Market Overview

| Study Period | 2021 - 2031 |

|---|---|

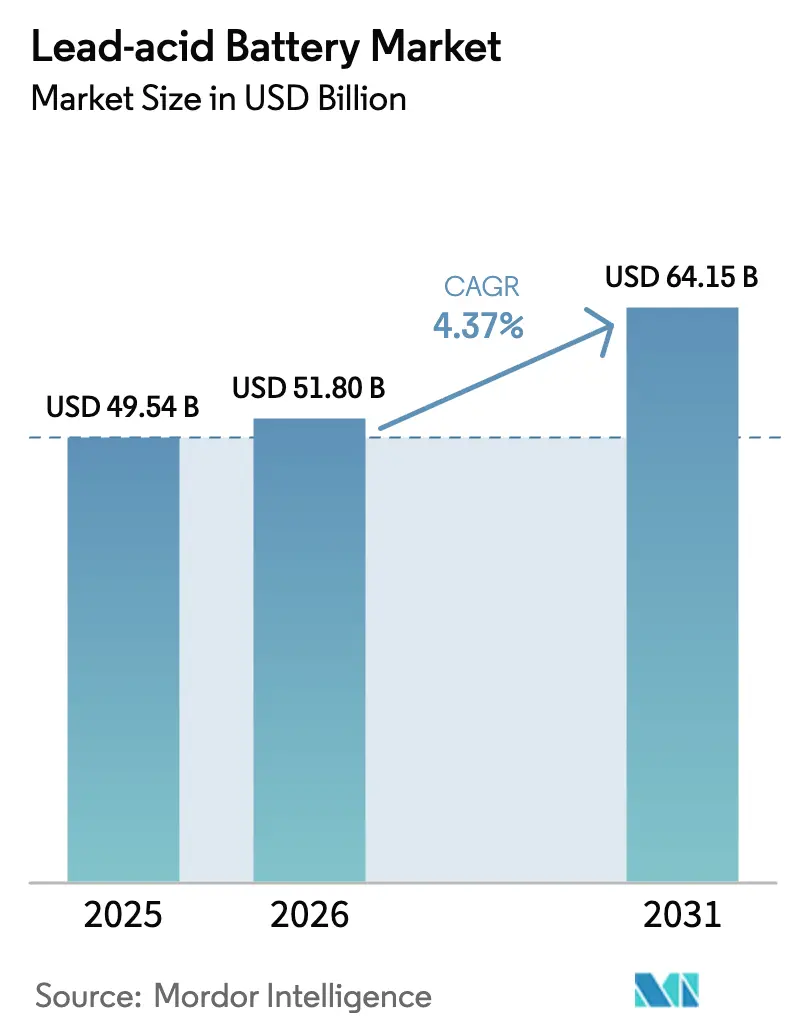

| Market Size (2026) | USD 51.80 Billion |

| Market Size (2031) | USD 64.15 Billion |

| Growth Rate (2026 - 2031) | 4.37% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lead-Acid Battery Market Analysis by Mordor Intelligence

The Lead-Acid Battery Market size is projected to expand from USD 49.54 billion in 2025 and USD 51.80 billion in 2026 to USD 64.15 billion by 2031, registering a CAGR of 4.37% between 2026 to 2031.

Mature chemistry, wide service networks, and strong price-to-performance ratios keep the technology relevant even as lithium-ion costs fall. Premium valve-regulated lead-acid (VRLA) formats continue to win share because they satisfy automotive start-stop, telecom uptime, and data-center backup requirements without routine maintenance. Aftermarket demand from the 1.4 billion internal-combustion and hybrid vehicles on the road underpins recurring sales, while stationary growth comes from telecom densification and edge data-center build-outs in emerging regions. On the risk side, tightening environmental regulations and the accelerating economic case for lithium-ion batteries are increasing compliance costs and spurring product upgrades. Intensifying consolidation, led by Brookfield’s USD 13.2 billion purchase of Clarios in 2024, signals that scale, recycling integration, and premium chemistries define sustainable advantage in the lead acid battery market.[1]Reuters Staff, “Brookfield Completes USD 13.2 Billion Acquisition of Clarios,” Reuters, reuters.com

Key Report Takeaways

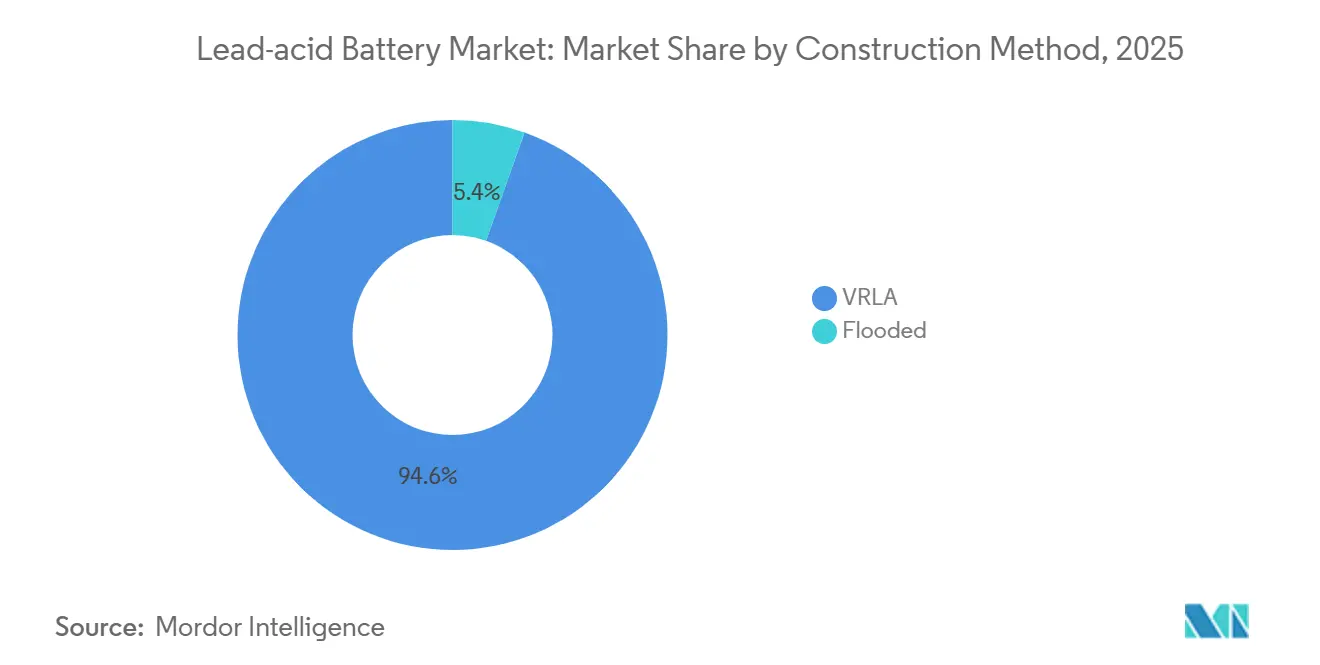

- By construction method, VRLA captured 94.57% of revenue in 2025 and is forecast to grow at a 5.51% CAGR through 2031, while flooded designs represented the remainder.

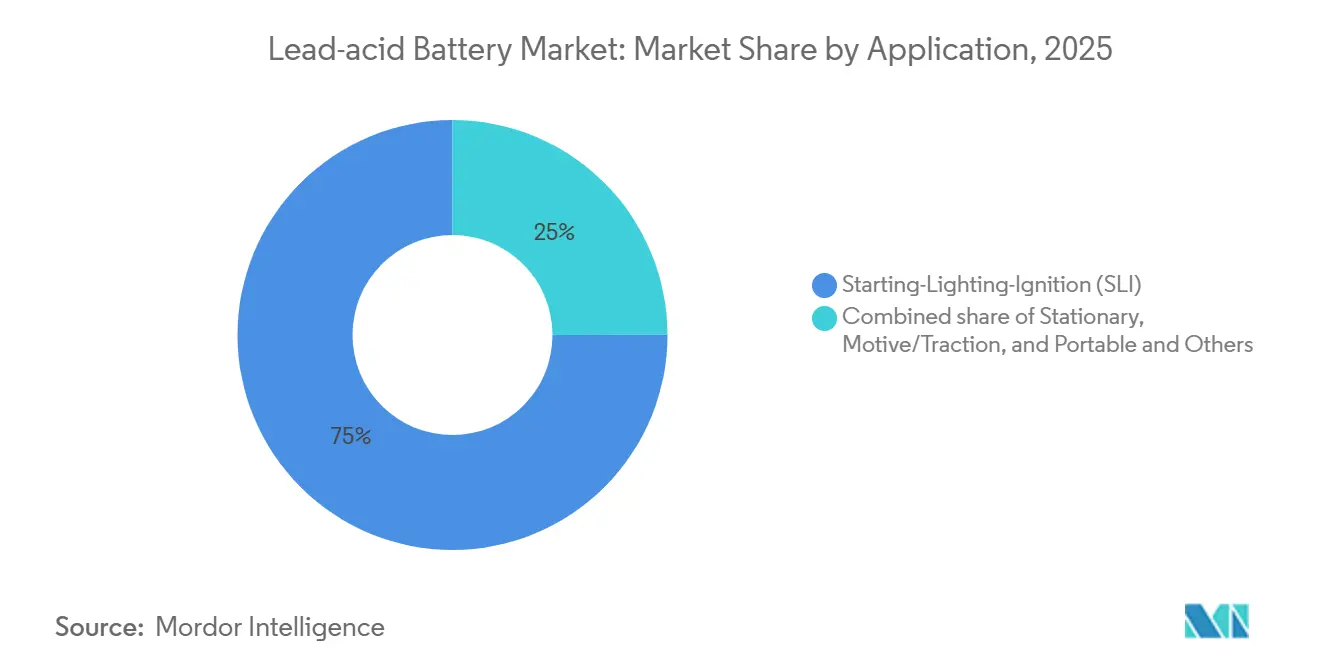

- By application, starting-lighting-ignition batteries accounted for 75.01% of shipments in 2025; the stationary segment is advancing at a 5.61% CAGR to 2031.

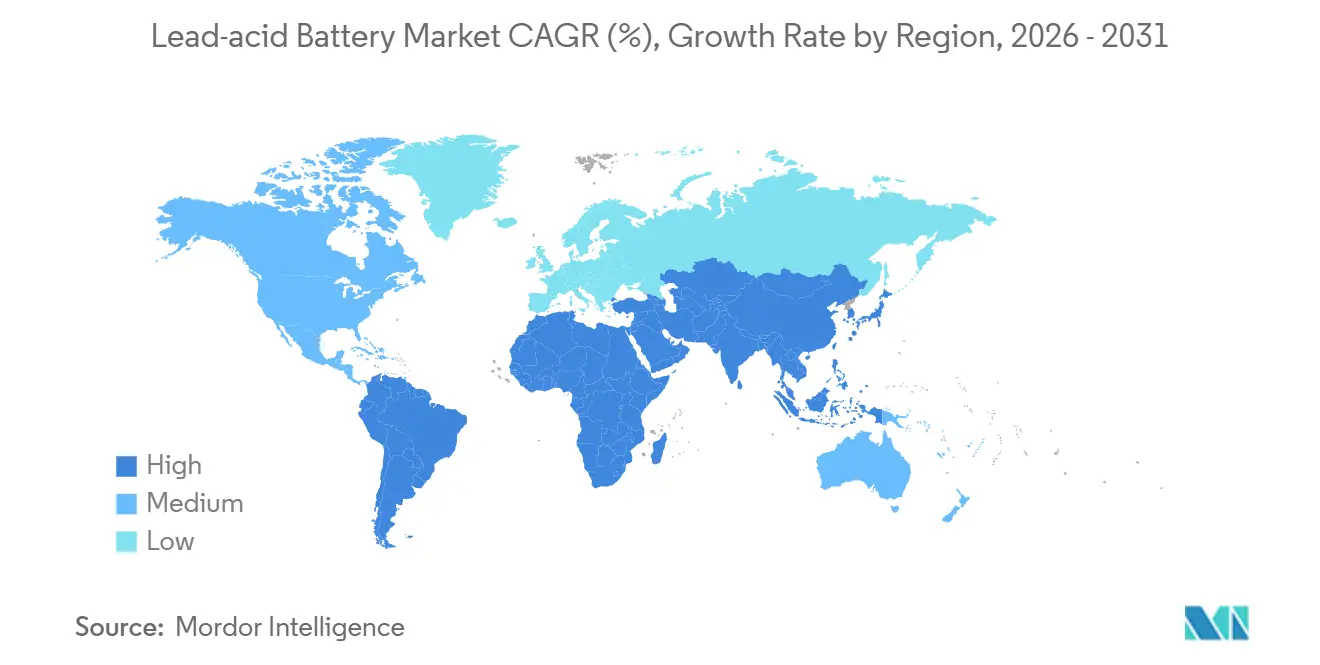

- By geography, Asia-Pacific generated 52.59% of global volume in 2025, and the region is set to register the fastest growth at 4.83% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Lead-Acid Battery Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE-vehicle parc replacement demand remains resilient | +1.2% | Global, notably North America, Europe, China, India | Long term (≥ 4 years) |

| Telecom network densification in emerging Asia & Africa | +0.9% | APAC, Sub-Saharan Africa, Middle East | Medium term (2-4 years) |

| Data-center UPS build-outs in tier-2 cities | +0.6% | APAC, Latin America, MEA | Medium term (2-4 years) |

| Aftermarket lock-in for micro-hybrid SLI batteries | +0.8% | North America, Europe, China | Long term (≥ 4 years) |

| “Smart-mixing” additives extending flooded-cell life | +0.4% | China, India, Brazil | Medium term (2-4 years) |

| Low-speed EV demand in LMICs | +0.5% | India, ASEAN, Africa, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

ICE-Vehicle Parc Replacement Demand Remains Resilient

Internal-combustion and hybrid vehicles are predicted to dominate the global fleet well into the next decade, securing a steady replacement cycle for lead-acid batteries. More than 50 million vehicles equipped with absorbent-glass-mat (AGM) batteries required aftermarket replacements in 2025, and this figure will rise as start-stop penetration deepens. China’s 280 million-unit vehicle parc and India’s 280 million registered vehicles represent substantial reservoirs where battery life averages four years in tropical climates and five years in temperate zones. Consolidation toward DIN-standard sizing in Europe simplifies distributor inventory yet raises replacement costs, creating margin upside for incumbents that control supply chains. These fundamentals keep the lead acid battery market anchored in the automotive aftermarket despite the rise of electric vehicles.[2]EnerSys, “ODYSSEY Battery: The Ultimate Power Source,” enersys.com

Telecom Network Densification in Emerging Asia & Africa

Unreliable grids drive telecom operators to rely on lead-acid batteries for base-station uptime. India’s 400,000 towers face daily outages exceeding eight hours and therefore deploy battery banks rated 300-900 ampere-hours to bridge diesel-generator switchover periods.[3]International Telecommunication Union, “ITU-T Recommendation L.1384,” itu.int Sub-Saharan Africa, where 88% of sites are off-grid or bad-grid, opts for sealed VRLA units because theft concerns and thermal-runaway risks restrict lithium-ion adoption. ASEAN nations are adding up to 15,000 towers annually, specifying lead-acid for rural deployments that require low capital investment and straightforward recycling. This persistent demand supports steady shipment growth even as lithium-ion captures urban installations.

Data-Center UPS Build-Outs (Tier-2 Cities)

Edge computing expansion in second-tier urban centers sustains stationary battery demand. Lithium-ion already commands 30-40% of new edge deployments due to footprint and lifecycle savings, yet VRLA retains a niche in retrofits and cost-sensitive projects where grid stability is marginal but acceptable. The U.S. Department of Energy notes that lead-acid historically supplied 95% of UPS capacity, a share now declining in primary hubs but holding in smaller facilities. In India, Indonesia, and Brazil, data-center developers continue to select VRLA for 15-30-minute backup durations because the lower upfront cost offsets higher replacement frequency. Continued power-quality gaps in these regions delay wholesale substitution.

Aftermarket Revenue Lock-In for Micro-Hybrid SLI Batteries

Start-stop systems embed premium chemistries in the vehicle parc, locking users into AGM and enhanced-flooded battery (EFB) replacements every three to five years. More than half of new vehicles sold in Europe and North America in 2024 featured start-stop technology, pushing AGM average selling prices to two or three times those of flooded cells. Leading OEM suppliers leverage branded channels to capture this captive aftermarket, and independent repair shops often lack diagnostics to downgrade to lower-cost options. The resulting margin resilience helps offset volume attrition in entry-level segments, reinforcing the value proposition of the lead acid battery market for investors and strategists.

Restraints Impact Analysis of Lead-Acid Battery Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithium-ion cost curve crossing below USD 70 kWh | -0.8% | Global, earliest in North America, Europe, China | Medium term (2-4 years) |

| Stricter EU end-of-life lead limits | -0.5% | Europe, spillover to export markets | Long term (≥ 4 years) |

| Insurance risk premiums for urban recycling clusters | -0.3% | North America, Europe | Medium term (2-4 years) |

| Graphene-enhanced AGM cannibalizing conventional VRLA | -0.4% | China, Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lithium-Ion Cost Curve Crossing Below USD 70 kWh for Automotive

Lithium-ion battery pack prices declined to USD 115 kWh in 2024 and are projected to fall to USD 80 kWh by 2026, closing the total-cost-of-ownership gap in starter and motive-power use cases. Goldman Sachs pegs full drivetrain parity with internal-combustion engines at USD 80 kWh, a threshold that accelerates electric-vehicle adoption and shrinks the captive SLI aftermarket. Chinese suppliers such as CATL and BYD already achieve cell-level costs below USD 75 kWh through vertical integration and scale efficiencies, putting additional pressure on lead-acid producers. McKinsey forecasts lithium-ion will secure 60-70% of the motive-power segment by 2030 as operators prioritize fast charging and higher energy density. The impending cost crossover removes lead-acid’s historic advantage, low upfront price, forcing manufacturers to compete on service life, collection infrastructure, and regulatory compliance instead.

Stricter EU End-of-Life Lead Limits

The European Union’s Battery Regulation 2023/1542 mandates collection targets of 63% by 2027 and 73% by 2030, while requiring 70% lead recovery efficiency by 2030. Digital battery passports, compulsory from 2027, will log carbon footprint, recycled-content share, and disposal pathway for every unit, increasing compliance costs for firms lacking closed-loop systems. Extended producer responsibility provisions shift end-of-life liabilities onto battery makers, compressing margins for non-integrated suppliers. Restrictions on hazardous substances and mandatory carbon-footprint disclosures further raise barriers to imports from regions with looser standards. The U.S. Environmental Protection Agency is drafting parallel rules that tighten lead-exposure limits and heighten environmental-justice scrutiny for urban smelters. Together, these policies erode lead-acid’s competitiveness relative to lithium-ion, which avoids toxic-metal recovery and benefits from simpler recycling logistics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Lead-Acid Battery Market Segment Analysis

By Construction Method:

VRLA Dominance Reflects Maintenance-Free ImperativeVRLA batteries commanded 94.57% of 2025 revenue, and the segment is forecast to compound at 5.51% to 2031. Premium AGM variants deliver 20-30% longer service life and tolerate partial-state-of-charge cycling, making them essential for micro-hybrid vehicles and telecom sites. Graphene-enhanced AGM designs further raise durability, extending cycle life by about 25% in lab tests.[4]Journal Editors, “Graphene-Enhanced Lead-Acid Batteries: A Review,” Journal of Power Sources, journals.elsevier.com The lead acid battery market size for VRLA products is therefore positioned to outpace the overall average.

Flooded batteries held the remaining 5.43% share in 2025. They persist in price-sensitive stationary and motive-power niches where maintenance labor is inexpensive. Carbon and graphene additives now allow 500-700 cycles at 50% depth-of-discharge, matching early VRLA performance at 60–70% of the cost. This technical catch-up keeps flooded chemistry viable, particularly in rural telecom installations across Sub-Saharan Africa and South Asia.

By Application:

SLI Aftermarket Anchors Volume, Stationary Drives GrowthStarting-lighting-ignition batteries represented 75.01% of shipments in 2025, buoyed by the huge global vehicle fleet. The segment accounts for the bulk of lead acid battery market share and remains a profit engine thanks to premium AGM and EFB replacements. Electric-vehicle adoption is eroding entry-level flooded demand, but the embedded base of micro-hybrid vehicles preserves volume through the forecast horizon.

Stationary applications are growing at a 5.61% CAGR, led by telecom densification and edge data-center expansion. The lead acid battery market size in stationary use cases is translating into incremental revenue despite lithium-ion competition. Motive and traction formats face faster substitution because logistics operators value fast charging and high energy density, yet lead-acid sustains presence in low-utilization fleets and developing-market forklifts.

Geography Analysis

APAC Lead-acid Battery Market

Asia-Pacific generated 52.59% of global revenue in 2025 and will grow at 4.83% a year to 2031. China combines a vast vehicle parc, strong start-stop uptake, and policy-driven recycling mandates that favor domestic vertically integrated producers. India’s aftermarket offers significant upside, driven by short replacement cycles and a rising share of premium chemistries. ASEAN markets add thousands of new telecom towers each year, most of which specify VRLA batteries due to capital constraints and established recycling routes.[5]GSMA Intelligence, “The Mobile Economy: Sub-Saharan Africa 2020,” gsma.com

North America and Europe Lead-acid Battery Market

North America exhibits moderate expansion because electric vehicles reduce flooded SLI volume, yet aftermarket resilience persists thanks to 50% start-stop penetration in new-car sales. Recycling compliance costs are climbing as the U.S. Environmental Protection Agency tightens lead exposure limits for urban smelters. Europe faces similar regulatory pressures under the Battery Regulation 2023/1542, which stipulates 70% lead recovery by 2030 and digital battery passports by 2027. Faster EV adoption in Germany, France, and the United Kingdom accelerates SLI volume erosion, but premium AGM replacements boost average selling prices.

South America and MEA Lead-acid Battery Market

South America and the Middle East & Africa remain opportunity regions. Brazil’s 50 million-vehicle parc and low EV penetration favor conventional and premium lead-acid formats, although economic volatility occasionally lengthens replacement cycles. Sub-Saharan Africa relies on lead-acid for 88% of base-station sites, citing theft risk and cost barriers to lithium-ion. Gulf Cooperation Council states and South Africa continue to install VRLA UPS systems for data-center expansions linked to digital-economy strategies. Across these regions, established collection and recycling networks reinforce the incumbency of the Lead-Acid Battery Market.

Competitive Landscape

The top five manufacturers, Clarios, Exide Technologies, EnerSys, GS Yuasa, and East Penn Manufacturing, collectively control about 45% of global revenue. Brookfield’s acquisition of Clarios underscores the strategic value of large aftermarket channels and closed-loop recycling assets. EnerSys is scaling thin-plate pure-lead (TPPL) capacity to defend motive-power share where lithium-ion competition is intensifying. GS Yuasa is partnering with a major automaker to boost AGM durability for 48-volt mild-hybrid systems.

Chinese suppliers such as Chaowei, Tianneng, and Camel Group leverage carbon-additive formulations to lift flooded-cell life and compete on price in electric-bicycle and low-speed vehicle markets. Compliance with emerging digital-passport and lead-recovery rules is becoming a differentiator, encouraging vertical integration of recycling. Barriers to entry also stem from the 99% material-recovery rate already achieved by established smelters, which new entrants find costly to replicate. Overall, the market is moving toward moderate concentration, structured around recycling infrastructure, premium chemistries, and geographic expansion into high-growth emerging regions.

Lead-Acid Battery Industry Leaders

GS Yuasa Corporation

EnerSys

East Penn Manufacturing Co.

Clarios

Exide Technologies

- *Disclaimer: Major Players sorted in no particular order

Lead-Acid Battery Market Companies Covered in this Report

- Clarios

- Exide Technologies

- EnerSys

- GS Yuasa Corp.

- East Penn Manufacturing

- Panasonic

- Amara Raja Batteries

- C&D Technologies

- Leoch International

- Chaowei Power

- Narada Power

- NorthStar Battery

- Crown Battery

- Trojan Battery

- Camel Group

- FIAMM Energy Technology

- Hitachi Chemical

- HOPPECKE

- Shuangdeng (Sacred Sun)

- Sunlight Group

Recent Industry Developments in Lead-Acid Battery Market

- May 2025: Clarios began site selection for a USD 1 billion U.S. recovery plant that targets improved recycling efficiency and reduced dependency on imported antimony.

- March 2025: Clarios announced a USD 6 billion American Energy Manufacturing Strategy to scale U.S. low-voltage battery output, including USD 2.5 billion for advanced production lines and USD 1.9 billion for critical minerals processing.

- August 2024: Clarios committed EUR 200 million to boost European AGM capacity by 50% between 2022 and 2026, creating 150 jobs across four countries.

- June 2024: Clarios completed a USD 16 million upgrade to its AGM component plant in South Carolina, expanding output for modern vehicles.

Global Lead-Acid Battery Market Report Scope

The lead-acid battery is a rechargeable battery that consists of two electrodes submerged in an electrolyte of sulfuric acid. The positive electrode is made of grains of metallic lead oxide, while the negative electrode is attached to a grid of metallic lead.

The Lead-Acid Battery Market is segmented by construction method (flooded and VRLA), application [SLI (starting, lighting, and ignition), stationary (telecom, UPS, energy storage systems (ESS), etc.), motive/traction (forklifts, golf-carts), and portable and others (consumer electronics, etc.)], and geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The report offers the market size and forecasts in terms of revenue in USD billion for all the above segments.

Segmentation Overview

By Construction Method

| Flooded |

| VRLA |

By Application

| Starting-Lighting-Ignition (SLI) |

| Stationary |

| Motive/Traction (Forklifts, Golf-carts) |

| Portable and Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Construction Method | Flooded | |

| VRLA | ||

| By Application | Starting-Lighting-Ignition (SLI) | |

| Stationary | ||

| Motive/Traction (Forklifts, Golf-carts) | ||

| Portable and Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the lead acid battery market in 2026?

It is projected to reach USD 51.80 billion in 2026.

Which construction method dominates shipments?

Valve-regulated lead-acid units account for nearly 95% of global revenue thanks to maintenance-free operation and compatibility with start-stop vehicles.

What segment drives future growth?

Stationary batteries for telecom and edge data-center backup are expanding at 5.61% CAGR through 2031.

Why is Asia-Pacific the largest region?

The region hosts the biggest vehicle fleets, rapid telecom tower additions and supportive recycling infrastructure, giving it over half of global volume in 2025.

How are regulations affecting manufacturers?

EU and U.S. rules require higher lead-recovery rates and digital tracking, driving consolidation toward players that own closed-loop recycling systems.

Page last updated on: