Lactose Intolerance Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

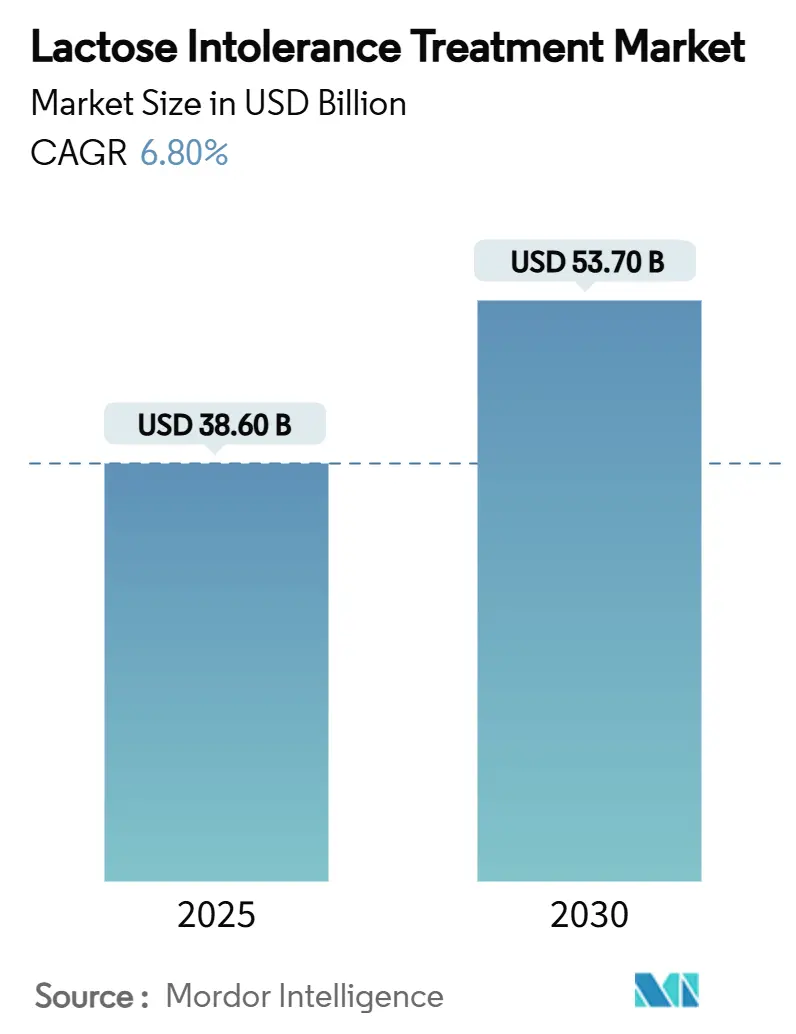

| Market Size (2025) | USD 38.60 Billion |

| Market Size (2030) | USD 53.70 Billion |

| Growth Rate (2025 - 2030) | 6.80% CAGR |

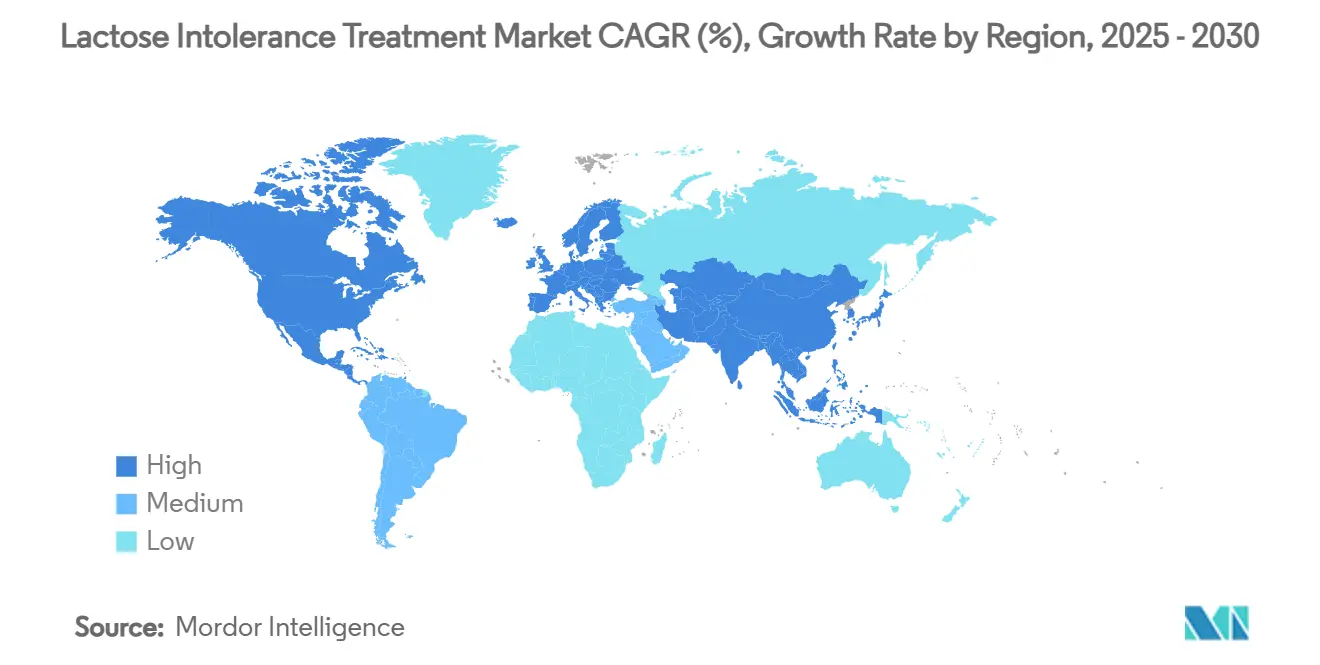

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lactose Intolerance Treatment Market Analysis by Mordor Intelligence

The lactose intolerance treatment market size stood at USD 38.6 billion in 2025 and is forecast to reach USD 53.7 billion by 2030, registering a 6.8% CAGR over the period. This trajectory reflects rising disposable income in high-prevalence regions, expanding flexitarian eating patterns, and rapid technological innovation around enzyme stability and precision fermentation. The lactose intolerance treatment market is also benefiting from retail channel digitalization, with online and direct-to-consumer sales growing faster than traditional outlets. Competitive intensity is shaping around differentiated product positioning, private-label expansion, and biotech-driven protein alternatives that meet demand for dairy nutrition minus digestive discomfort.

Key Report Takeaways

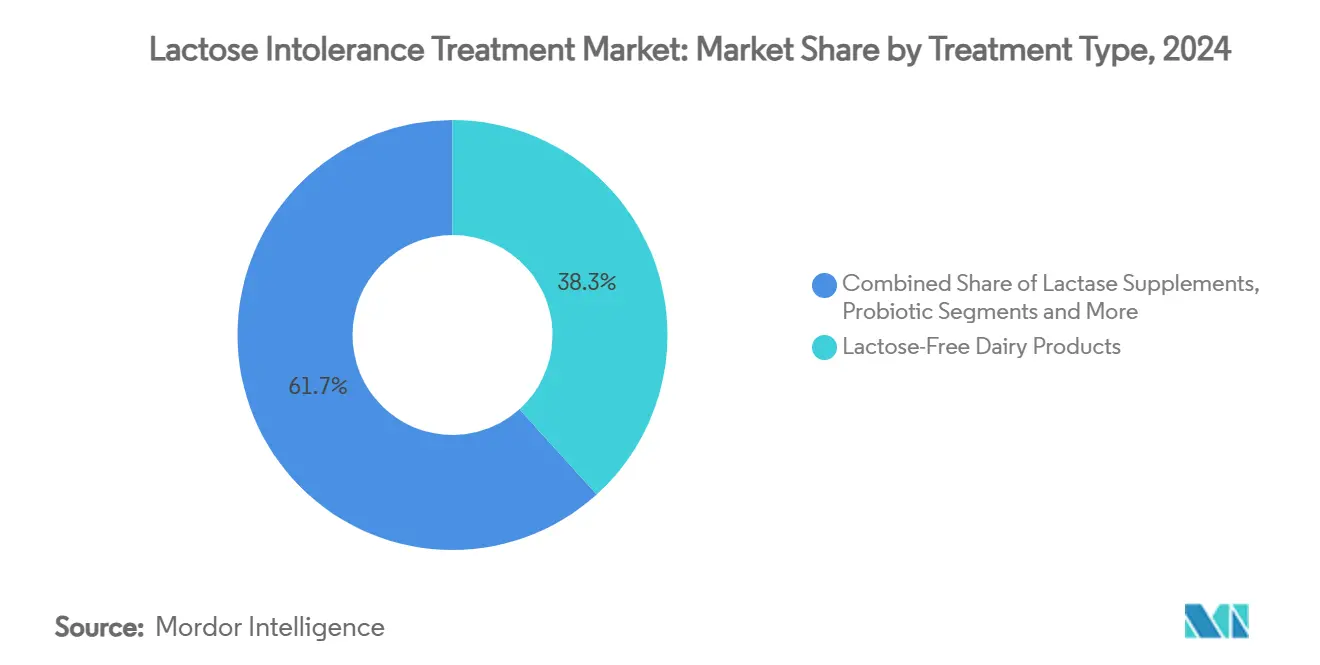

- By treatment type, lactose-free dairy products led with a 38.3% revenue share in 2024; probiotic and synbiotic formulas are forecast to expand at an 11.8% CAGR through 2030.

- By formulation, tablets and capsules held 44.5% of the lactose intolerance treatment market size in 2024, while powders are advancing at a 10.2% CAGR to 2030.

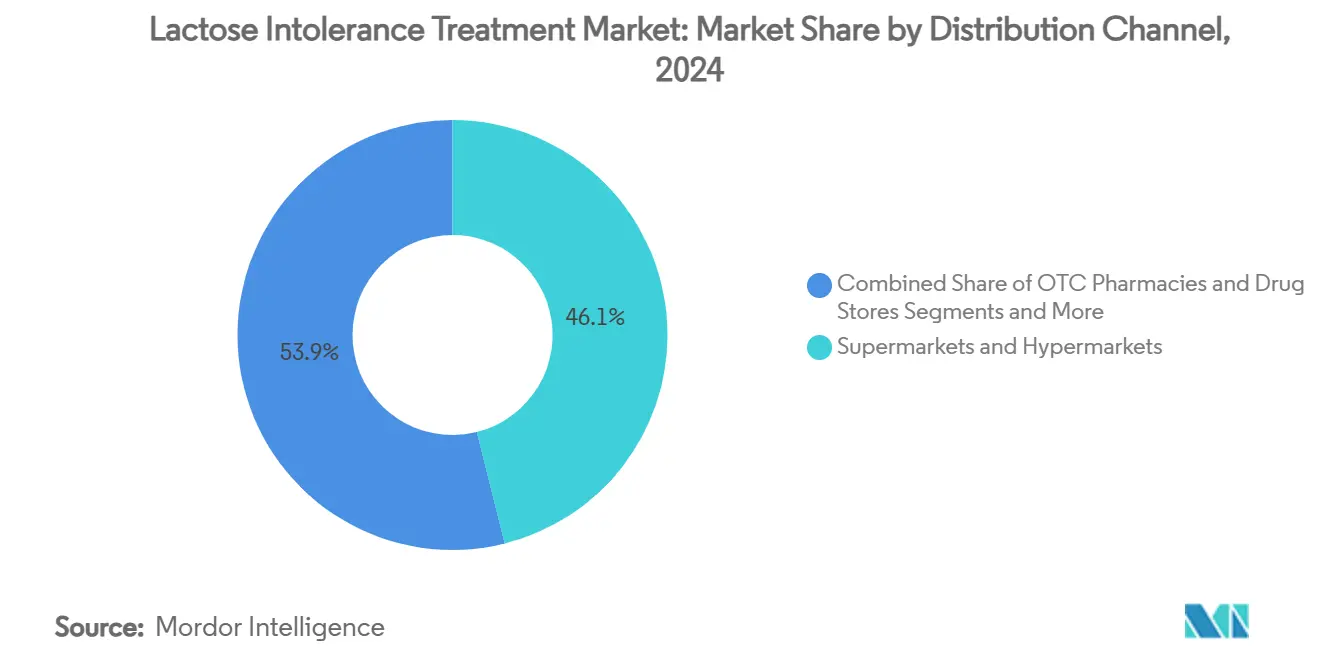

- By distribution channel, supermarkets and hypermarkets commanded 46.1% share of the lactose intolerance treatment market size in 2024, whereas online retailers and direct-to-consumer platforms are expected to rise at a 14.3% CAGR between 2025 and 2030.

- By patient age group, adults (13-59 years) represented 41.2% of the population treated in 2024, while infants (0-2 years) are the fastest-growing segment at a 12.7% CAGR.

- By geography, North America accounted for 35.6% of the lactose intolerance treatment market share in 2024, while Asia-Pacific is projected to post a 10.8% CAGR to 2030.

Global Lactose Intolerance Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of flexitarian diets pushing lactose-free demand | +1.20% | North America & EU (spill-over global) | Medium term (2-4 years) |

| Growing ethnic prevalence in emerging Asian populations | +1.80% | APAC core; spill-over to MEA | Long term (≥ 4 years) |

| Clinical proof of synbiotic interventions | +0.90% | Global | Medium term (2-4 years) |

| Retailer private-label expansion in lactose-free SKUs | +0.70% | North America & EU; expanding to APAC | Short term (≤ 2 years) |

| Digital self-diagnosis tools boosting early detection | +0.50% | Developed markets first | Short term (≤ 2 years) |

| ESG-driven investment shifting dairy toward value-added enzymes | +0.40% | EU-led; spreading worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise of Flexitarian Diets Pushing Lactose-Free Demand

Flexitarian eating is extending the lactose intolerance treatment market beyond clinically diagnosed consumers. Retail take-off is evident in lactose-free milk, which outpaced oat and almond alternatives by 14% growth in the last 12 months as shoppers seek dairy nutrition without discomfort. Brands such as Fairlife surpassed USD 1 billion in annual sales by marrying premium protein levels with zero-lactose positioning. Product pipelines now combine lactose removal with probiotic fortification and sugar reduction to attract wellness consumers. Retailers increasingly allocate chilled shelf space to lactose-free items, normalizing them alongside conventional dairy. This demand diversification is helping stabilize volumes and margins for processors that invest in enzyme technologies and consumer education.

Growing Ethnic Prevalence in Emerging Asian Populations

Asia-Pacific hosts the largest genetically predisposed consumer base, where lactose intolerance affects up to 90% of South Asian adults.[1]Sutter Health, “Lactose Intolerance,” sutterhealth.org Urbanization raises exposure to Western dairy, while disposable incomes improve the ability to pay for specialty treatments. In Indonesia, lactose malabsorption climbs from 21.3% in preschoolers to 73% in junior high students, underscoring the lifelong escalation of unmet need.[2]C. Martianti, “Lactose Intolerance in Indonesian Children,” University of Indonesia Repository, scholar.ui.ac.id Regulators in China now require raw milk inputs for shelf-stable products, a rule that is motivating processors to accelerate lactose-free process innovation. Collectively, these factors support double-digit expansion of the lactose intolerance treatment market through 2030.

Clinical Proof of Synbiotic Interventions

Randomized trials with balanced nine-strain synbiotic blends achieved 70% symptom relief in irritable bowel syndrome, signaling translational potential for lactose intolerance management.[3]MDPI, “Effectiveness of a Balanced Nine-Strain Synbiotic,” mdpi.comBifidobacterium adolescentis iVS-1 supplementation cut diarrhea episodes within two weeks for maldigesters. Evidence that galacto-oligosaccharides modulate inflammatory markers furthers the case for microbiome-targeted protocols. These findings push the lactose intolerance treatment market toward premium therapeutics that promise functional gut restoration, incentivizing investment in clinically backed formulations.

Retailer Private-Label Expansion in Lactose-Free SKU Space

Regional cooperatives such as Prairie Farms launched family-size lactose-free gallons, delivering 33% more volume at competitive pricing. Lower enzyme costs and production scale have lowered unit economics, empowering retailers to grow private-label ranges. Branded producers respond by layering organics, protein enrichment, and synbiotic claims to protect price premiums. The strategic push intensifies merchandising battles inside supermarkets, compelling continued innovation across the lactose intolerance treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regional labeling inconsistencies | -0.80% | EU-US-APAC divergence | Medium term (2-4 years) |

| High production cost of ultra-filtered lactose-free milk | -1.10% | Greater impact in emerging markets | Short term (≤ 2 years) |

| Consumer confusion between dairy allergy & intolerance | -0.60% | Lack of health education in several regions | Long term (≥ 4 years) |

| Limited reimbursement for OTC lactase supplements | -0.40% | Primarily developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regional Labeling Inconsistencies

The FDA’s draft to revoke 18 dairy standards of identity heightens uncertainty over lactose-free claims. Europe caps “reduced-lactose whey” at 60% residual lactose, while Asian regulators apply unique thresholds, forcing exporters to vary formulations. Meeting divergent rules inflates compliance costs and slows multinational launches, restraining growth in the lactose intolerance treatment market.

High Production Cost of Ultra-Filtered Lactose-Free Milk

Ultrafiltration requires precise mineral management and capital-intensive membranes that drive up per-liter costs, with acid-whey pH optimization adding complexity. Novel β-galactosidase strains cut hydrolysis time dramatically but need investment to scale. Such economics dampen affordability in emerging markets, constraining the lactose intolerance treatment market when price sensitivity is high.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Dairy Leadership Amid Synbiotic Upsurge

Lactose-free dairy products delivered 38.3% of 2024 revenue, confirming mainstream preference for familiar taste and nutrient density. Probiotic-synbiotic formulations, however, are set to expand at an 11.8% CAGR, buoyed by clinical validation and premium pricing potential. Lactase supplements retain a core audience that requires on-demand digestive aid when consuming conventional dairy. Non-dairy alternatives encounter stiffer rivalry as lactose-free dairy narrows sensory gaps. Precision-fermentation proteins produced by companies like Perfect Day introduce an animal-free yet dairy-identical protein source positioned at the intersection of sustainability and gut comfort.

A widening R&D pipeline blurs lines between food and therapy. Enzyme-treated whey proteins integrate into sports nutrition, widening addressable demand. Fermented infant formulas offer lactose-safe options with improved digestibility. Collectively, these dynamics sustain the lactose intolerance treatment market as a nexus for biotech, functional foods, and consumer health.

By Formulation: Tablets Hold Ground, Powders Accelerate

Tablets and capsules comprised 44.5% of the 2024 value thanks to portability, unit dosage accuracy, and pharmacist endorsement. Powder formats are projected to climb 10.2% annually as enzyme immobilization boosts shelf life and solubility. The lactose intolerance treatment market size for powders is expected to broaden as consumers blend them into smoothies and baked goods. Drops retain pediatric relevance, while chewables attract users seeking a pleasant taste without water intake.

Advances such as spray-freeze-dried probiotics enable novel respiratory delivery vehicles, hinting at future category disruption. Ingredient suppliers like Kerry, after acquiring Chr. Hansen’s lactase unit now bundles stabilized enzymes with flavor systems to shorten brand owners' development timelines.

By Distribution Channel: Digital Momentum Reshapes Reach

Supermarkets and hypermarkets still hold a 46.1% share, leveraging shopper familiarity and impulse purchasing. Yet online and direct-to-consumer routes are rising at 14.3% CAGR as brands deploy subscription models that auto-replenish lactase tablets and lactose-free UHT milk. Data-driven storefronts provide personalized recommendations derived from nutrigenomic tests. Specialty stores concentrate on premium synbiotics and animal-free proteins, maintaining a niche but profitable foot traffic. Successful companies marry e-commerce agility with selective brick-and-mortar presence to enhance trial and trust across the lactose intolerance treatment market.

By Patient Age Group: Lifespan-Spanning Needs

Adults 13-59 account for 41.2% of cases and prioritize convenience, driving steady demand for tablet and ready-to-drink formats. Infant incidence is climbing fastest at a 12.7% CAGR as secondary intolerance post-infection triggers physician-recommended specialty formulas. Children require flavored chewables, whereas the geriatric cohort values multi-benefit gut health products that mitigate broader digestive issues. Personalized diet apps now combine genetic lactase persistence testing with age-specific nutrition algorithms, enabling tailored product bundles within the lactose intolerance treatment industry.

Geography Analysis

North America dominates the lactose intolerance treatment market, holding a 35.6% share in 2024. Mature regulatory frameworks, extensive cold chain infrastructure, and aggressive private-label activity underpin volume growth. Brands leverage omnichannel tactics, integrating telehealth consultations and at-home breath tests to reinforce consumer loyalty. Investment in precision fermentation plants across the United States reflects a commitment to next-generation lactose-free dairy proteins.

Asia-Pacific is the fastest-growing region, registering a 10.8% CAGR to 2030 as awareness and purchasing power converge with exceptionally high genetic prevalence. The lactose intolerance treatment market size in key APAC metros is expanding through localized flavors and smaller pack sizes that suit traditional meal occasions. Government nutrition campaigns in Japan and Korea promote low-lactose processed milk to improve calcium intake without discomfort.

Europe, the Middle East & Africa, and South America collectively add diversification potential. EU consumers show a preference for sustainable supply chains, encouraging the uptake of enzyme-efficient processes that cut energy use. Goat milk products, naturally lower in lactose, have gained traction and are forecast to reach USD 18.28 billion globally by 2033. In Latin America, cross-border trade with the United States accelerates the adoption of over-the-counter lactase supplements, while local dairies pilot lactose-free line extensions to protect their domestic share.

Competitive Landscape

The lactose intolerance treatment market presents moderate fragmentation—Johnson & Johnson’s Lactaid range benefits from pharmacist endorsement and widespread shelf presence. Nestlé Health Science exploits multi-category expertise, recently debuting precision-fermented whey beverages that remove lactose yet mimic conventional dairy functionality. Prairie Farms extends cooperative scale to democratize lactose-free milk pricing in the U.S. heartland.

Strategic consolidation is visible among ingredient players: Kerry’s purchase of Chr. Hansen-Novozymes' lactase assets signal ambition to provide end-to-end solutions from enzyme to finished product. Zydus Lifesciences acquired a 50% stake in Sterling Biotech, securing entry to the precision-fermentation supply chain. Meanwhile, smaller innovators such as Perfect Day license animal-free casein to dairy majors, accelerating go-to-market speed.

Digital-first entrants leverage direct-to-consumer logistics to undercut pharmacies, bundling breath tests and product subscriptions. In response, incumbents integrate telehealth partnerships and dynamic pricing to retain share. Mergers and technology alliances are expected to continue as firms race to secure enzyme IP, optimize fermentation yields, and expand global distribution footprints.

Lactose Intolerance Treatment Industry Leaders

Johnson & Johnson (Lactaid)

Danone SA

Nestlé Health Science

Arla Foods amba

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nestlé enhanced precision-fermentation capabilities and launched Cowabunga animal-free dairy beverages alongside lactose-free whey protein powder.

- August 2024: Zydus Lifesciences acquired 50% of Sterling Biotech from Perfect Day to manufacture fermented animal-free protein.

- July 2024: Leprino Foods partnered with Fooditive Group to produce non-animal casein protein via precision fermentation.

- April 2024: Prairie Farms rolled out “Gold Standard” lactose-free milk, cottage cheese, and sour cream, including family-size gallons

Global Lactose Intolerance Treatment Market Report Scope

| Lactase Supplements |

| Probiotic & Synbiotic Formulas |

| Lactose-Free Dairy Products |

| Non-Dairy Milk Alternatives |

| Enzyme-Treated Dairy Ingredients |

| Tablets & Capsules |

| Drops & Liquids |

| Powders |

| Chewables |

| Others |

| OTC Pharmacies & Drug Stores |

| Supermarkets & Hypermarkets |

| Online Retailers & DTC |

| Specialty Stores |

| Others |

| Infants (0-2 yrs) |

| Children (3-12 yrs) |

| Adults (13-59 yrs) |

| Geriatric (60+ yrs) |

| Pregnant & Lactating Women |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Lactase Supplements | |

| Probiotic & Synbiotic Formulas | ||

| Lactose-Free Dairy Products | ||

| Non-Dairy Milk Alternatives | ||

| Enzyme-Treated Dairy Ingredients | ||

| By Formulation | Tablets & Capsules | |

| Drops & Liquids | ||

| Powders | ||

| Chewables | ||

| Others | ||

| By Distribution Channel | OTC Pharmacies & Drug Stores | |

| Supermarkets & Hypermarkets | ||

| Online Retailers & DTC | ||

| Specialty Stores | ||

| Others | ||

| By Patient Age Group | Infants (0-2 yrs) | |

| Children (3-12 yrs) | ||

| Adults (13-59 yrs) | ||

| Geriatric (60+ yrs) | ||

| Pregnant & Lactating Women | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Frequently Asked Question

Concise Answer

What is the current size of the lactose intolerance treatment market?

The lactose intolerance treatment market size reached USD 38.6 billion in 2025.

How fast is the lactose intolerance treatment market expected to grow?

The market is projected to expand at a 6.8% CAGR, reaching USD 53.7 billion by 2030.

Which treatment type is leading the market today?

Lactose-free dairy products lead, accounting for 38.3% revenue share in 2024.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region, set to progress at a 10.8% CAGR through 2030.

What distribution channel is expanding most quickly?

Online retailers and direct-to-consumer platforms are forecast to rise at a 14.3% CAGR between 2025 and 2030.

How concentrated is the competitive landscape?

The top five companies control around 60% of sales, giving the market a concentration score of 6 on a 10-point scale.

Page last updated on: