Large Volume Parenteral (LVP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

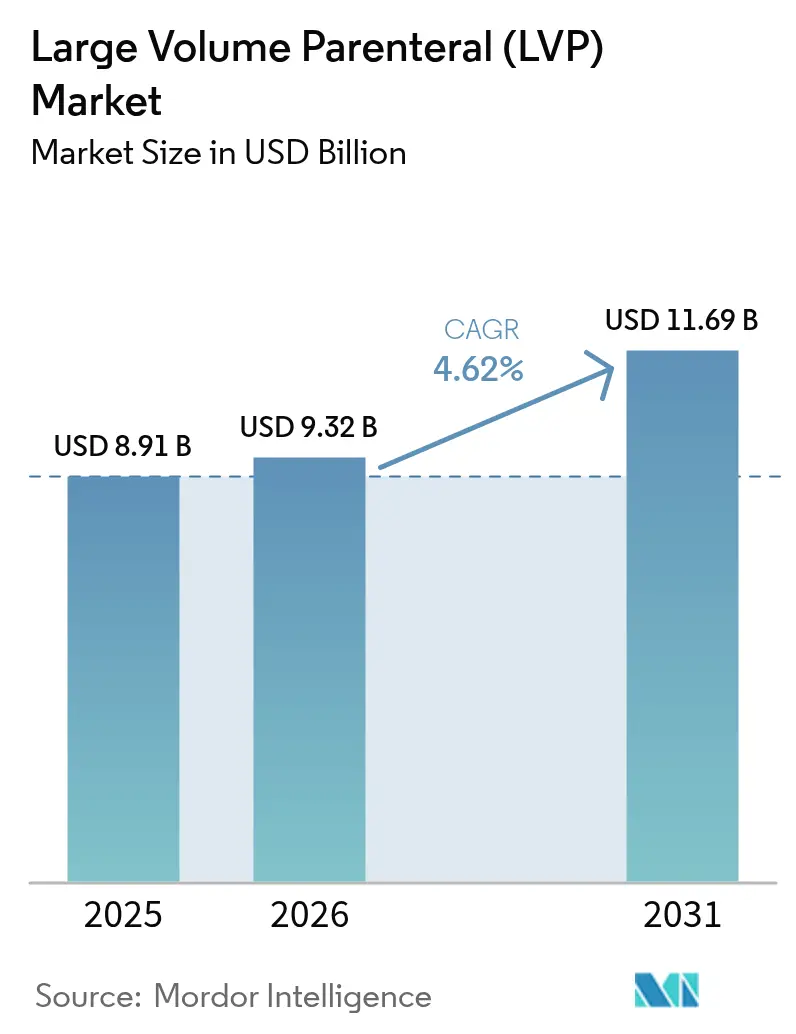

| Market Size (2026) | USD 9.32 Billion |

| Market Size (2031) | USD 11.69 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Large Volume Parenteral (LVP) Market Analysis by Mordor Intelligence

The Large Volume Parenteral Market size is projected to be USD 8.91 billion in 2025, USD 9.32 billion in 2026, and reach USD 11.69 billion by 2031, growing at a CAGR of 4.62% from 2026 to 2031.

Rising surgical case counts, an expanding chronic disease burden, and broader adoption of automated aseptic processing collectively underpin this stable trajectory. Demand also benefits from home-based infusion programs that shift IV therapy outside hospitals, while regulatory recognition of Blow-Fill-Seal (BFS) technology accelerates capacity expansion. Supply chain investments in polymer bags and pharmaceutical-grade water infrastructure continue to improve manufacturing resilience, even as glass vial shortages linger. Competitive strategies center on scale, vertical integration, and technology upgrades, indicating a structurally moderate yet steadily evolving landscape for the large-volume parenteral market.

Key Report Takeaways

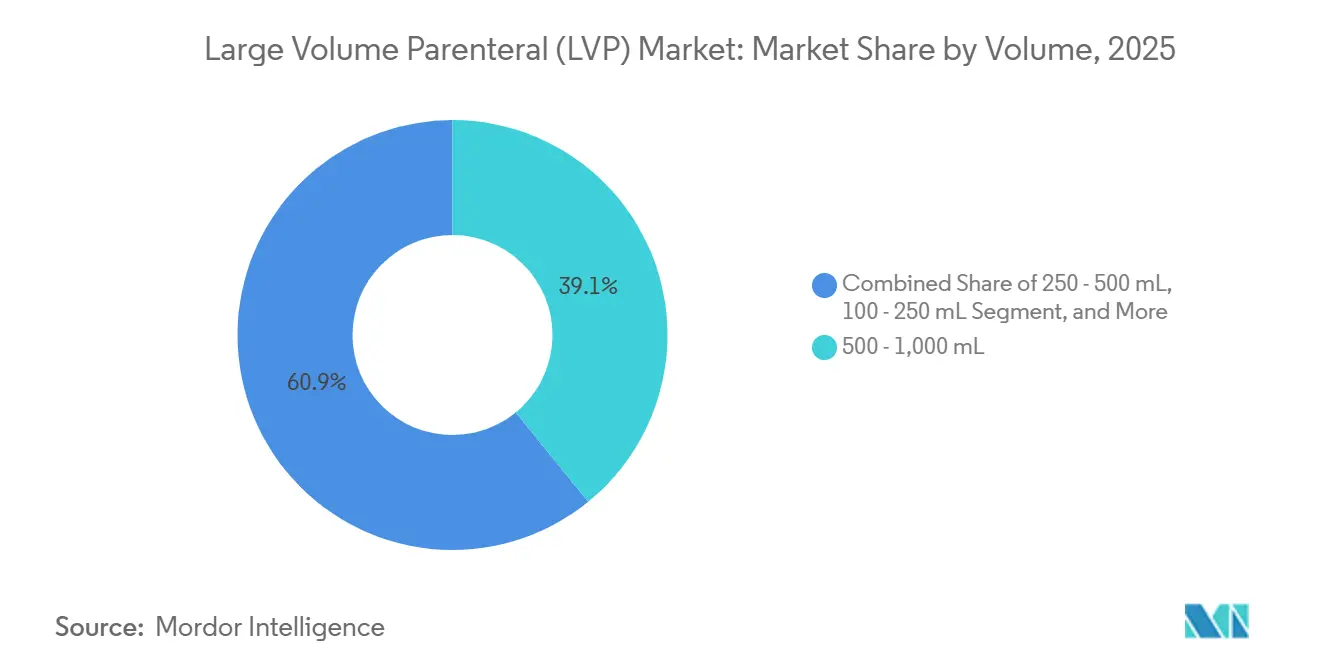

- By volume segment, 500-1,000 mL formats led with 39.12% of the large volume parenteral market share in 2025; >2,000 mL containers are forecast to log a 9.08% CAGR through 2031.

- By application, therapeutic injections captured 45.10% of the revenue share in 2025; nutritious/parenteral nutrition products are advancing at a 9.88% CAGR through 2031.

- By type of packaging, flexible bags accounted for 62.95% in 2025 and an 8.74% CAGR through 2031.

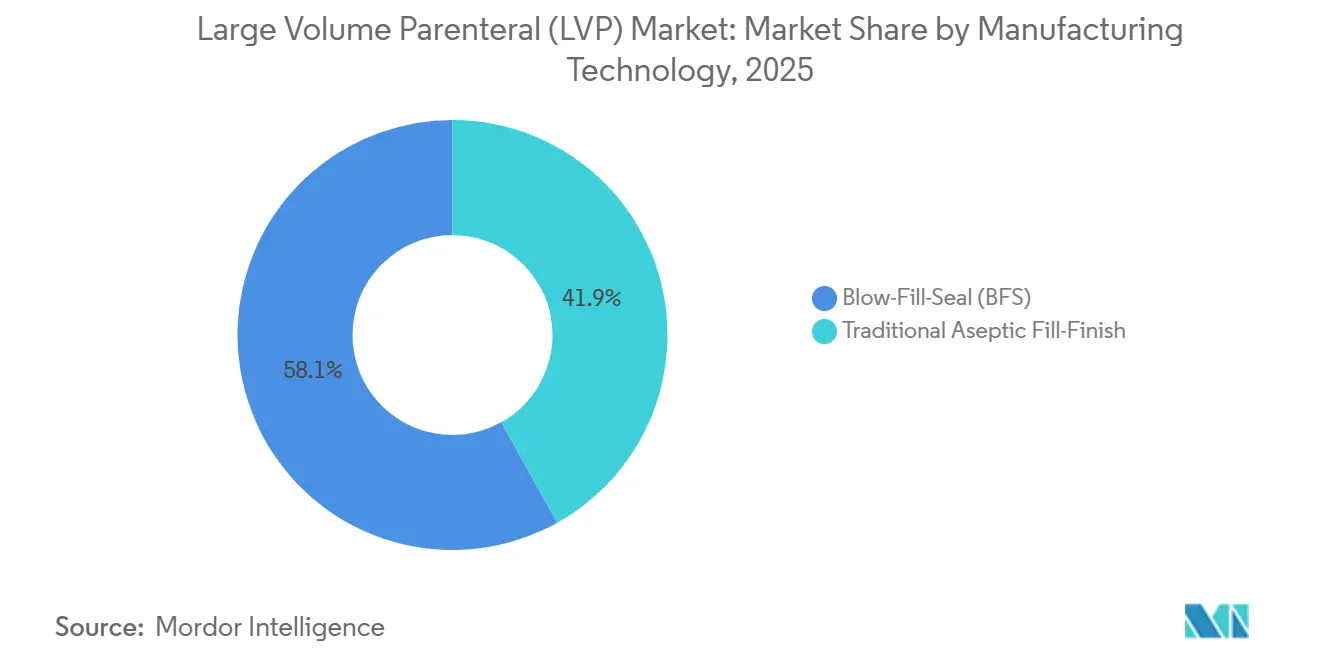

- In terms of manufacturing technology, blow-fill-seal (BFS) accounted for 58.10% in 2025 and posted an 8.12% CAGR through 2031.

- By end user, hospitals accounted for 62.98% of revenue in 2025, and ASCs are projected to register the fastest growth at a 9.41% CAGR.

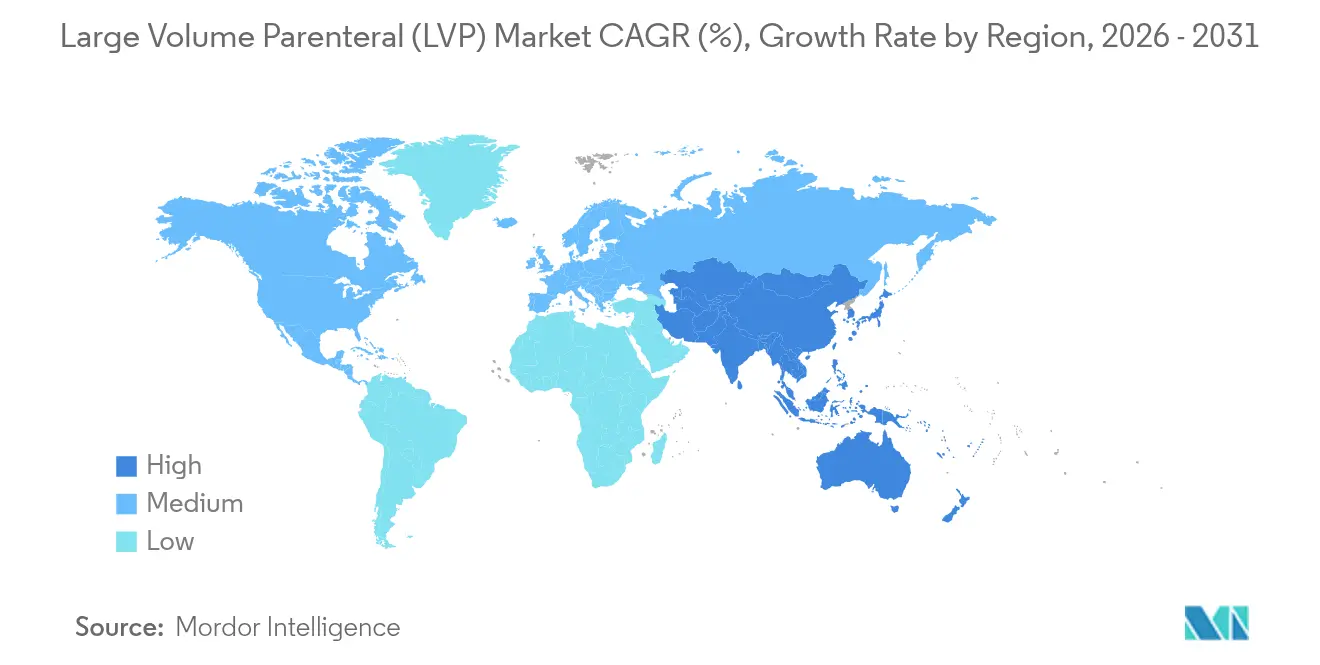

- By geography, North America accounted for 35.25% of the large-volume parenteral market in 2025, whereas Asia-Pacific is projected to expand at an 8.63% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Large Volume Parenteral (LVP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising surgical volumes worldwide | +1.2% | North America, Europe | Medium term (2-4 years) |

| Growing chronic disease prevalence & fluid replacement therapy adoption | +0.9% | Global, aging markets | Long term (≥ 4 years) |

| Expansion of home-based infusion & parenteral nutrition programs | +0.8% | North America, Europe, APAC | Medium term (2-4 years) |

| Adoption of BFS & other automated aseptic technologies | +0.7% | Regulated markets worldwide | Short term (≤ 2 years) |

| Shift toward large-volume wearable/SC injectors | +0.5% | North America, Europe | Long term (≥ 4 years) |

| Supply-chain investments in WFI & ready-to-use multichamber bags | +0.4% | Global manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Volumes Worldwide

Elective procedure throughput recovered sharply in 2024, exceeding 2019 baselines by 12% as hospitals addressed pandemic-era backlogs.[1]American College of Surgeons, “National Surgical Quality Improvement Program Annual Report,” FACS.org Each surgical event typically consumes 2–4 L of IV fluids, thereby increasing aggregate demand for the large-volume parenteral market. Growing robotic surgery uptake, up 18% in 2024, extends operating times and thus elevates perioperative fluid requirements. An aging patient cohort intensifies this pattern, as individuals over 65 often require greater volume to maintain hemodynamic stability. Elective orthopedic, cardiovascular, and oncology procedures surpassed pre-pandemic counts in 2025 as hospitals cleared backlogs and increased operating-room throughput. Each procedure typically uses multiple isotonic saline or lactated Ringer’s bags for intra-operative hemodynamic management, lifting per-day fluid demand in surgical suites.

Growing Chronic Disease Prevalence & Fluid Replacement Therapy Adoption

Chronic kidney disease affects 850 million people, and dialysis protocols alone represent a USD 2.8 billion fluid segment. Heart failure reached 64 million global cases in 2024, spurring demand for specialized electrolyte solutions. The Centers for Disease Control and Prevention recorded a 23% rise in diabetes-related hospitalizations requiring IV therapy, where typical diabetic ketoacidosis care involves 6–8 L of fluids per episode.[2]Centers for Disease Control and Prevention, “Diabetes-Related Hospitalizations Annual Report,” CDC.gov The International Diabetes Federation recorded 589 million adults living with diabetes in 2025 and projects 853 million by 2050; many will need periodic intravenous rehydration to correct electrolyte imbalance.[3]U.S. Food and Drug Administration, “Container-Closure System Testing Guidance,” FDA.gov

Expansion of Home-Based Infusion & Parenteral-Nutrition Programs

Medicare approved 47 new home parenteral nutrition (HPN) reimbursement pathways in 2024, saving USD 3,200 per patient episode and enlarging the eligible population to 180,000 annual recipients. Average at-home consumption now stands at 42 L per patient each month. FDA guidance on patient-controlled infusion devices further legitimizes wearable pumps capable of delivering 500 mL per hour, broadening the addressable base for the large-volume parenteral market. Home-infusion providers prefer pre-mixed, extended-shelf-life bags produced on blow-fill-seal lines because they minimize patient handling and infection risk. The National Home Infusion Association logged an 18% increase in patient volumes in 2024, with antibiotics, immunoglobulins, and parenteral nutrition topping utilization.

Adoption of Blow-Fill-Seal & Other Automated Aseptic Technologies

Manufacturers invested USD 1.2 billion in BFS capacity in 2024, motivated by sterility assurance levels of 10^-6 that far exceed those of traditional fill-finish processes. BFS eliminates the need for separate washing and depyrogenation steps, reducing production time by 40% and lowering contamination risk. EMA quality guidelines released in 2024 explicitly promote BFS for parenteral solutions, accelerating global convergence on this automated standard. ICU Medical and Otsuka committed USD 200 million in November 2024 to build a 1.4 billion-unit BFS facility in Japan, underscoring the technology’s scalability.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex formulation & E&L compliance challenges | −0.6% | Regulated markets worldwide | Medium term (2-4 years) |

| Price pressures & reimbursement caps in high-volume tenders | −0.8% | North America, Europe, emerging markets | Short term (≤ 2 years) |

| Glass-packaging shortages & material recall risks | −0.4% | Global, acute in APAC | Short term (≤ 2 years) |

| Emerging shift of some biologics from IV to SC | −0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price Pressures and Reimbursement Caps in High-Volume Tenders

Group purchasing organizations in the United States and single-payer systems in Europe bundle saline and dextrose solutions into multi-year contracts with 2–5% annual price deflators, compressing supplier margins. India’s National Pharmaceutical Pricing Authority and China’s volume-based procurement scheme extended similar caps in 2024, cutting bid prices by an average 18%. Manufacturers respond by closing low-margin glass-bottle lines and consolidating production in lower-cost regions, but these moves risk supply fragility, as seen in 2024, when a recall triggered spot shortages across North America. Margin compression also deters investment in premium features such as RFID tracking or bio-based polymers, slowing innovation.

Complex E&L Compliance for Next-Generation Multilayer Bags

United States Pharmacopeia chapters <661> and <1663>, and European Pharmacopoeia requirements, require exhaustive chromatography-mass spectrometry studies for new polymers, adding 12–18 months and USD 2–5 million to each formulation cycle. Smaller contract fillers often lack analytical infrastructure and cede market share to integrated players able to finance the work. The challenge intensifies when PFAS regulations require reformulating fluoropolymer seals, triggering a new compliance loop. Divergent FDA and EMA guidance complicates global launches and inflates costs, delaying market entry for innovations that would otherwise elevate patient safety and sustainability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Volume: High-Dose Formats Gain as Nutrition Protocols Intensify

The >2,000 mL category will post a 9.08% CAGR through 2031, buoyed by oncology and critical-care protocols that demand continuous delivery for 24-48 hours. Manufacturing advances have shaved 18% off production costs for these ultra-large containers since 2024. Meanwhile, the 500-1,000 mL range retained 39.12% large volume parenteral market share in 2025, due to standardized intra-operative and emergency guidelines that specify this mid-sized format. Regulatory bodies favor larger units to minimize line changes, further anchoring growth. Smaller segments serve pediatric and outpatient needs and collectively add resilience by diversifying end-use profiles in the large volume parenteral market.

By Application: Nutrition Formulations Gain Momentum

Therapeutic injections dominated 2025 revenues at 45.10%, covering antibiotics, chemotherapy agents, and specialty drugs that require dilution in large volumes for safe infusion. Nutritious formulations, however, are accelerating at a 9.88% CAGR on the back of expanded HPN coverage and longer shelf-life stability. Customized amino-acid and lipid blends now match patient-specific metabolic profiles, supporting premium price points that offset volume discounts elsewhere in the large volume parenteral market.

By Type of Packaging: Flexible Bags Secure Trust

Flexible polymer bags captured 62.95% share in 2025, driven by superior breakage resistance and a 35% lower carbon footprint than glass. Reduced particle contamination risk, 40% smaller storage footprints, and fewer supply constraints position bags as the default option for high-volume products in the large volume parenteral market. Glass containers still serve niche needs-primarily concentrated electrolyte or cytotoxic solutions-but face capacity shortfalls that triggered USD 371 million in new glass production investments during 2024.

By Manufacturing Technology: Automation Becomes the Norm

BFS lines held 58.10% share in 2025 and are forecast to grow 8.12% annually to 2031, reflecting a sector-wide pivot toward integrated, human-free aseptic processing. Hybrid BFS machines now accommodate 3,000 mL units, extending automation benefits into the larger-format corner of the large volume parenteral market. Legacy fill-finish processes persist only for formulations that remain incompatible with current BFS parameters.

By End User: Home-Care Settings Show the Fastest Uptake

Hospitals still absorbed 62.98% of 2025 volumes, but Home-Care & Alternate Site Infusion settings are expanding at 9.41% CAGR. CMS reimbursement revisions and remote-monitoring pumps with cellular connectivity have eased safety and payment barriers, widening patient eligibility for home-based large-volume therapy.

Geography Analysis

North America commanded 35.25% of 2025 revenues, anchored by high procedure counts, advanced reimbursement systems, and established regulatory pathways. Market leaders leverage dense distribution networks that secure timely deliveries to urban and rural facilities alike. Robust insurance coverage also cushions price pressures in the large volume parenteral market.

Asia-Pacific is the fastest-growing territory at 8.63% CAGR through 2031. India’s Production Linked Incentive scheme injected more than USD 2 billion into sterile injectable facilities, lifting domestic output 25%. China slashed approval timelines by 40% in 2024, enabling local firms to capture share in both domestic and export channels. Aging populations in Japan and South Korea further amplify demand.

Europe retains a sizable footprint owing to stringent but harmonized EMA standards that streamline multi-country registrations. Sustainability mandates push hospitals toward recyclable polymer bags, giving European suppliers an early-adopter advantage in green packaging. Germany leads adoption of hybrid BFS lines, reinforcing the competitive position of the European large volume parenteral market.

Emerging regions in Latin America, the Middle East, and Africa report double-digit unit growth, albeit from small bases. Infrastructure upgrades, donor-funded health programs, and gradual regulatory modernization provide incremental tailwinds, but supply chain gaps persist.

Competitive Landscape

The large volume parenteral market features moderate concentration. Baxter, Fresenius Kabi, and B. Braun collectively hold a commanding share through extensive manufacturing footprints and regulated-market dossiers. These incumbents prioritize vertical integration to secure raw materials and deploy capital into BFS lines and polymer-bag conversions that raise quality consistency.

Regional producers compete on price and logistics agility, especially in Asia-Pacific where government tenders favor local content. Schott Pharma’s USD 371 million outlay for pharmaceutical-grade glass expands capacity to relieve container shortages, reducing dependency on a few high-technology furnaces.

Innovation themes now include smart infusion pumps that interface with electronic health records to automate dose tracking, as well as on-demand compounding solutions for personalized amino acid mixes. Contract development and manufacturing organizations (CDMOs) with BFS expertise offer scale-up pathways for biologics transitioning from small-volume vials to large-volume infusion formats.

Large Volume Parenteral (LVP) Industry Leaders

Pfizer, Inc

B. Braun SE

Otsuka Pharmaceutical Co.

Fresenius Kabi AG

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Sanjivani Parenteral Limited began commercial production of intravenous fluids at its new Pune, India facility.

- May 2025: ICU Medical and Otsuka Pharmaceutical announced a USD 200 million joint venture to construct an IV manufacturing plant in Japan with 1.4 billion-unit annual capacity, scheduled to open in Q4 2026.

- January 2025: Lakeside Holding subsidiary Hupan Pharmaceutical signed distribution agreements with Hubei Kelun to supply large volumes of parenteral solutions across China.

Global Large Volume Parenteral (LVP) Market Report Scope

As per the scope of the report, large-volume parenteral refers to intravenous solutions with volumes greater than 100 ml, commonly prescribed to correct fluid and electrolyte disturbances, provide nutrition, or serve as a vehicle for administering drugs. Commonly used large-volume parenteral preparations include infusions of amino acids, mannitol, dextrose, lactated Ringer's injection, Ringer's injection, and sodium chloride injection.

The large-volume parenteral (LVP) market is segmented by volume, application, packaging type, manufacturing technology, end user, and geography. By volume, the market is segmented into 100 ml - 250 ml, 250 ml - 500 ml, 500 ml - 1000 ml, 1000 ml - 2000 ml, and 2000 ml and more. By application, the market is segmented into therapeutic injections, fluid-balance injections, and nutritional injections. By packaging type, the market is segmented into bottles and bags. By manufacturing technology, the market is segmented into traditional aseptic fill-finish and blow-fill-seal (BFS). By end user, the market is segmented into hospitals, home care & alternate-site infusion, and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle-East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| 100 - 250 mL |

| 250 - 500 mL |

| 500 - 1,000 mL |

| 1,000 - 2,000 mL |

| >2,000 mL |

| Therapeutic Injections |

| Fluid-Balance Injections |

| Nutritious/Parenteral-Nutrition Injections |

| Glass Bottles |

| Flexible Bags (PVC, Non-PVC) |

| Traditional Aseptic Fill-Finish |

| Blow-Fill-Seal (BFS) |

| Hospitals |

| Home-Care & Alternate-Site Infusion |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Volume | 100 - 250 mL | |

| 250 - 500 mL | ||

| 500 - 1,000 mL | ||

| 1,000 - 2,000 mL | ||

| >2,000 mL | ||

| By Application | Therapeutic Injections | |

| Fluid-Balance Injections | ||

| Nutritious/Parenteral-Nutrition Injections | ||

| By Type of Packaging | Glass Bottles | |

| Flexible Bags (PVC, Non-PVC) | ||

| By Manufacturing Technology | Traditional Aseptic Fill-Finish | |

| Blow-Fill-Seal (BFS) | ||

| By End User | Hospitals | |

| Home-Care & Alternate-Site Infusion | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the large volume parenteral market?

The sector is valued at USD 9.32 billion in 2026 and is projected to reach USD 11.69 billion by 2031 at a 4.62% CAGR.

Which volume range holds the largest revenue share?

Containers sized 500-1,000 mL accounted for 39.12% of 2025 sales, making them the dominant format.

Why are flexible polymer bags preferred over glass bottles?

Bags minimize breakage, cut storage needs by 40%, and show a 35% lower carbon footprint, all while mitigating particle contamination risk.

What technology is gaining favor for aseptic manufacturing?

Blow-Fill-Seal technology led with 58.10% share in 2025 and continues to grow due to superior sterility assurance and cost efficiency.

Which region is expanding the fastest?

Asia-Pacific is forecast to grow at an 8.63% CAGR through 2031, driven by large-scale manufacturing investments and streamlined regulatory approvals.

How are home-based infusion programs influencing demand?

CMS reimbursement expansions and wearable infusion pumps have boosted home-care adoption, pushing the home segment to a 9.41% CAGR.

Page last updated on: