.

Page last updated on: