Gastrointestinal Bleeding Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

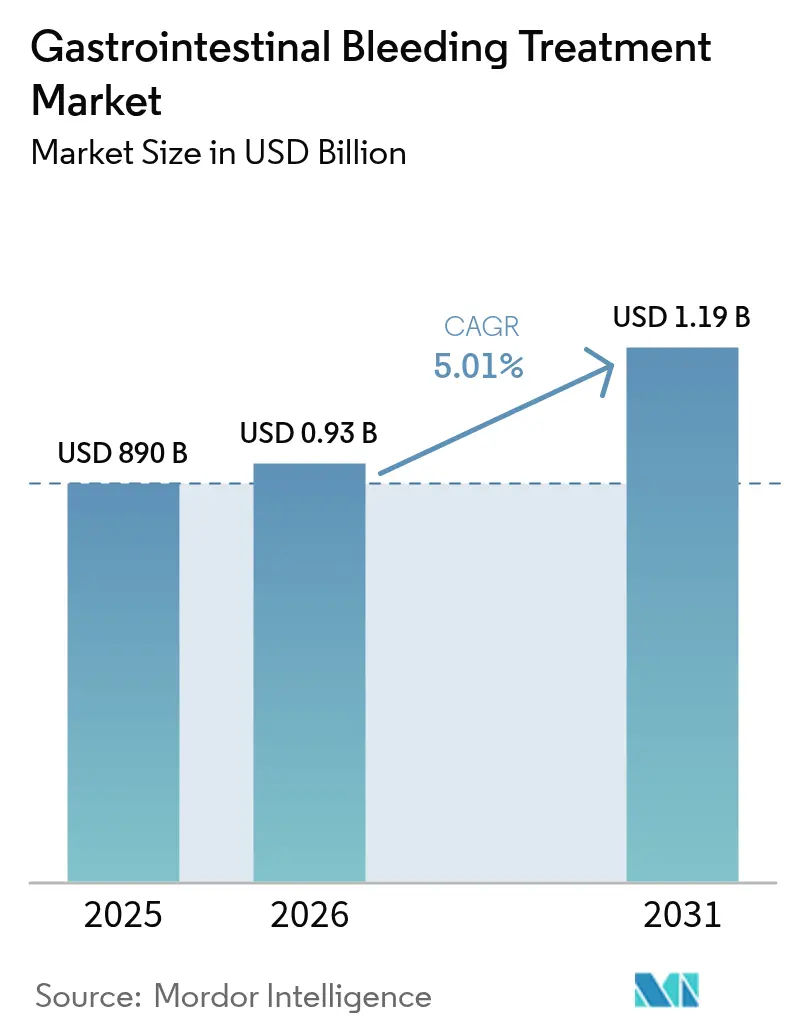

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.19 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

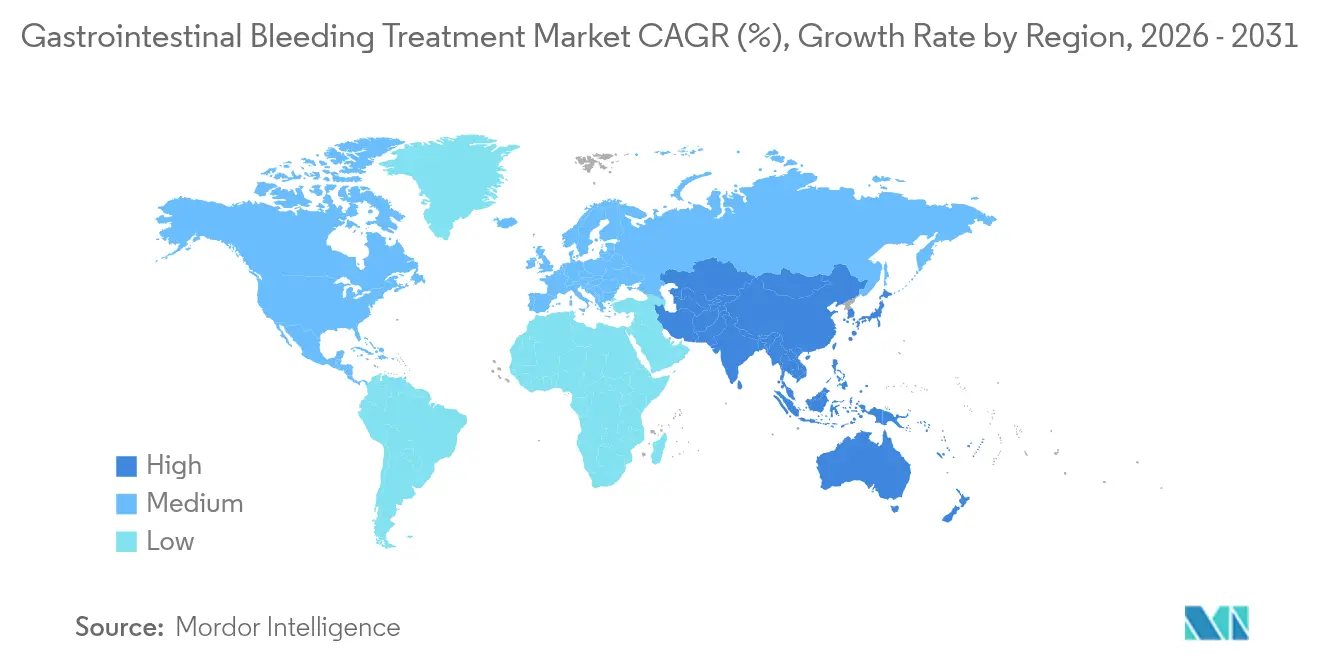

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

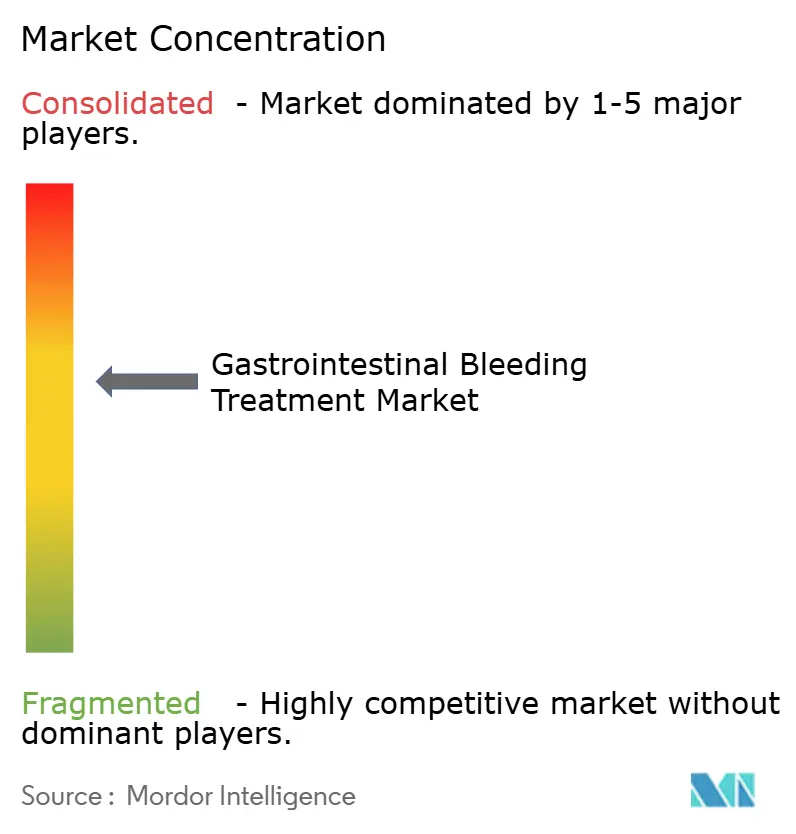

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gastrointestinal Bleeding Treatment Market Analysis by Mordor Intelligence

The gastrointestinal bleeding treatment market size in 2026 is estimated at USD 934.59 million, growing from 2025 value of USD 890 million with 2031 projections showing USD 1.19 billion, growing at 5.01% CAGR over 2026-2031. Momentum comes from the steady rise in complex upper-GI cases, broader adoption of minimally invasive hemostasis, and a reimbursement climate that rewards technology capable of shortening hospital stays. Hospitals remain the spending core, yet ambulatory surgical centers (ASCs) attract investment because Medicare now reimburses an expanded list of endoscopic procedures, allowing outpatient sites to capture revenue that once defaulted to inpatient settings. Endoscopic mechanical clips still dominate procedure volumes, but topical hemostatic sprays, capsule endoscopy, and AI-assisted risk stratification tools are the fastest-scaling niches. Regionally, North America anchors demand, while Asia-Pacific delivers the highest incremental growth as hospitals equip new endoscopy suites and train specialists.

Key Report Takeaways

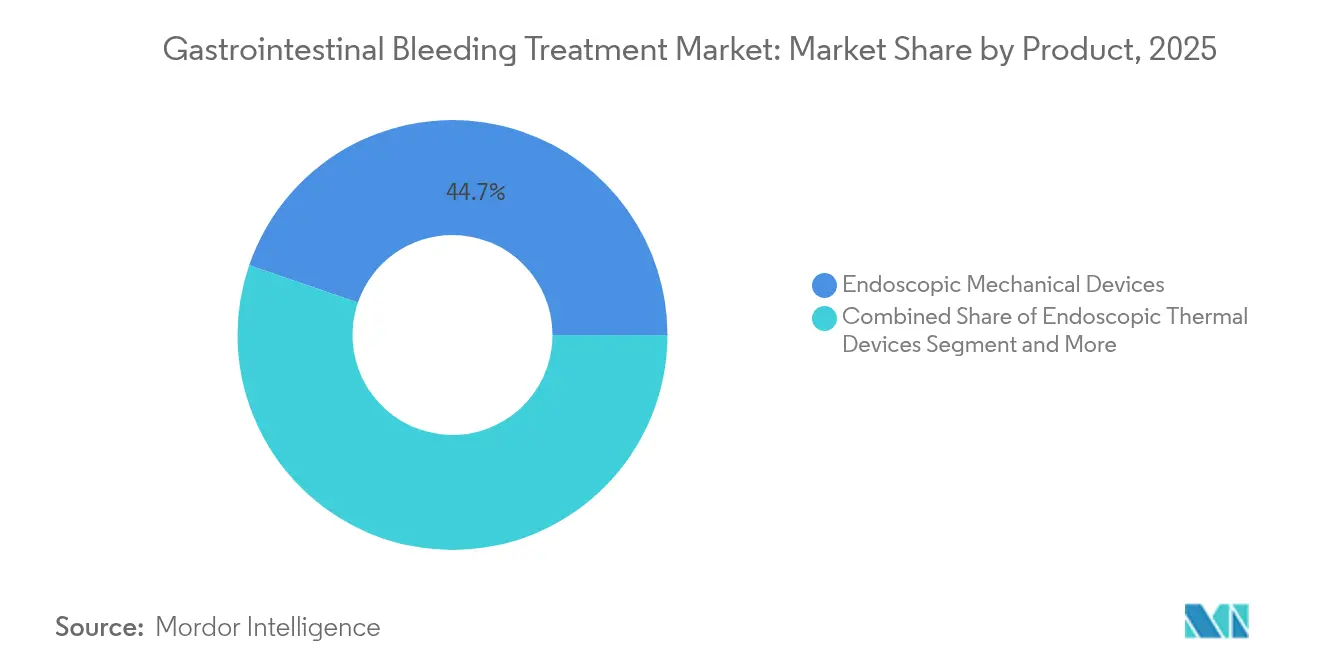

- By product, endoscopic mechanical devices led with 44.74% gastrointestinal bleeding treatment market share in 2025; topical hemostatic sprays are projected to expand at a 11.9% CAGR to 2031.

- By GI tract division, upper-GI procedures accounted for 62.53% of the gastrointestinal bleeding treatment market size in 2025, while small bowel interventions advance at a 9.74% CAGR through 2031.

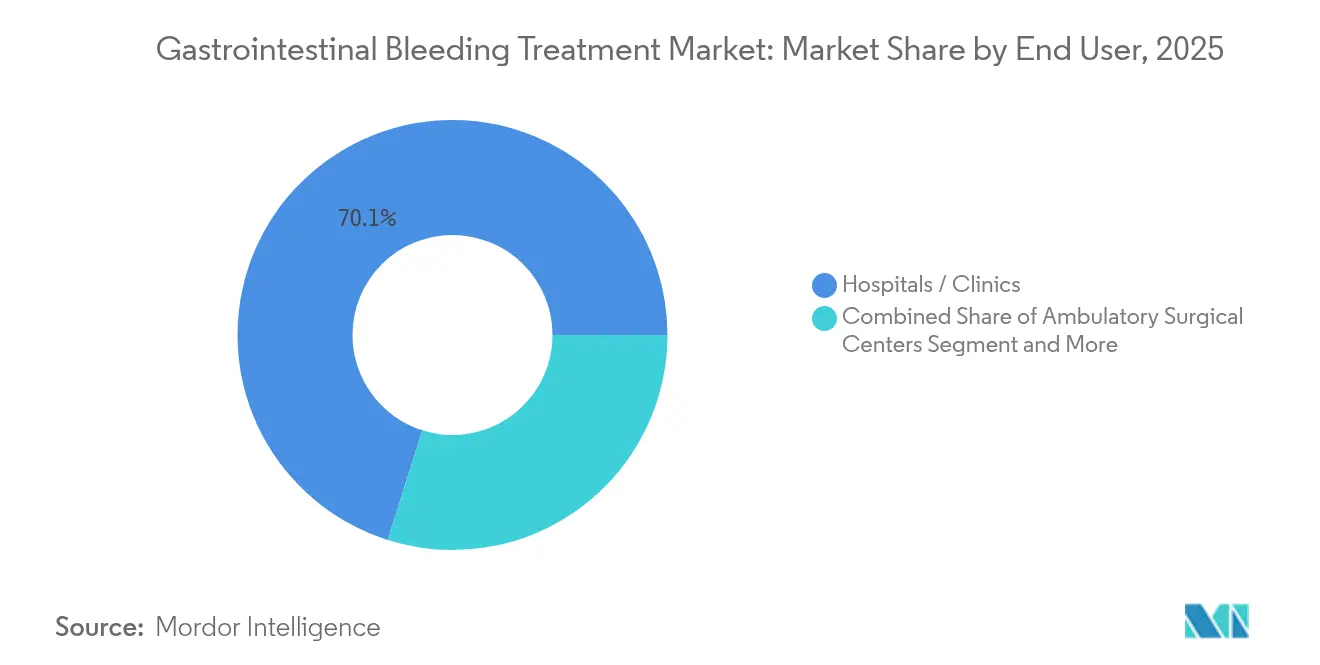

- By end user, hospitals and clinics held 70.12% revenue share in 2025; ASCs record the fastest growth at 9.18% CAGR to 2031.

- By geography, North America commanded 40.25% of the gastrointestinal bleeding treatment market in 2025, whereas Asia-Pacific posts an 8.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gastrointestinal Bleeding Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of upper-GI bleeding cases | +1.2% | Global, higher in North America & Europe | Medium term (2-4 years) |

| Shift toward minimally invasive endoscopic hemostasis | +0.8% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Availability of next-generation clips & sprays | +0.9% | Global, led by developed markets | Short term (≤ 2 years) |

| Expanding elderly population using anticoagulants | +1.1% | Global, especially Asia-Pacific & North America | Long term (≥ 4 years) |

| AI-driven bleeding-risk prediction algorithms | +0.4% | North America & EU first, global rollout | Medium term (2-4 years) |

| Hospital incentives for 24/7 GI-bleed teams | +0.6% | North America & EU, selective Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Of Upper GI Bleeding Cases

Upper-GI bleeding rates remain 84-160 per 100,000 adults, with mortality still near 10% despite newer therapies. Anticoagulant uptake in aging cohorts magnifies risk and pushes clinicians to deploy combination hemostasis kits during the index endoscopy to curb costly rebleeds. Hospitals quantify savings when rapid hemostasis avoids surgical conversion, strengthening demand for devices that shorten procedure time and enhance clip retention. Manufacturers therefore package clips, sprays, and injection catheters in modular kits to ensure readiness for any bleeding phenotype. Health systems with capitated payment models increasingly standardize these kits across sites to cut variation and improve outcomes reporting.

Shift Toward Minimally-Invasive Endoscopic Hemostasis

Over-the-scope clips and single-channel suturing systems now seal full-thickness wall defects once referred for open surgery, reducing hospital days and narcotic use. Boston Scientific’s OverStitch NXT connects to a standard gastroscope and completes suture patterns in fewer passes, allowing faster turnover in busy labs. Early data show lower 30-day rebleed rates relative to thermal coagulation, especially for fibrotic ulcers. The skill gap, however, necessitates simulation-based upskilling and has opened a parallel market for VR-enabled training modules. Hospitals that couple advanced tools with rigorous credentialing enjoy fewer emergency transfers and better quality scores under pay-for-performance contracts.

Availability Of Next-Generation Hemostatic Clips & Sprays

FDA clearance for plant-derived powders such as Traumagel validates alternative biomaterials that form an instant mechanical barrier, useful in coagulopathic patients. STERIS’s Padlock Clip deploys circumferential arms that grasp tissue in under 12 seconds, trimming average deployment time by 4 minutes 45 seconds and reducing the clip count per lesion by 44% against legacy systems. Non-contact powders like Hemospray coat diffuse oozing surfaces, closing a treatment gap for malignancy-related bleeding where mechanical closure is impractical[1]Cook Medical, “Hemospray Endoscopic Hemostat,” cookmedical.com. Side-by-side trials demonstrate significant reductions in procedure length and anesthesia exposure when sprays precede clip placement for large-area bleeding.

Expanding Elderly Population Using Anticoagulants

Direct oral anticoagulants drive major bleeding at 27.9 per 1,000 person-years, with the GI tract accounting for 45% of events. Mortality climbs to 10.5% within 28 days for anticoagulated patients compared with 2.8% for controls, intensifying calls for device-plus-drug protocols that expedite reversal and achieve durable hemostasis. Device makers now design clips validated in anticoagulated models and seek labeling that specifies performance under altered coagulation. Hospitals develop bundled order sets embedding reversal agents and next-gen clips to cut time-to-hemostasis, an approach that bolsters procedure volumes in centers of excellence and pushes the gastrointestinal bleeding treatment market toward outcome-based purchasing agreements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled endoscopists in emerging markets | -0.7% | Asia-Pacific emerging, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| High cost of advanced endoscopic devices | -0.5% | Global, most acute in price-sensitive regions | Medium term (2-4 years) |

| Supply-chain bottlenecks in specialty metals & powders | -0.3% | Global manufacturing hubs in Asia | Short term (≤ 2 years) |

| Antimicrobial-stewardship limits on prophylactic PPIs | -0.4% | North America & Europe regulatory environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Skilled Endoscopists In Emerging Markets

Asia-Pacific adds thousands of endoscopy rooms annually, yet lacks certified staff trained in advanced closure devices, delaying uptake of premium solutions. ESGE recommends objective competence metrics that extend training cycles, placing strain on national budgets and widening urban-rural gaps. Vendors respond with simplified clip applicators and tele-mentoring platforms, but credentialing backlogs persist. Consequently, procurement committees defer purchase of high-end kits until skill pipelines mature, tempering the gastrointestinal bleeding treatment market in lower-income countries.

High Cost Of Advanced Endoscopic Devices

Single-use suturing catheters and robotic platforms raise per-case supply costs by up to USD 640, challenging ASCs that operate on fixed facility fees. Hospitals renegotiate bulk contracts, demanding tiered pricing and evidence of rebleed avoidance to justify premiums. Component shortages in nitinol and biopolymer powders elevate manufacturing costs, which suppliers partially pass through in 2025[2]U.S. FDA, “Medical Device Supply Chain and Shortages,” fda.gov. Emerging markets pivot toward reusable devices, but stricter infection-control rules in high-income jurisdictions constrain that option, keeping pricing pressure elevated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Mechanical Devices Lead Innovation Wave

Mechanical clips held 44.74% of the gastrointestinal bleeding treatment market in 2025 thanks to decades-long clinician familiarity and multi-lesion versatility. The segment benefits from continuous miniaturization and stronger grasp forces that cut clip counts per case. The gastrointestinal bleeding treatment market size for topical sprays, though smaller, expands at a 11.9% CAGR because powders address diffuse bleeding and function regardless of coagulation status. Thermal probes and injection catheters maintain niche roles for variceal management and are frequently bundled in combination kits to guarantee first-pass hemostasis.

Performance metrics now focus on deployment speed; Boston Scientific’s MANTIS clip requires 4 fewer clips and nearly 5 fewer minutes than predecessors, freeing lab capacity for additional cases. Biocompatible hemostatic agents sourced from algae reduce immunogenicity, opening use in immunosuppressed cohorts. Manufacturers differentiate via pre-loaded, rotation-controlled handle designs and radiopaque markers that aid fluoroscopic confirmation during hybrid procedures.

By GI Tract Division: Small Bowel Innovations Drive Growth

Upper-GI interventions represented 62.53% gastrointestinal bleeding treatment market share in 2025, supported by clear diagnostic pathways and higher bleeding incidence. Capsule endoscopy enables small bowel visualization without fluoroscopy, propelling mid-GI procedure volumes at a 9.74% CAGR. The gastrointestinal bleeding treatment market size attributed to small-bowel cases will accelerate as PillCam Genius transmits real-time alerts, letting clinicians retrieve and treat lesions during the same encounter.

Robotic wireless capsules under development incorporate steering coils and onboard drug reservoirs to one-day deliver therapeutics directly to bleeding sites. Pan-intestinal capsules appeal to inflammatory bowel disease care models, promising a single-day, non-sedated assessment of mucosal health. Lower-GI bleeding management also benefits from AI-aided colonoscopy that flags oozing lesions in real time, tightening polypectomy margins and reducing miss rates in busy outpatient lists.

By End User: ASCs Capitalize On Outpatient Shift

Hospitals anchored 70.12% of procedures in 2025, supported by trauma call coverage and interventional radiology backup. Nonetheless, ASCs grow at 9.18% CAGR as Medicare’s ASC fee schedule now lists over 30 upper- and lower-GI codes, incentivizing providers to move eligible bleeds to outpatient sites. Diagnostic labs integrate with regional ASC networks to offer platelet function testing and drug-level assays that inform reversal strategies before same-day discharge.

Specialized GI centers win referrals by combining 24/7 call coverage with fixed-price episode bundles that guarantee no unplanned readmission penalties. Manufacturers supply ASC-specific device kits with pre-sterilized, single-use handles that align with quicker room turnovers. Vendor service models now include loaner inventories delivered overnight, minimizing downtime and smoothing capital expenditure peaks for independent operators.

Geography Analysis

North America generated 40.25% of global revenue in 2025 because Medicare reimburses both inpatient and ASC-based hemostasis, stabilizing cash-flows for providers. U.S. health systems also pilot AI-guided triage that decreases emergency endoscopy wait times and promotes early intervention. Canada’s single-payer framework funds national bulk buys of hemostatic powders, ensuring uniform access and driving predictable procurement cycles. Mexico benefits from cross-border medical tourism for endoscopic treatment, particularly among uninsured U.S. patients seeking lower procedure costs.

Asia-Pacific is the fastest-growing region at 8.49% CAGR, reflecting a sharp rise in gastrointestinal cancers and anticoagulant prescriptions. China upgrades county-level hospitals with fluoroscopy suites and capsule endoscopy readers under national health reforms, whereas Japan commercializes robot-assisted suturing platforms that cater to a super-aged population. India’s private hospitals expand advanced GI services for an insured middle class and focus on rebleed-avoidance metrics to compete for medical tourists from the Gulf.

Europe posts stable growth, aided by ESGE guidelines that harmonize training and drive collective device purchasing across hospital consortia. Germany pioneers outpatient reimbursement for over-the-scope clips, while the United Kingdom expands rapid-access GI bleed units to meet the National Health Service’s 4-hour emergency target. The new EU Medical Device Regulation lengthens approval timelines but lifts public confidence, encouraging hospitals to invest in CE-marked innovations.

The Middle East and Africa plus South America occupy smaller shares yet report double-digit volume growth as tertiary centers open dedicated endoscopy units. High import tariffs remain a hurdle, steering facilities toward multipurpose devices that cover both bleeding and polypectomy use-cases.

Competitive Landscape

Market fragmentation persists, with the top five suppliers accounting for significant global revenue. Boston Scientific leverages a portfolio that spans Resolution 360 clips, OverStitch suturing, and Gold Probe catheters, underpinned by longitudinal data showing lower rebleed rates than monotherapy approaches. STERIS differentiates through vacuum-packaged, ready-to-use clip systems and integrated irrigation pumps that slot into existing towers. Cook Medical focuses on non-contact powders and actively seeks indications that extend beyond NVUGIB into malignant bleeding.

Emerging entrants exploit novel biomaterials; Cresilon’s plant-based Traumagel gains early adopters among trauma surgeons and may transition into endoscopy once delivery catheters are scaled. Software firms such as RedEye AI bundle real-time bleed detection into visualization systems, selling subscriptions that integrate with existing scopes. Partnerships between device firms and AI platforms accelerate because predictive analytics boost procedure volumes by flagging high-risk patients earlier.

Direct purchasing groups in the United States negotiate multi-year value-based contracts tying clip spend to rebleed rates, motivating vendors to supply both training and data-collection dashboards. In Asia, distributors play a pivotal role due to fragmented hospital ownership, compelling manufacturers to co-invest in local training centers that shorten learning curves for advanced tools.

Gastrointestinal Bleeding Treatment Industry Leaders

Boston Scientific Corporation

CONMED Corporation

ERBE Elektromedizin GmbH

Ovesco Endoscopy AG

Cook Group (Cook Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: NextBiomedical announced that its Nexpowder hemostatic powder lowered rebleed rates in a large randomized NVUGIB trial published in GUT.

- February 2024: Researchers unveiled GastroShield sprayable hydrogel sealant, demonstrating superior wound sealing in preclinical GI models.

Global Gastrointestinal Bleeding Treatment Market Report Scope

As per the scope of the report, gastrointestinal bleeding refers to any form of hemorrhage or blood loss that occurs within the digestive organs like the esophagus, stomach, and small intestine, including the duodenum and rectum. It includes all forms of bleeding of the gastrointestinal tract, from the mouth to the rectum.

The Gastrointestinal Bleeding Treatment Market is Segmented by Product (Endoscopic Mechanical Devices, Endoscopic Thermal Devices, and Other Products), GI Tract Division (Upper GI Tract and Lower GI Tract), End User (Hospitals/Clinics, Ambulatory Surgical Centres, and Other End Users), and Geography (North America, Europe, Asia Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD billion) for the above segments.

| Endoscopic Mechanical Devices |

| Endoscopic Thermal Devices |

| Endoscopic Injection Devices |

| Topical Hemostatic Sprays |

| Combination Therapy Kits |

| Other Products |

| Upper GI Tract |

| Small Bowel / Mid GI Tract |

| Lower GI Tract |

| Hospitals / Clinics |

| Ambulatory Surgical Centers |

| Specialized GI Centers |

| Diagnostic Laboratories |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Endoscopic Mechanical Devices | |

| Endoscopic Thermal Devices | ||

| Endoscopic Injection Devices | ||

| Topical Hemostatic Sprays | ||

| Combination Therapy Kits | ||

| Other Products | ||

| By GI Tract Division | Upper GI Tract | |

| Small Bowel / Mid GI Tract | ||

| Lower GI Tract | ||

| By End User | Hospitals / Clinics | |

| Ambulatory Surgical Centers | ||

| Specialized GI Centers | ||

| Diagnostic Laboratories | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the gastrointestinal bleeding treatment market?

The gastrointestinal bleeding treatment market size stands at USD 934.59 million in 2026, with a projected value of USD 1.19 billion by 2031.

Which product category leads the market?

Endoscopic mechanical devices hold the largest share at 44.74% because clinicians rely on clip-based closure across most bleeding scenarios.

Why are ambulatory surgical centers gaining traction?

ASCs grow at a 9.18% CAGR because expanded Medicare coverage and lower facility fees encourage outpatient management of eligible GI bleeds.

Which region is expanding fastest?

Asia-Pacific records the highest CAGR of 8.49% due to healthcare infrastructure upgrades and rising elderly populations requiring anticoagulant therapy.

How are AI tools influencing treatment pathways?

EHR-linked algorithms predict bleeding risk up to a day earlier, permitting earlier endoscopy scheduling and improving outcomes while optimizing resource use.

Page last updated on: