Shrink Wrap Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

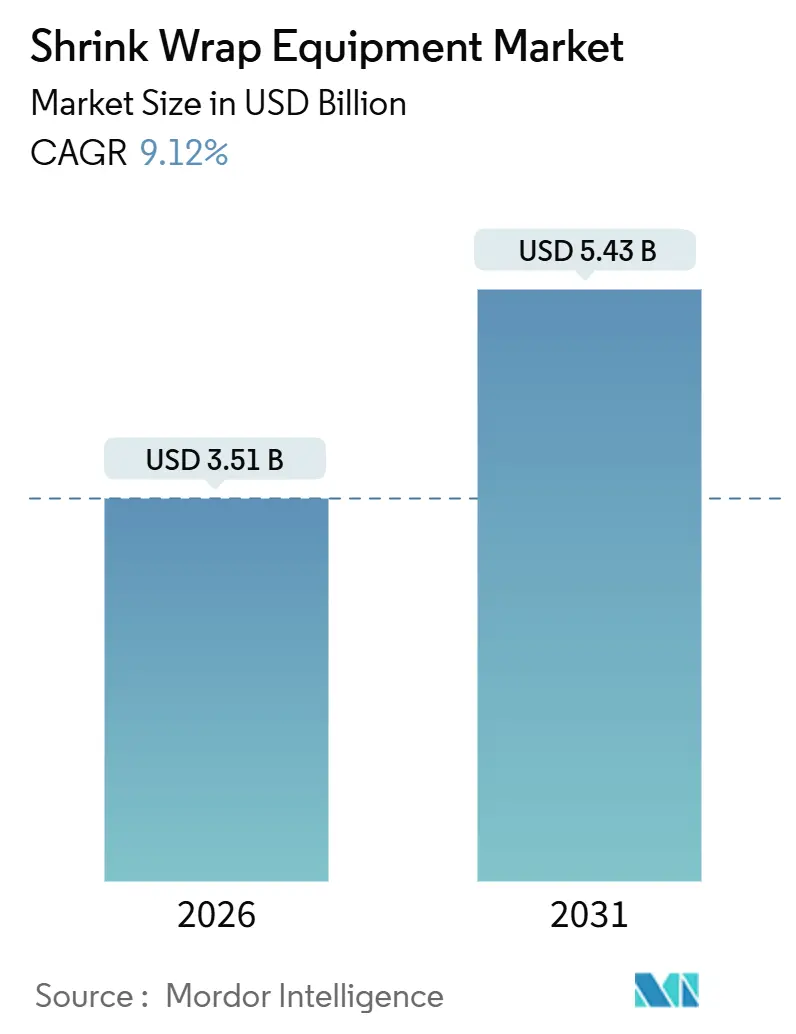

| Market Size (2026) | USD 3.51 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Shrink Wrap Equipment Market Analysis by Mordor Intelligence

The shrink wrap equipment market size reached USD 3.51 billion in 2026 and is projected to attain USD 5.43 billion by 2031, advancing at a 9.12% CAGR over the forecast period. Rising parcel volumes from global e-commerce, sustained investment in automation to offset labor shortages, and tightening recyclability mandates collectively underpin this expansion. Manufacturers prioritize integrated machinery that reduces total labor time per pack, optimizes film yield, and handles mono-material substrates required by circular-economy regulations. Equipment suppliers able to offer servo-driven precision, predictive-maintenance software, and rapid changeovers capture premium pricing while broadening their installed base in fast-growing fulfillment centers.

Key Report Takeaways

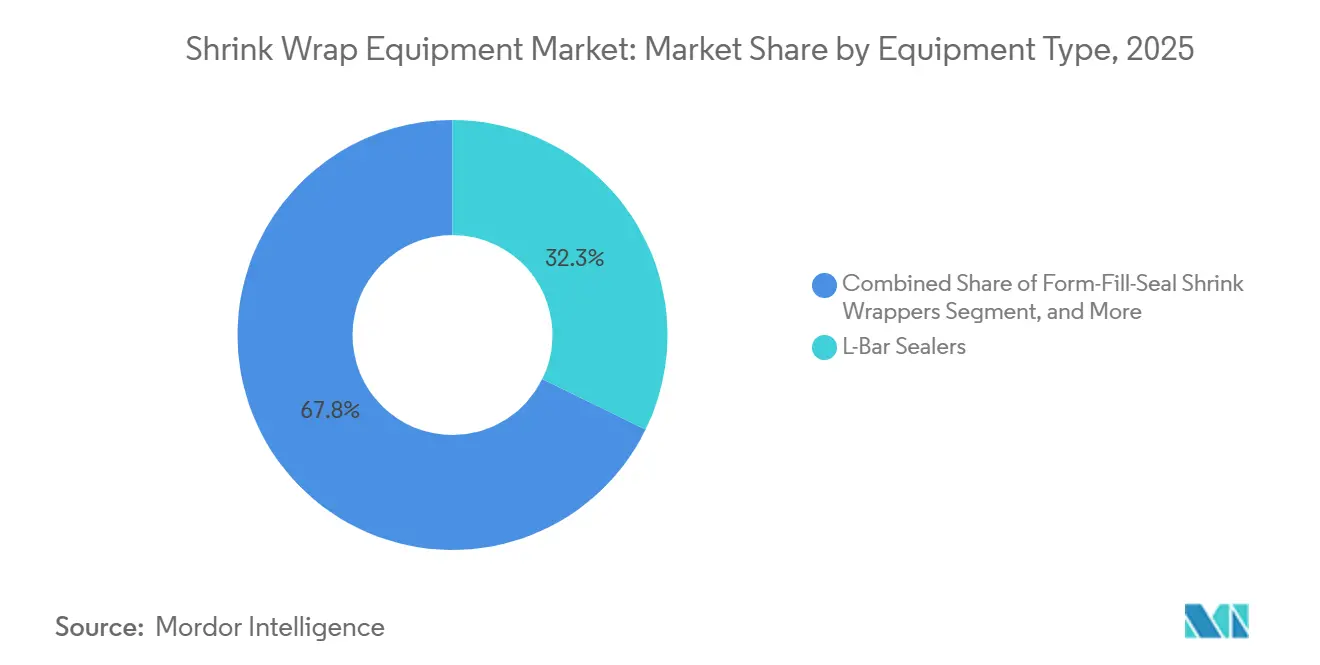

- By equipment type, L-bar sealers captured 32.25% of the shrink wrap equipment market share in 2025.

- By automation level, the shrink wrap equipment market size for fully automatic systems is projected to grow at a 10.57% CAGR from 2026 to 2031.

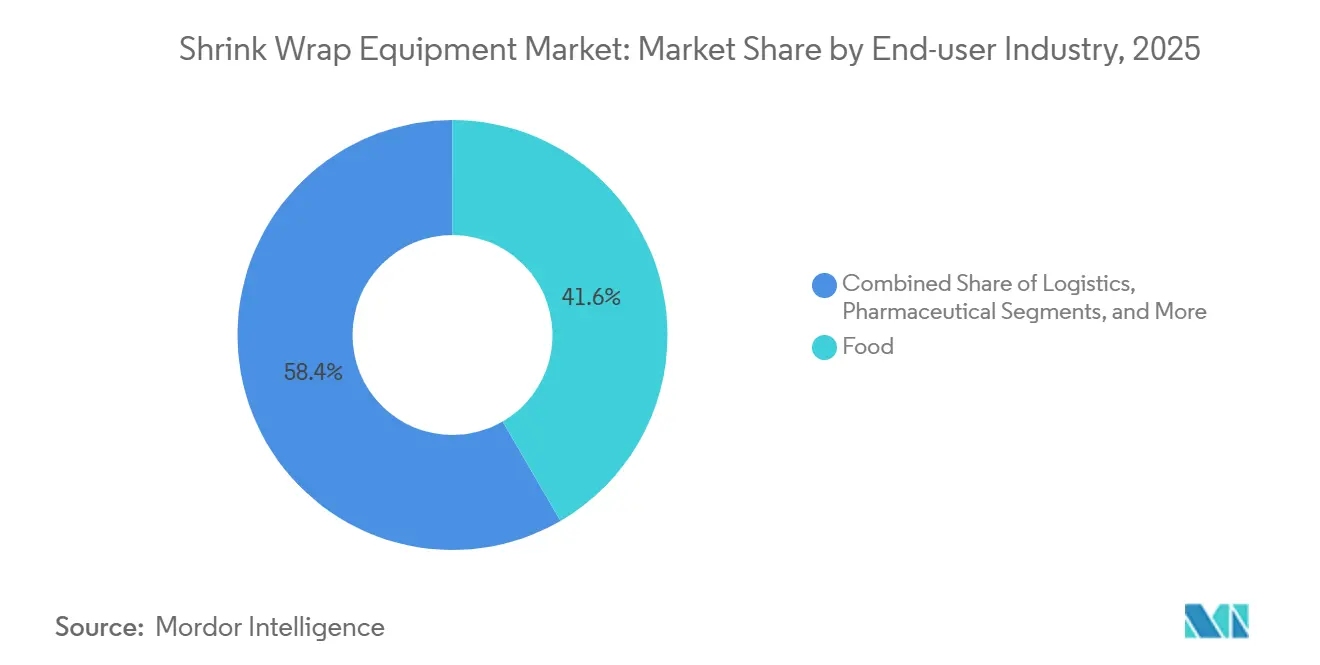

- By end-user industry, food applications captured 41.62% of the shrink wrap equipment market share in 2025.

- By geography, the shrink wrap equipment market size in the Asia-Pacific is projected to grow at a 11.59% CAGR between 2026 and 2031.

Global Shrink Wrap Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce parcel volumes | +2.8% | Global, concentrated in North America and the Asia-Pacific | Short term (≤ 2 years) |

| Growth of food-grade polyolefin shrink films | +1.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Automation demand to reduce labor costs | +2.1% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Brand-owner shift to 360 shrink-sleeve labels | +1.4% | North America and Europe, expanding to the Asia-Pacific | Long term (≥ 4 years) |

| Adoption of Industry 4.0 predictive maintenance | +1.6% | Europe and North America, and selective Asia-Pacific | Long term (≥ 4 years) |

| Circular-economy mandates favoring recyclable films | +2.2% | Europe primary, North America secondary, Asia-Pacific emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Parcel Volumes

Accelerated online retail is pushing fulfillment centers to replace manual wrapping with high-throughput automation that can seal, shrink, and label in a single pass. Operations deploying automated shrink systems report film-use reductions of nearly one-third and measurable gains in load stability, making capital payback feasible within two peak seasons. Logistics operators now account for more than one-fifth of new machinery demand, a share expected to widen as parcel networks densify. Form-Fill-Seal platforms, which integrate bagging, sealing, and shrink heating, align with this consolidation logic and are therefore specified in most greenfield e-commerce hubs. The result is a cascading upgrade cycle in upstream film and tunnel systems that must match the higher line speeds delivered by the new wrappers.

Growth of Food-Grade Polyolefin Shrink Films

Food contact regulations in the United States and the European Union impose stringent migration limits on packaging polymers, accelerating the shift toward mono-material polyolefin shrink films. Compliant films require tighter thermal windows during shrinking, driving the demand for equipment with multi-zone temperature control and real-time seal-strength monitoring. European bans on per- and polyfluoroalkyl substances (PFAS) in food packaging further compel brand owners to reformulate films, creating a retrofit business for machinery that can process the new chemistries without excessive energy draw. Suppliers offering certification support and documented material trials command margins 15-20% above general-purpose alternatives, reinforcing a premium segment within the broader shrink wrap equipment market.

Automation Demand to Reduce Labor Cost

Escalating wages and persistent labor vacancies motivate manufacturers to automate end-of-line packaging. A single fully automatic wrapper can eliminate up to three manual posts per shift, translating into monthly labor savings exceeding USD 9,000 at North American wage rates.[1]Polypack, “Automating Film Removal with the Polypack Unwrapper,” polypack.com Servo motors and linear actuators enhance positional accuracy, cutting cycle time by up to one-quarter and improving seal repeatability. Roughly 40% of new installations now incorporate IoT sensors that feed cloud-based analytics and maintenance dashboards, reducing unplanned stoppages and extending the life of consumables. The capital premium for these smart systems is increasingly offset by predictive-maintenance-enabled uptime, reinforcing the case for rapid technology adoption across both developed and emerging markets.

Brand-Owner Shift to 360 Shrink-Sleeve Labels

Consumer-product marketers value the billboard effect and tamper-evident features provided by full-body shrink sleeves, a format that requires high-precision application and uniform heat distribution. Pharmaceutical and personal-care brands adopt these sleeves to accommodate irregular containers and dense regulatory text, favoring machinery with tension-controlled unwinders and segmented heating tunnels. Sleeve applicators yield notably higher margins for equipment builders due to specialized engineering and lower global volume, yet unit demand grows steadily as sustainability initiatives drive the adoption of lightweight rigid containers that still require design real estate for brand communication. Forward-looking suppliers design machines that can handle recycled-content PET-G and polypropylene sleeves without compromising label integrity, positioning themselves for the next sustainability wave.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex and retrofit complexity | -1.8% | Global, particularly affecting SMEs in emerging markets | Short term (≤ 2 years) |

| Volatile polymer resin prices | -1.4% | Global, with an acute impact on resin-importing regions | Short term (≤ 2 years) |

| Regulatory pressure on heat-energy consumption | -0.9% | Europe is primary, North America is emerging | Medium term (2-4 years) |

| Competition from stretch-hood and paper wraps | -1.1% | Europe and North America, with selective Asia-Pacific adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and Retrofit Complexity

A modern, fully automatic shrink wrapper with Industry 4.0 readiness can cost USD 150,000-500,000, a figure that rises further when conveyors, electrical panels, and facility reconfiguration are factored in. Small and medium-sized enterprises frequently defer such investments or opt for refurbished units, which are priced at one-third lower but often lack energy-efficient drives and predictive diagnostics. Payback is longest in labor-cost-advantaged regions, stretching capital justification beyond typical three-year hurdles. Retrofit projects add complexity, as legacy lines often require floor-space expansion or power-supply upgrades that double the total project cost. This financial barrier hinders the penetration of advanced technology into the lower end of the market, tempering overall growth momentum.

Volatile Polymer Resin Prices

Polyethylene and polypropylene spot prices recorded swings exceeding 20% per quarter during 2025, injecting uncertainty into packagers’ cost structures. Film contracts are typically negotiated on a monthly or quarterly basis, so brand owners facing sharp price increases freeze discretionary capital, including machinery upgrades, until raw material markets stabilize. High resin costs may also trigger short-term switches to stretch-hood or paper solutions, resulting in reduced film consumption and underutilization of shrink tunnels. Equipment suppliers, therefore, experience order deferrals in resin-tight cycles and must maintain flexible manufacturing schedules to absorb demand volatility. Although long-term fundamentals remain strong, these short shocks create ongoing forecasting challenges for machinery builders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Integrated Solutions Propel Form-Fill-Seal Growth

Form-Fill-Seal Shrink Wrappers posted the fastest 11.57% CAGR outlook because users prefer a single chassis that bags, seals, and shrinks without manual film threading. This configuration minimizes footprint and reduces line stops, an advantage that is particularly significant in e-commerce hubs, which run thousands of stock-keeping units per day. L-Bar Sealers nonetheless retained 32.25% of the shrink wrap equipment market share in 2025 due to their versatility and lower upfront cost. Sleeve and bundling wrappers dominate beverage multipack applications, while shrink tunnels capture add-on revenue proportional to sealing equipment installations. The shrink wrap equipment market size for top-down sealing machines, such as Christ Packing Systems’ FilmTeq 250, is expected to expand steadily in food and personal-care sites that value compact footprints and low heat-emission profiles.[2]Pharmaceutical Technology, “Christ Packing Systems Receives Patent for Innovative Sealing Technology in the FilmTeq 250,” pharmaceutical-technology.com

Rising demand for energy efficiency drives a shift toward servo-controlled side-sealers and hood machines that modulate fan speed and heater output, reducing kilowatt-hour consumption without compromising throughput. Premium shrink-sleeve applicators serve pharmaceutical lines that require validated tension control and maintain a margin buffer due to their specialized nature. Emerging designs incorporate machine-vision verification that rejects mis-sleeved containers in real time, protecting downstream labeling accuracy and reducing rework. Suppliers bundling these capabilities win multi-line contracts with global consumer-goods companies standardizing platform architecture across plants.

By Automation Level: Labor Economics Cement Fully Automatic Leadership

Fully Automatic platforms captured 58.04% of 2025 demand and are projected to retain dominance with a 10.57% CAGR, anchored by wage inflation and chronic staffing gaps. Predictive-maintenance modules built into these machines offer uptime guarantees that semi-automatic models cannot match, a critical benefit for 24-7 distribution centers. The integration of collaborative robots to feed products into the sealing zone further enhances productivity and narrows the labor advantages once held by manual tables. The shrink wrap equipment market size for semi-automatic units is expected to continue growing, particularly among mid-tier manufacturers that need flexibility but lack the capital for full automation. Manual stations remain relevant for low-volume specialty items but face gradual attrition as servo prices decline.

Industry-wide, about 60% of packaging plants have installed some form of robotics or advanced automation, signaling a tipping point that favors complete line redesigns over incremental retrofits. As vendors roll out performance-based leasing and equipment-as-a-service models, smaller firms can access full automation without large cash outlays, moderating the capex barrier. Yet such financing packages hinge on reliable data streams from embedded sensors, further entrenching fully automatic architectures as the analytics backbone of modern packaging halls.

By End-user Industry: Logistics Disrupts Traditional Hierarchy

Food processors still accounted for 41.62% of the 2025 shrink wrap equipment market, driven by safety regulations and the need for unitization during cold-chain transport. However, logistics companies tied to e-commerce fulfillment now represent the fastest-growing customer group, with a projected 12.07% CAGR. They require variable-length wraps that can accommodate diverse product catalogs without manual intervention. The shrink wrap equipment market size linked to logistics installations is expected to expand as omnichannel retailers integrate ship-from-store models, requiring compact, easy-to-install lines in backrooms.

Beverage bottlers invest in high-speed sleeve wrappers for multipack promotions, while pharmaceutical companies require stainless-steel housings and validated control software to comply with Good Manufacturing Practice (GMP). Personal-care brands intensify aesthetic requirements, ordering machines capable of handling high-gloss and recycled PET sleeves that match premium visual standards. Industrial goods sectors, especially those in the automotive parts and electronics industries, seek ruggedized machines that deliver puncture-resistant wraps for export crates, thereby expanding demand for thicker-gauge film compatibility.

Geography Analysis

The Asia-Pacific region held 38.51% of global revenue in 2025 and is projected to grow at a 11.59% CAGR, driven by China’s manufacturing scale, India’s accelerating online retail growth, and Southeast Asia’s fresh capital inflows. In China, state-backed programs promoting smart manufacturing have spurred domestic OEMs to develop servo-driven wrappers that undercut European imports in terms of price while closing performance gaps. India, which imported INR 73.5 billion of packaging machinery in fiscal 2024, increasingly balances cost-effective Chinese supply with high-specification German equipment for regulated sectors, underscoring a dual-track demand profile. Japan and South Korea favor premium systems with integrated inspection, reflecting stringent quality norms, whereas Australia’s dispersed population encourages investments in high-throughput, labor-saving machinery to offset high wage levels.

North America remains a replacement and upgrade market dominated by the United States, which alone generates nearly two-thirds of regional spend. Extended Producer Responsibility laws in multiple states are hastening the adoption of equipment compatible with recyclable mono-material films, thereby stimulating retrofit activity despite macroeconomic uncertainty. Canada mirrors U.S. dynamics but benefits from trilateral trade rules that lower import barriers for machinery, while Mexico attracts nearshoring investors seeking proximity to North American consumers without trans-Pacific freight delays. Across the region, fulfillment centers anchor new equipment orders that blend robotics with shrink wrapping to meet same-day delivery expectations.

Europe grapples with the Packaging and Packaging Waste Regulation 2025/40, which compels recyclability and sets energy-consumption thresholds that shrink tunnels must satisfy. Germany spearheads adoption of Industry 4.0-enabled machines, Italy exports specialized food-grade wrappers, and France channels investment into sustainable film technologies. The United Kingdom’s regulatory divergence after Brexit creates local sourcing opportunities but demands dual compliance mapping for exporters. Eastern markets such as Poland and Turkey absorb entry-level automatic lines as foreign brands expand local co-packing, whereas Russia’s demand-side outlook is clouded by supply-chain sanctions that restrict advanced component imports.

Competitive Landscape

Competitive intensity is moderate, with a cluster of multinational vendors competing alongside nimble regional specialists. ProMach, Aetna Group, and Sealed Air leverage broad portfolios and service networks, yet smaller automation-first entrants penetrate niche applications through modular, software-rich offerings. Strategic acquisitions remain common; players such as Krones and Duravant pursue bolt-ons that add technological depth or geographic reach, rather than focusing solely on volume.

Vertical integration into film production or digital services emerges as a differentiator, exemplified by DIC Corporation’s patented process for manufacturing flexible packaging film, which enhances control over consumable-machine compatibility.[3]European Patent Office, “Method for Manufacturing Flexible Packaging Film – EP 3508437 B1,” epo.org Suppliers emphasize servo-drive retrofits, top-down sealing patents, and predictive maintenance platforms to secure service contracts and generate recurring revenue.

Pricing power is concentrated in segments where regulatory compliance or complex changeovers increase switching costs, notably in the pharmaceutical and personal care product industries. Meanwhile, Asian manufacturers are disrupting mid-tier budgets with cost-competitive machines that increasingly match Western performance specifications, forcing incumbents to sharpen their value proposition through bundled analytics and financing. Sustainability credentials also shape competition, as buyers favor partners that can validate recyclable film compatibility and document energy savings with on-machine meters.

Shrink Wrap Equipment Industry Leaders

Texwrap Packaging Systems LLC (Pro Mach Inc.)

Standard-Knapp, Inc.

U.S. Packaging & Wrapping LLC

Conflex Incorporated

Aetna Group S.P.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Krones acquired 60% of GHS Separationstechnik and 100% of Can Systems Worldwide to extend filling and packing technologies for PET recycling.

- September 2025: Polypack introduced the automated Unwrapper, achieving 20 packs per minute and eliminating three manual labor positions per shift.

- August 2025: Christ Packing Systems gained a patent for top-down sealing in the FilmTeq 250 stretchbander, removing the need for a heated table.

- May 2025: SIG InnoVentures and Optima became strategic investors in PulPac to accelerate Dry Molded Fiber packaging solutions.

Global Shrink Wrap Equipment Market Report Scope

The shrink wrap equipment market refers to the segment of packaging machinery that applies heat-shrinkable film around products or bundles to create a secure, tamper-evident, and protective package. These machines are essential for improving product safety, enhancing shelf appeal, and optimizing logistics by reducing bulk.

The Shrink Wrap Equipment Market refers by Equipment Type (L-Bar Sealers, I-Bar Sealers, Side Sealers, Sleeve/Bundling Wrappers, Shrink Tunnels and Hood Machines, Shrink-Sleeve Labelers, and Other Equipment Types), Automation Level (Manual, Semi-Automatic, and Fully Automatic), End-user Industry (Food, Beverage, Pharmaceutical, Personal Care and Cosmetics, Industrial Manufacturing, Logistics, and Other End-user industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| L-Bar Sealers |

| I-Bar Sealers |

| Side Sealers |

| Sleeve / Bundling Wrappers |

| Shrink Tunnels and Hood Machines |

| Shrink-Sleeve Labelers |

| Other Equipment Types |

| Manual |

| Semi-Automatic |

| Fully Automatic |

| Food |

| Beverage |

| Pharmaceutical |

| Personal Care and Cosmetics |

| Industrial Manufacturing |

| Logistics |

| Other End-user industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Equipment Type | L-Bar Sealers | ||

| I-Bar Sealers | |||

| Side Sealers | |||

| Sleeve / Bundling Wrappers | |||

| Shrink Tunnels and Hood Machines | |||

| Shrink-Sleeve Labelers | |||

| Other Equipment Types | |||

| By Automation Level | Manual | ||

| Semi-Automatic | |||

| Fully Automatic | |||

| By End-user Industry | Food | ||

| Beverage | |||

| Pharmaceutical | |||

| Personal Care and Cosmetics | |||

| Industrial Manufacturing | |||

| Logistics | |||

| Other End-user industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the shrink wrap equipment market by 2031?

The marketplace is forecast to reach USD 5.43 billion by 2031, driven by a 9.12% CAGR.

Which region is expected to post the fastest growth through 2031?

The Asia-Pacific region leads with an anticipated 11.59% CAGR, driven by increasing manufacturing scale and e-commerce penetration.

Which equipment type is growing the quickest?

Form-Fill-Seal Shrink Wrappers are projected to grow at a 11.57% CAGR as users increasingly favor integrated bagging, sealing, and shrinking solutions.

How are labor shortages influencing equipment choices?

Persistent staffing gaps prompt buyers to opt for fully automatic systems that automate manual tasks and integrate predictive maintenance analytics.

What regulatory trend is shaping machine specifications in the European Union?

The Packaging and Packaging Waste Regulation 2025/40 mandates recyclability and energy efficiency, spurring demand for equipment that can process mono-material films with lower heat consumption.

Why is the logistics sector gaining importance among end users?

E-commerce fulfillment centers require high-speed, versatile wrapping lines to manage soaring parcel volumes, driving a 12.07% CAGR in logistics installations.

Page last updated on: