Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 4.01 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gas Detectors Market Analysis by Mordor Intelligence

The gas detectors market size was valued at USD 2.99 billion in 2025 and estimated to grow from USD 3.14 billion in 2026 to reach USD 4.01 billion by 2031, at a CAGR of 5.01% during the forecast period (2026-2031). The trajectory reflects rising capital investment in real-time worker-safety solutions, growing retrofit demand across legacy plants, and the integration of connected detection platforms that feed predictive analytics engines. Strict enforcement of OSHA, NFPA 72, and regional mining codes is stimulating equipment replacement cycles, while sustained buildouts of midstream LNG hubs, hydrogen production assets, and lithium-ion battery lines elevate baseline demand for combustible and toxic-gas monitoring.[1]Source: National Fire Protection Association, “NFPA 72 2025 Edition,” nfpa.org Intensifying cybersecurity rules for safety systems is steering procurement toward vendors that can combine certified sensor hardware with secured IoT software stacks. Although wired networks still dominate brownfield installations, advances in wireless mesh topologies and multiyear battery modules are lowering total installed cost and unlocking untapped niches such as remote wellheads and temporary turnaround zones. Competitive activity is accelerating as incumbent global suppliers defend share against specialist entrants promising lower drift rates, hydrogen specificity, or subscription-based calibration services.

Key Report Takeaways

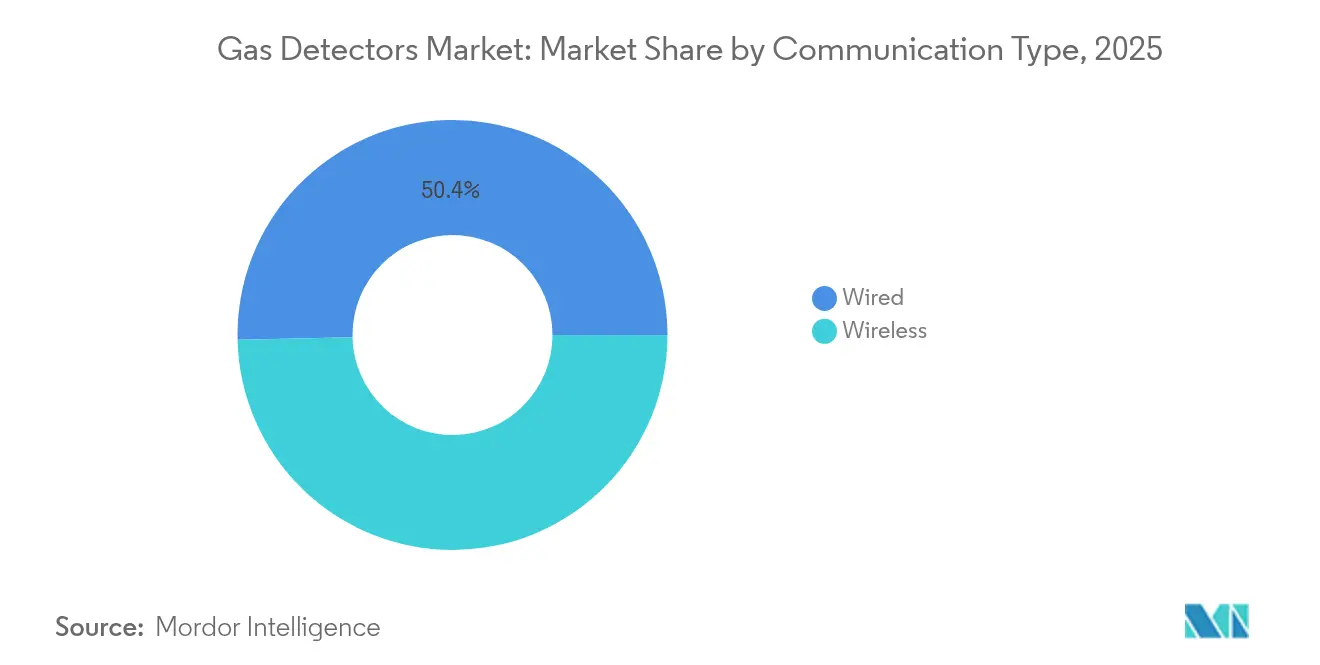

- By communication type, wired systems led with 50.35% of gas detectors market share in 2025, while wireless solutions are forecast to post the highest 7.05% CAGR through 2031.

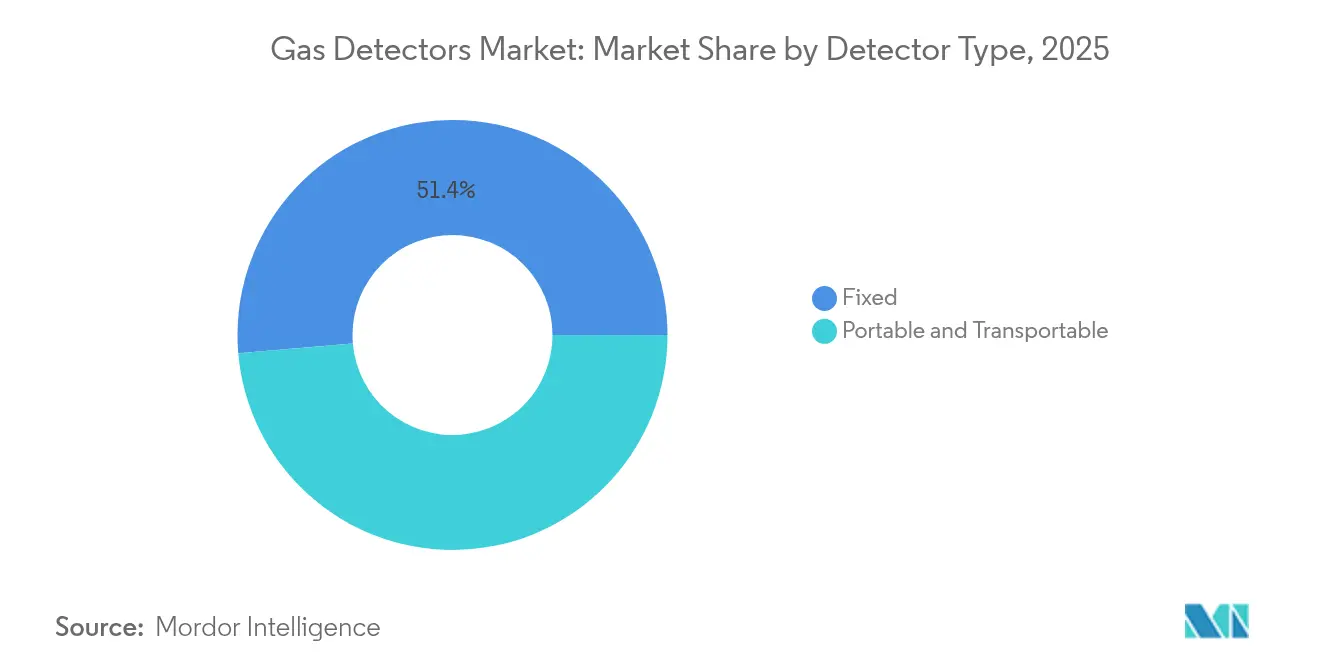

- By detector type, fixed installations accounted for a 51.35% share of the gas detectors market size in 2025, whereas portable and transportable units are estimated to advance at a 6.72% CAGR to 2031.

- By end-user industry, chemicals and petrochemicals commanded 38.55% of 2025 revenue, and utilities are projected to expand at a 6.58% CAGR through 2031.

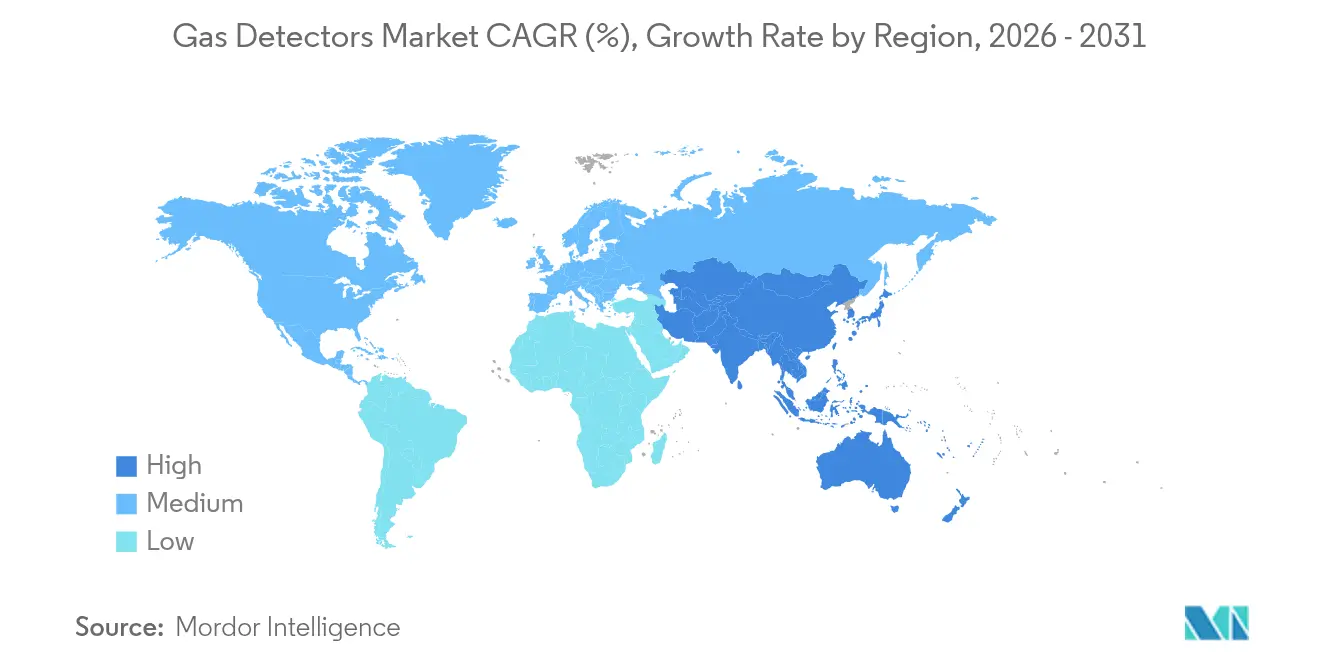

- By geography, Asia-Pacific dominated with 48.60% revenue share in 2025 and is projected to grow at a 6.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gas Detectors Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent worker-safety mandates in hazardous industries | +1.2% | Global, with stronger enforcement in North America and Europe | Medium term (2-4 years) |

| Rising installation of smart, connected detectors | +0.9% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Growing demand for real-time multigas monitoring | +0.8% | Global, concentrated in industrial hubs | Medium term (2-4 years) |

| Expansion of midstream LNG and hydrogen infrastructure | +0.7% | Asia-Pacific, Middle East, North America | Long term (≥ 4 years) |

| Indoor air-quality compliance in smart buildings | +0.5% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Lithium-ion battery plants' gas-leak scrutiny | +0.4% | Asia-Pacific core, expanding to North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Worker-Safety Mandates in Hazardous Industries

Regulators now require live environmental telemetry rather than periodic spot checks, compelling mines, refineries, and chemical complexes to deploy continuous monitoring networks. OSHA’s 2025 program of data-driven inspections is motivating operators to replace legacy single-gas units with networked multigas arrays that transmit readings into centralized dashboards.[2]Source: AVTECH Software Inc., “Navigating OSHA 2025,” avtech.com Australian coal legislation mandates mine-drained-roadway (MDR) certification, prompting orders for explosion-proof fixed heads and UAV-mounted sensors that map underground methane in three dimensions. Municipal water utilities must comply with NFPA 820 thresholds for hydrogen sulfide, leading to multi-thousand-unit retrofits of wet-well ventilated spaces. Leading vendors respond with predictive analytics software that flags abnormal patterns before alarms trigger, aligning with zero-harm directives such as Industrial Scientific’s vision to eliminate workplace fatalities by 2050. Annual compliance spending can top USD 100,000 for a single refinery, locking in replacement cycles and service contracts.

Rising Installation of Smart, Connected Detectors

IoT connectivity converts the gas detectors market from product sales to data-service ecosystems. Blackline’s EXO 8 streams to the cloud for 100 days on a single charge, allowing remote safety teams to watch exposure trends in real time.[3]Source: Ansac Technology, “Blackline EXO 8 Multi-Gas Area Monitor,” ansac-tech.com.sg Honeywell’s Sensepoint XCL pairs with smartphones through Bluetooth Low Energy, guiding technicians step-by-step and shortening calibration windows by up to 30%. Predictive dashboards schedule sensor replacement automatically, mitigating skilled-labor shortages and cutting unplanned downtime. Subscription bundles such as Industrial Scientific’s iNet Exchange shift procurement from capex to opex, bundling hardware, consumables, and analytics in multi-year contracts. Automated compliance logs shave audit preparation from weeks to hours, an attractive benefit for multinationals juggling disparate regional regulations.

Growing Demand for Real-Time Multigas Monitoring

Complex chemical and petrochemical sites host multiple toxic and combustible hazards, prompting migration from single-gas units to multigas analyzers that reduce equipment counts and training complexity. Gas Clip Technologies’ MGC Simple offers four-gas coverage with a two-year maintenance-free design that eliminates charging cradles and bump-test routines. Riken Keiki’s GX-9000 extends simultaneous measurement to six gases and samples up to 45 m, delivering plant-wide visibility from a single deployment point. Built-in gas libraries allow automatic correction factors across 25 + chemistries, while wireless relays trigger ventilation or process-shutdown sequences when thresholds are crossed. Consolidated devices lower the lifetime cost per detection point and simplify inventory management for distributed workforces.

Expansion of Midstream LNG and Hydrogen Infrastructure

Energy-transition megaprojects are scaling hydrogen and LNG assets that demand ultra-fast leak detection. Hydrogen’s 4-75% flammability range and high diffusivity require sensors with accelerated response and poisoning resistance, such as International Gas Detectors’ MK8 Pellistor technology. LNG terminals need high-density methane monitoring because rapid vaporization of cryogenic liquid can create explosive mixtures within minutes. Green-field plants increasingly design in wireless mesh networks supporting thousands of nodes, with gateway controllers routing encrypted data into DCS environments for integrated safety shutdown. Specialized sensor costs run 20-35% above hydrocarbon-only models, lifting the gas detectors market value mix toward premium tiers over the forecast horizon.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront cost and limited product differentiation | -0.8% | Global, more pronounced in price-sensitive emerging markets | Short term (≤ 2 years) |

| Maintenance-calibration burdens | -0.6% | Global, particularly affecting remote installations | Medium term (2-4 years) |

| Cybersecurity concerns in IIoT-enabled detectors | -0.4% | North America and Europe, expanding to the Asia-Pacific | Medium term (2-4 years) |

| Periodic semiconductor-sensor supply shortages | -0.3% | Global, with an acute impact on the Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost and Limited Product Differentiation

Industrial-grade multigas portables range from USD 500 to USD 1,500 per unit, figures that double once installation hardware, commissioning, and user training are included. The AimSafety PM400 lists at USD 558.57 while Gas Clip’s maintenance-free MGC Simple commands USD 697.07, highlighting price premiums linked to no-calibration claims. Low-cost Asian clones undercut established brands by up to 50%, compressing margins and delaying replacement programs in budget-constrained plants. Fixed-system installs often exceed USD 1 million for a mid-size refinery section once certified conduit, control cabinets, and functional testing are included. Price sensitivity is amplified in regions where enforcement remains inconsistent, enabling some operators to defer upgrades.

Maintenance-Calibration Burdens

Electrochemical and catalytic cells drift 2-5% monthly, requiring recalibration every 6-12 months at USD 35-85 per detector, or more than USD 100 per unit if ISO/IEC 17025 certification is mandated. Remote mines and offshore platforms face travel expenses that surpass service fees, while production downtime during calibration complicates shift planning. Portable fleets demand asset-tracking systems to avoid expired sensors circulating through the field. Some operators attempt to extend intervals to save cost, risking false negatives and regulatory fines. Predictive maintenance platforms issue advance alerts and ship pre-calibrated sensor cartridges, yet many budget holders remain wary of recurring subscription fees.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Type: Wireless Momentum Builds Around Retrofit Flexibility

The wired segment held 50.35% of 2025 revenue as established refineries, LNG trains, and chemical parks rely on proven hardwired loops that meet hazardous-area standards. In these legacy environments, the gas detectors market continues to favor flameproof junction boxes and armored cable runs that withstand electromagnetic interference. However, wireless solutions are on a 7.05% CAGR through 2031, buoyed by projects where trenching costs or temporary turnaround schedules favor rapid deployment. Early-generation radio systems suffered from limited battery life, yet second-generation mesh designs now deliver up to 100 days of uptime on a single charge and can hop data through multiple gateways to reach a plant’s supervisory control network. New-build hydrogen hubs and battery plants increasingly budget for hybrid architectures in which wireless nodes feed hardwired safe-area gateways, blending flexibility with deterministic uptime. Regulators are beginning to clear suitably redundant wireless life-safety loops, a policy evolution that removes a historic adoption barrier in jurisdictions such as the European Union and parts of the United States. Equipment manufacturers thus channel research and development into firmware-based cybersecurity, OT network segmentation, and over-the-air sensor calibration routines that align with National Institute of Standards and Technology guidelines. The shift lifts overall solution ASPs and introduces subscription revenue as vendors monitor network health remotely, thus enlarging the gas detectors market value pool even though absolute sensor counts continue to favor wired nodes for the next five years.

Wireless uptake also benefits from digital transformation budgets that seek to unify disparate field instruments under common asset-performance dashboards. When procurement teams tally the total cost of ownership, the elimination of conduit, cable trays, and hot-work permits often offsets the premium list price of wireless analyzers. Added mobility widens safety coverage during turnaround events, where temporary pipework changes create fresh leak paths each day. Downstream petrochemical players that trialed wireless packs during 2024 turnaround seasons report 15% fewer confined-space entry violations and 8% shorter maintenance windows. These operational wins reinforce payback models and solidify management buy-in, further accelerating wireless share gains within the broader gas detectors market.

By End-User Industry: Chemicals Retain Leadership While Utilities Accelerate

Complex reaction trains, solvent storage farms, and feedstock pipelines position chemicals and petrochemicals as the single largest buying center with 38.55% 2025 revenue. Many operators run mega-projects integrating steam cracking, aromatics, and polyolefin units, each with unique hazard profiles that demand comprehensive four-layer safety architectures. Consequently, large complexes deploy thousands of point and open-path sensors, making the chemicals segment the backbone of the gas detectors market. Corporate sustainability pledges add oxygen-deficiency and carbon-dioxide monitoring where inert-gas blanketing is deployed, further lifting detector density. Process optimization councils now incorporate leak-detection analytics into flare-loss reduction targets, ensuring continued budget allocation even when chemical margins tighten.

Utilities emerge as the fastest-growing adopter segment with a 6.58% forecast CAGR thanks to urban gas-distribution modernization, smart meter rollouts, and digitization of compressor stations. Federal funding for aging pipeline replacement in the United States and cross-border interconnector upgrades in Europe underpins sustained detector demand. Electric utilities also expand monitoring in battery energy-storage systems and hydrogen-ready gas-turbine peaker plants. Water and wastewater operators add hydrogen sulfide and chlorine sensors to comply with updated NFPA 820 and EPA Clean Water Act interpretations. Mining companies invest in multigas portable fleets to track methane, carbon monoxide, and oxygen depletion in underground headings. Although oil and gas majors continue to outfit upstream and midstream assets, capex volatility linked to commodity cycles encourages vendors to diversify toward utilities and municipal infrastructure projects. This diversification supports steady baseline demand and underlines the structural resilience of the overall gas detectors market.

By Detector Type: Fixed Networks Anchor Large Sites While Portables Capture Workforce Mobility

Fixed heads captured 51.35% of 2025 revenue because continuous 24/7 monitoring around process units, compressor buildings, and storage spheres is mandatory under API RP 500 and IEC 60079 standards. Electrochemical cells dominate toxic-gas service due to favorable cost-performance ratios, whereas infrared open-path arrays guard hydrocarbon loading racks where fast wind dispersal complicates point detection. Semiconductor sensors are expanding in hydrogen service lines as operators build out electrolyzer parks and fuel-cell vehicle stations. Photo-ionization detectors protect solvent storage rooms and semiconductor fabrication lines that emit low-ppm volatile organic compounds. MEMS micro-calorimetric elements are emerging in consumer and light-industrial segments, but performance trade-offs in humidity and temperature extremes still limit heavy-industrial adoption.

Portable and transportable units are poised for a 6.72% CAGR through 2031 as worker-centric safety protocols drive personal exposure monitoring. Multigas portables now integrate color OLED screens, automatic bump checks, and Bluetooth gateways that relay exposure logs to supervisors in real time. The segment benefits from declining battery costs, enabling two-year continuous runtime designs that eliminate daily charging routines and support large-area internet-of-things compliance programs. Construction firms, shipyards, and renewable-energy sites appreciate transportable area monitors that create ad-hoc safety perimeters without erecting fixed infrastructure. Collective uptake of portables raises shipment volume, yet average selling price erosion tempers segment revenue unless vendors bundle subscription firmware and reporting analytics. Consequently, the gas detectors market share balance between fixed and portable form factors will edge closer to parity by 2031, though fixed nodes will still account for a slight majority of global revenue.

Geography Analysis

Asia-Pacific accounted for 48.60% of global revenue in 2025 and is forecast to maintain the fastest 6.92% CAGR, anchored by China’s surge in coal-to-chemicals complexes, India’s new-build refineries, and Southeast Asia’s battery-supply-chain investment wave. Frequent safety audits under China’s Ministry of Emergency Management are compelling facility operators to replace uncertified low-cost imports with ATEX and IECEx-compliant equipment. South Korea and Japan accelerate hydrogen refueling networks, each pump incorporating dual redundant hydrogen sensors as mandated by fire codes. India’s Jal Jeevan Mission triggers upgrades in chlorine and ozone monitoring across thousands of water plants, further widening demand. Domestic electronics firms ramp gallium-nitride power-switch fabrication, creating fresh opportunities for specialty ammonia and hydrogen chloride detection.

North America ranks second by revenue share, driven by OSHA enforcement, shale gas processing, and liquid-natural-gas export terminals along the Gulf Coast. New York City’s Local Law 157 requires residential natural-gas detectors by May 2025, injecting multi-million-unit volume into the residential and light-commercial slice of the gas detectors market. U.S. hydrogen hubs funded under the Infrastructure Investment and Jobs Act prescribe multigas fixed networks with encrypted wireless backbones, stimulating orders for hydrogen-specific sensors. Canada’s oil sands operations specify heaters and analyzers that remain accurate at -40 °C, favoring vendors with arctic-rated equipment lines. Mexico’s industrial corridors around Monterrey and Bajío integrate VOC detectors in auto-paint shops to meet OEM sustainability audits.

Europe maintains strict ATEX compliance, EPBD indoor-air-quality mandates, and decarbonization targets that collectively sustain steady upgrades. Germany’s large chemical basin along the Rhine invests in benzene and butadiene monitoring to cut fugitive emissions, while the United Kingdom enforces CO₂ monitoring in commercial offices to improve occupant well-being. Offshore North Sea platforms demand detector heads certified for hydrogen sulfide concentrations exceeding 100 ppm, alongside open-path infrared units that span 200 metres across platform topsides. Eastern European member states leverage EU cohesion funds to modernize district-heating plants, integrating carbon-monoxide and methane sensors into combined-heat-and-power modules. Mediterranean LNG import terminals adopt wireless flame and gas packages to retrofit legacy jetties without disrupting operations.

The Middle East and Africa region captures a smaller revenue share but sees robust adoption in green-hydrogen pilot plants, liquefaction trains, and mining expansion corridors. GCC refiners retrofit hydrocracker units to meet Euro VI sulfur limits, upgrading catalytic bead LEL heads in the process. South African gold mines face stricter Department of Mineral Resources oversight that mandates continuous fixed monitoring in deep-level shafts. In Latin America, Brazil’s pre-salt offshore fields require high-specification detectors rated for high hydrogen-sulfide concentrations, while Chile’s lithium brine processors install hydrogen-chloride analyzers to comply with environmental statutes. Collectively, these regional dynamics sustain balanced multilayer growth in the gas detectors market across the forecast horizon.

Regulatory Landscape

Compliance for gas detection equipment continues to be anchored on explosive-atmosphere and functional-safety regimes that shape certification, installation, and maintenance practices. In Europe, Directive 2014/34/EU (ATEX) remains the core legal framework for placing equipment in potentially explosive atmospheres on the market, while IECEx guidance is used to streamline acceptance across multiple jurisdictions for Ex-certified equipment and documentation.

Recent standard updates tighten technical baselines and reduce fragmentation in product qualification. IEC published IEC 60079-29-0:2025 for flammable, oxygen, and toxic gas detection equipment, and BSI released BS EN IEC 60079-29-0:2026 as the aligned national adoption, reinforcing harmonized test methods that manufacturers and end users reference in procurement specifications. In the United States, municipal and federal actions also shape deployment timing and compliance planning, including New York City Council legislation (Int 1281-2025) that extends the timeline for certain natural gas alarm requirements tied to property transactions, and a December 2025 US EPA Federal Register action extending deadlines in oil and natural gas sector standards that affect inspection and monitoring schedules.

Competitive Landscape

The competitive field is moderately fragmented. Honeywell, MSA Safety, and Emerson are leveraging global channel networks, broad sensor line-ups, and managed-service add-ons. Honeywell posted USD 9.82 billion consolidated revenue in Q1 2025, with its safety and productivity segment showing double-digit growth as Sensepoint XCL shipments scaled into smart-building retrofits. The firm’s forthcoming three-way split, slated for H2 2026, is expected to sharpen product focus and potentially unlock pure-play valuation multiples. MSA Safety reported USD 421.3 million Q1 2025 sales, with gas-detection products delivering 17% organic growth, amplified by the May 2025 acquisition of M&C TechGroup that extends sample-draw analytics expertise.[4]Source: MSA Safety Incorporated, “First-Quarter 2025 Results,” msasafety.com

Industrial Scientific pursues a subscription-heavy strategy: its iNet platform remotely calibrates more than 1 million detectors worldwide and has cut customer downtime by 40% since 2023. International Gas Detectors specializes in hydrogen-ready pellistors and holds proprietary catalyst formulations that resist silicone poisoning, a differentiation acknowledged by several electrolyzer OEMs. CO2Meter competes in fixed indoor-environment systems with controllers supporting up to 128 nodes and MODBUS integration, a feature set that wins hospitality and beverage clients. Blackline, Dräger, and Riken Keiki round out the top-tier, each emphasizing rugged portables with extended runtimes. Niche entrants in Asia offer low-cost single-gas units, pressuring price points at the lower end but struggling to pass IEC Ex audits and cybersecurity penetration tests.

Strategic moves revolve around wireless protocol certification, IEC 62443-4-2 cyber-hardening, and service-wrapped contracts that generate predictable cash flows. Several majors expanded attack surfaces by opening REST APIs for third-party analytics, positioning themselves at the center of industrial-IoT ecosystems. Patent filings show heightened activity in non-consumptive sensor films and laser-based spectroscopy, signaling a pivot toward zero-maintenance detectors that could disrupt existing calibration revenue streams. Overall, capex-to-opex business models are expected to lift lifetime customer value and sustain competitive intensity in the gas detectors market throughout the forecast period.

Gas Detectors Industry Leaders

Honeywell International Inc.

Drägerwerk AG & Co. KGaA

MSA Safety Incorporated

Industrial Scientific Corporation

Teledyne Gas & Flame Detection

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is expanding as end users standardize connected safety programs that unify portable fleets, fixed networks, and compliance workflows. Honeywell introduced enhanced capabilities for its Safety Suite 2.0 in June 2026 to provide real-time visibility into portable gas detection fleets, including historical alarm data and automated compliance workflows, which points to an addressable opportunity for vendors that combine certified sensor hardware with audit-ready software, cybersecurity controls, and managed services. This shift supports subscription and lifecycle revenue models (calibration logistics, asset tracking, reporting), especially for multi-site operators in chemicals and petrochemicals, utilities, and municipal water and wastewater systems where audit preparation and maintenance planning influence total cost of ownership.

Technology-led opportunities are also coalescing around higher-selectivity sensing and lower-maintenance architectures needed for hydrogen, LNG, and other fast-leak-risk environments, alongside tighter functional-safety expectations in buildings and commercial installations. Honeywell launched a 4-Series non-dispersive infrared (NDIR) hydrocarbon gas sensor in March 2026, highlighting demand for poisoning-resistant optical approaches in harsh industrial settings compared with legacy catalytic technologies. On the standards side, NFPA 72 (2025 edition) incorporating NFPA 715 requirements for fuel gas detection systems, and regional functional-safety requirements such as GSO EN 50402:2024 in GCC markets, provide concrete compliance pull for higher-reliability system designs and can accelerate upgrades from basic point detection toward integrated detection-and-control architectures across new builds and retrofits.

Recent Industry Developments

- June 2026: Honeywell launched enhanced capabilities for Safety Suite 2.0 to improve real-time visibility into portable gas detection fleets, adding features such as historical alarm data and automated compliance workflows. The update reinforces the market shift toward software-wrapped gas detection programs where reporting and governance features influence vendor selection alongside sensor performance.

- November 2025: MSA Safety debuted the ALTAIR io 6 Multigas Detector in Europe at the A+A International Trade Fair and Congress, highlighting a cellular-connected, six-gas platform with an integrated pump and XCell sensors. The launch broadens addressable use cases for connected, managed fleets in hazardous industries that want remote oversight and simpler compliance documentation.

- February 2024: Honeywell became the first manufacturer of gas detection solutions to join Saudi Arabia's Made in Saudi program. The move supports localization of supply and procurement alignment in the Middle East, where large energy and industrial projects increasingly prefer domestically supported equipment and services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers revenues generated from gas detectors used to identify hazardous gas presence and help prevent incidents across industrial and commercial settings. It includes fixed installations and portable or transportable detectors, along with the common communication setups used to connect or monitor them.

Scope exclusions: It excludes standalone laboratory analyzers and process control instrumentation that measure gas composition for production quality rather than safety monitoring.

Segmentation Overview

- By Communication Type

- Wired

- Wireless

- By End-User Industry

- Oil and Gas

- Chemicals and Petrochemicals

- Water and Wastewater

- Metal and Mining

- Utilities

- Other End-User Industries

- By Detector Type

- Fixed

- Electrochemical

- Semiconductor

- Photo-ionization

- Catalytic

- Infra-red

- MEMS

- Portable and Transportable

- Multi-Gas

- Single-Gas

- Fixed

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to shape the demand map and keep assumptions realistic before we spoke with industry participants. We referred to public safety and compliance references such as OSHA guidance, NFPA standards, and mine safety publications where relevant, and we also used trade and production statistics from sources such as the US Census Bureau, UN Comtrade, Eurostat, and the International Energy Agency to understand activity in key end-use industries.

Company annual reports, investor decks, and press releases helped us identify product mix shifts, typical selling routes, and broad pricing direction for fixed versus portable units. For additional cross-checks, we used paid subscriptions for company financials and news intelligence, import and export shipment level data where applicable, and patent databases to sanity check technology adoption timing. These examples are not exhaustive, and many other public and paid sources were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on filling the gaps that desk sources do not explain well, especially around mix between fixed and portable deployments, replacement cycles, and average selling price movement by region. We spoke with manufacturers, channel partners, system integrators, and end users across APAC, EMEA, and the Americas, so the assumptions could be checked against observed procurement patterns and planned safety upgrades.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 44% |

| Mid tier: 55% | Functional/Unit leaders: 34% | EMEA: 31% |

| Smaller Players: 17% | Managers: 51% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where industrial activity and safety spending signals are translated into an addressable demand pool for gas detection, and then aligned to the split between fixed systems and portable or transportable devices. To keep it grounded, results are corroborated with selective bottom-up approximations, such as rolling up a sampled set of supplier revenues, checking distributor throughput in a few regions, and validating implied ASP times unit volumes against what buyers report.

Key inputs used in the model include indicative installed base and replacement timing for detectors in high risk sites, the share of wired versus wireless deployments in new and retrofit projects, expansion activity in oil and gas and chemicals, mining safety enforcement intensity, and the relative pricing spread between fixed detectors, portable multi-gas units, and accessories. Forecasting is done using scenario analysis supported by variable trends, and then tightened using simple regression style relationships where interview feedback indicates a stable link between industry output and detector demand. Where bottom-up detail is missing in smaller countries, we bridge gaps using proxy indicators like sector output and import patterns, followed by a consistency check against regional penetration ranges shared by respondents.

Data Validation & Update Cycle

Validation is done in layers so one data point does not drive the outcome. Model outputs are compared with independent signals such as implied units shipped, end-user capex direction in hazardous industries, and trade flows for relevant product categories, and then large variances are reviewed and resolved. When something looks off, assumptions are reopened and, where needed, respondents are re-contacted to confirm whether the change is structural or primarily timing-driven.

Each report goes through multi-step analyst reviews before sign-off, with particular attention to calculation logic, currency treatment, and growth drivers so they remain internally consistent. The report is refreshed annually, and interim updates are made when material events change pricing, regulations, or industrial activity. Before delivery, a final pass is completed to ensure the latest public and interview-led signals are reflected.

Mordor Intelligence's Gas Detectors Market Size Measured Against Other Published Estimates

Published market sizes for gas detectors often differ because refresh timing and currency conversion points do not always match, and because pricing assumptions can shift when the mix changes between fixed and portable deployments. Differences also show up when some studies include a wider equipment bundle, which can raise totals even if unit demand is similar.

In this study, the estimate is kept stable by rechecking ASP steps (by form factor and region) and by locking currency timing to the same reference window used across the dataset. Those outputs are then revalidated against industrial activity and shipment signals, following the refresh-led routine applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.14 B (2026) | |

| Industry Research Publisher A | USD 3.11 B (2025) | Uses an earlier base year and a longer forecast window, and the method is less explicit on how ASP is updated for portable multi-gas units versus fixed systems, which can compress the near-term market value. |

| Business Research Portal B | USD 5.75 B (2024) | Broader scope is implied by the term gas detection equipment, which can include systems, bundles, and adjacent monitoring components, and it also applies a different currency year and faster growth case that lifts the headline size. |

Looking across the three figures, the spread is mainly explained by scope boundaries and by how pricing and currency timing are handled year to year. By keeping the inputs tied to clear demand signals, and by separating detector revenues from wider equipment bundles, the final number stays traceable and can be repeated when assumptions are revisited.

Key Questions Answered in the Report

What is the current global gas detectors market size and growth outlook through 2031?

The market is valued at USD 3.14 billion in 2026 and is projected to reach USD 4.01 billion by 2031 at a 5.01% CAGR.

Which region will contribute the most incremental demand for gas detectors by 2031?

Asia-Pacific is set to provide the largest absolute growth, expanding at a 6.92% CAGR due to rapid industrialization and hydrogen infrastructure buildouts.

Which detector form factor is growing fastest?

Portable and transportable units are forecast to rise at a 6.72% CAGR as workforce mobility and confined-space rules spur adoption.

What communication technology trend is reshaping new installations?

Wireless mesh networks are gaining traction, growing at a 7.05% CAGR, because they cut cabling costs and enable rapid turnaround deployments.

Page last updated on: