Gas Detection System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.88 Billion |

| Market Size (2031) | USD 7.46 Billion |

| Growth Rate (2026 - 2031) | 4.86% CAGR |

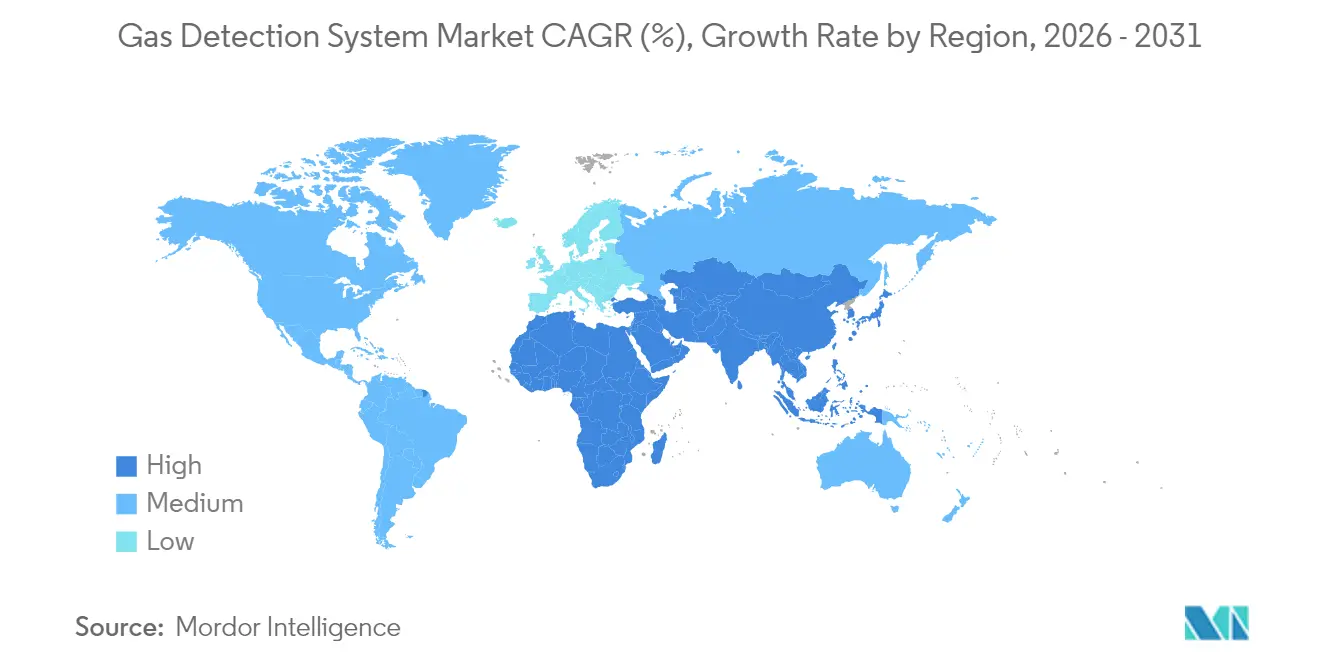

| Fastest Growing Market | Asia |

| Largest Market | North America |

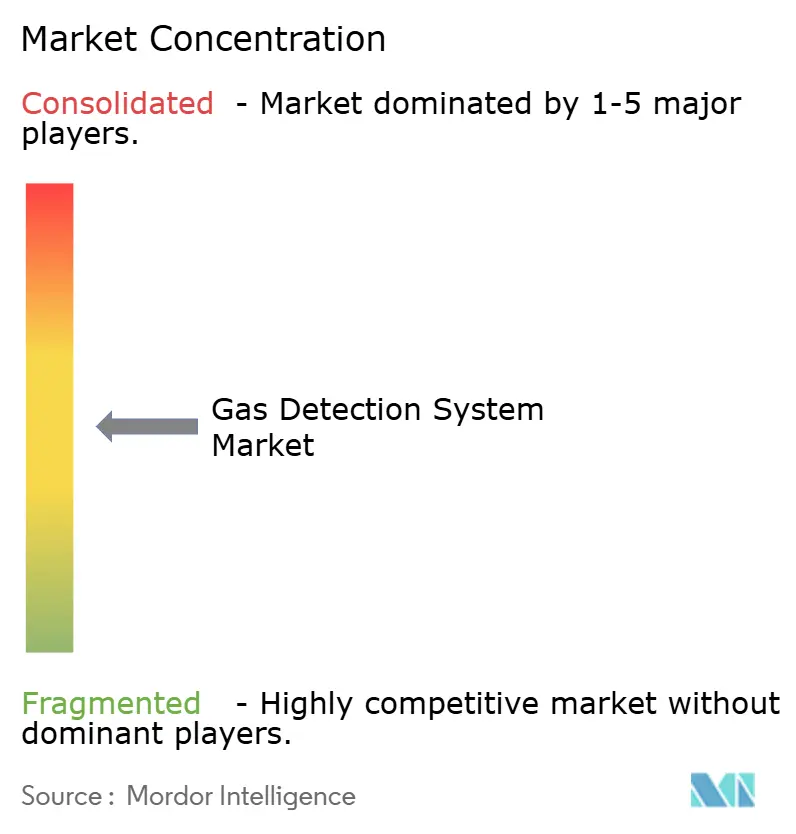

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gas Detection System Market Analysis by Mordor Intelligence

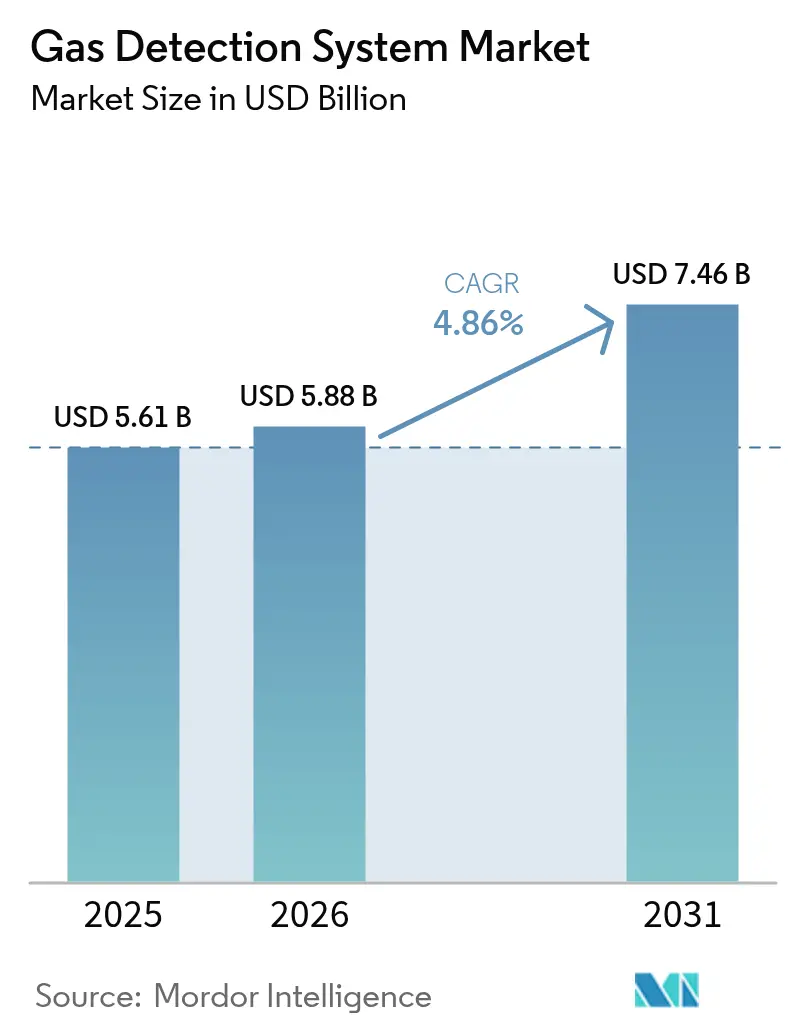

The Gas Detection System Market size was valued at USD 5.61 billion in 2025 and estimated to grow from USD 5.88 billion in 2026 to reach USD 7.46 billion by 2031, at a CAGR of 4.86% during the forecast period (2026-2031). A shift away from exclusive oil-and-gas dependence toward hydrogen infrastructure, battery energy storage, and low-GWP refrigerant applications supports steady demand. Mandatory IIoT safety upgrades in China, updated NFPA 855 codes for energy storage, and Europe’s REPowerEU hydrogen targets collectively enlarge the addressable base. Growth accelerators include wireless networking, predictive analytics, and multi-gas integration, while technical barriers around sensor calibration and certified wireless spectrum temper momentum. Competitive activity remains moderate as established vendors secure technology breadth through acquisitions and joint ventures.

Key Report Takeaways

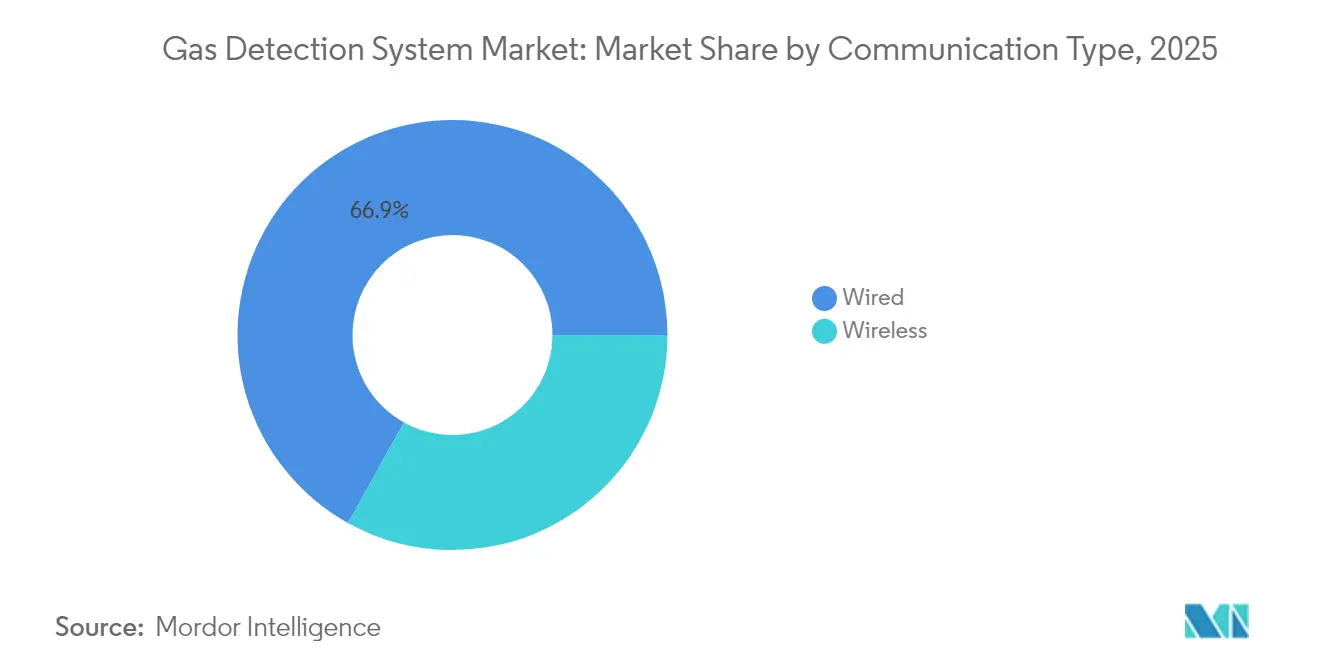

- By communication type, wired systems led with 66.92% revenue share in 2025, whereas wireless recorded the highest 6.12% CAGR through 2031.

- By detector design, fixed installations held 70.62% of the gas detection system market share in 2025, while portable devices are set to expand at 5.48% CAGR to 2031.

- By sensor technology, electrochemical units accounted for 44.55% share of the gas detection system market size in 2025 and infrared sensors are projected to grow 6.84% CAGR over 2026-2031.

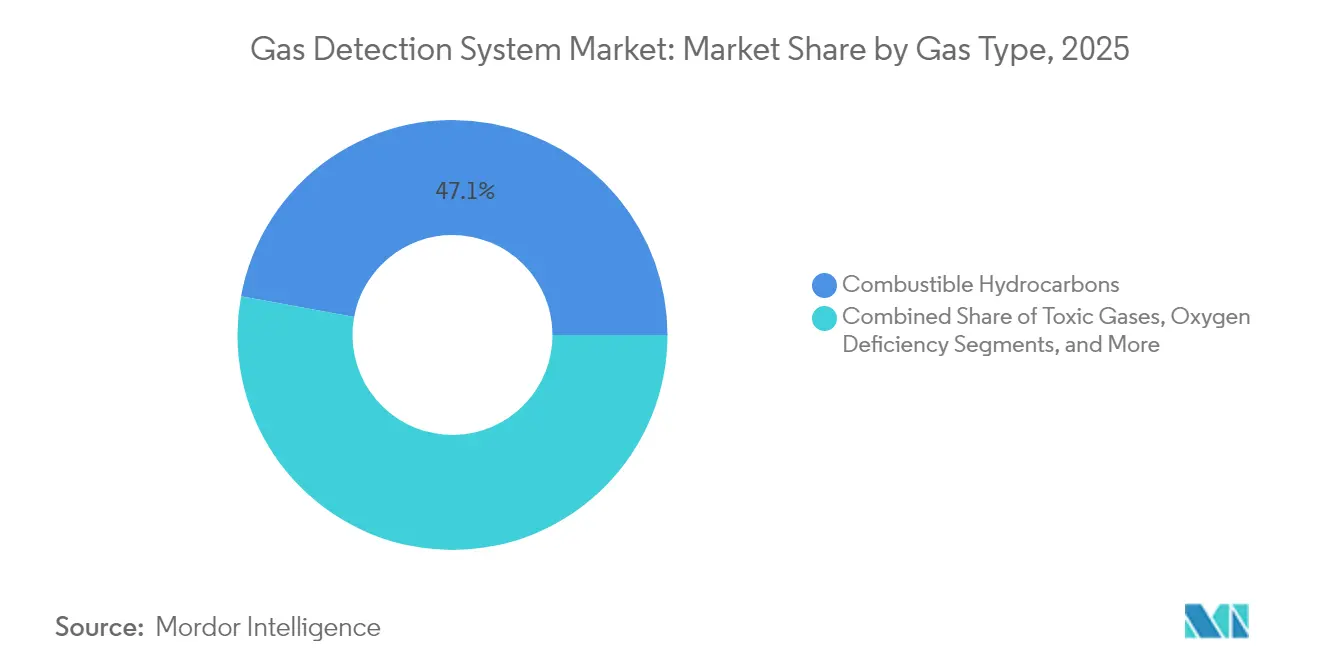

- By gas type, combustible hydrocarbon detection commanded 47.12% share of the gas detection system market size in 2025; refrigerant monitoring is advancing at 5.03% CAGR.

- By device type, multi-gas platforms captured 60.05% revenue share in 2025.

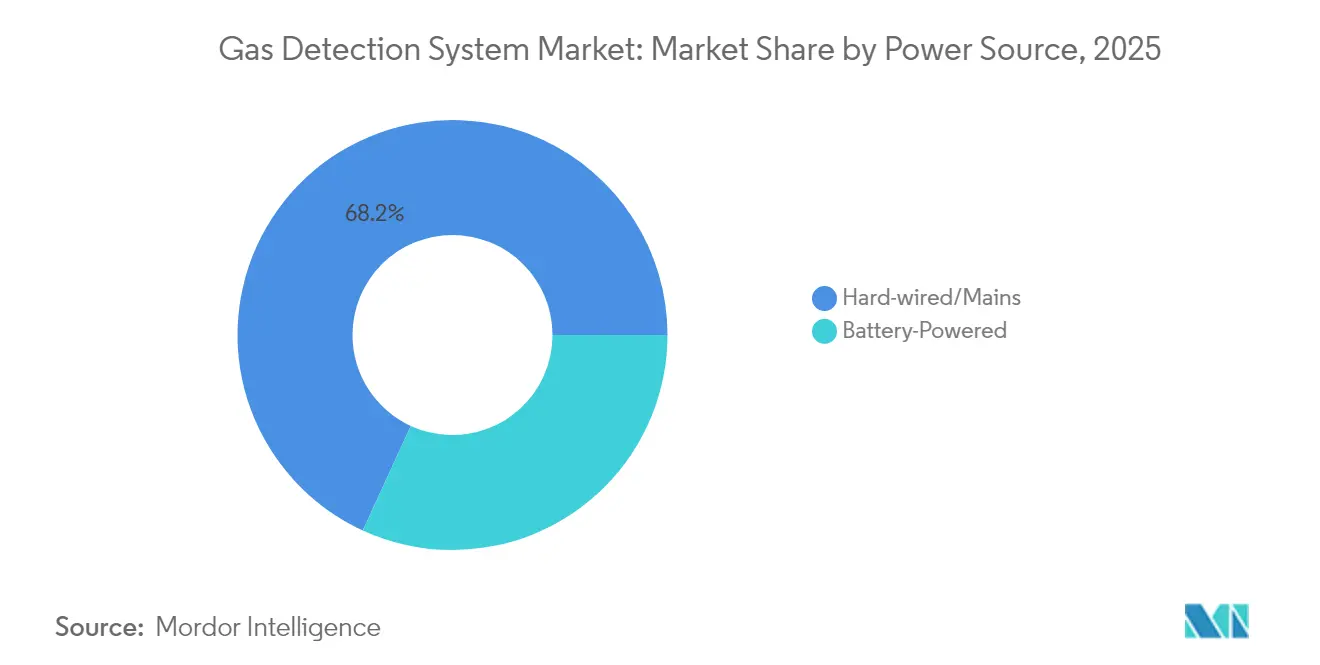

- By power source, hard-wired solutions controlled 68.15% of 2025 revenue and battery-powered units post a 5.98% CAGR outlook.

- By end-user, oil & gas led with 34.18% share in 2025, while discrete manufacturing rises fastest at 7.33% CAGR.

- By geography, North America represented 31.74% revenue share in 2025; Asia-Pacific exhibits the quickest 5.62% regional CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gas Detection System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Hydrogen Economy Driving Demand for Multi-Gas Detectors in Europe | +0.8% | Europe, with spillover to North America | Medium term (2-4 years) |

| Rising Offshore Deepwater E&P Activities Requiring High-Reliability Gas Monitoring | +0.6% | North America, Gulf of Mexico | Short term (≤ 2 years) |

| Mandatory IIoT-enabled Safety Upgrades under China State Administration of Work Safety | +0.7% | China, with regional influence in APAC | Medium term (2-4 years) |

| Accelerating Adoption of Battery Energy Storage Systems with Fire/Gas Codes | +0.5% | Global, concentrated in North America and Europe | Long term (≥ 4 years) |

| Surge in Green Ammonia Projects Boosting NH3 Leak Detection | +0.4% | EMEA, with expansion to APAC | Long term (≥ 4 years) |

| Transition to Low-GWP Refrigerants Driving Refrigerant Gas Detection | +0.3% | Global, led by developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Hydrogen Economy

Europe’s hydrogen build-out under the REPowerEU plan demands sensors able to track hydrogen alongside traditional combustibles and oxygen-deficiency risks. Palladium-nanotransistor prototypes now detect parts-per-billion H₂ with minimal power draw.[2]Nature Communications, “Nanotransistor-based gas sensing with record-high sensitivity,” nature.com As projects scale, multi-gas devices become budgeted line items, embedding the gas detection system market deeper into European energy infrastructure. Procurement cycles favor vendors with hydrogen-specific analytics and ATEX certificates, elevating design complexity and average selling prices.

Rising Offshore Deepwater Exploration

Thirteen new Gulf of America fields scheduled online through 2026 will add 0.27 Bcf/d of gas, prompting operators to specify marine-certified methane detectors.[1]U.S. Energy Information Administration, “Gulf of America oil and natural gas production expected to remain stable through 2026,” eia.gov Honeywell’s Emissions Management Suite-approved for hazardous marine zones-illustrates product differentiation that meets stricter uptime and remote-maintenance criteria. Predictive algorithms trimming false alarms by 40% strengthen value propositions where offshore interventions run into millions of USD per call-out.

Mandatory IIoT Safety Upgrades in China

China’s Three-Year Action Plan mandates real-time, connected gas monitoring in mining, chemicals, and heavy manufacturing.[3]Ministry of Emergency Management, “安全生产治本攻坚三年行动主要任务,” mem.gov.cn Facilities facing 2026 compliance deadlines accelerate replacement of analog systems with wireless-enabled platforms. The regulation shifts demand from standalone detectors to integrated, cloud-reporting networks, broadening the gas detection system market envelope and raising the technological entry bar for domestic entrants.

Accelerating Battery Energy Storage Deployment

NFPA 855 now requires multi-species gas detection tied to ventilation and suppression controls for storage systems above 20 kWh. Texas fire codes add state-level urgency. Compliance turns detection from optional to mandatory, positioning integrated solution suppliers for premium capture across utility-scale and behind-the-meter projects.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Faulty Calibrations in Sulfur-rich Environments Causing False Alarms | -0.3% | Global, particularly oil & gas regions | Short term (≤ 2 years) |

| Scarcity of Certified Wireless Spectrum for Hazardous Locations (Zones 0/1) | -0.4% | Global, with acute impact in Europe and North America | Medium term (2-4 years) |

| High CapEx for Redundant Sensor Networks in Brown-field Refineries | -0.2% | Global, concentrated in mature oil & gas markets | Medium term (2-4 years) |

| Limited Availability of Long-life Solid-State NH3 Sensors Less than -40 °C (Nordics) | -0.1% | Nordic countries, with spillover to Arctic regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Faulty Calibrations in Sulfur-Rich Environments

Hydrogen sulfide above 50 ppm shortens electrochemical sensor life by 60%, inflating maintenance budgets and eroding operator trust. MEMS-based detectors mitigate poisoning but carry higher capital costs . Cross-sensitivities force redundant arrays, complicating wiring schemas and dampening the gas detection system market’s short-term uptake in sour-gas facilities.

Scarcity of Certified Wireless Spectrum

Zone 0 certification for wireless nodes can stretch to 24 months, delaying projects and nudging buyers back toward wired architectures.. Regional NB-IoT spectrum gaps further constrain deployment density, sustaining premium pricing for compliant wireless SKUs and moderating the gas detection system market’s upgrade rate in digitally transforming plants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Type: Wireless Infrastructure Modernization Accelerates

Wired installations accounted for 66.92% of 2025 revenue, anchoring the gas detection system market in legacy process industries. Modern plants now weigh material cost savings and installation agility; hence wireless revenues are advancing at 6.12% CAGR. Mesh topologies preserve link resilience, while NB-IoT energy-harvesting prototypes underscore future autonomy. Certification roadblocks and interference management still cap near-term penetration, yet wireless remains the chief modernization lever across brownfield projects.

Reduced trenching costs appeal to temporary construction and turnaround scenarios, and battery-free sensor nodes promise maintenance relief. With wireless links feeding cloud dashboards, operators move from compliance-driven monitoring toward predictive asset health, reinforcing recurring-service revenue streams in the gas detection system market.

By Detector Type: Portable Solutions Gain Traction in Flexible Operations

Fixed detectors retained 70.62% share in 2025, reflecting code requirements for continuous coverage in petrochemical and utility sites. Workforce mobility and shutdown activities fuel a 5.48% CAGR for portables, which now bundle CAT-M cellular modems and cloud APIs. Fleet-wide analytics streamline compliance documentation, improving ROI narratives.

Hybrid area monitors extend portable coverage with 100-day battery life, bridging gaps between personal and fixed layers. While fixed arrays remain foundational for process control integration, modular sensor cartridges and hot-swap designs cut downtime, fortifying their long-term position inside the gas detection system market.

By Sensor Technology: Infrared Innovation Reconfigures Maintenance Economics

Electrochemical cells delivered 44.55% of 2025 revenues, yet infrared devices are rising 6.84% CAGR on stability and low drift. Photoacoustic IR systems detect ammonia to 1 ppm without frequent recalibration. Mid-IR metasurface microspectrometers show promise for multi-gas analytics at chip-scale footprints.

Catalytic bead sensors still underpin basic hydrocarbon alarms, but sensor-fusion firmware now marries IR, PID, and electrochemical channels for selectivity gains. These advances cut lifetime ownership costs and expand the gas detection system market into environments where maintenance access is constrained.

By Gas Type: Refrigerant Monitoring Gains Regulatory Tailwind

Combustible gases generated 47.12% of 2025 sales, yet low-GWP refrigerant detection is growing 5.03% CAGR as HVAC-R codes tighten. ASHRAE 15-2024 mandates dual-range sensors, stimulating demand for specialized A2L products. NDIR-based R290 detectors with ±2.5% LFL accuracy meet flammability challenges.

Toxic gas and oxygen-deficiency monitoring retain steady industrial relevance, while semiconductor fabs spur niche demand for ultra-trace specialty-gas detection. Such diversification shields the gas detection system market from commodity price swings in hydrocarbons.

By Device Type: Multi-Gas Integration Becomes Default Specification

Multi-gas instruments captured 60.05% of 2025 turnover as facilities prioritize platform simplicity over single-species specialization. Controllers supporting up to 16 channels streamline rack space and supervisory system integration. Parts-per-trillion comb-interferometry prototypes could enable 20-gas monitoring on one optical bench.

Single-gas units continue where extreme sensitivity is paramount, but life-cycle economics and reduced calibration overhead anchor multi-gas as the mainstream of the gas detection system market.

By Power Source: Battery and Energy-Harvesting Options Broaden Deployment

Hard-wired products held 68.15% share in 2025, supported by code preferences and intrinsic power reliability. Battery-powered units grow 5.98% CAGR as Li-ion density climbs and firmware throttles current below 0.5 mA . Thermoelectric harvesters reclaim process heat to create autonomous nodes, ideal for pipelines and flare stacks.

Hybrid solar or vibration-assisted systems extend deployments into remote or mobile assets, deepening reach of the gas detection system market while easing total-cost barriers for smaller operators.

By End-User Industry: Discrete Manufacturing Sparks Technology Refresh

Oil & gas retained 34.18% share, yet discrete manufacturing posts a 7.33% CAGR on semiconductor, battery, and EV supply-chain expansion. Sub-ppm toxic-gas detection in fabs and battery fire-gas analytics spearhead premium sensor adoption

Water-wastewater, chemicals, mining, and food processing each maintain niche, regulation-driven baselines. Cross-industry diversification cushions the gas detection system industry against cyclical swings in any one vertical.

Geography Analysis

North America led revenue with 31.74% share in 2025, reflecting entrenched OSHA and NFPA frameworks that compel comprehensive safety monitoring. Offshore project starts and LNG build-outs sustain capital spending on marine-certified detectors, while battery energy storage rollouts widen scope into utility and commercial real estate. Canadian hydrogen pilots and carbon-capture hubs further reinforce demand across multi-gas platforms.

Europe follows with strong growth tied to hydrogen infrastructure and refrigerant phase-downs. ATEX and IECEx compliance requirements raise entry barriers, channeling contracts toward firms with established certification pedigrees. German chemical clusters and UK pharmaceuticals champion early adoption of wireless analytics, whereas Nordic operators specify low-temperature sensor packages calibrated to -40 °C.

Asia-Pacific records the fastest 5.62% CAGR, propelled by China’s IIoT safety mandate and India’s hazardous-chemical rules. Japanese updates to the High-Pressure Gas Safety Act and SEA petrochemical investments also boost uptake. Rapid industrialization, combined with maturing safety cultures, enlarges regional opportunity for both basic and advanced offerings, positioning APAC as the primary incremental engine for the gas detection system market through 2031.

Competitive Landscape

Industry consolidation remains moderate. Honeywell’s USD 1.81 billion LNG technology buy and USD 2.25 billion catalyst acquisition underscore a strategy to couple process know-how with detection hardware, embedding sales into larger energy-transition projects. MSA Safety added German gas-analysis expertise through the USD 200 million M&C TechGroup deal and logged 17% Q1 2025 organic growth in detection revenue, validating cross-sell leverage.

Connected-safety specialist Blackline Safety crossed USD 100 million in annual sales on service-centric models, highlighting a shift from hardware margins to SaaS-recurring revenue. The SICK–Endress+Hauser joint venture pools analyzer and flow-meter intellectual property, aiming to speed multi-parameter product launches and compete on integrated plant packages.

Emerging disruptors exploit rare-earth orthoferrites and nanomaterial electrodes for heightened sensitivity, though certification complexity slows rapid scaling. Players capable of merging AI diagnostics, cloud analytics, and IECEx Zone 0 wireless certificates hold a defensible technology moat, shaping the medium-term structure of the gas detection system market.

Gas Detection System Industry Leaders

Honeywell International Inc.

Drägerwerk AG & Co KgaA

SENSIT Technologies

Hanwei Electronics Group Corporation

Emerson Electric Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Honeywell agreed to acquire Johnson Matthey’s Catalyst Technologies business for GBP 1.8 billion, broadening lower-emission process capabilities

- May 2025: MSA Safety completed the USD 200 million purchase of M&C TechGroup, enhancing gas analysis depth

- April 2025: MSA Safety reported USD 421 million Q1 net sales with 17% organic growth in detection products

- March 2025: IEC released the 60079:2025 SER standards series covering equipment for explosive atmospheres

Global Gas Detection System Market Report Scope

The Global Gas Detection System Market is Segmented by Communication Type (Wired, Wireless), Type of Detector (Fixed, Portable, and Transportable), End-user (Oil and Gas, Chemicals and Petrochemicals, Water and Wastewater, Metal and Mining, Utilities), and Geography.

The gas detection system includes products that use technology to promote safety, and it is used preferably to protect workers and to ensure plant safety. Gas detection systems are dedicated to detecting dangerous gas concentrations, triggering alarms, and activating countermeasures before the situation turns hazardous and places the employees, assets, and environment at risk.

| Wired |

| Wireless |

| Fixed |

| Portable |

| Electrochemical |

| Infra-red (IR) |

| Catalytic Bead |

| Photo-ionization (PID) |

| Others (MOS, Optical) |

| Combustible Hydrocarbons |

| Toxic Gases (CO, H?S, Cl?, SO?) |

| Oxygen Deficiency |

| Refrigerant Gases |

| Specialty and Rare Gases |

| Single-Gas Detectors |

| Multi-Gas Detectors |

| Battery-Powered |

| Hard-wired/Mains |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Water and Wastewater |

| Metals and Mining |

| Power and Utilities |

| Food and Beverage |

| Pharma and Life-Sciences |

| Discrete Manufacturing (Semiconductor, Automotive, Battery) |

| Other Industries (Battery Energy Storage, and More) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Communication Type | Wired | ||

| Wireless | |||

| By Detector Type | Fixed | ||

| Portable | |||

| By Sensor Technology | Electrochemical | ||

| Infra-red (IR) | |||

| Catalytic Bead | |||

| Photo-ionization (PID) | |||

| Others (MOS, Optical) | |||

| By Gas Type | Combustible Hydrocarbons | ||

| Toxic Gases (CO, H?S, Cl?, SO?) | |||

| Oxygen Deficiency | |||

| Refrigerant Gases | |||

| Specialty and Rare Gases | |||

| By Device Type | Single-Gas Detectors | ||

| Multi-Gas Detectors | |||

| By Power Source | Battery-Powered | ||

| Hard-wired/Mains | |||

| By End-user Industry | Oil and Gas | ||

| Chemicals and Petrochemicals | |||

| Water and Wastewater | |||

| Metals and Mining | |||

| Power and Utilities | |||

| Food and Beverage | |||

| Pharma and Life-Sciences | |||

| Discrete Manufacturing (Semiconductor, Automotive, Battery) | |||

| Other Industries (Battery Energy Storage, and More) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the gas detection system market?

The gas detection system market stands at USD 5.88 billion in 2026.

How fast is the gas detection system market expected to grow?

It is forecast to expand at a 4.86% CAGR, reaching USD 7.46 billion by 2031.

Which region is growing the quickest?

Asia-Pacific shows the fastest regional CAGR of 5.62% through 2031 due to mandatory IIoT safety upgrades and industrial expansion.

What technology segment is outperforming others?

Infrared sensor technology is projected to post the highest 6.84% CAGR thanks to greater stability and lower maintenance demands.

Page last updated on: