Global Pediatric Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

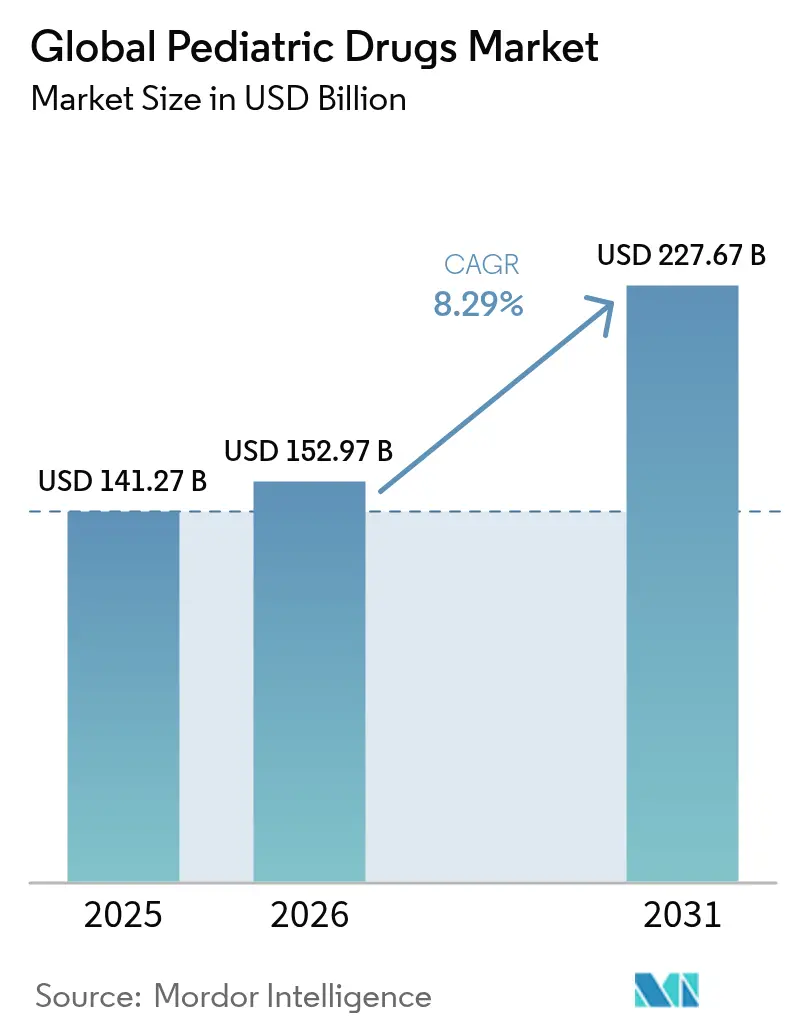

| Market Size (2026) | USD 152.97 Billion |

| Market Size (2031) | USD 227.67 Billion |

| Growth Rate (2026 - 2031) | 8.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Pediatric Drugs Market Analysis by Mordor Intelligence

The pediatric drugs market size was valued at USD 141.27 billion in 2025 and estimated to grow from USD 152.97 billion in 2026 to reach USD 227.67 billion by 2031, at a CAGR of 8.29% during the forecast period (2026-2031). Growth is underpinned by the rare pediatric disease priority review voucher program, rapid progress in nanotechnology-enabled formulations, and vaccination initiatives that close care gaps in emerging economies. Regulatory incentives have galvanized pharmaceutical investment in diseases once overlooked in childhood, while smart inhaler devices and digital adherence platforms enhance therapeutic outcomes and drive prescription volumes. Heightened awareness of chronic pediatric illnesses, coupled with real-world evidence programs that optimize age-appropriate dosing, further supports expansion of the pediatric drugs market.

Key Report Takeaways

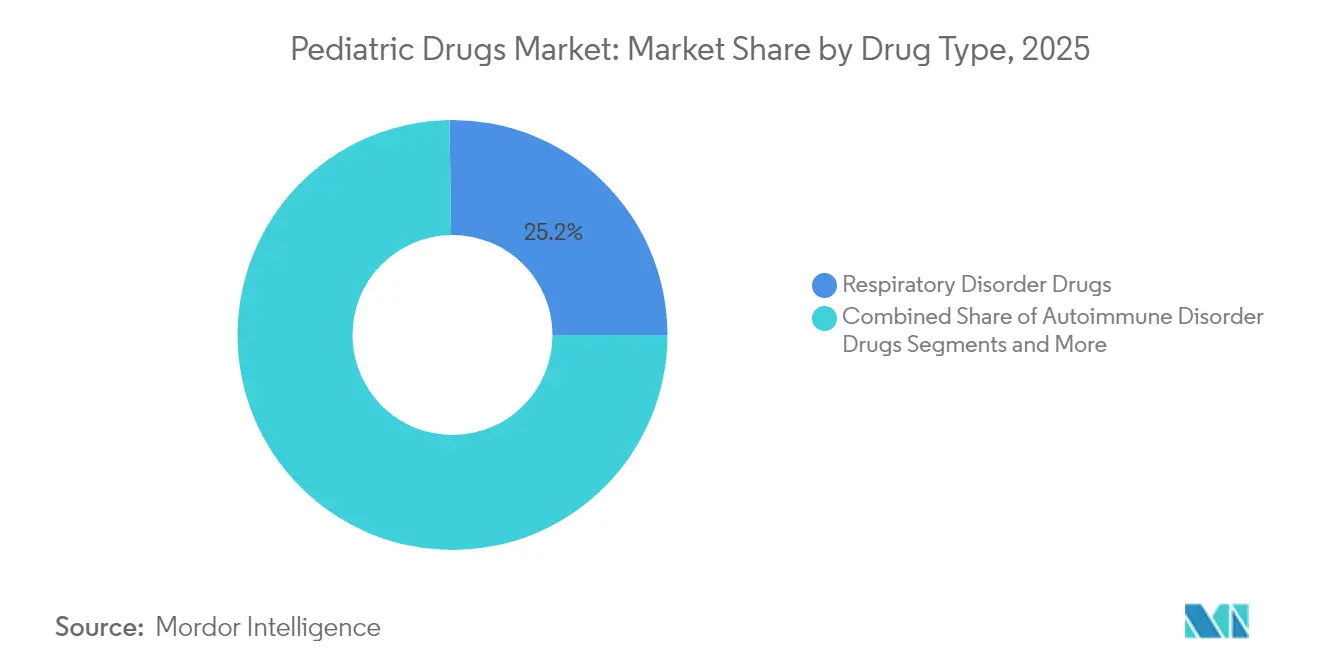

- By drug type, respiratory disorder therapies led with 25.22% revenue share of the pediatric drugs market in 2025; neurology and ADHD drugs are projected to advance at a 8.96% CAGR to 2031.

- By route of administration, oral formulations held 52.78% of the pediatric drugs market share in 2025, whereas inhalation delivery systems are forecast to expand at 9.15% CAGR through 2031.

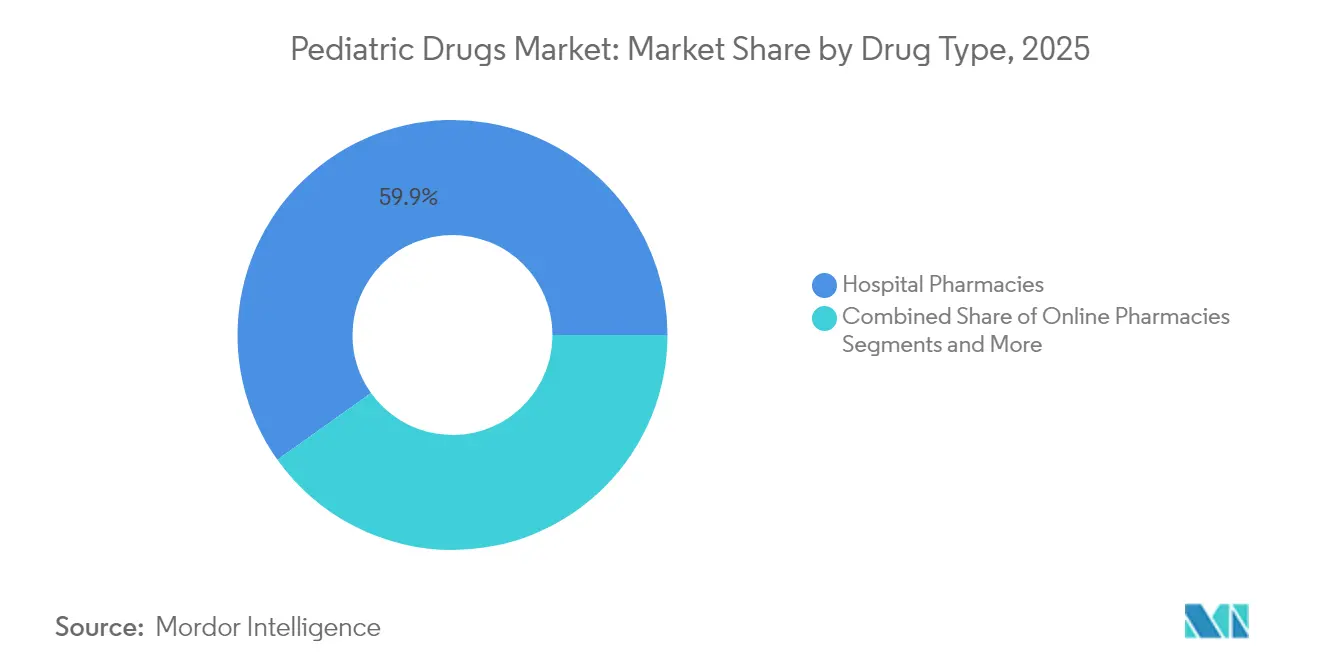

- By distribution channel, hospital pharmacies accounted for 59.85% share of the pediatric drugs market size in 2025, while online pharmacies post the highest projected CAGR at 10.05% to 2031.

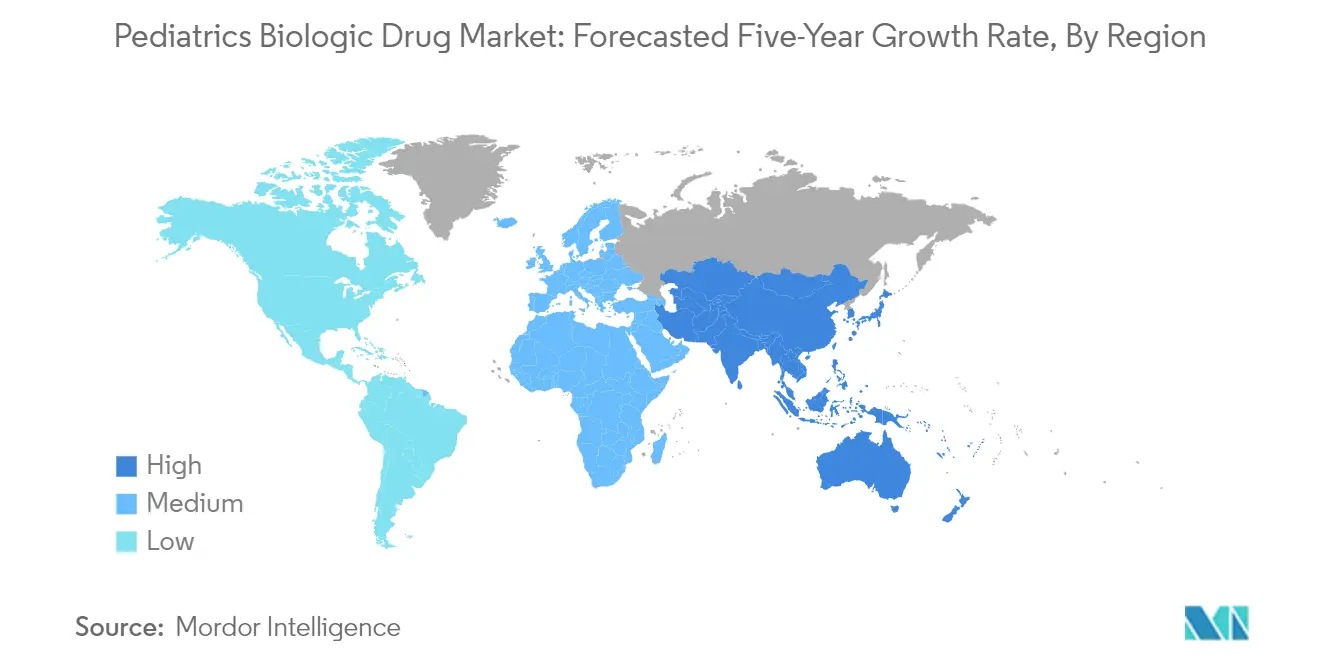

- By geography, North America retained 39.85% share of the pediatric drugs market in 2025; Asia-Pacific is expected to grow the fastest at a 10.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pediatric Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of chronic pediatric illnesses | +1.8% | Global, with concentration in developed markets | Long term (≥ 4 years) |

| Expanding R&D pipelines & pediatric-exclusive designations | +2.1% | North America & EU regulatory zones | Medium term (2-4 years) |

| Government incentives for orphan & pediatric drugs | +1.5% | Global, led by FDA/EMA frameworks | Medium term (2-4 years) |

| Expansion of pediatric vaccination schedules in emerging markets | +1.2% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Real-world evidence accelerating age-appropriate dosing | +0.9% | Global, early adoption in North America | Short term (≤ 2 years) |

| Digital adherence platforms boosting treatment outcomes | +0.8% | Global, with urban concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic Pediatric Illnesses

Childhood obesity affects 6 million U.S. children, and therapies such as liraglutide now target ages 6-12 [1]Michael Freedman, “Childhood Obesity and Liraglutide Outcomes,” New England Journal of Medicine, nejm.org. Rising prevalence of complex neurological disorders has led to approvals like KEBILIDI for aromatic L-amino acid decarboxylase deficiency [2]U.S. Federal Register, “Approval of KEBILIDI for Aromatic L-Amino Acid Decarboxylase Deficiency,” federalregister.gov. Pediatric oncology similarly shifts toward nanomedicine, where exosome-based carriers enhance drug targeting and reduce systemic toxicity. Longer treatment horizons magnify the need for safe, palatable formulations and reinforce demand in the pediatric drugs market.

Expanding R&D Pipelines & Pediatric-Exclusive Designations

The FDA issued 38 rare pediatric disease priority review vouchers through 2024, sparking 569 designations since 2013, most in neurology, metabolism, and oncology. Companies rushed applications before the program sunset in December 2024, increasing deal-making momentum exemplified by Merck KGaA’s USD 3.9 billion SpringWorks acquisition for the neurofibromatosis therapy GOMEKLI. Firms are now designing drugs specifically for pediatric physiology, illustrated by BioCryst’s planned NDA for ORLADEYO granules for children under 12. These moves strengthen innovation depth within the pediatric drugs market.

Government Incentives for Orphan & Pediatric Drugs

The FDA’s National Priority Voucher program accelerates review of drugs addressing pressing child health needs. In Europe the EMA granted advanced-therapy designations for LENMELDY, underscoring trans-Atlantic regulatory alignment on pediatric priorities. Multinational studies such as Global PARITY demonstrate commitment to evidence-based pediatric care even in low-income countries. Collectively, these frameworks reduce financial risk and elevate visibility of the pediatric drugs market.

Expansion of Pediatric Vaccination Schedules in Emerging Markets

India’s Intensified Mission Indradhanush aims for 90% immunization coverage, backed by USD 250 million from Gavi to cut zero-dose children by 30% before 2026. Nigeria’s conditional cash transfers doubled vaccination uptake in northern states. Latin America is modernizing with hexavalent combination schedules championed by PAHO even as historic DTP3 coverage dipped. Vaccine expansion broadens addressable populations for the pediatric drugs market.

Real-World Evidence Accelerating Age-Appropriate Dosing

Registry data from 13,553 children on growth-hormone therapy inform precise dosing adjustments that boost adherence. Apixaban cohorts in congenital heart disease provide reassurance for wider anticoagulant use. Such evidence expedites labeling updates and quickens product uptake across the pediatric drugs market.

Digital Adherence Platforms Boosting Treatment Outcomes

Smart inhalers track rescue usage and feed data to clinicians, cutting emergency visits in asthma programs piloted in the United States. European e-pharmacies integrate teleconsultation and e-prescription services that raise refill compliance in chronic therapies. Digital solutions create pull-through demand, supporting the growth trajectory of the pediatric drugs market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethical & recruitment hurdles in pediatric trials | -1.4% | Global, acute in developed markets | Medium term (2-4 years) |

| High palatability/formulation costs | -0.9% | Global, cost-sensitive in emerging markets | Short term (≤ 2 years) |

| Antibiotic-stewardship pressure on prescriptions | -0.7% | Global, led by European guidelines | Long term (≥ 4 years) |

| Supply-chain gaps for taste-masking excipients | -0.6% | Global, concentrated in specialized suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ethical & Recruitment Hurdles in Pediatric Trials

Only 10% of eligible children enroll in trials because parents weigh risks carefully and IRB processes vary across sites. Language-related consent barriers further lower participation among Black and Hispanic families [3]Rachel Ellis, “Language Barriers in Pediatric Research Participation,” JAMA Network Open, jamanetwork.com . Deferred consent models in neonatal studies aim to reconcile urgency with ethics. These hurdles slow evidence generation for the pediatric drugs market.

High Palatability / Formulation Costs

Taste-masking of bitter APIs such as acetaminophen requires labor-intensive sensory testing and specialized excipients that lift R&D spend by millions. Orally disintegrating tablets add manufacturing complexity, while stability studies lengthen timelines. The financial burden deters smaller firms from entering the pediatric drugs industry and restrains broader competition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Type: Respiratory Dominance Amid ADHD Acceleration

Respiratory treatments captured 25.22% of 2025 revenue in the pediatric drugs market as corticosteroid dependence and recent shortages sustained demand. The launch of albuterol / budesonide combination inhalers alleviates supply pressure and enhances dual-action therapy. Neurology and ADHD agents grow at 8.96% CAGR through 2031 as diagnostic clarity rises and non-stimulant options gain favor. Oncology pipelines integrate exosome-based nanocarriers that widen the therapeutic window for cytotoxics. Collectively, therapeutic diversification secures resilience in the pediatric drugs market.

The segment also includes autoimmune breakthrough therapies such as LENMELDY, which highlight curative potential in ultrarare leukodystrophies. Gastrointestinal drugs are affected by stewardship programs that keep empirical antibiotic usage in check, while cardiovascular agents benefit from emerging real-world safety data. Across categories, firms increasingly design pediatric‐specific formulations rather than scaling down adult products, ensuring compliance with taste, texture, and dose-flexibility requirements intrinsic to the pediatric drugs market.

By Route of Administration: Oral Leadership Challenged by Inhalation Innovation

Oral dosage forms controlled 52.78% of the pediatric drugs market share in 2025, buoyed by convenience, low cost, and broad age compatibility. Inhalation routes, however, are set to outpace with a 9.15% CAGR to 2031 as smart inhalers and nanogrid delivery platforms extend residence time in airways and lessen dosing frequency. Budesonide / formoterol inhalation powder attained a 93.75% clinical response in pediatric viral pneumonia, supporting rapid uptake.

Inhalation advances pressure innovators to refine particle engineering, digital sensors, and child-friendly actuation forces, enriching the competitive landscape of the pediatric drugs market. Topical nano-microneedles and facilitated self-assembly nanoparticles improve transdermal and parenteral efficiency yet remain niche. As gene therapies expand, intravenous delivery retains importance despite its logistic challenges in ambulatory care. This route heterogeneity positions the pediatric drugs market for continuous technological upgrades.

By Distribution Channel: Hospital Pharmacy Strength Versus Digital Disruption

Hospital pharmacies held 59.85% of the pediatric drugs market size in 2025, reflecting institutional stewardship over high-acuity treatments. Complex dosing needs in oncology, rare diseases, and neonatal care entrench hospital control of dispensing. Online platforms post a 10.05% CAGR to 2031, empowered by telehealth integration and rising caregiver preference for doorstep delivery. Quality variance in e-pharmacy applications, notably in India, prompts regulatory tightening that will shape competitive dynamics.

Retail pharmacies navigate a squeezed middle position, contending with hospital formularies for specialty medications and with digital convenience for chronic refills. Digital adherence portals that merge monitoring and clinical feedback loops are emerging differentiators, likely accelerating migration of maintenance-therapy volumes toward online channels. Collectively, distribution innovation diversifies access points and broadens patient reach within the pediatric drugs market.

Geography Analysis

North America commanded 39.85% of the pediatric drugs market in 2025 on the back of robust regulatory frameworks, insurance coverage for specialty formulations, and early technology adoption. The FDA granted multiple priority review vouchers in 2024 for products such as XOLREMDI and DUVYZAT, reinforcing the region’s attractiveness. Supply shocks like the withdrawal of established inhaled steroids highlighted vulnerability to single-product reliance, yet the maturity of telemedicine and home-based monitoring supports continuity of care and future expansion.

Asia-Pacific is forecast to grow at 10.32% CAGR to 2031, making it the fastest-expanding region in the pediatric drugs market. China registered 895 pediatric clinical trials between 2013-2022 and now emphasizes innovative over generic pipelines. India’s USD 250 million Gavi partnership targets a 30% reduction in zero-dose children, while successful nationwide pneumococcal vaccine implementation underscores capability to scale. Japan advances gene therapy approvals such as OTL-200, signaling regional strength in precision medicine.

Europe sustains moderate growth despite chronic shortages that affected 779 pediatric medicines from 2001-2015. The EMA facilitates centralized pediatric oversight, yet logistical complexities post-Brexit necessitate new supply configurations. Germany adopted RSV prophylaxis for infants, evidencing evidence-driven uptake of novel biologics. In the Middle East and Africa, conditional cash transfers doubled immunization rates in Nigerian pilot areas, and similar programs could uplift coverage across the continent. South America faces headwinds as DTP3 rates dropped to 75% in 2021, but combination-vaccine reforms in Colombia and Peru offer templates for recovery. These divergent trajectories create geographically diverse opportunities within the pediatric drugs market.

Competitive Landscape

The pediatric drugs market shows moderate fragmentation. Large pharmaceutical firms such as Pfizer, Sanofi, and GSK leverage regulatory familiarity and scale to navigate complex pediatric requirements. Biotechnology entrants focus on niche indications; BioCryst’s ORLADEYO recorded USD 437 million in 2024 revenue and is expanding to younger cohorts. Deal activity remains brisk; Merck KGaA’s USD 3.9 billion purchase of SpringWorks secured GOMEKLI, an FDA-approved neurofibromatosis therapy with strong pediatric positioning.

Technology stands out as a differentiator. Nanotechnology platforms enhance drug solubility and targeting, while patent filings around albuterol formulations illustrate a shift toward digital monitoring embedded in delivery devices. Artificial intelligence tools that adjust dosing in real time are in development, though wide clinical adoption is pending.

White-space opportunities persist in neonatal care and mental health, segments historically underfunded yet now drawing attention under revised regulatory incentives. Competitive intensity is poised to rise as the sunset of the priority review voucher program reduces future windfalls, pushing firms to sharpen focus on formulation science, supply resilience, and value-based care collaborations inside the pediatric drugs market.

Global Pediatric Drugs Industry Leaders

BioMarin Pharmaceutical Inc

Horizon Therapeutics plc

Sumitomo Dainippon Pharma Co Ltd

Jazz Pharmaceuticals Inc

Gilead Sciences Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MaaT Pharma won a positive EMA Pediatric Committee opinion approving the Pediatric Investigation Plan for MaaT013 for acute graft-versus-host disease.

- October 2024: The FDA extended methotrexate (Jylamvo) approval to pediatric acute lymphoblastic leukemia and polyarticular juvenile idiopathic arthritis.

- October 2024: Barcelona scientists introduced WNTinib, a candidate aimed at slowing hepatoblastoma progression in young children, with clinical trials planned.

- August 2024: Florida State University researchers enhanced natural killer cells derived from induced pluripotent stem cells to target rare pediatric brain cancers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the pediatric drugs market as all prescription and over-the-counter medicines that are formulated, labeled, and dosed specifically for patients from birth to 18 years, spanning small-molecule drugs, biologics, and age-appropriate delivery formats such as liquids, melts, and mini-caps.

Scope exclusion: pediatric vaccines and clinical-trial service revenues sit outside this valuation, as they are sized in separate Mordor titles.

Segmentation Overview

- By Drug Type

- Respiratory Disorder Drugs

- Autoimmune Disorder Drugs

- Gastrointestinal Drugs

- Cardiovascular Drugs

- Neurology & ADHD Drugs

- Oncology Drugs

- Other Drug Types

- By Route of Administration

- Oral

- Topical

- Parenteral

- Inhalation

- Other Routes

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drug Stores

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview pediatricians, hospital pharmacists, procurement heads, and drug-safety regulators across North America, Europe, Asia-Pacific, and Latin America. These discussions clarify real-world dosing practice, off-label spillovers, typical wholesale mark-ups, and likely adoption curves for orally disintegrating tablets versus inhaled formats.

Desk Research

We begin with harmonized definitions from open regulators like the FDA, EMA, and WHO, add epidemiological series from UNICEF and the Global Burden of Disease project, and map trade volumes drawn from UN Comtrade. Cost inputs come from national health-spending dashboards, while pricing corridors are sampled from government reimbursement lists and tender portals. Paid vaults, D&B Hoovers for company splits and Questel for formulation patents, supply additional signals. A wider set of annual reports, investor decks, and hospital formularies helps us trace formulation launches and channel shifts. The sources named illustrate our approach; many others were consulted for cross-checks.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-patient model converts disease incidence data into therapy volumes; average strength per regimen and median annual price points yield value demand. Supplier roll-ups of leading branded and generic portfolios act as a selective bottom-up lens that flags over- or under-count. Key variables include live-birth cohorts, chronic-disease prevalence (asthma, ADHD), generic erosion rates, regulatory exclusivity expiries, median wholesale acquisition cost, and pediatric formulary additions. Forecasts rely on multivariate regression blended with scenario analysis, where price erosion, reimbursement shifts, and pipeline approvals form the core drivers. Gaps in bottom-up inputs are bridged through regional channel checks and ASP proxies.

Data Validation & Update Cycle

Outputs pass variance screens against historic spend, UNICEF procurement values, and customs flows; anomalies trigger secondary reviews before senior sign-off. Reports refresh annually, and interim reruns occur when major label approvals, safety withdrawals, or reimbursement reforms materially move the baseline.

Why Our Pediatric Drugs Baseline Stands Out for Decisions

Published estimates often diverge because firms pick different age bands, bundle vaccines variably, or refresh on unequal cadences.

Key gap drivers include scope creep into immunization sales, aggressive ASP uplift assumptions, and limited triangulation with real procurement data before currency conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 141.27 B | Mordor Intelligence | - |

| USD 163.28 B | Global Consultancy A | Includes vaccines and applies uniform 4% annual price rise |

| USD 166.28 B | Industry Association B | Uses hospital purchase data only, excludes retail and online channels |

| USD 179.43 B | Regional Consultancy C | Converts local currencies at fixed 2023 rates, no generic erosion factor |

In sum, by anchoring valuations on treated-patient math, regularly refreshed price corridors, and verified channel splits, Mordor delivers a balanced, transparent baseline that decision-makers can retrace and replicate with confidence.

Key Questions Answered in the Report

How big is the Global Pediatric Drugs Market?

The Global Pediatric Drugs Market size is expected to reach USD 152.97 billion in 2026 and grow at a CAGR of 8.29% to reach USD 227.67 billion by 2031.

Which therapeutic segments present the strongest opportunities through 2031?

Respiratory drugs hold the largest 2025 share at 25.22%, while neurology and ADHD therapies are projected to rise the fastest at a 8.96% CAGR.

Who are the key players in Global Pediatric Drugs Market?

BioMarin Pharmaceutical Inc, Horizon Therapeutics plc, Sumitomo Dainippon Pharma Co Ltd, Jazz Pharmaceuticals Inc and Gilead Sciences Inc are the major companies operating in the Global Pediatric Drugs Market.

Which is the fastest growing region in Global Pediatric Drugs Market?

Asia-Pacific leads with a 10.32% CAGR forecast to 2031, driven by rapid clinical-trial expansion in China and aggressive vaccination programs in India.

Which region has the biggest share in Global Pediatric Drugs Market?

In 2025, the North America accounts for the largest market share in Global Pediatric Drugs Market.

Page last updated on: