Lamination Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

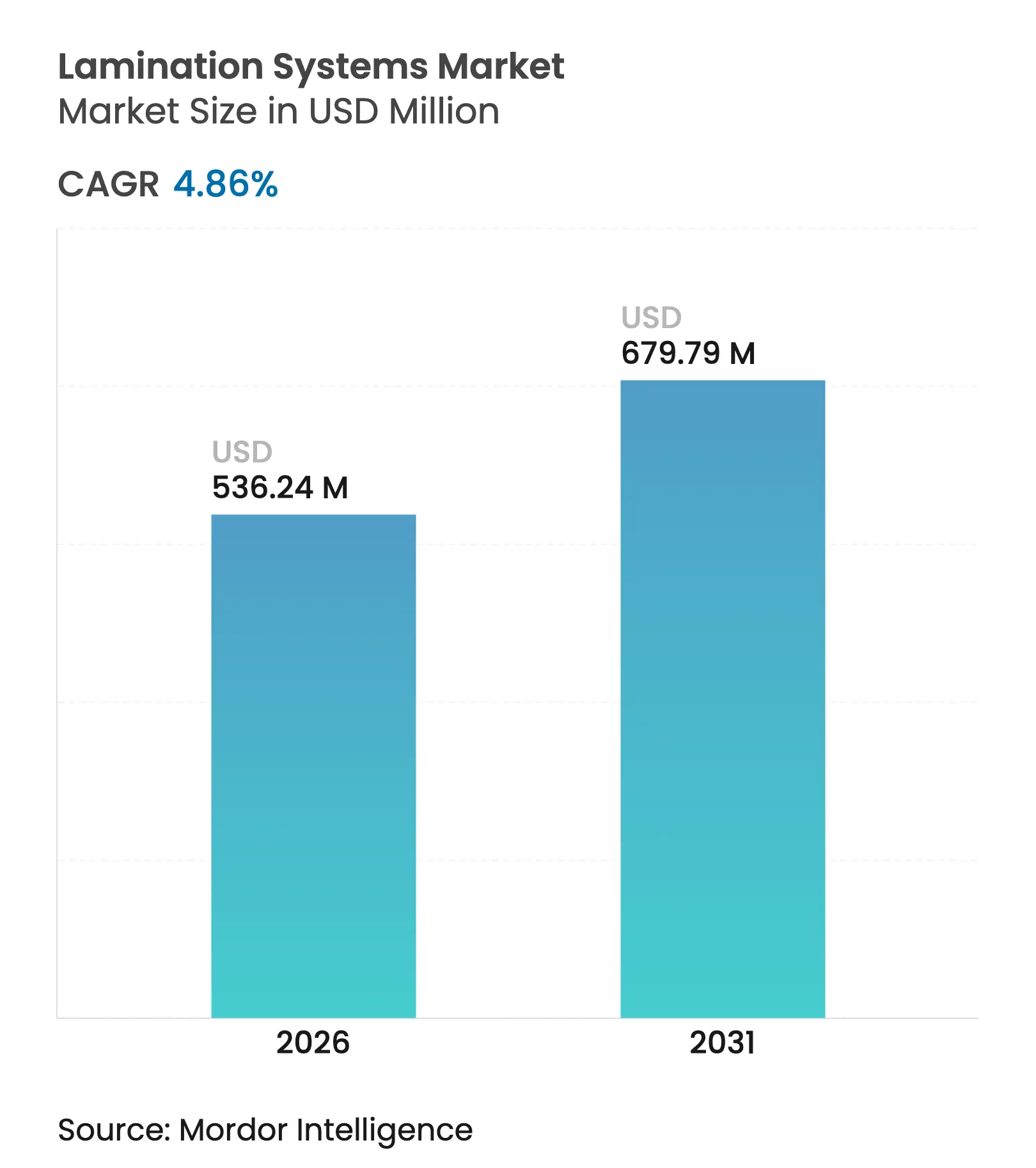

| Market Size (2026) | USD 536.24 Million |

| Market Size (2031) | USD 679.79 Million |

| Growth Rate (2026 - 2031) | 4.86 % CAGR |

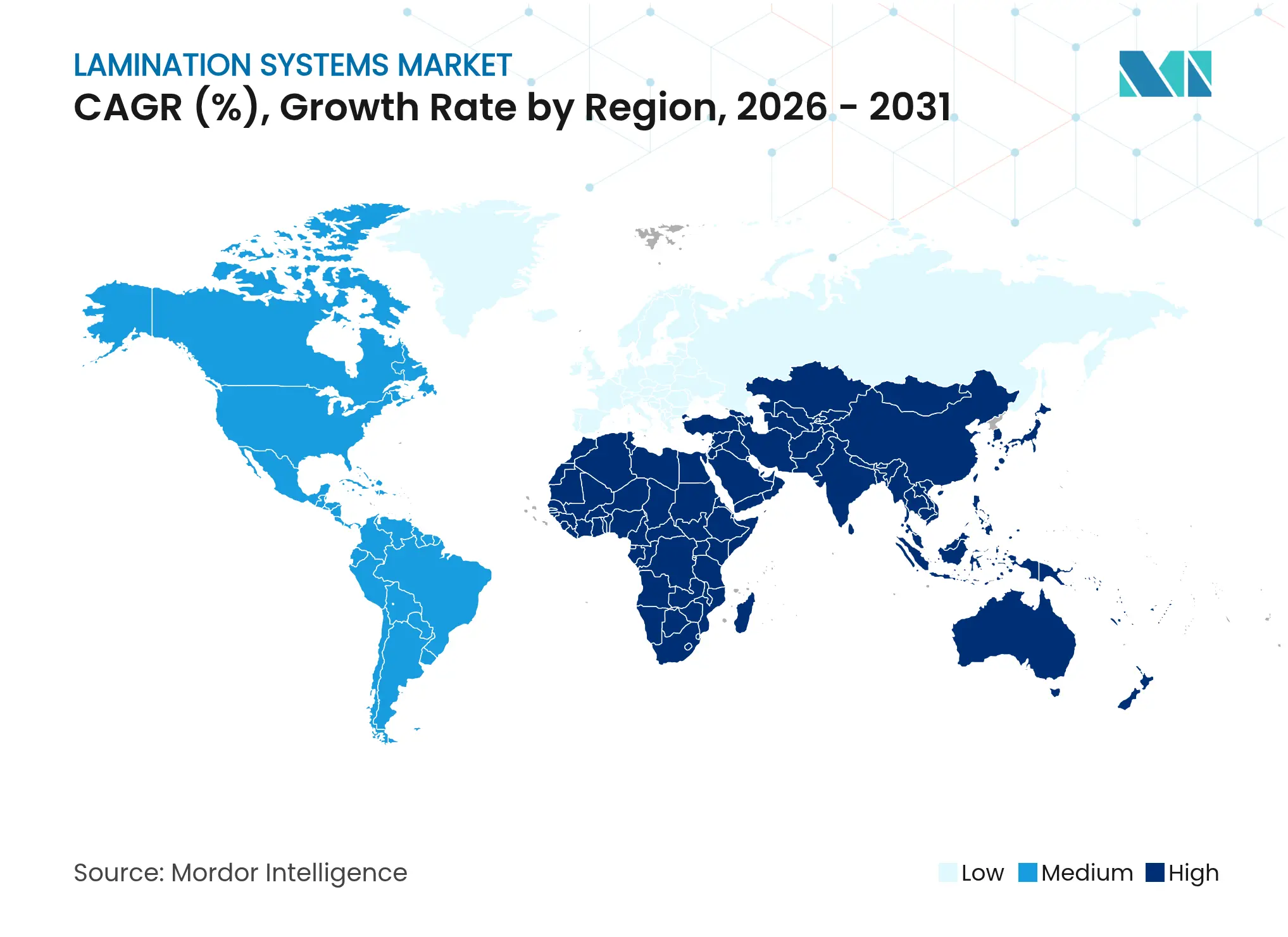

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Lamination Systems Market Analysis by Mordor Intelligence

lamination systems market size in 2026 is estimated at USD 536.24 million, growing from 2025 value of USD 511.41 million with 2031 projections showing USD 679.79 million, growing at 4.86% CAGR over 2026-2031. Current growth stems from surging demand for flexible e-commerce packaging, rapid adoption of solvent-free technologies to meet tightening VOC caps, and the need for precision motor laminates in electric vehicles. End users continue to replace legacy solvent lines with water-based or hybrid platforms that cut emissions and shorten compliance audits. Concurrently, manufacturers in China, India and Vietnam are scaling capacity, prompting equipment makers to localize service hubs and spare-parts inventories. Material cost volatility for aluminum foil, PET film and specialty adhesives has heightened interest in predictive analytics that optimize run-time economics, making new installations more of a strategic asset than a commodity purchase.

Key Report Takeaways

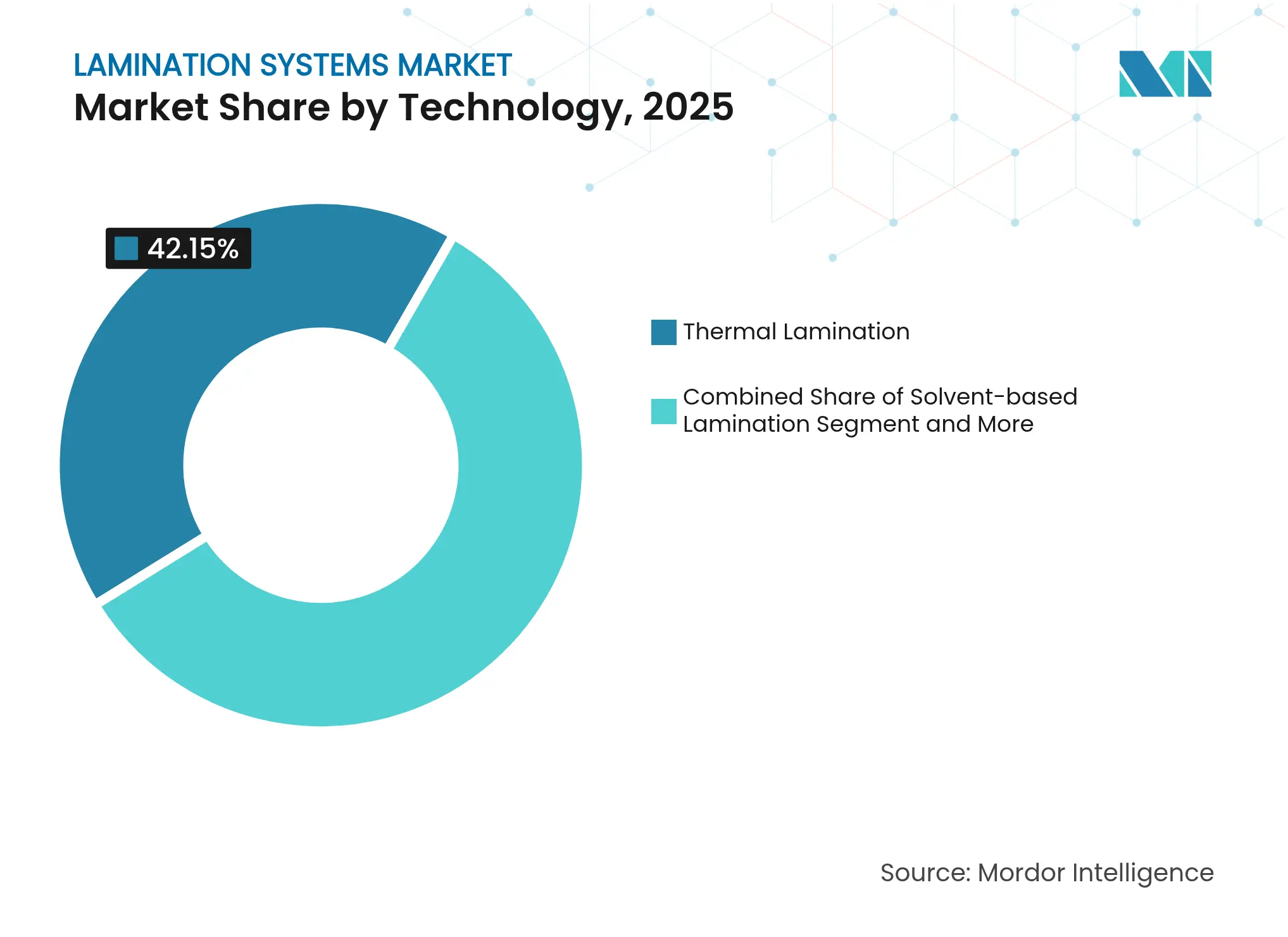

- By technology, thermal lamination led with 42.15% revenue share in 2025, while water-based units are projected to expand at a 4.91% CAGR through 2031.

- By material, film applications accounted for 47.70% of the lamination systems market share in 2025; bio-based substrates are forecast to post the fastest 4.96% CAGR to 2031.

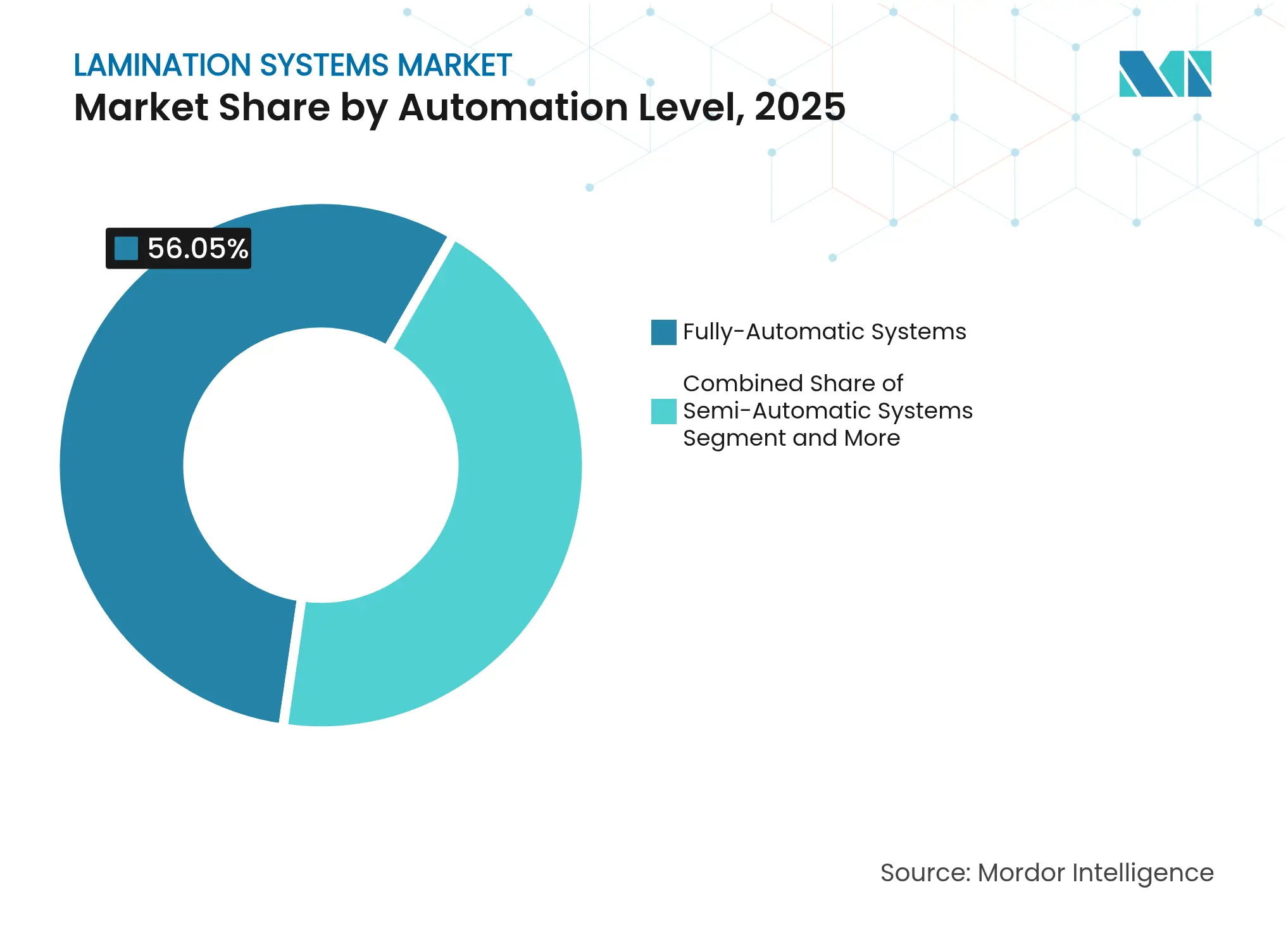

- By automation level, fully-automatic systems captured 56.05% of the lamination systems market size in 2025 and will grow at a 4.88% CAGR through the outlook period.

- By end-use industry, packaging held 37.15% share in 2025, whereas medical and healthcare applications are set to grow at a 4.87% CAGR to 2031.

- By geography, Asia-Pacific dominated with a 41.10% revenue share in 2025, yet the Middle East is poised for the highest 5.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lamination Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Sustainability-driven shift to solvent-free and water-based lamination Sustainability-driven shift to solvent-free and water-based lamination | +0.8% | EU & North America core, global spill-over | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:EU & North America core, global spill-over | Impact Timeline:Medium term (2-4 years) |

Surge in flexible packaging for e-commerce fulfilment Surge in flexible packaging for e-commerce fulfilment | +0.9% | APAC & North America | Short term (≤ 2 years) | |||

Electrification of vehicles boosting high-precision motor lamination lines Electrification of vehicles boosting high-precision motor lamination lines | +0.6% | China & Europe | Long term (≥ 4 years) | |||

Rapid expansion of APAC converting capacity Rapid expansion of APAC converting capacity | +0.7% | APAC core, MEA spill-over | Medium term (2-4 years) | |||

Adoption of Industry 4.0 for predictive maintenance Adoption of Industry 4.0 for predictive maintenance | +0.5% | North America & EU | Long term (≥ 4 years) | |||

Government bans on single-use plastics Government bans on single-use plastics | +0.4% | EU & North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Sustainability-driven shift to solvent-free and water-based lamination

Manufacturers are accelerating investment in water-borne and solvent-free adhesive units to satisfy EU and California VOC limits that took effect in 2024. Early adopters demonstrate 25% faster regulatory approvals and 15% lower hazardous-waste disposal fees, making the total cost of ownership lower than comparable solvent platforms. Key suppliers have teamed with adhesive formulators to guarantee bond strength and migration compliance, especially for food and pharma packs. Orders increasingly specify modular dryers and in-line viscosity sensors that maintain coat-weight uniformity without operator intervention. The switch is also unlocking marketing advantages as brand owners publicize reductions in carbon and solvent footprints to meet Scope 3 targets.

Surge in flexible packaging for e-commerce fulfilment

One-piece mailers, inflatable pouches and multi-layer barrier films now dominate shipment formats, forcing converters to handle thicker laminates and rapid roll changes. High-barrier structures that once posted 125 meters of start-up scrap have reached best-practice levels below 5 meters once automatic splice synchronizers and tension-feedback loops are installed. Demand has lifted utilisation rates at North American plants past 85%, prompting line extensions in Texas, Ontario and Nuevo León. Order books show a 30% jump in requests for 1 600 mm web widths to run parcel films and thermal labels side-by-side. Equipment vendors that bundle web inspection cameras with cloud dashboards report 10% sales premiums over hardware-only models, reflecting the shift toward performance contracting. [1]Rogers Corporation, “ROLINX Busbars,” rogerscorp.com

Electrification of vehicles boosting high-precision motor lamination lines

Electric-motor cores require stacking tolerances below 15 µm, driving demand for servo-driven feeders, punch-press integration and automated stacking modules. In 2024, European tier-one suppliers invested in multi-station lamination centres that weld, anneal and test stator stacks in-line, slashing cycle times by 40%. Chinese battery makers have specified dual-lane adhesive coaters that process dielectric films at 120 m/min while maintaining temperature variance under 2 °C. Copper-and-aluminum busbar laminates used in power inverters need die-cut registration within 50 µm; laser-guided edge tracking is therefore now standard. Global volume of dedicated motor lamination equipment rose 18% year-on-year in 2025, signalling a structural, not cyclical, shift.

Rapid expansion of APAC converting capacity

Vietnam, Indonesia and India commissioned more than 70 new laminators in 2024-2025 as branded consumer goods shift production closer to demand centres. Greenfield projects often bundle solvent-less, solvent-based and water-based heads on a common frame, allowing quick changeovers as raw-material availability fluctuates. Regional governments offer import-duty rebates on machinery that meets energy-efficiency thresholds, compressing payback periods to under four years for fully-automatic lines. European OEMs have responded with joint-venture service depots, while local challengers compete on price but lag in after-sales uptime. As a result, capacity utilisation in SE-Asia is forecast to rise steadily rather than overshoot, supporting stable demand for spare parts and retrofits. [2]MDPI Editorial Office, “Predictive Maintenance for Cutter System of Roller Laminator,” mdpi.com

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capex and skilled-operator scarcity for multi-layer laminators High capex and skilled-operator scarcity for multi-layer laminators | -0.6% | Global, acute in emerging markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.6% | Geographic Relevance:Global, acute in emerging markets | Impact Timeline:Medium term (2-4 years) |

Volatile prices of aluminum, PET and specialty adhesives Volatile prices of aluminum, PET and specialty adhesives | -0.8% | Global, APAC core most affected | Short term (≤ 2 years) | |||

Regulatory hurdles on VOC emissions in legacy solvent lines Regulatory hurdles on VOC emissions in legacy solvent lines | -0.4% | North America & EU | Short term (≤ 2 years) | |||

Fragmented after-sales service in emerging markets Fragmented after-sales service in emerging markets | -0.3% | APAC & MEA | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

High capex and skilled-operator scarcity for multi-layer laminators

Typical turnkey lines exceed USD 3 million, a hurdle for converters in the Middle East and Latin America that must finance equipment in hard currency. Even after installation, plants face a shortage of technicians proficient in servo tuning, adhesive rheology and sensor calibration. Firms have responded by sponsoring dual-certification programs with polytechnic institutes, yet 2025 graduate output still covers only 60% of openings. OEMs now embed augmented-reality work-instructions that cut mean-time-to-repair by 30%, but connectivity issues in remote zones dilute effectiveness. In sum, capital intensity and talent gaps delay project roll-outs and temper the otherwise strong growth path of the lamination systems market. [3]BOBST Group, “Laminating Machines,” bobst.com

Volatile prices of aluminum, PET and specialty adhesives

Spot PET film prices spiked 11% between April and June 2024 after unplanned cracker outages, inflating substrate costs by USD 200 per ton. Aluminum foil quotations swung more than 20% during the same quarter on energy-price uncertainty, upsetting bill-of-materials assumptions baked into customer contracts. Specialty adhesive makers passed on higher brominated resin costs, raising lamination unit-costs by 9 cents/m² and compressing converter margins. Such volatility forces buyers to hedge through long-term supply pacts, yet doing so elevates working-capital needs and extends payback horizons on new machines. Consequently, several planned expansions in Southeast Asia were postponed to 2026, trimming near-term demand for high-end laminators.

Segment Analysis

By Technology: Hybrid Platforms Gain Ground

Thermal units retained the largest 42.15% share of the lamination systems market in 2025, largely because mature converters value proven bonding consistency and high throughput. Water-based platforms, though, deliver the fastest 4.91% CAGR as food and pharmaceutical brands mandate low-migration structures. Solvent-less lines attract fresh orders in snack-food packaging thanks to odor neutrality, while pressure-sensitive cold lamination finds traction in wide-format graphics. Across all platforms, OEMs market hybrid frames that accommodate two or more adhesive types without offline changeovers. Such flexibility allows converters to match adhesive choice with fluctuating resin prices, a hedge against cost swings that plague single-technology plants. Digital twin simulations further shorten commissioning time by 15%, helping new lines reach stable yield sooner. As the competitive bar rises, vendors increasingly bundle analytics licenses with capital equipment, transforming the lamination systems market into a life-cycle-service play.

The transition also shifts component demand: modular induction dryers replace long hot-air tunnels to handle lower-solid water-borne coatings, and servo-driven nip stations replace pneumatics for micro-gap control. EU buyers now specify on-board VOC sensors even for water-borne lines to document near-zero emissions during audits. Meanwhile, electronics makers in Japan favor electron-beam systems for ultra-thin copper laminates, albeit from a small base. Collectively, these developments diversify revenue streams and buffet the lamination systems market against single-segment downturns.

Note: Segment shares of all individual segments available upon report purchase

By Material: Bio-Based Films Break Out

Film substrates commanded 47.70% of the lamination systems market size in 2025, underpinned by PET, BOPP and nylon’s dominance in food and consumer electronics. Bio-based substrates, however, deliver the quickest 4.96% CAGR, catalysed by compostability mandates in France, California and South Korea. Converters deploying PLA-based laminates report demand premiums of 12% from conscious brands, offsetting higher resin cost per kilogram. Paper-foil combinations regain popularity for specialty coffee pouch applications, leveraging printability and recyclability claims, while metal foil laminations grow alongside automotive EMI-shielding demand. The proliferation of material types obliges equipment builders to engineer rapid-temperature-ramp dryers and precise web-tension logic to avoid wrinkling or heat-set distortion. These advances reinforce supplier differentiation, ensuring sustained capital budgets even when commodity film volumes plateau.

Heightened substrate diversity requires inline optical gauges and near-infrared sensors to verify bond integrity in real time, slashing destructive testing frequency. OEMs marketing such self-learning quality control modules enjoy shorter sales cycles, especially where production networks span multiple plants. Consequently, material-led complexity fortifies aftermarket revenue pools as converters contract for sensor calibration, software updates and operator retraining, supporting the long-run expansion of the lamination systems market.

By Automation Level: Digital Intelligence Leads Investment

Fully-automatic lines seized 56.05% share in 2025 and are on track for a 4.88% CAGR as manufacturers prioritize throughput, waste reduction and labour savings. Standard features now include closed-loop viscosity control, automatic reel splice and AI-based defect detection, cutting waste by up to 35 kg per roll change. Semi-automatic equipment stays relevant among mid-scale Asian printers that juggle diverse run lengths yet lack capital depth; they often retrofit ultrasound tension sensors incrementally. Manual or offline coat-laminate systems survive in décor paper and short-run specialty labels where changeovers trounce speed. Rising energy tariffs spur installs of regenerative braking on nip motors, reclaiming up to 8% of power draw in continuous operation. As cloud platforms expand, even entry-tier machines ship with OPC-UA gateways, enabling future analytics subscriptions and embedding customers deeper into OEM ecosystems. These trends consolidate the lamination systems market around solution-providers that marry mechatronics, software and process chemistry.

Second-generation predictive-maintenance algorithms, trained on vibration and temperature data from 500-plus installed bases, now flag bearing faults up to 72 hours before failure and verify recommendations via AR headsets. Plants adopting such suites recorded 6.5 percentage-point gains in overall equipment effectiveness in 2025. The economic logic is decisive: downtime avoidance outweighs subscription fees, ensuring continued migration from semi-automatic to full automation across regions.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: Healthcare Uptick Redraws Mix

Packaging applications retained the highest 37.15% stake in 2025, propelled by online retail, quick-service food and high-barrier snack formats. Medical and healthcare use cases, however, register a 4.87% CAGR thanks to blister innovations and hospital sterility standards that demand class 100 clean-room compatibility. Pharmaceutical line validations now include cyclic-disinfection testing, steering OEMs to adopt stainless frames and encapsulated drives. Automotive buyers accelerate orders for battery module laminates that combine flame-retardant films with copper or aluminum, bolstered by e-mobility incentives in the EU and China. Electronics laminates ride 5G handset cycles, requiring low-dielectric films bonded at tighter tolerances. Meanwhile, décor laminates in flooring and furniture benefit from renovation upswing in mature markets. The resulting end-user spread shields the lamination systems market from sector-specific downturns and complicates supplier go-to-market strategies.

As converters diversify, they seek machines qualified under multiple GMP regimes—ISO 15378 for pharma, IATF 16949 for automotive and thus favour OEMs with cross-sector references. This elevates the total addressable service revenue, as every audit or re-qualification triggers calibration, documentation and software-update fees that only the original supplier can efficiently provide.

Geography Analysis

Asia-Pacific generated the largest share of lamination systems market revenues at 41.10% in 2025, buoyed by aggressive greenfield builds in China, India and Vietnam. Regional converters enjoy cost advantages in labour, land and cluster synergies, enabling capacity additions that outpace global averages. Local governments subsidize high-efficiency machinery that cuts energy intensity below 0.45 kWh/kg of product, sustaining capital orders despite tighter financing conditions. The lamination systems market size for China alone is forecast to top USD 223.6 million by 2031, with fully-automatic lines making up two-thirds of spend.

North America posts steady growth anchored by e-commerce fulfilment centres that need barrier mailer films and by auto electrification programs led by Michigan and Ontario battery corridors. Retrofit packages that integrate predictive analytics sell briskly as brown-field plants modernize without full line replacements. Europe, meanwhile, channels demand toward solvent-free and water-based systems, stimulated by the EU Packaging and Packaging Waste Regulation effective July 2024. OEM figures indicate that 80% of 2025 European orders specify on-board VOC reporting modules, a compliance-driven upsell.

The Middle East, though smaller today, advances at a 5.02% CAGR on the back of packaging localisation in Saudi Arabia and the United Arab Emirates. Major tissue and board makers place cluster orders to leapfrog to Industry 4.0 capabilities, creating service-intensive opportunities for global OEMs. Africa and South America contribute niche gains: Brazil’s agricultural export boom spurs pouch laminate demand, while South Africa aligns beverage can lines with foil-seal laminators. Collectively, these regional patterns diversify revenue streams and mitigate macro-economic shocks, reinforcing the multi-contingent expansion path of the lamination systems market.

Competitive Landscape

Market Concentration

The lamination systems market exhibits moderate consolidation: top five suppliers command roughly 60% of revenue, yet numerous regional builders satisfy entry-level projects. Nordmeccanica dominates converting machinery niches with a 70% slice of specialised coaters and vacuum metallizers, shipping more than 300 units yearly. BOBST maintained momentum in 2025, expanding its Florence competence centre to provide live demos and joint-process trials that accelerate customer decision cycles. Both groups emphasise integrated solutions bundling software, adhesives know-how and long-term service contracts, protecting margins against pure-hardware price erosion.

Challengers centre on digital intelligence. Several European robotics specialists license multi-arm stacking modules that retrofit onto legacy lines, raising throughput by 25% without floor-space expansion. Asian entrants underbid on base frames yet stumble on after-sales uptime, a gap incumbents exploit by offering guaranteed response times backed by IoT diagnostics. Patent filings in 2024-2025 reveal a shift toward AI-driven bond-strength prediction, with at least six OEMs referencing convolutional-neural inspection routines in published claims.

Customer procurement criteria have therefore broadened. Beyond web width and speed, buyers now score vendors on software roadmap, parts localisation and energy-consumption metrics. OEMs respond with subscription models that convert capital outlay into service revenue, a trend exemplified by multi-year performance-based agreements signed in 2025 between leading suppliers and global snack-food groups. The strategic pivot from machine sales to life-cycle partnerships recalibrates competitive moats and cements the lamination systems market as a technology-enabled service arena.

Lamination Systems Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hotpack invested USD 100 million in a New Jersey food-packaging plant, targeting 200 new jobs and sustainable product lines.

- March 2025: Timberlab commenced construction of a USD 117 million cross-laminated timber facility in Millersburg, Oregon, slated to create 100 jobs at USD 80 000 average wages.

- February 2025: Chemplast Sanmar budgeted INR 160 crore (USD 19.2 million) to enlarge its specialty-chemical capacity in Tamil Nadu.

- January 2025: BOBST opened a 1 200 m² competence centre in Florence, Italy, featuring six lines and showcasing the MASTER M6 flexo and DIGITAL MASTER 340 presses.

- November 2024: Polyplex launched a USD 100 million PET film expansion in Alabama, boosting North American substrate supply from Q1 2025.

- October 2024: Laminations relocated to a larger Oregon plant, increasing Northwest capacity for protective packaging

- September 2024: SRF Limited ordered a third BOBST EXPERT K5 high-barrier metallizer for its Thai facility, leveraging AluBond and AlOx GEN II processes.

- August 2024: Mill Rock Packaging acquired the Woodland Packaging and Laminating assets in California, adding large-format die-cutting and Masterflute capability.

Table of Contents for Lamination Systems Industry Report

1. INTRODUCTION

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Sustainability-driven shift to solvent-free and water-based lamination

- 4.2.2Surge in flexible packaging for e-commerce fulfilment

- 4.2.3Electrification of vehicles boosting high-precision motor lamination lines

- 4.2.4Rapid expansion of APAC converting capacity (China-India-Vietnam investment wave)

- 4.2.5Adoption of Industry 4.0 for predictive maintenance and waste reduction

- 4.2.6Government bans on single-use plastics accelerating barrier-film lamination demand

- 4.3Market Restraints

- 4.3.1High capex and skilled-operator scarcity for multi-layer laminators

- 4.3.2Volatile prices of aluminium, PET and speciality adhesives

- 4.3.3Regulatory hurdles on VOC emissions in legacy solvent lines

- 4.3.4Fragmented after-sales service in emerging markets

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

- 4.8Pricing Analysis

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Technology

- 5.1.1Thermal Lamination

- 5.1.2Solvent-based Lamination

- 5.1.3Solvent-less Lamination

- 5.1.4Water-based Lamination

- 5.1.5Pressure-Sensitive / Cold Lamination

- 5.1.6Other Technologies

- 5.2By Material

- 5.2.1Film Lamination

- 5.2.2Paper Lamination

- 5.2.3Foam Lamination

- 5.2.4Metal Lamination

- 5.2.5Bio-based and Compostable Substrates

- 5.3By Automation Level

- 5.3.1Fully-Automatic Systems

- 5.3.2Semi-Automatic Systems

- 5.3.3Manual/Offline Systems

- 5.4By End-use Industry

- 5.4.1Packaging

- 5.4.2Automotive

- 5.4.3Electronics and Electrical

- 5.4.4Textiles and Decor

- 5.4.5Medical and Healthcare

- 5.4.6Consumer Goods and Stationery

- 5.4.7Others

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2South America

- 5.5.2.1Brazil

- 5.5.2.2Argentina

- 5.5.3Europe

- 5.5.3.1Germany

- 5.5.3.2Italy

- 5.5.3.3United Kingdom

- 5.5.3.4France

- 5.5.3.5Spain

- 5.5.3.6Rest of Europe

- 5.5.4Asia-Pacific

- 5.5.4.1China

- 5.5.4.2India

- 5.5.4.3Japan

- 5.5.4.4South Korea

- 5.5.4.5Rest of Asia-Pacific

- 5.5.5Middle East

- 5.5.5.1Turkey

- 5.5.5.2GCC

- 5.5.5.3Rest of Middle East

- 5.5.6Africa

- 5.5.6.1South Africa

- 5.5.6.2Nigeria

- 5.5.6.3Egypt

- 5.5.6.4Rest of Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1BOBST Group SA

- 6.4.2Nordmeccanica S.p.A.

- 6.4.3Davis-Standard LLC

- 6.4.4SML Maschinen GmbH

- 6.4.5Reifenhäuser GmbH & Co. KG

- 6.4.6Uteco Converting S.p.A.

- 6.4.7Comexi Group Industries S.A.

- 6.4.8Fujipla (KALBAS & Co. Ltd.)

- 6.4.9Brückner Maschinenbau GmbH & Co. KG

- 6.4.10Barberán S.A.

- 6.4.11OLBRICH GmbH

- 6.4.12Faustel Inc.

- 6.4.13Kohli Industries

- 6.4.14KROENERT GmbH

- 6.4.15Polytype Converting AG

- 6.4.16SOMA Engineering

- 6.4.17W&H (Windmöller & Hölscher KG)

- 6.4.18Jiangyin Changjing Xinda Machinery

- 6.4.19Zhejiang Wenzhou Dapeng Printing Machinery

- 6.4.20Guangdong Decro Film New Materials Co. Ltd.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-need Assessment

Global Lamination Systems Market Report Scope

The lamination systems market encompasses the technologies and equipment used to apply a protective or decorative layer to various substrates such as paper, plastic, metal, and textiles. These systems are widely used across industries like packaging, automotive, electronics, and textiles to enhance product durability, appearance, and functionality. Lamination technologies include thermal, cold, solvent-based, and water-based methods, catering to diverse industrial and commercial applications.

The Lamination Systems Market is segmented by technology (thermal lamination, cold lamination, pressure-sensitive lamination, solvent-based lamination, water-based lamination, other technology), material (film lamination, paper lamination, foam lamination, metal lamination, and other material), end-use industry (packaging, automotive, electronics, textiles, medical & healthcare, consumer goods, and other end-use industries), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.