Law Enforcement Software Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

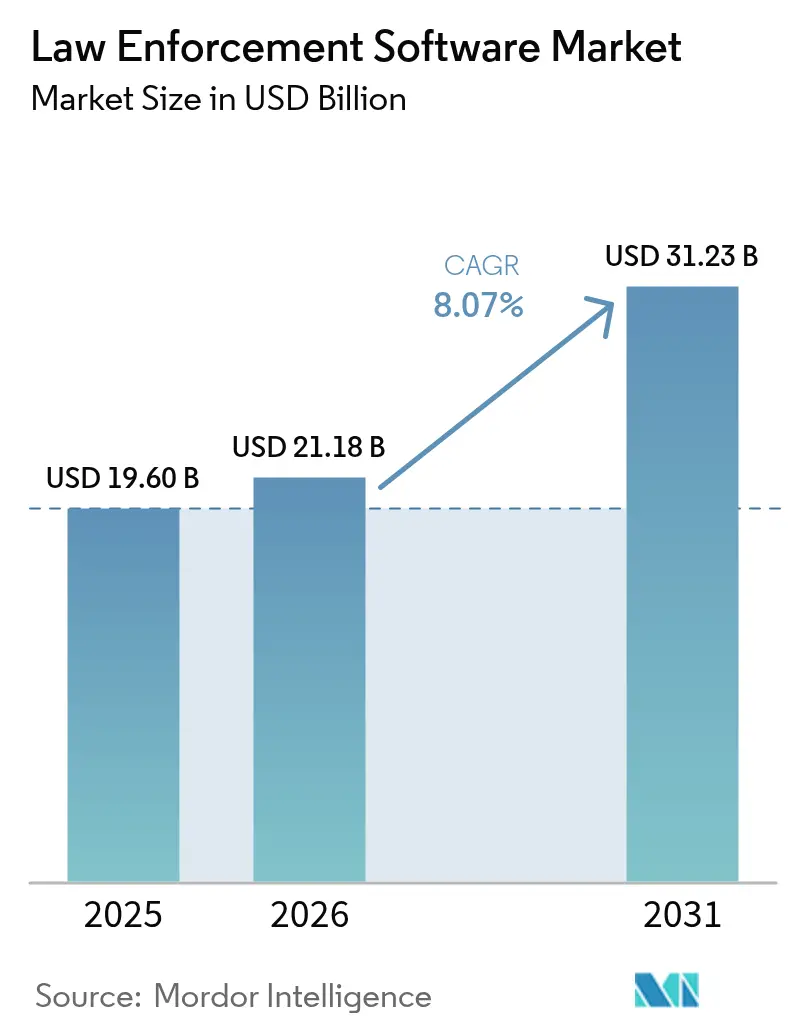

| Market Size (2026) | USD 21.18 Billion |

| Market Size (2031) | USD 31.23 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

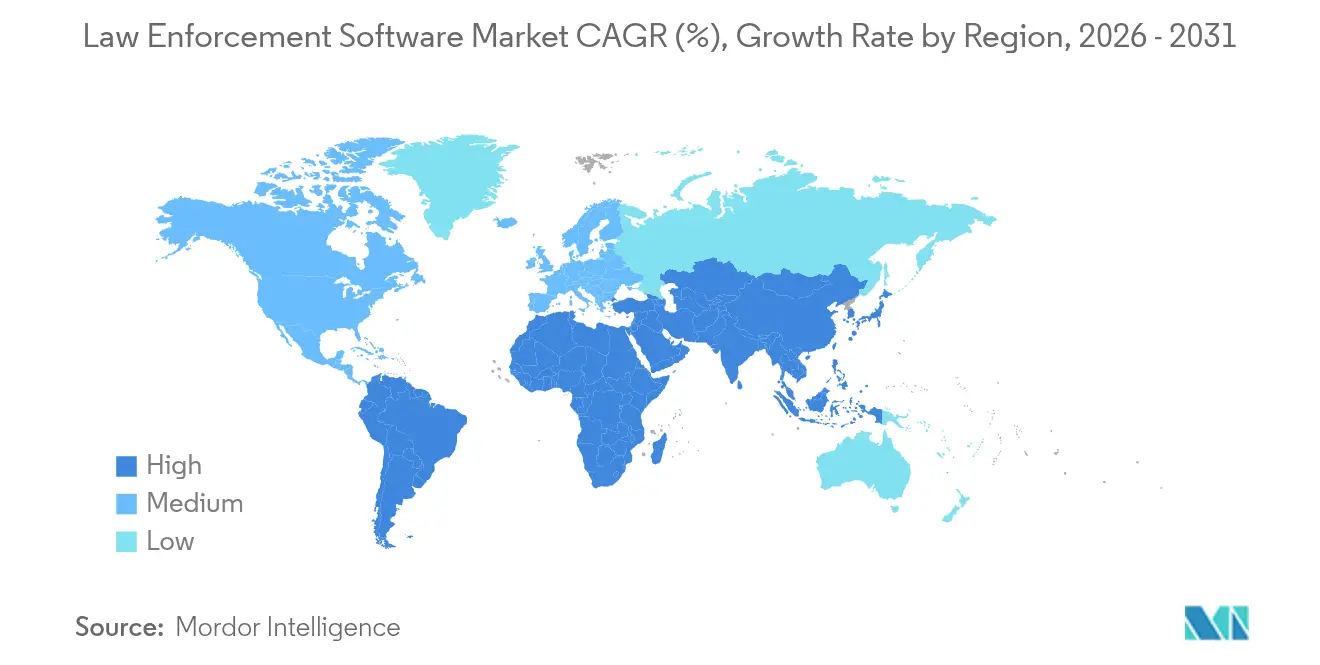

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

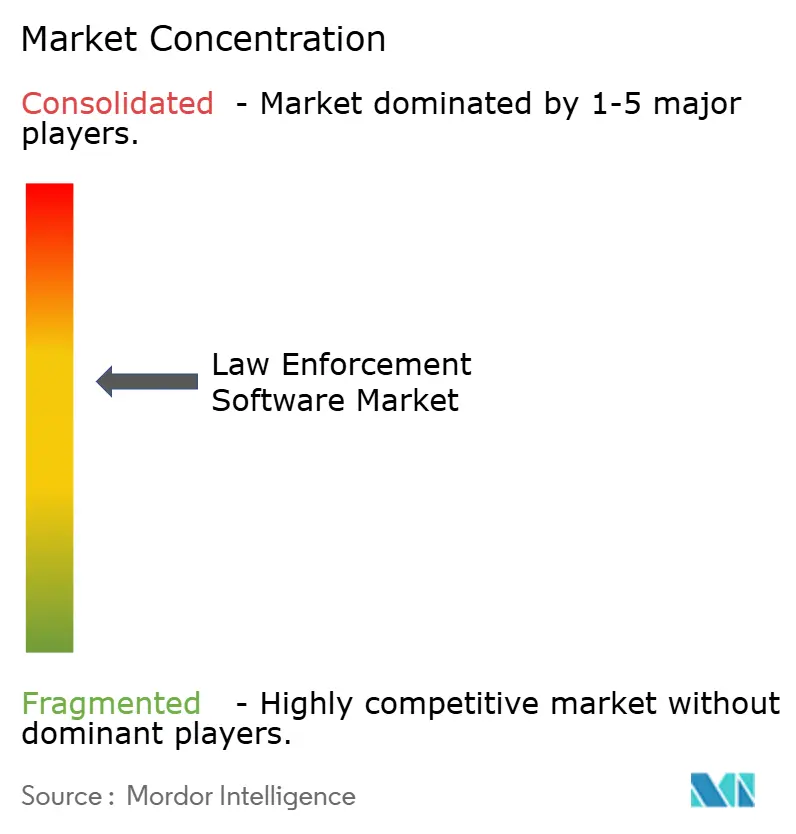

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Law Enforcement Software Market Analysis by Mordor Intelligence

The law enforcement software market size is expected to grow from USD 19.60 billion in 2025 to USD 21.18 billion in 2026 and is forecast to reach USD 31.23 billion by 2031 at 8.07% CAGR over 2026-2031. Continued digitization of policing workflows, mounting data volumes and persistent staffing shortages are pushing public-safety agencies to invest in integrated platforms that automate dispatch, records and evidence administration. Federal stimulus such as the Edward Byrne Memorial Justice Assistance Grant, which assigns USD 419 million to technology improvements in 2025, is compressing replacement cycles and widening access for mid-sized departments.[1]Edward Byrne Memorial Justice Assistance Grant Program, “FY 2025 Allocation,” sam.gov At the same time, cloud-first mandates balanced with sovereign-data requirements are forcing suppliers to build region-specific hosting options that satisfy CJIS as well as EU localization rules. Convergence of predictive analytics, real-time crime centers and body-worn-camera ecosystems is expected to reward vendors delivering end-to-end suites rather than point products, thereby reshaping competitive dynamics over the next decade.

Key Report Takeaways

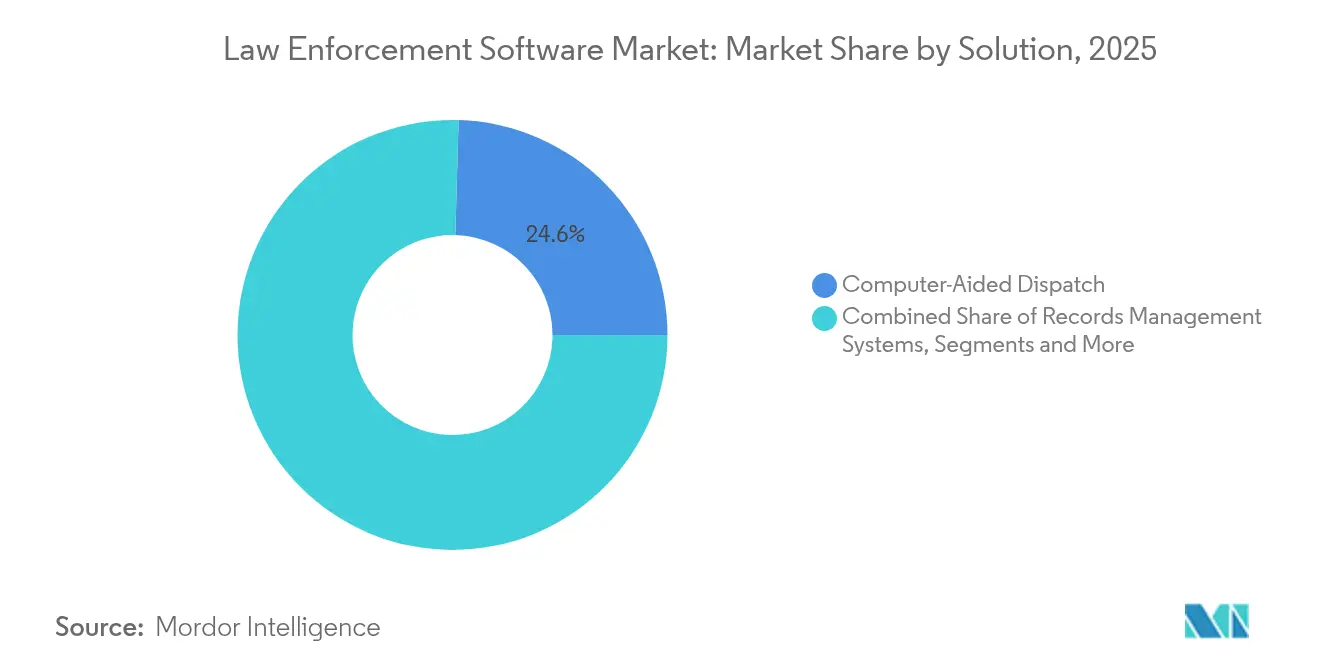

- By solution, computer-aided dispatch platforms led revenue with 24.55% in 2025, while predictive and crime-analytics offerings are projected to expand at a 9.45% CAGR to 2031.

- By deployment, on-premise models held 58.35% of the law enforcement software market share in 2025; cloud deployment is pacing a 10.25% CAGR through 2031.

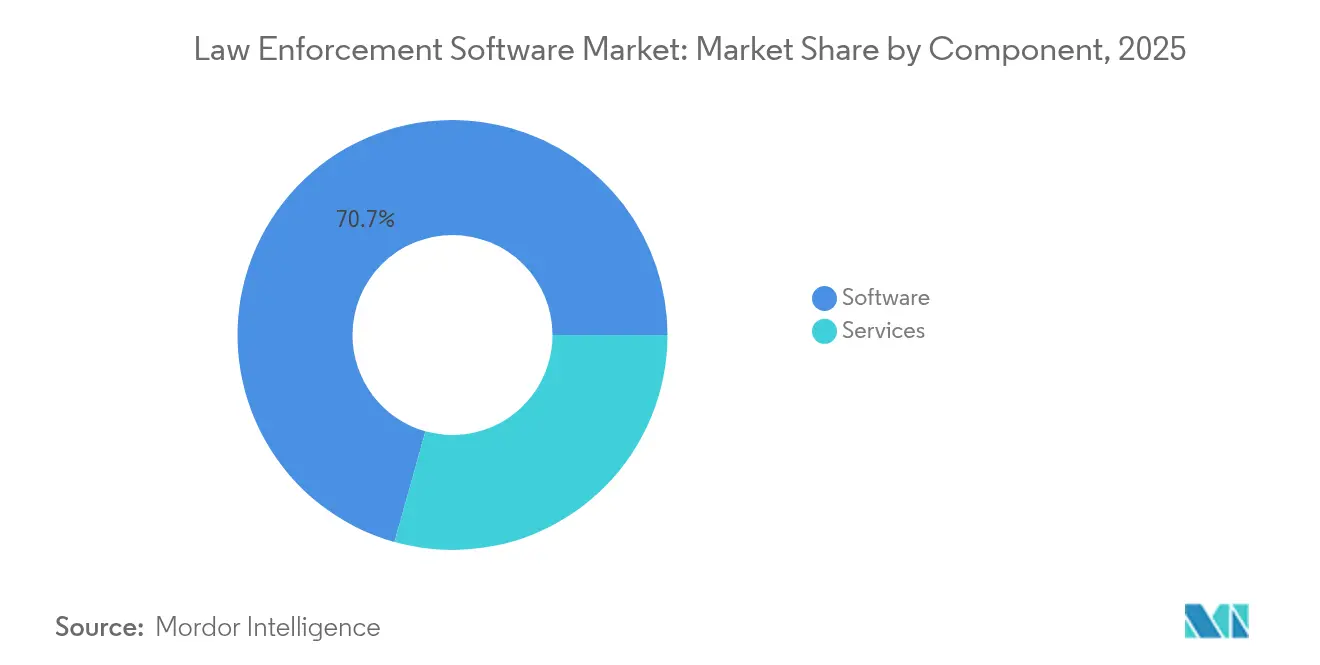

- By component, software captured 70.65% of the law enforcement software market size in 2025, whereas managed services are growing at 9.12% CAGR.

- By end-user, municipal and local agencies accounted for 45.95% of demand in 2025; federal and national police agencies represent the fastest-growing cohort with a 10.02% CAGR to 2031.

- By geography, North America commanded 36.85% of 2025 revenue, yet Asia-Pacific is on course for a 9.42% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Law Enforcement Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of National Real-Time Crime Centers in North America | +1.2% | North America, spill-over to EU | Medium term (2-4 years) |

| Mandatory Body-Worn-Camera Evidence-Management Mandates in Europe | +0.9% | Europe core, adoption in APAC | Short term (≤ 2 years) |

| Federal Grant Acceleration for Cloud-First Public-Safety Platforms (U.S.) | +1.5% | North America, influence on global procurement | Short term (≤ 2 years) |

| Asia-Pacific Smart-City Spend Pivoting to Public-Safety Software | +1.1% | APAC core, early adoption in MEA | Medium term (2-4 years) |

| Inter-agency Data-Sharing Frameworks Boosting CAD/RMS Upgrades (U.K.) | +0.8% | Global, with early gains in UK, EU | Long term (≥ 4 years) |

| Digital-Evidence Backlogs Driving AI Video-Analytics Investments | +1.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of National Real-Time Crime Centers in North America

Real-time crime centers are evolving from reactive monitoring hubs into predictive-intelligence platforms that merge body-worn-camera streams, license-plate recognition and social-media feeds to deliver situational awareness within seconds. The Los Angeles Police Department’s deployment of premier CAD and Command Point mobile systems illustrates how large agencies centralize call-taking and field coordination. [2]Los Angeles Police Department, “New Premier Computer-Aided Dispatch and Command Point Mobile Systems,” lapdonline.orgFollow-on investments such as Motorola Solutions’ USD 12 million command-center order with the Las Vegas Metropolitan Police Department underscore the momentum behind integrated intelligence hubs. Federal incentives are amplifying uptake; the COPS Technology and Equipment Program allocated USD 247 million in 2024 to extend advanced command-center capabilities to smaller jurisdictions. As more centers embed AI models for pattern detection, agencies report double-digit gains in response precision and officer safety.

Mandatory Body-Worn-Camera Evidence-Management Mandates in Europe

European regulators now require comprehensive video workflows that link officer-worn devices with CJIS-compliant digital-evidence vaults. Puerto Rico’s expansion of Axon Body 4 cameras, featuring live-streaming and geolocation, demonstrates how functionality has shifted beyond accountability toward real-time officer support. New procurement frameworks in the United Kingdom for live facial-recognition modules further widen addressable demand, accelerating vendor innovation in automated redaction, transcription and metadata tagging. Competing suppliers are fast-tracking AI-assisted report-writing tools that can summarise multi-hour footage in minutes, freeing detectives to focus on investigative tasks.

Federal Grant Acceleration for Cloud-First Public-Safety Platforms (U.S.)

Washington’s cloud-first doctrine is reshaping procurement as agencies move mission systems to FedRAMP-authorized SaaS environments. The FBI’s USD 85 million contract for Criminal Justice Information Services operational services validates federal appetite for elastic compute that scales investigative workloads on demand. Complementing agency contracts, the Department of Homeland Security earmarked USD 836.1 million in its 2025 Science & Technology budget for advanced computing and information-security research that directly benefits public-safety software.[3]Federal DHS, “Science and Technology Directorate Budget FY 2025,” dhs.gov These allocations lower technical-risk perceptions, encouraging smaller municipalities to adopt cloud records-management platforms that stay online during hurricanes or wildfires.

Asia-Pacific Smart-City Spend Pivoting to Public-Safety Software

Smart-city budgets once dominated by traffic and environmental sensors now prioritise integrated public-safety stacks that unify video analytics, emergency-alerting and predictive policing. Japan’s Crime Nabi AI system achieved a 69% drop in metal-cable theft during international pilots, signalling regional leadership in machine-learning crime deterrence.[4]Government of Japan, “AI-Based Crime Prediction System,” japan.go.jpSouth Korea’s Incheon Free Economic Zone pairs intelligent CCTV with abnormal-sound detection to deliver always-on urban monitoring at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Procurement Cycles in Municipal Agencies | -0.7% | Global, particularly acute in North America | Long term (≥ 4 years) |

| Data-Sovereignty Regulations Limiting Cross-Border SaaS Deployments | -1.1% | Europe core, expanding to APAC | Medium term (2-4 years) |

| Resistance to Legacy System Migration Among State Police Forces | -0.6% | North America and Europe | Long term (≥ 4 years) |

| Budget Volatility from Crime-Rate-Linked Allocations (Latin America) | -0.4% | Latin America, spill-over to MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Procurement Cycles in Municipal Agencies

City departments often operate discrete budgeting calendars for police, fire and emergency-medical services, forcing multi-year alignments before a comprehensive software upgrade can be approved. Joint-procurement models offer relief: CentralSquare Technologies delivered a consolidated CAD platform to Boulder Regional Emergency Telephone Service Authority that now services police, fire and EMS across five counties. Similarly, El Paso County’s scalable CAD deployment covering 39 public-safety entities allowed smaller districts to access enterprise-grade dispatch while sharing capital expense

Data-Sovereignty Regulations Limiting Cross-Border SaaS Deployments

Tightening localisation rules in the EU oblige vendors to store and process sensitive policing records within national borders, curbing the hyperscaler efficiencies that drive SaaS economics. The upcoming EU Cloud Services Scheme introduces assurance tiers that could bar non-EU-headquartered cloud providers from hosting law-enforcement workloads unless a local subsidiary maintains operational control. While the stipulations raise trust, they also compel suppliers to build region-pruned code repositories and separate support teams, diluting global R&D leverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: CAD Leads While Predictive Analytics Accelerate

The computer-aided dispatch segment captured 24.55% of 2025 revenue, underscoring its centrality to incident routing and resource optimisation within the law enforcement software market size. Successive hardware refresh cycles and Next-Generation 911 mandates are renewing interest in GIS-rich CAD modules that integrate seamlessly with AVL, mobile data terminals and drone feeds. In parallel, predictive-analytics platforms are scaling at a 9.45% CAGR to 2031 as agencies pivot toward data-guided deployment models that anticipate hotspots a shift that is reshaping the broader law enforcement software market. Vendors are embedding machine-learning libraries directly inside CAD dashboards, allowing shift supervisors to see historical crime correlations alongside live call loads, narrowing response lags.

Growing appetite for integrated suites is also blurring traditional product boundaries. Motorola Solutions’ acquisition of RapidDeploy expanded its offering into cloud-native NG911 mapping and analytics, giving the firm cross-sell latitude across its radio and body-camera customer base. Evidence-management, facial-recognition and digital-forensics modules are being folded into single license agreements, reducing stitching costs for buyers while increasing stickiness for providers.

By Deployment Mode: Cloud Migration Accelerates Despite On-Premise Dominance

On-premise installations retained 58.35% of the law enforcement software market share in 2025, a testament to entrenched concerns over data-control and air-gapped integrations with legacy radio networks. Yet cloud instances are registering a 10.25% CAGR, propelled by shrinking capital budgets and the perception that FedRAMP-high authorisations now meet or exceed many local security benchmarks. This switch is enlarging the addressable law enforcement software market as small agencies adopt subscription models that once seemed out-of-reach. Disaster resiliency is another catalyst: the New Orleans Police Department’s move to a cloud-native RMS maintained continuity throughout the 2024 hurricane season, reinforcing cloud’s operational case among hurricane-prone states.

Hybrid architectures have emerged as an interim waypoint. Sensitive evidence files remain at the edge under agency control, while SaaS dashboards supply analytics, workflow automation and mobile accessibility. Vendors are deploying “sovereign cloud” regions with geo-fenced support teams to appease EU watchdogs, although certification cycles still stretch procurement timelines. Over the forecast horizon, machine-learning inference conducted at the edge combined with heavy-compute model training in the cloud is expected to normalise hybrid topologies across the law enforcement software market.

By Component: Software Dominance Faces Services Growth Challenge

Software licences and subscriptions represented 70.65% of 2025 spend, reflecting historical capital-outlay patterns across the law enforcement software industry. However, managed-services revenue is outpacing licences at a 9.12% CAGR as departments outsource configuration, patching and AI-model tuning to domain specialists. This swing aligns with Tyler Technologies’ strategy to drive recurring revenue above 90% by 2030 through cloud migration and outcome-based support contracts. Professional-services demand is further buoyed by requirements to migrate decades of RMS data into CJIS-compliant cloud stores without disrupting case workflows.

Training and change-management engagements are now bundled into multi-year agreements, reflecting recognition that algorithmic efficacy depends on officer adoption. Cybersecurity advisory services are likewise surging as ransomware attacks increasingly target dispatch centers and evidence vaults. Suppliers offering turnkey security operation centers alongside core applications differentiate themselves in bid processes that score heavily on resilience metrics.

By End-User Agency: Municipal Leadership Meets Federal Growth

Municipal departments remain the largest buyer group, contributing 45.95% of 2025 revenue as community policing and emergency-response functions sit closest to citizens, making modernization politically salient. Their focus on body-camera mandates and digital-evidence backlogs keeps steady pressure on budgets, cementing their central role in the law enforcement software market. Conversely, federal and national police agencies are pacing the fastest growth at 10.02% CAGR to 2031, driven by cross-border intelligence sharing and counter-terror operations that favour high-end analytics. Palantir’s USD 650 million award to supply big-data capabilities to a federal client reflects escalating appetite for mission-level platforms.

State and provincial constabularies occupy a middle ground, refreshing highway-patrol and forensic-lab systems while collaborating in regional data-lakes that spread capital costs. Tribal and special-jurisdiction forces are increasingly adopting multi-tenant SaaS to avoid building duplicate infrastructure. As cooperative purchasing agreements mature, vendors capable of multi-agency instance management with granular role-based access controls stand to win larger footprints across the law enforcement software market.

Geography Analysis

North America continues to anchor the law enforcement software market with 36.85% revenue share in 2025. Federal funding streams such as the Edward Byrne Memorial Justice Assistance Grant funnel USD 419 million in 2025 into technology upgrades for smaller departments, ensuring that even rural agencies access enterprise-grade solutions. The region’s well-developed integrator ecosystem accelerates complex rollouts, while CJIS cloud-authorisation frameworks give procurement officers confidence to migrate core workloads.

Asia-Pacific is the fastest-growing territory with a 9.42% CAGR projected through 2031. Japan’s Crime Nabi pilot and South Korea’s Incheon Free Economic Zone illustrate how smart-city budgets earmark predictive policing and AI-enhanced surveillance. Regional governments bundle public-safety procurement with broader digital-governance initiatives, unlocking multi-year financing and fostering public-private partnerships. China’s mass-deployment of AI-assisted video analytics creates enormous scale for algorithm refinement, while India’s cloud-first e-governance schemes entice SaaS vendors with multi-state roll-out opportunities. Australia and New Zealand focus on evidence-management modernisation to counter rising cyber-enabled crime, further enlarging regional demand.

Europe records steady albeit more measured growth as data-sovereignty and privacy mandates dictate deployment architectures. The United Kingdom’s GBP 20 million framework for live facial-recognition underscores appetite for advanced analytics, yet stipulates stringent audit and bias-mitigation requirements. Germany’s leadership in shaping the EU Artificial Intelligence Act informs vendor roadmaps, compelling them to embed explainability into predictive models from inception. Sovereign-cloud build-outs by hyperscalers combine local data residency with elastic compute, encouraging agencies previously bound to on-premise servers to experiment with hybrid deployments.

Competitive Landscape

Competitive intensity remains moderate as diversified conglomerates, mid-market specialists and AI-native start-ups vie for wallet share across the law enforcement software market. Motorola Solutions leverages an end-to-end portfolio spanning radios, body-cams and software, delivering USD 2.5 billion in Q1 2025 revenue and adding RapidDeploy’s NG911 mapping suite to deepen its cloud stack. Platform consolidation persists as agencies favour integrated environments: Tyler Technologies aims for USD 3.6–3.8 billion annual revenue by 2030 via cloud migration and expanded managed-services penetration.

Advanced-analytics specialists retain a moat in mission-level deployments. Palantir’s USD 650 million federal contract underscores demand for graph analytics and data-fusion at petabyte scale. Rather than building competing stacks, infrastructure providers form alliances: Oracle’s partnership with Palantir places AI accelerators onto Oracle Cloud Infrastructure, packaging compute, storage and analytics into a single procurement line. Emerging disruptors differentiate through mobile-first UX and voice-driven report writing, yet face rising certification costs that favour capital-rich incumbents. Cybersecurity posture is now a bid-critical differentiator; suppliers offering built-in zero-trust frameworks and sovereign-cloud endpoints command premium price points.

Acquisition pipelines remain active as strategic buyers seek best-of-breed point solutions that close functional gaps. Deals concentrate in evidence-management, officer-wellness analytics and automated transcription where innovation cycles move faster than internal R&D budgets. As platformisation advances, the law enforcement software market is expected to tilt toward fewer, broader ecosystems linked by open APIs, while niche vendors anchor themselves through patented AI models or domain-specific data sets.

Law Enforcement Software Industry Leaders

IBM Corporation

Motorola Solutions, Inc.

Hexagon AB

Axon Enterprise Inc.

Palantir Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Motorola Solutions acquired RapidDeploy, adding NG911 mapping and analytics that support 1,600 PSAPs across 24 states to its command-center cloud suite.

- February 2025: NICE won a contract with the Fire Department of New York to deploy NICE Investigate, a cloud digital-evidence platform that auto-ingests CAD, CCTV and IoT feeds while meeting New York discovery-law timetables.

- January 2025: TRULEO secured an enterprise agreement with OpenAI to create a voice-activated patrol assistant featuring zero-data-retention protocols for U.S. agencies (company announcement, domain withheld).

- December 2024: McHenry County State’s Attorney’s Office adopted NICE Justice to automate video transcoding, accelerating case preparation across 3,000 annual prosecutions.

Global Law Enforcement Software Market Report Scope

Law Enforcement Software is an integrated software solution that helps law enforcement bodies and public safety organizations to ensure the safety of the citizens, public spaces, communities, etc., by providing a faster response, improved operational efficiency, and reduced costs. The solutions provided by such software are Records Management Systems, Computer-Aided Dispatch Systems, GIS/Mapping, Emergency Response, Jail Management, Evidence Management, and Video Analytics, which can be deployed both on-premise and on the cloud.

| Records Management Systems |

| Computer-Aided Dispatch (CAD) |

| Jail Management |

| Evidence / Digital Evidence Management |

| GIS / Mapping |

| Emergency Response |

| Video Analytics and Facial Recognition |

| Mobile / Field Reporting |

| Predictive and Crime-Analytics Platforms |

| Cloud |

| On-Premise |

| Hybrid |

| Software |

| Services |

| Federal and National Police |

| State and Provincial Police |

| Municipal / Local Agencies |

| Special-Jurisdiction and Tribal Forces |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Solution | Records Management Systems | ||

| Computer-Aided Dispatch (CAD) | |||

| Jail Management | |||

| Evidence / Digital Evidence Management | |||

| GIS / Mapping | |||

| Emergency Response | |||

| Video Analytics and Facial Recognition | |||

| Mobile / Field Reporting | |||

| Predictive and Crime-Analytics Platforms | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Component | Software | ||

| Services | |||

| By End-User Agency | Federal and National Police | ||

| State and Provincial Police | |||

| Municipal / Local Agencies | |||

| Special-Jurisdiction and Tribal Forces | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current valuation of the law enforcement software market?

It is valued at USD 21.18 billion in 2026 and is projected to reach USD 31.23 billion by 2031, reflecting an 8.07% CAGR.

Which solution type holds the largest share of spending?

Computer-aided dispatch platforms lead with 24.55% of 2025 revenue, underscoring their role as the operational backbone for emergency response coordination.

Why are agencies moving to cloud deployment even though on-premise still dominates?

Cloud platforms cut capital expense, offer built-in disaster resilience and now meet CJIS and sovereign-cloud compliance, driving a 10.25% CAGR despite a 58.35% on-premise base.

Which region is growing fastest and why?

Asia-Pacific is expanding at a 9.42% CAGR thanks to smart-city programmes that integrate AI-powered surveillance, predictive policing and urban-management applications.

How fragmented is the competitive landscape?

The market receives a concentration score of 2 because the top ten vendors hold under 30% of revenue, leaving room for specialised analytics and SaaS entrants.

What funding sources are most influential for U.S. agencies?

Federal programmes like the Edward Byrne Memorial Justice Assistance Grant and DHS Science & Technology budgets inject hundreds of millions of dollars annually into technology modernisation.

Page last updated on: