Parenteral Nutrition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.99 Billion |

| Market Size (2031) | USD 11.94 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

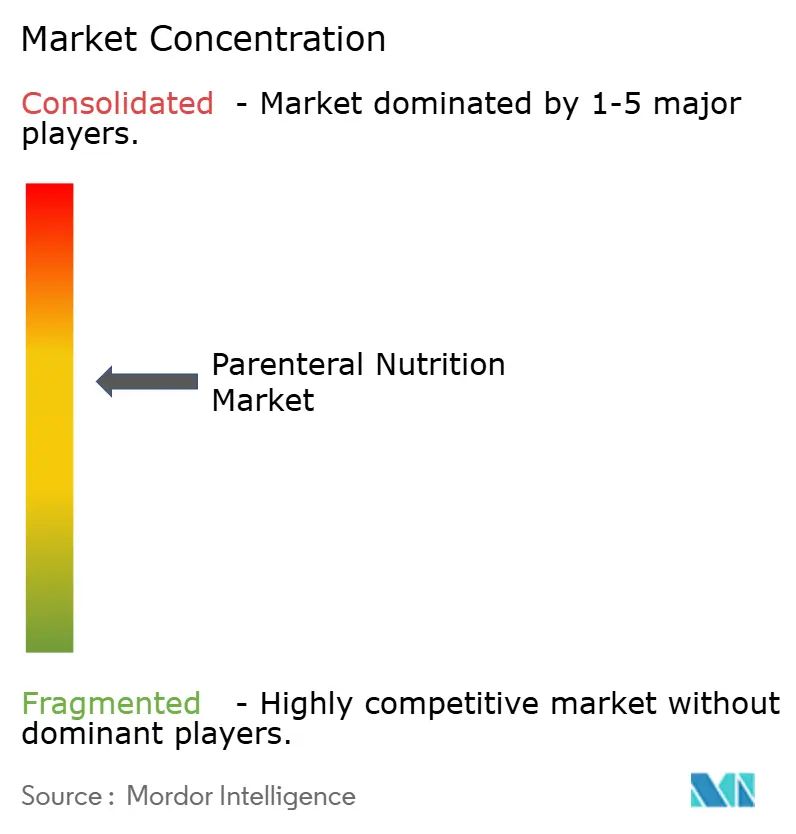

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Parenteral Nutrition Market Analysis by Mordor Intelligence

The parenteral nutrition market size was valued at USD 8.50 billion in 2025 and estimated to grow from USD 8.99 billion in 2026 to reach USD 11.94 billion by 2031, at a CAGR of 5.82% during the forecast period (2026-2031). An ageing global population primarily supports expansion, the clinical focus on early-life nutrition for pre-term infants, and rising chronic disease prevalence that extends the duration of nutritional support. Hospitals are integrating multi-chamber bag systems that shorten preparation time by 62% and cut medication errors by 54%, allowing pharmacists to redeploy labor to higher-value tasks. Regional sourcing of amino acids, backed by a USD 17.5 million federal award to Resilience, is strengthening supply security after recent ingredient shortages. Simultaneously, broader reimbursement for home-based care, coupled with portable infusion pumps, is accelerating adoption beyond inpatient settings. These intertwined factors keep the parenteral nutrition market on a steady upward trajectory.

Key Report Takeaways

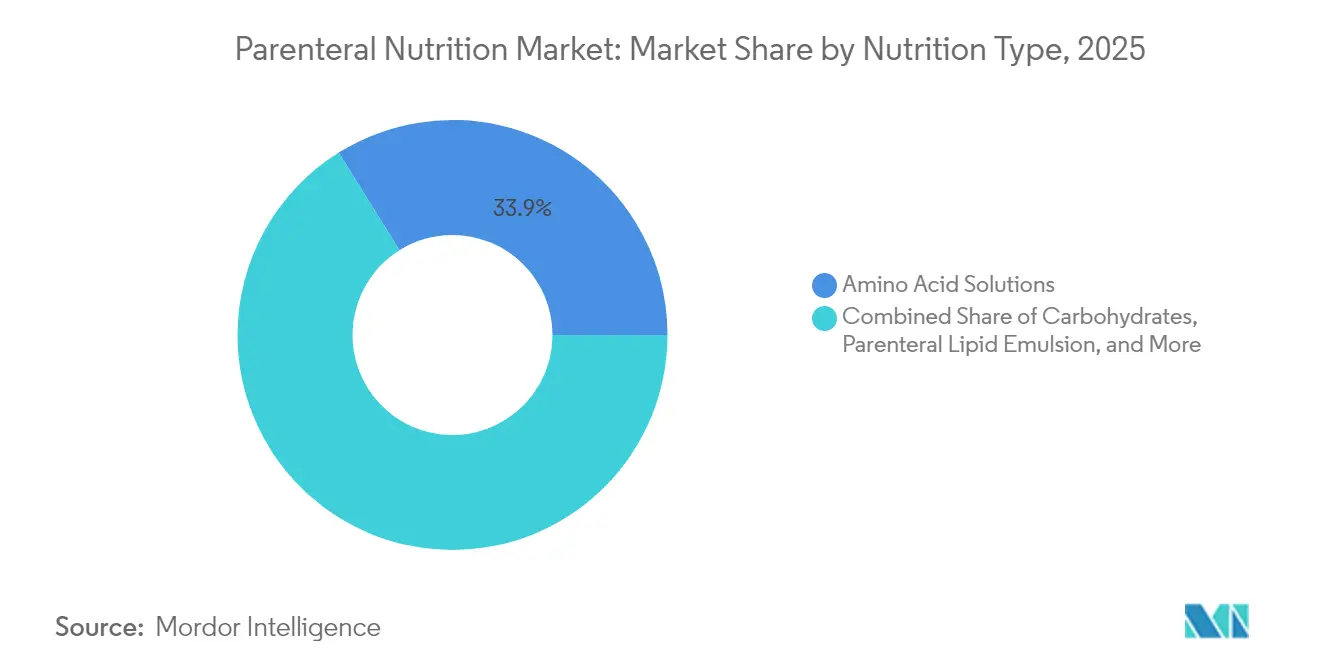

- By nutrition type, amino acid solutions led with 33.88% of the parenteral nutrition market share in 2025, and the segment is forecast to advance at a 5.52% CAGR to 2031.

- By patient type, adults held 64.25% of revenue in 2025, while the neonatal cohort is projected to expand at a 6.54% CAGR through 2031.

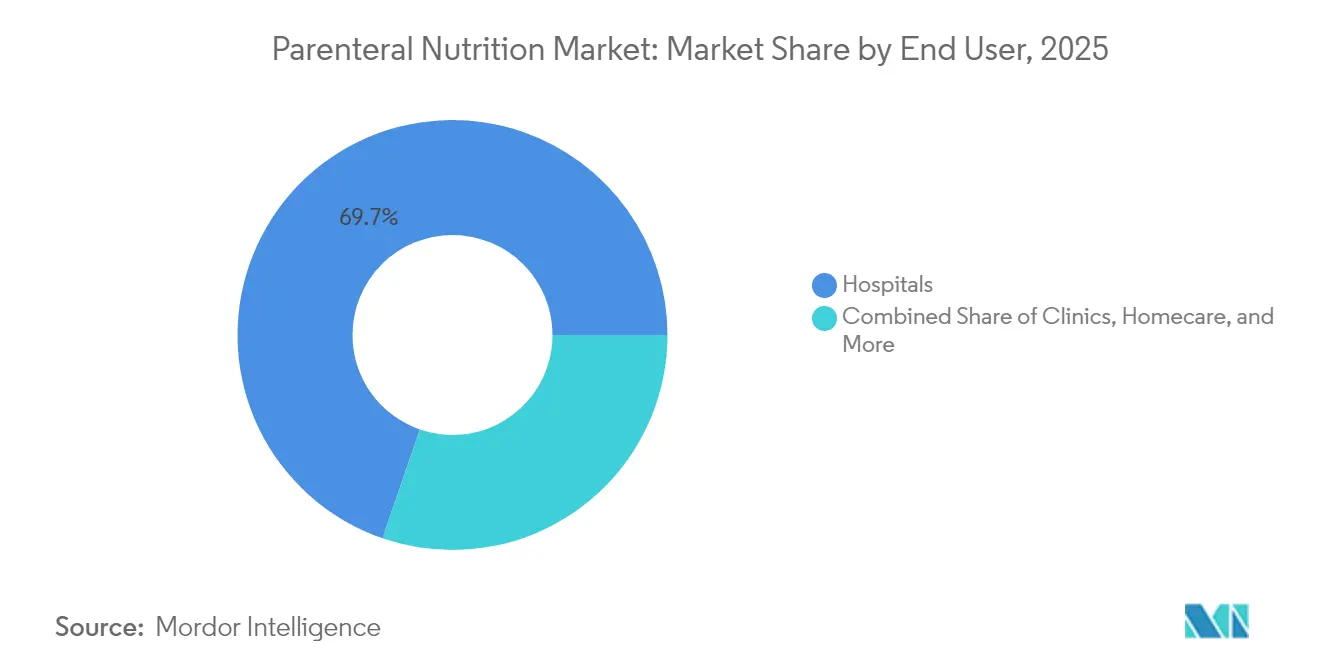

- By end-user, hospitals commanded 69.72% of sales in 2025, whereas homecare is expected to grow at an 7.98% CAGR over the forecast period.

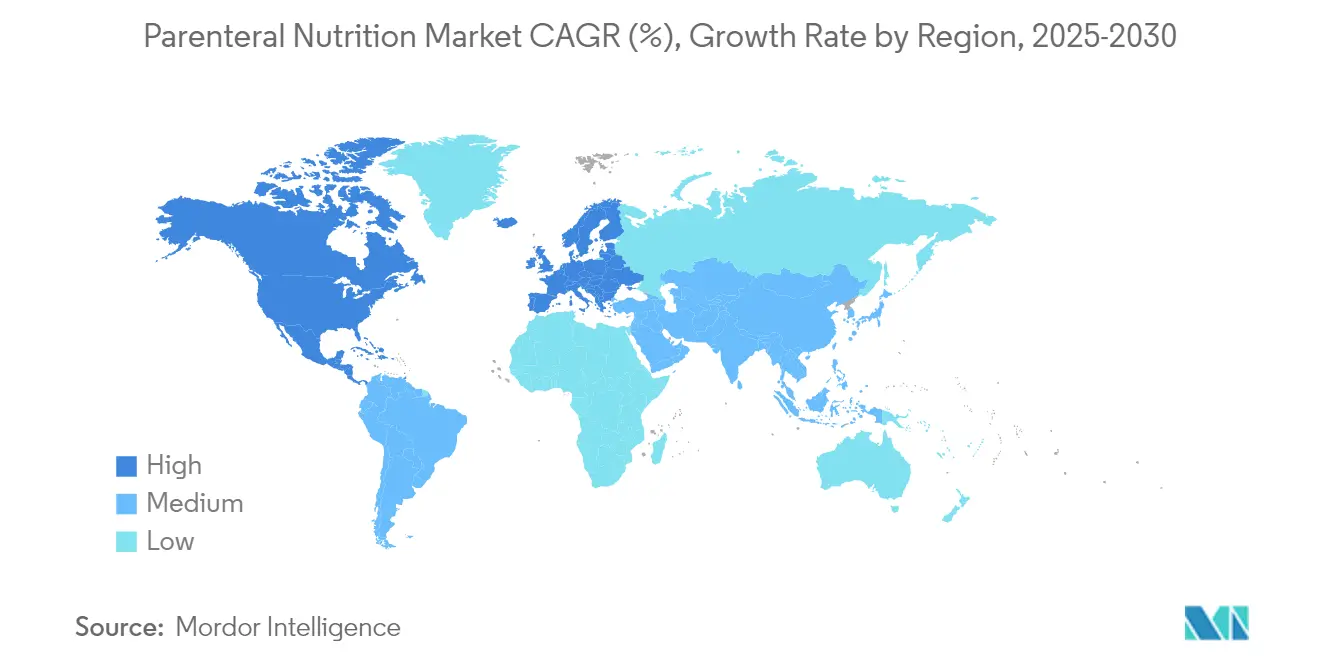

- By geography, North America led with roughly 43.85% of revenue in 2025, while Asia-Pacific is anticipated to post the fastest growth at about 6.84% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Parenteral Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Rate of Pre-Mature Births | +0.80% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Increasing Burden of Chronic Conditions | +1.20% | Global, particularly APAC and North America | Long term (≥ 4 years) |

| Rising Prevalence of Malnutrition | +1.00% | Global, with acute needs in developing regions | Medium term (2-4 years) |

| Rapid Uptake of Multi-Chamber Bag Technology | +0.90% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Supply-Chain Localization of Amino-Acid Components | +0.60% | North America & Europe primarily | Long term (≥ 4 years) |

| Expansion Of Reimbursement for Home Parenteral Nutrition | +0.70% | North America & Europe, selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Rate of Pre-Mature Births

Higher survival rates of low-birth-weight infants sustain a strong need for intravenous nutrition. Early amino acid delivery within 24 hours supports superior weight gain and neurodevelopment compared with delayed feeding.[1]Andrew Smith, “Early Parenteral Amino Acid Delivery in Preterm Infants,” Frontiers in Nutrition, frontiersin.org Triple-chamber neonatal bags now supply 2.8 g kg¹ of amino acids and 80 kcal kg¹ daily, aligning bedside practice with updated guidelines. Hospitals also record fewer compounding errors because pharmacy staff activate pre-filled chambers instead of mixing individual components. Broader use of these dedicated bags ensures consistent nutrient profiles that reduce metabolic stress in fragile neonates. Altogether, neonatal demand anchors a reliable growth pillar within the parenteral nutrition market.

Increasing Burden of Chronic Conditions

Chronic illnesses such as inflammatory bowel disease, short bowel syndrome, and malignancy-related cachexia expand the long-term user base. Poland’s reimbursement for home intravenous nutrition exceeded EUR 146 million (USD 167 million) in 2024, illustrating the fiscal weight of sustained therapy. Combined enteral and parenteral regimens let physicians meet higher energy targets, improving survival in complex adult patients. Medicare’s policy change that removed restrictive coverage determinations further opened access to home programs in the United States.[2]Andrew Smith, “Early Parenteral Amino Acid Delivery in Preterm Infants,” Frontiers in Nutrition, frontiersin.orgGiven long disease duration, the parenteral nutrition market gains a dependable stream of recurring demand across public and private payers.

Rising Prevalence of Malnutrition

Systematic screening shows that 53% of hospitalized adults meet diagnostic malnutrition criteria and face double the one-year mortality risk compared with well-nourished peers. Where oral intake fails, intravenous nutrition provides a definitive route to close nutrient gaps. Audits in Japan revealed 82.9% of patients on total parenteral nutrition receive amino acids below 1.0 g kg¹, underscoring practice gaps and prospective volume upside. Hospitals that implement mandatory nutrition support teams report shorter stays and fewer readmissions, outcomes that translate into quantifiable savings for payers. These findings fuel administrative support for broader adoption, reinforcing the parenteral nutrition market outlook.

Rapid Uptake of Multi-Chamber Bag Technology

Multi-chamber systems shorten pharmacy workflow from 14.3 minutes to 5.5 minutes per bag and drop bloodstream infection rates from 6.8% to 2.1%, saving USD 11,552 per admission. Unit-dose format also curtails wastage of high-cost micronutrients, a pressing concern amid periodic trace-element shortages. Lower handling steps mean fewer opportunities for compounding errors, enhancing patient safety in busy wards. As guidelines pivot toward standardized formulations, multi-chamber adoption continues to ramp in North America and Western Europe. Technology, therefore, acts as both an efficiency lever and a growth catalyst inside the parenteral nutrition market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack Of Awareness in Developing Countries | -0.40% | APAC, Latin America, Africa primarily | Long term (≥ 4 years) |

| High Risk of Catheter-Related Infections & Sepsis | -0.60% | Global, with acute impact in resource-limited settings | Medium term (2-4 years) |

| Volatile Pricing & Shortages of Critical Parenteral Nutrition Ingredients | -0.50% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Antimicrobial-Stewardship Limits on Soybean Lipid Use | -0.30% | North America & Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Risk of Catheter-Related Infections & Sepsis

Catheter-associated bloodstream infections range from 0.97 to 10.97 per 1,000 catheter days and nearly double inpatient mortality. Antimicrobial lock therapy can cut events below 1.1 per 1,000 catheter days, but widespread rollout requires specialised staff and higher consumable budgets. Some facilities still lack dedicated nutrition support teams, prolonging device dwell time and raising infection odds. As payers tighten sepsis penalties, hospitals may hesitate to start parenteral nutrition when enteral options exist. These safety concerns partly temper growth, yet advances in antimicrobial dressings and education programs are gradually mitigating risk.

Volatile Pricing & Shortages of Critical Ingredients

Global shortages of IV fluids and amino acids periodically disrupt therapy schedules. Hurricane Maria demonstrated how a single manufacturing outage can ripple worldwide and lead to rationing. Australia’s recent saline deficit triggered conservation protocols that delayed the start of non-urgent parenteral nutrition.[3]Centers for Medicare & Medicaid Services, “Medicare Coverage Policy Changes for Home Parenteral Nutrition,” CMS.gov Although multi-sourcing and domestic plants lower vulnerability, raw material prices remain sensitive to energy costs and geopolitical instability. Temporary ingredient spikes inflate hospital budgets and can prompt formulary restrictions. Consequently, supply volatility introduces planning uncertainty across the parenteral nutrition market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nutrition Type: Amino Acids Drive Clinical Outcomes

Amino acid solutions secured 33.88% of the 2025 revenue base, the most significant slice within the parenteral nutrition market share. The component advances at 5.52% CAGR to 2031 as clinicians prioritize early protein delivery for wound healing, immune defense, and growth. Carbohydrate dextrose solutions follow in volume but face intensified glucose-control protocols that moderate their expansion. Lipid emulsions are pivoting to mixed-oil blends that curb omega-6 overload and reduce cholestasis risk, satisfying pediatric guideline shifts away from pure soybean oil. Vitamins, trace elements, and electrolytes, though smaller in unit sales, remain indispensable for preventing deficiency-related complications during long-term therapy. Stability improvements, such as light-protective multilayer bags, now extend shelf life to seven days in automated pumps, cutting changeovers and nursing time. Collectively, these advances enlarge the parenteral nutrition market by enabling safer, more tailored prescriptions amid rising patient acuity.

By Patient Type: Neonatal Segment Accelerates Growth

Adults represented 64.25% of 2025 revenue, driven by oncology, gastrointestinal, and post-surgical requirements. The neonatal fraction, however, clocks the fastest 6.54% CAGR through 2031, buoyed by higher pre-term survival and proactive early-life nutrition standards. Triple-chamber neonatal bags meet 100% of the recommended amino acid intake while lowering pharmacist workload by 37%. Paediatric patients beyond infancy hold steady as congenital disorders stabilise, yet require ongoing nutritional oversight. Geriatric uptake is climbing in parallel with longer life expectancy and multimorbidity. By 2031, the parenteral nutrition market size for neonates is projected to approach USD 2.04 billion, underscoring their growing weight in overall demand.

By End-User: Homecare Transforms Delivery Models

Hospitals maintained 69.72% of 2025 billings because initiation, monitoring, and acute interventions still occur in inpatient settings. Nonetheless, homecare recorded the highest 7.98% CAGR forecast, reflecting payers’ push for lower-cost sites. Smart pumps with dose-error-reduction software allow safe bedside use and transmit logs for remote clinical review. Clinics serve stable oncology and inflammatory bowel cohorts that require periodic central line checks and micronutrient dosing adjustments. Ambulatory surgical centers increasingly deploy short-term parenteral nutrition protocols to optimize perioperative recovery, trimming length of stay. With Medicare’s 2022 reimbursement liberalization, the parenteral nutrition market size associated with home settings is expected to reach USD 2.46 billion by 2031, reshaping care delivery economics.

Geography Analysis

North America remains the leading contributor to the parenteral nutrition market, accounting for approximately 43.85% of global revenue in 2025. CMS’s decision to drop restrictive National Coverage Determinations expanded home therapy eligibility, leading to increased utilization in smaller community hospitals. Domestic amino acid plants funded by the HHS-Resilience partnership reduce reliance on overseas inputs and bolster supply security. Technology adoption is also rapid; Baxter’s Novum IQ platform downloads drug libraries over the air, aligning dose limits across multiple facilities in real time.

Europe is a mature yet innovative arena. ESPEN and ESPGHAN guidelines standardize practices for both pediatric and adult patients, promoting consistent nutrient delivery across member states. Six nations now codify home parenteral nutrition in legislation, with Denmark covering the majority of patient costs. Wage expenses account for 54% of total neonatal compounding costs, prompting hospitals to shift toward fixed multi-chamber bags to enhance efficiency. Increased scrutiny of soybean-only lipids drives demand for composite emulsions, advancing formulation science throughout the region.

Asia-Pacific stands out as the fastest-growing geography, anticipating a 6.84% CAGR between 2026 and 2031. Japan’s audit highlighted underdosing trends, indicating a need for guideline alignment and potential volume growth. Meanwhile, an ICU Medical-Otsuka joint venture will add 1.4 billion IV units annually, extending regional manufacturing and providing a buffer against future shortages. Reimbursement remains uneven: only 40% of surveyed countries subsidize home intravenous nutrition; however, the rising prevalence of chronic diseases is pressuring policymakers toward coverage expansion. These forces combine to elevate the parenteral nutrition market across urban and emerging provincial centers.

Competitive Landscape

The parenteral nutrition industry features moderate concentration. Fresenius Kabi, Baxter International, and B. Braun together own close to half of global sales, leveraging large portfolios, vertically integrated supply, and hospital contracts. Fresenius Kabi won a 2024 supply-chain excellence award for predictive analytics that lowered stockouts. Baxter distinguishes itself through connected infusion ecosystems - Novum IQ’s integrated syringe and large-volume pumps display identical user interfaces, reducing training time and error rates. B. Braun’s DUPLEX system combines antibiotic powder and diluent in separate chambers, cutting dose prep by four minutes and halving mishandling incidents.

Strategic consolidation is reshaping competitive dynamics. The USD 200 million ICU Medical–Otsuka alliance forms a global IV network with 1.4-billion-unit capacity, ensuring resilience against regional shocks. Mid-tier companies are investing in lipid innovation; mixed-oil emulsions integrate fish and olive oils to balance omega-6:omega-3 ratios. Digital health newcomers supply pumps with cellular modules that relay infusion parameters to cloud dashboards, enabling real-time adherence monitoring. Meanwhile, contract development and manufacturing organizations position themselves as on-demand partners capable of sterile fill-finish for hospitals and branded suppliers alike. These varied strategies intensify competition and foster steady product innovation, ensuring that the parenteral nutrition market remains dynamic through 2030.

________________________________________

Parenteral Nutrition Industry Leaders

Fresenius Kabi AG

B. Braun Melsungen AG

Baxter

ICU Medical

Option Care Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Baxter launched the Novum IQ infusion platform in the United States, featuring over-the-air drug library updates and dose-error-reduction software.

- April 2025: B. Braun gained FDA approval for Piperacillin–Tazobactam in the DUPLEX system, reducing dose preparation time by 54%.

- November 2024: ICU Medical and Otsuka Pharmaceutical Factory formed a USD 200 million joint venture to build a 1.4-billion-unit IV network.

- October 2024: Resilience secured USD 17.5 million HHS funding to expand domestic amino acid production for parenteral nutrition.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the parenteral nutrition market as all commercially manufactured, sterile nutrient formulations, amino acid, carbohydrate, lipid, electrolyte, vitamin, and trace-element solutions administered intravenously to patients who cannot meet caloric or micronutrient needs through the gut.

Scope exclusion: Devices such as infusion pumps, catheters, and enteral feeding products sit outside this measurement.

Segmentation Overview

- By Nutrition Type

- Carbohydrates

- Lipid Emulsions

- Amino Acid Solutions

- Vitamins

- Trace Elements

- Electrolytes

- Others

- By Patient Type

- Neonates (Pre-term & Term)

- Pediatrics (1-17 yrs)

- Adults (18-64 yrs)

- Geriatric (Above 65 yrs)

- By End-user

- Hospitals

- Clinics

- Homecare

- Ambulatory Surgical Centres

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed clinical nutritionists, NICU pharmacists, hospital procurement heads, and regional distributors across North America, Europe, Asia-Pacific, and Latin America. Discussions tested inpatient dwell days, average selling prices, supply bottlenecks, and adoption of three-in-one bags, enabling us to fine-tune assumptions pulled from desk research.

Desk Research

We started with pharmacovigilance alerts, FDA / EMA product registries, and import-export codes for HS 300432 and HS 300490, which map volumes of multi-chamber bags and single-entity vials. National hospital discharge datasets from sources such as the Healthcare Cost and Utilization Project, Eurostat, and Japan's MHLW clarified procedure counts that typically trigger parenteral nutrition. Trade statistics from UN Comtrade, annual reports, and clinical-trial repositories supplied additional price, demand, and pipeline signals. Subscription databases, notably D&B Hoovers and Dow Jones Factiva, helped us validate manufacturer revenue splits and shipment trends. The references listed illustrate, not exhaust, the secondary material reviewed.

Market-Sizing & Forecasting

A top-down reconstruction starts with national procedure volumes for conditions needing parenteral nutrition, pre-term births, short-bowel syndrome surgeries, and critical care sepsis cases, which are then multiplied by validated prevalence-to-treatment rates. Results are cross-checked with sampled bottom-up rolls of leading suppliers' PN revenues and typical ASP × bag volumes before final adjustment. Key model drivers include pre-term birth incidence, median PN therapy duration, lipid emulsion ASP movements, shift toward home PN, and macroeconomic health-spend ratios. Five-year forecasts employ multivariate regression blended with scenario analysis, using these variables plus currency outlooks vetted by our primary respondents. Data gaps, especially in cash-pay settings, are bridged with regional proxy ratios agreed during interviews.

Data Validation & Update Cycle

Outputs pass a two-step peer review, anomaly flags initiate re-runs, and any variance above three percent against new regulatory filings triggers a call-back to expert panels. Reports refresh each year, with interim amendments when material recalls or reimbursement shifts emerge, ensuring buyers receive the latest viewpoint.

Why Mordor's Parenteral Nutrition Baseline Commands Reliability

Published estimates vary because firms pick different nutrient mixes, price points, and update cadences.

Key gap drivers include some publishers folding in infusion pumps, others freezing exchange rates at proposal time, and a few applying uniform ASP growth without checking supply contracts that Mordor captures through ongoing hospital outreach.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.50 B (2025) | Mordor Intelligence | - |

| USD 7.52 B (2024) | Global Consultancy A | Excludes adult home-care volumes; single-year currency conversion |

| USD 7.09 B (2025) | Trade Journal B | Bundles peripheral nutrition and small-volume parenteral drugs |

| USD 7.67 B (2025) | Industry Association C | Uses blanket ASP escalation, no supplier revenue cross-check |

The comparison shows how differing scopes and unchecked assumptions can compress totals. By aligning clinical need, real purchase prices, and annual refreshes, Mordor delivers a balanced, transparent baseline that decision-makers can track and reproduce with confidence.

Key Questions Answered in the Report

What is the projected parenteral nutrition market size by 2031?

The parenteral nutrition market size is forecast to reach USD 11.94 billion by 2031.

Which product segment currently dominates revenue?

Amino acid solutions lead the market, holding 33.88% of 2025 revenue.

Why is Asia-Pacific the fastest-growing region?

Rising chronic disease burden, expanded critical-care capacity, and new regional manufacturing are propelling a 6.84% CAGR in Asia-Pacific.

How fast is the homecare channel expanding?

Homecare is expected to log an 7.98% CAGR to 2031 due to reimbursement reforms and portable smart pumps.

What clinical risk most constrains growth?

Catheter-associated bloodstream infection remains the primary safety concern, though antimicrobial lock therapy can markedly lower event rates.

Page last updated on: