Global Legal Tech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

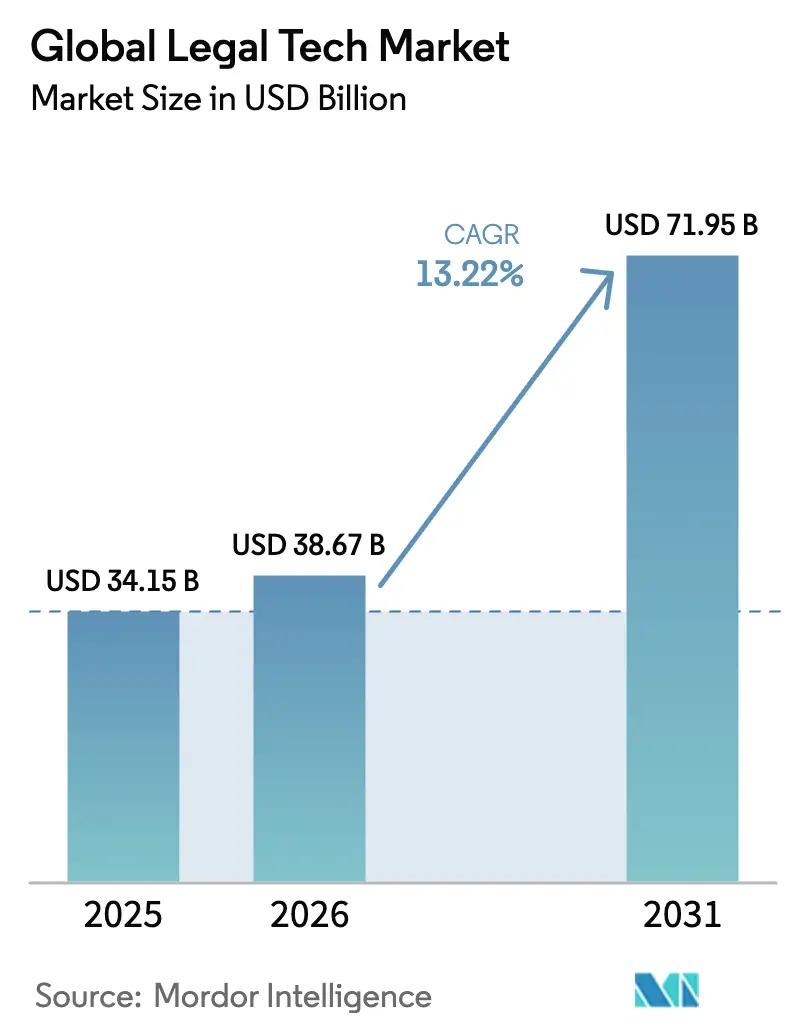

| Market Size (2026) | USD 38.67 Billion |

| Market Size (2031) | USD 71.95 Billion |

| Growth Rate (2026 - 2031) | 13.22% CAGR |

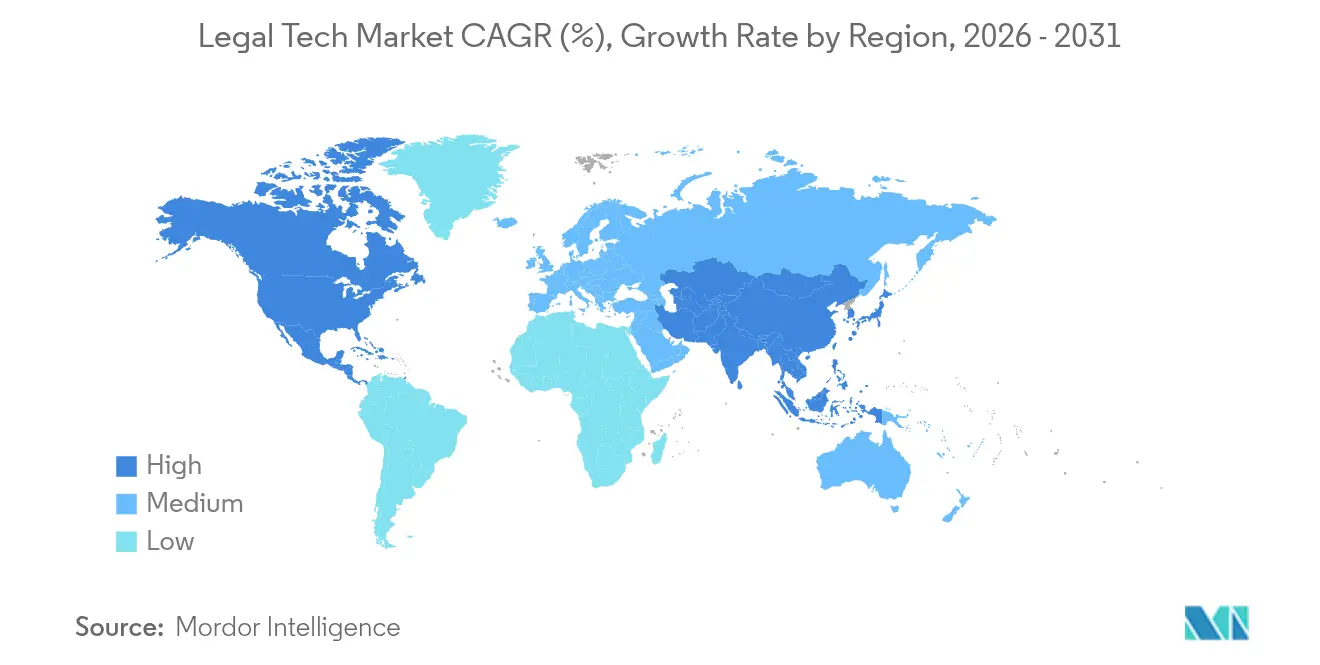

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Legal Tech Market Analysis by Mordor Intelligence

The legal technology market size is expected to grow from USD 34.15 billion in 2025 to USD 38.67 billion in 2026 and is forecast to reach USD 71.95 billion by 2031 at 13.22% CAGR over 2026-2031. Adoption of artificial intelligence, cloud deployment, and workflow-automation platforms underpins this momentum. Enterprise legal teams now prioritize end-to-end contract lifecycle management, while law firms look to counter margin pressure by automating research and drafting tasks. Ongoing venture-capital investment in AI-native vendors and rising ESG disclosure duties continue to widen the addressable user base. Heightened cybersecurity expectations and data-sovereignty obligations temper growth, but overall spending resilience keeps the legal technology market on a sustained upward trajectory.

Key Report Takeaways

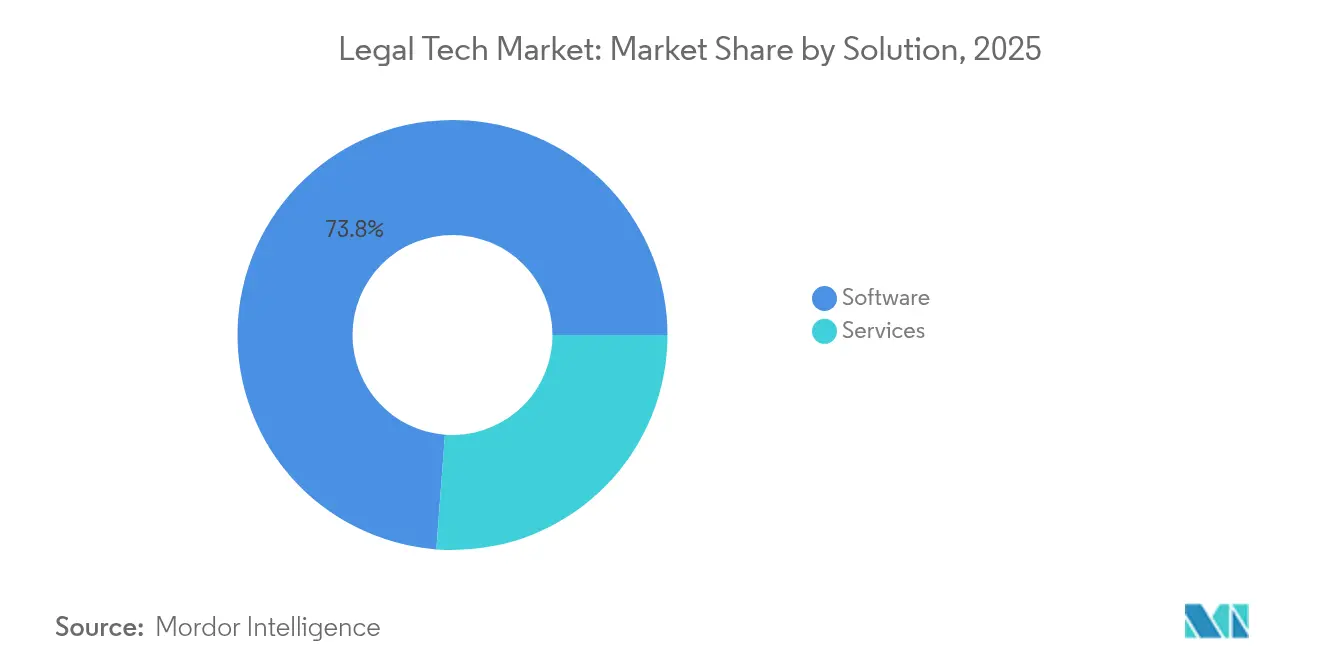

- By solution, software retained 73.80% revenue share in 2025, while services are predicted to grow at a 13.65% CAGR through 2031.

- By deployment model, cloud captured 64.90% of the legal technology market share in 2025; hybrid deployments are forecast to expand at a 15.55% CAGR to 2031.

- By application, eDiscovery led with 24.65% revenue share in 2025, whereas contract lifecycle management is advancing at a 18.35% CAGR through 2031.

- By organization size, large enterprises held 46.60% share in 2025, but small and mid-sized enterprises are set to grow at a 16.45% CAGR to 2031.

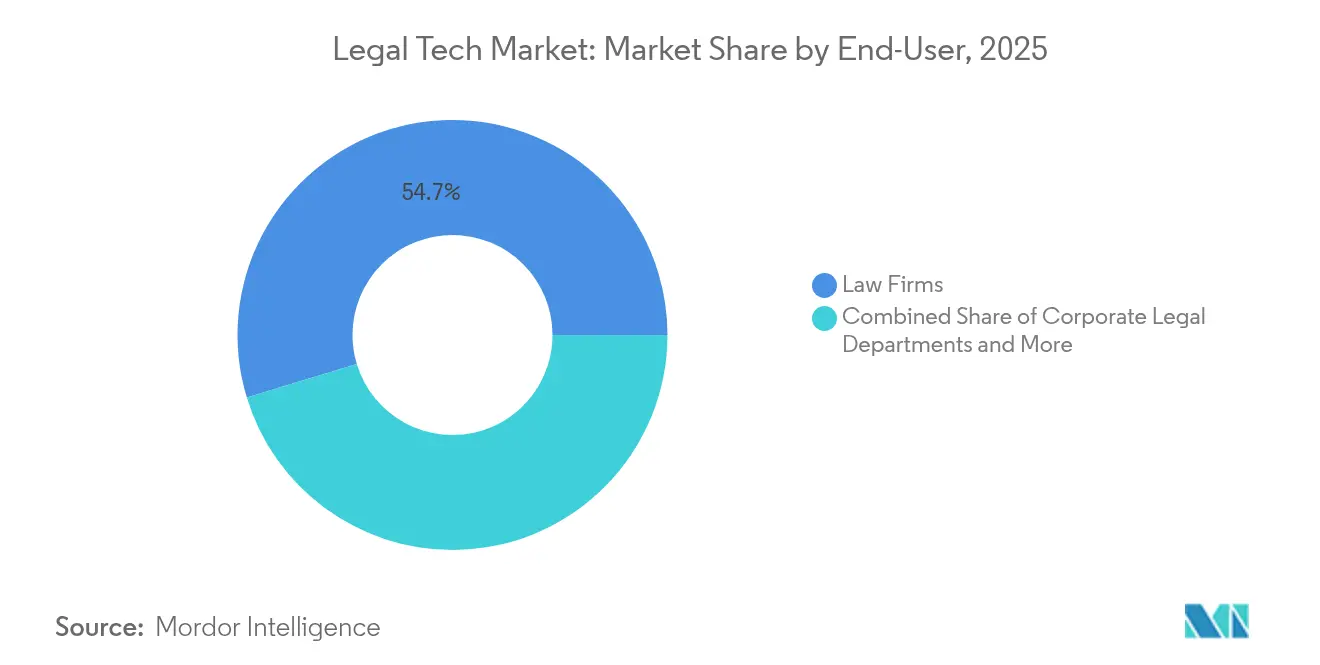

- By end-user, law firms controlled 54.70% of the legal technology market share in 2025, while corporate legal departments record the fastest 14.58% CAGR through 2031.

- By geography, North America led with 38.50% share in 2025; Asia-Pacific is projected to register a 13.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Legal Tech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workflow automation and cost-saving demand | +3.2% | North America, EU, global expansion | Medium term (2-4 years) |

| AI-powered generative contract tools | +4.1% | Developed markets worldwide | Short term (≤ 2 years) |

| Mandatory ESG and privacy compliance | +2.8% | EU lead, spreading to Asia-Pacific and Americas | Long term (≥ 4 years) |

| Remote / hybrid work acceleration | +1.9% | Global post-pandemic | Medium term (2-4 years) |

| Venture-capital inflows into point solutions | +1.5% | North America and EU, emerging Asia-Pacific hubs | Short term (≤ 2 years) |

| Blockchain evidence validation | +0.8% | Advanced digital economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Demand for Workflow Automation and Cost-Savings in Legal Service Delivery

Profits per equity partner rose 11.6% in 2024 even as productivity slipped, underscoring automation’s financial pull. Major firms such as Dechert LLP demonstrate that automating routine drafting and research compresses turnaround times and sustains client pricing confidence. Client preference for flat-fee arrangements—up 34% versus 2016—reinforces the revenue logic for workflow platforms.

Surge in AI-Powered Generative Tools for Contract Drafting and Review

AI now reduces contract-drafting time by up to 90%, freeing lawyers for strategic work[2]Jeff Pruitt, “Generative AI Adoption Jumps Among Legal Teams,” LexisNexis, lexisnexis.com. Thomson Reuters’ CoCounsel illustrates the shift, boosting its legal-segment revenue by 8% in Q1 2025. With 44% of in-house leaders already employing generative AI, mainstream integration has eclipsed pilot-stage testing, compelling firms to rethink hourly billing.

Mandatory ESG and Privacy Compliance Reporting Across Jurisdictions

The EU Corporate Sustainability Reporting Directive now reaches 10,000 non-EU firms, driving adoption of ESG-focused compliance suites. Software such as IBM Envizi helps legal teams manage multi-framework obligations while overcoming data-quality gaps that 60% of finance leaders flag as critical[3]Christina Montgomery, “IBM Envizi Expands ESG Reporting Capabilities,” IBM, ibm.com.

Expansion of Remote / Hybrid Work Models in Legal Practice

With 87% of firms offering remote options, cloud-based practice-management usage has climbed to 75%. Virtual law-firm models flourish in intellectual-property and transactional niches, although mentoring gaps create demand for specialized training platforms.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty and cybersecurity exposure | -2.1% | EU, Asia-Pacific, global | Long term (≥ 4 years) |

| Budget rigidity in small and mid-sized firms | -1.8% | Global, sharpest in emerging markets | Medium term (2-4 years) |

| Fragmented legacy data silos | -1.3% | Mature IT estates | Medium term (2-4 years) |

| Regulatory uncertainty on autonomous advice | -0.9% | Regulated developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Data-Sovereignty and Cybersecurity Liability Exposure

Incidents targeting law firms doubled during 2024, while overlapping regimes such as GDPR and the CLOUD Act complicate cloud deployment. Forty-two percent of legal teams cite security worries as their top AI-adoption barrier, prompting parallel on-premise builds that dilute cloud efficiency gains.

Budget Rigidity Among Small and Mid-Sized Firms

Training costs deter 45% of small practices from new technology, keeping only 24% of firms on a 12-month upgrade path. Vendors counter with tiered SaaS pricing and turnkey onboarding, yet skills gaps and fear of job displacement still prolong adoption cycles in resource-constrained settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Software Dominance Drives Innovation

Software captured 73.80% revenue in 2025, commanding the largest slice of the legal technology market. The segment will expand at a 13.65% CAGR as AI-embedded platforms mature. Thomson Reuters alone pours more than USD 200 million annually into AI enhancements for Westlaw Precision and CoCounsel. Services revenue grows when clients seek integration expertise, but modular SaaS design trims external consulting spend.

The hybrid product-plus-service model is becoming standard. DocuSign’s Intelligent Agreement Management suite blends software with advisory modules, lifting fiscal 2025 revenue to USD 2.98 billion. Such packaging secures recurring revenue while easing change management for law-firm and corporate buyers, reinforcing software’s central role within the legal technology market.

By Deployment Model: Cloud Transformation Accelerates

Cloud-based deployments accounted for 64.90% of the legal technology market size in 2025, reflecting a decisive break from on-premise stacks. A 15.55% forecast CAGR is supported by 75% daily cloud usage among practitioners. Hybrid builds remain relevant where cross-border data flows face legal barriers, providing staging grounds for workload segmentation.

Lower capital outlay and rapid release cycles draw small firms into the legal technology market. Platforms such as Lexis+ deliver AI analytics globally while meeting local data-protection rules. Continuous delivery allows vendors to roll out new contract-analysis algorithms without client-side upgrades, further accelerating adoption.

By Application: Contract Management Emerges as Growth Leader

eDiscovery led 2025 revenue at 24.65%, yet contract lifecycle tools are on track for a 18.35% CAGR, the fastest within the legal technology market. Organizations now favor front-loaded risk mitigation over post-dispute discovery, pushing real-time drafting analytics mainstream. Spellbook’s Microsoft Word plugin flags risk clauses during composition, compressing review cycles.

AI also refines research and analytics, while document-management suites embed machine-learning classifiers to cut filing drudge work. ESG and IP-compliance modules are gaining share, mirroring demand for multi-framework reporting in global enterprises, particularly within highly regulated sectors.

By End-User: Corporate Legal Departments Drive Modernization

Law firms retained a 54.70% hold on the legal technology market share in 2025, but corporate legal departments will grow fastest at 14.58% CAGR to 2031. Ninety-nine percent of in-house teams now use at least one AI tool, with 48% reporting frequent usage. Technology shifts their remit from task execution to strategic risk stewardship.

Alternative legal service providers leverage cloud platforms to offer niche expertise at lower cost, intensifying competition for traditional firms. The resulting diversification widens platform-feature requirements, prompting vendors to expand APIs for specialist workflows and cross-industry integrations.

By Organisation Size: SMEs Accelerate Technology Adoption

Large enterprises held 46.60% share in 2025, grounded in deeper budgets and IT support. Yet small and mid-sized enterprises are forecast to post a 16.45% CAGR, closing the capability gap. After widespread exposure to cloud services, 53% of small firms reported active AI use in 2025. Subscription pricing and intuitive interfaces lower barriers for solo practitioners, injecting fresh growth into the legal technology market.

Vendors now launch “starter” packages that bundle e-signatures, research, and billing into a single dashboard. This bundling provides a runway for upselling advanced analytics as firms scale, making the SME cohort a strategic priority within the broader legal technology industry.

Geography Analysis

North America accounted for 38.50% of the legal technology market size in 2025, supported by early AI uptake and capital availability. Venture-funded challengers such as Harvey AI, reportedly valued at USD 5 billion, add dynamism while spurring incumbents to quicken release cycles. Regulatory clarity around cloud services and mature eDiscovery precedents continue to encourage platform spending.

Asia-Pacific is projected to expand at a 13.95% CAGR, the fastest regional pace, as governments promote digital transformation in professional services. Japan’s drive to boost service-sector exports and nurture start-up ecosystems underscores the region’s growth logic. Rising cross-border commerce further elevates demand for multilingual contract-management tools calibrated to varied legal frameworks.

Europe’s growth remains steady, buttressed by sweeping ESG mandates and a unified data-privacy regime that accelerates compliance-software uptake. Meanwhile, the Middle East and Africa show emerging interest as legal systems modernize, though infrastructure gaps and budget limits temper immediate acceleration. Latin America, led by Brazil and Mexico, forms a nascent opportunity pool where economic stabilization and legal-reform agendas could unlock further platform adoption.

Competitive Landscape

The legal technology market displays moderate concentration, with established players actively consolidating AI talent. Thomson Reuters invested more than USD 200 million in AI during 2025 and acquired SafeSend for USD 600 million to extend workflow coverage ThomsonReuters. RELX reports 7% underlying revenue growth for its Lexis division, propelled by Lexis+ analytics rollouts. DocuSign moves beyond e-signatures into integrated agreement management, securing USD 2.98 billion fiscal-year revenue.

Disruptors shape the next competitive wave. Harvey AI prototypes generative-advice engines for Big Law, while Midpage raised USD 6.2 million to improve legal research usability LawNext[1]Karen Sloan, “Harvey AI in USD 5 Billion Valuation Talks,” Reuters, reuters.com. White-space opportunities include ESG dashboards layered over legal data, jurisdiction-aware data-sovereignty tools, and predictive litigation-risk scoring for insurers. Expect more acquisitions as incumbents race to lock in specialized capabilities and defend platform breadth.

Vendor strategy increasingly centers on open-API ecosystems and modular AI components. This architecture lets clients mix best-of-breed functions without high switching costs, pressuring suite providers to blend flexibility with integrated user experiences. Support services and domain-specific training content emerge as differentiators as technology adoption rates converge across firm sizes.

Global Legal Tech Industry Leaders

Thomson Reuters

RELX (LexisNexis)

Clio (Themis Solutions)

DocuSign

Relativity

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Midpage raised USD 4 million in seed funding and launched Proposition Search to strengthen legal-research relevancy.

- May 2025: RELX’s Decisis service doubled its bar-association partnerships, broadening reach across 20 associations.

- April 2025: Keplera secured EUR 770,000 (USD 825,000) to expand LexHero, its AI-driven document-management platform.

- March 2025: LexisNexis introduced Protégé, the first personalized voice-AI legal assistant, enhancing reasoning depth in research queries.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global legal tech market as all revenues earned from purpose-built software and related support services that streamline, automate, or augment legal workflows in law firms, corporate legal departments, courts, and alternative legal service providers. This includes e-discovery, contract lifecycle management, legal research and analytics, document/practice management, compliance, and IP tools delivered via cloud, on-premise, or hybrid deployments.

Scope Exclusion: Hardware or purely advisory legal services that do not bundle proprietary software are outside the remit.

Segmentation Overview

- By Solution

- Software

- Services

- By Deployment Model

- Cloud-Based

- On-Premise

- Hybrid

- By Application

- eDiscovery

- Contract Lifecycle Management

- Legal Research and Analytics

- Document and Practice Management

- Compliance / Risk and IP Management

- By End-User

- Law Firms

- Corporate Legal Departments

- Government and Regulatory Bodies

- Alternative Legal Service Providers

- Others

- By Organisation Size

- Large Enterprises

- Small and Mid-Sized Enterprises (SMEs)

- Solo Practitioners

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Middle East and Africa

- GCC

- Israel

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia

- New Zealand

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conduct semi-structured interviews with software vendors' product leads, managing partners at mid-size law firms across North America, Europe, and Asia-Pacific, as well as corporate counsels in finance and life sciences. These discussions test unit economics, average seat prices, and rollout timelines, helping us close data gaps and recalibrate preliminary desk estimates.

Desk Research

We begin by mapping the universe of legal-tech offerings using public sources such as the Administrative Office of U.S. Courts filings, European Commission e-Justice statistics, the International Legal Technology Association's annual surveys, and patent data retrieved through Questel. Company 10-Ks, investor decks, and regional bar association reports supplement adoption and pricing signals. Subscription access to D&B Hoovers and Dow Jones Factiva provides revenue splits and recent deal activity, which are then reconciled with customs shipment hints for on-premise appliances.

Next, trend indicators, for example, cloud migration ratios from OECD ICT tables or venture capital flows tracked by Crunchbase, are scraped to gauge technology penetration across regions. These diverse strands are cataloged in a source matrix; however, many additional public records and proprietary datasets were also consulted during evidence collection.

Market-Sizing & Forecasting

A top-down demand pool is built from regional legal services spend, lawyer headcount, and cloud adoption rates, which are then multiplied by verified penetration ratios for each application cluster; bottom-up cross-checks using sampled annual subscription price multiplied by active user counts confirm plausibility. Variables such as average e-discovery data volume, contract digitization rates, cybersecurity compliance mandates, venture funding momentum, and SaaS price erosion feed a multivariate regression that projects revenue through 2030. Where respondent data are sparse, proxy metrics, for instance, attorney-to-paralegal ratios, plug interim gaps before iterative balancing.

Data Validation & Update Cycle

Outputs pass tri-layer variance checks, peer review, and anomaly flags. We refresh every twelve months, with mid-cycle revisions triggered by sizable M&A, regulatory shifts, or pricing shocks, ensuring clients always receive the latest vetted view.

Why Our Legal Tech Baseline Commands Reliability

Published estimates differ because each publisher tweaks the solution list, geographic roll-ups, and forecasting levers. Some favor historic deal counts, while others extrapolate user licenses; currency conversions and refresh cadence add more spread.

Key gap drivers include (a) exclusion of support services revenue, (b) inclusion of adjacent reg-tech tools, or (c) overly aggressive seat growth assumptions not validated through interviews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 34.15 B (2025) | Mordor Intelligence | - |

| USD 33.07 B (2024) | Global Consultancy A | Narrower product taxonomy plus optimistic growth coefficients |

| USD 28.72 B (2025) | Industry Journal B | Omits services revenue; relies on historic deal counts |

| USD 32.98 B (2025) | Regional Observatory C | Adds adjacent reg-tech; limited primary validation |

In summary, by grounding scope rigorously, validating assumptions with direct market voices, and blending complementary sizing techniques, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current valuation of the legal technology market?

The legal technology market size stands at USD 38.67 billion in 2026 and is forecast to reach USD 71.95 billion by 2031.

Which segment is growing fastest within the market?

Contract lifecycle management applications show the highest 18.35% CAGR to 2031 as organizations prioritize proactive risk management.

Why are cloud deployments dominant?

Cloud models captured 64.90% share in 2025 because they enable remote work, lower capital costs, and speed feature upgrades without on-premise maintenance.

How quickly is Asia-Pacific growing?

Asia-Pacific is projected to expand at a 13.95% CAGR through 2031, driven by digital-transformation policies and rising cross-border legal complexity.

What are the main challenges to adoption for small firms?

Budget constraints and training costs deter 45% of small practices, though tiered SaaS pricing and user-friendly interfaces are narrowing the gap.

Which technologies are most influential right now?

Generative AI for drafting and AI-powered contract-analysis tools are transforming workflows, cutting drafting time by up to 90% and reshaping billing models.

Page last updated on: