Global Laboratory Centrifuge Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

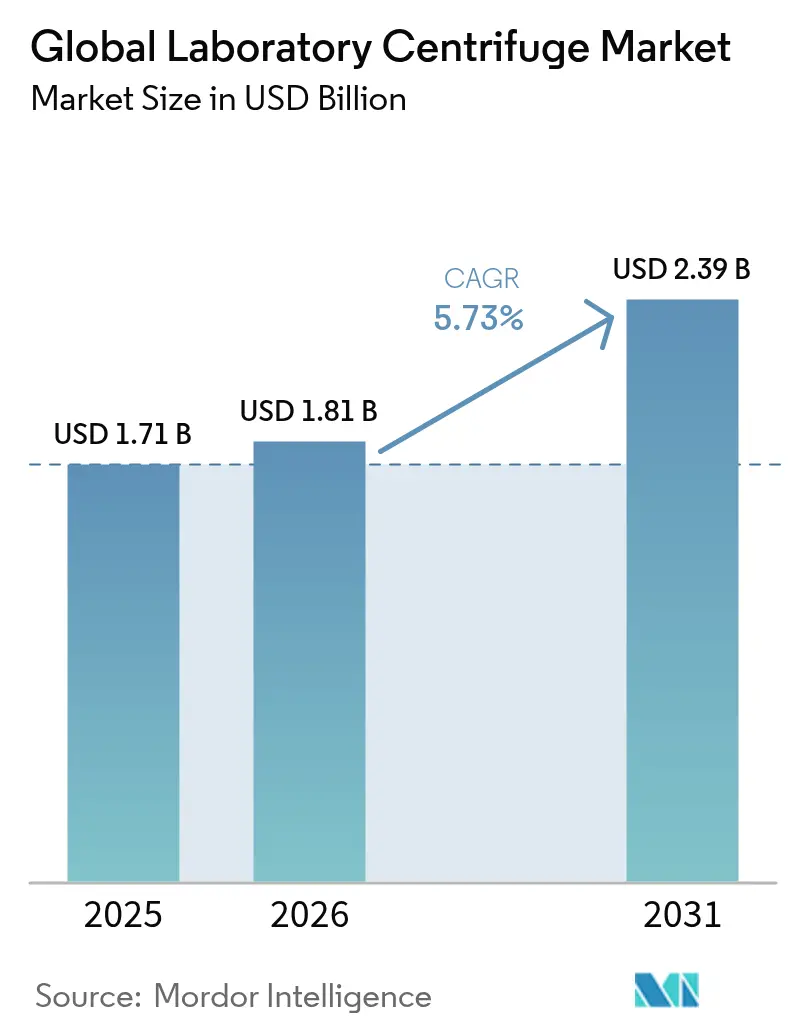

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

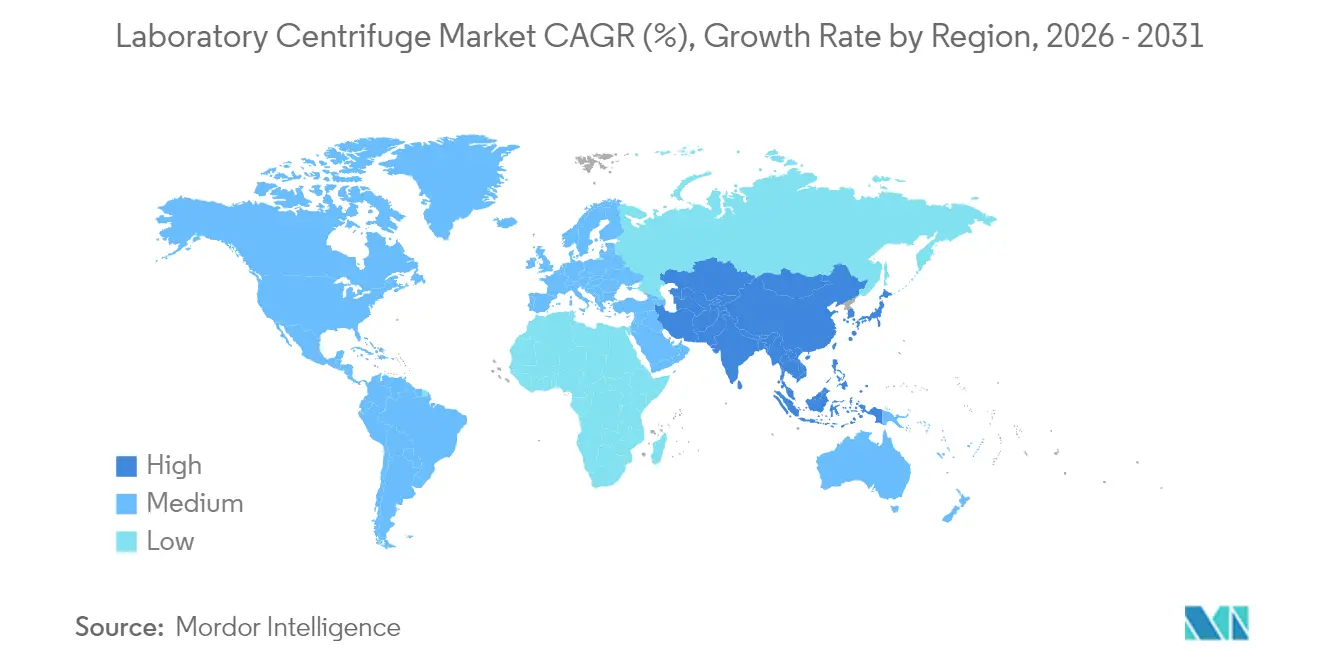

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

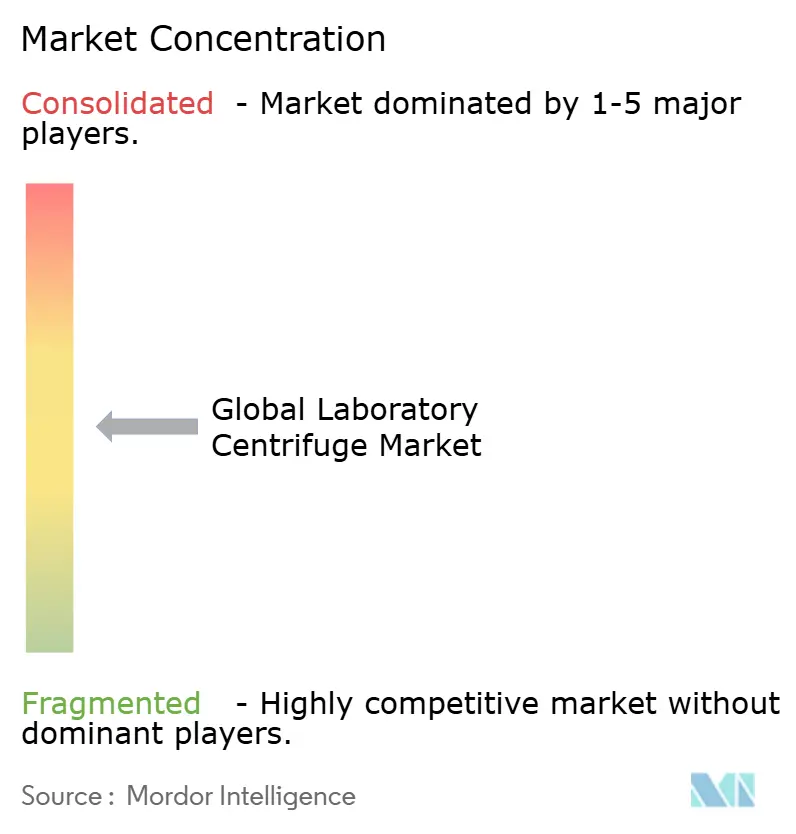

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Laboratory Centrifuge Market Analysis by Mordor Intelligence

The laboratory centrifuge market size was valued at USD 1.71 billion in 2025 and estimated to grow from USD 1.81 billion in 2026 to reach USD 2.39 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031). Vigorous demand from cell and gene therapy manufacturing, recovery in bioprocessing activity, and the push to automate diagnostic workflows anchor this expansion. Players enlarge capacity for viral-vector purification and integrate robotics to reduce manual touchpoints, while sustainability mandates spur adoption of energy-efficient refrigerated systems. North America holds the largest revenue base, yet Asia-Pacific logs the quickest gains as China and India channel public policy and capital into domestic medical-device production. These factors together reinforce the strategic relevance of the laboratory centrifuge market across precision medicine, academic research, and decentralized testing networks.

Key Report Takeaways

- By product type, equipment commanded 76.12% revenue share of the laboratory centrifuge market in 2025; accessories are forecast to post a 7.04% CAGR through 2031.

- By model type, benchtop systems led with 61.30% share in 2025, whereas floor-standing units are set to grow at 6.49% CAGR to 2031.

- By intended use, clinical applications accounted for 52.25% of the laboratory centrifuge market share in 2025, while pre-clinical research is projected to expand at a 6.28% CAGR.

- By application, diagnostics held 36.90% of revenue in 2025; cellomics is expected to record the highest 7.29% CAGR through 2031.

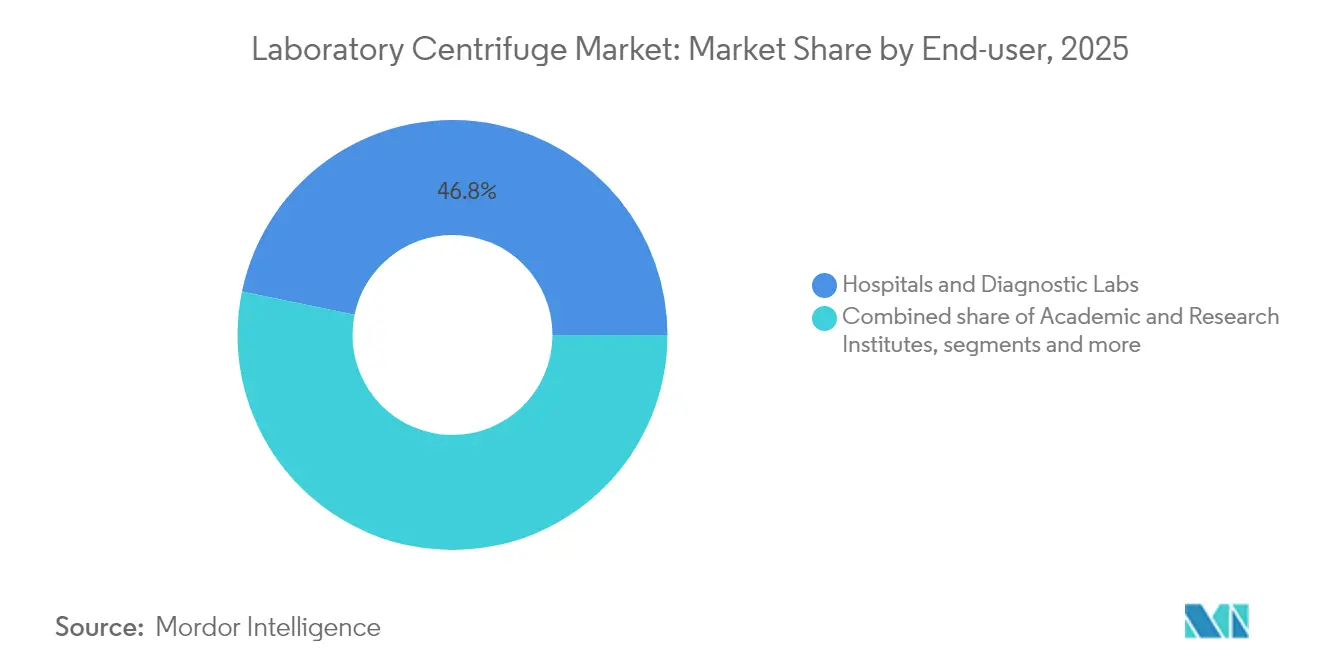

- By end-user, hospitals and diagnostic labs captured 46.75% of 2025 revenue, but biotech and pharma companies are poised for a 6.8% CAGR.

- By geography, North America led with 36.10% share in 2025, while Asia-Pacific is forecast to accelerate at a 7.68% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laboratory Centrifuge Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of chronic & infectious diseases | +1.2% | Global; highest concentration in aging populations of North America & Europe | Medium term (2-4 years) |

| Rising R&D spending in biopharma & life sciences | +1.5% | North America & Europe core; expanding to APAC | Long term (≥ 4 years) |

| Technological advances in high-throughput & refrigerated systems | +0.9% | Global; early adoption in developed markets | Short term (≤ 2 years) |

| Expansion of decentralised/near-patient diagnostic labs | +0.8% | APAC core; spill-over to MEA and Latin America | Medium term (2-4 years) |

| Viral-vector demand for cell & gene therapy manufacturing | +1.1% | North America & EU; expanding to APAC manufacturing hubs | Long term (≥ 4 years) |

| Rotor-refurbishment & circular-economy revenue streams | +0.4% | Global; emphasis on cost-conscious emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Chronic & Infectious Diseases

Diagnostic laboratories rely on centrifugation to separate plasma and isolate pathogens for biomarkers that guide diabetes, cardiovascular, and cancer management. Safety-bucket designs now meet WHO tuberculosis protocols that call for sealed operation to reduce aerosol risk. Aging populations in the United States and Western Europe keep specimen volumes high, while novel infection outbreaks spur health systems to deploy portable centrifuges in frontline clinics. These conditions collectively maintain baseline demand across the laboratory centrifuge market.

Rising R&D Spending in Biopharma & Life Sciences

Drug-discovery programs adopt advanced separation workflows for protein purification, extracellular-vesicle isolation, and viral-vector production. The EVics system shows how tandem tangential-flow filtration overcomes legacy ultracentrifuge bottlenecks by processing up to 1 L while preserving biomolecule integrity. Contract research organizations equip new automated platforms to keep pace with sponsor projects, further expanding the laboratory centrifuge market.

Technological Advances in High-Throughput & Refrigerated Systems

Manufacturers prioritize energy savings, rotor durability, and run-time reductions. Beckman Coulter’s OptiMATE Gradient Maker cuts purification cycles by 75% for viral-vector workflows. Carbon-fiber rotors lighten load weight and curb power draw, meeting institutional sustainability metrics. Programmable refrigeration safeguards thermolabile samples and links to laboratory information systems, embedding modern centrifuges inside broader automation ecosystems.

Viral-Vector Demand for Cell & Gene Therapy Manufacturing

Thermo Fisher’s CTS Rotea counter-flow system recovers more than 95% of target cells at volumes up to 20 L, underscoring how continuous-flow centrifugation resolves commercial-scale vector needs. Single-use designs eliminate cross-contamination between lots, trimming cleaning validation costs in GMP settings. With over 2,000 cell and gene therapy trials now under way, viral-vector purification remains a growth pillar of the laboratory centrifuge market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capital cost of advanced systems | -0.7% | Global; greater impact in emerging markets | Short term (≤ 2 years) |

| Long equipment lifespans slowing replacement sales | -0.5% | Developed markets with established laboratory infrastructure | Long term (≥ 4 years) |

| Growth of outsourced centrifugation services | -0.3% | North America & Europe; expanding to APAC | Medium term (2-4 years) |

| Tightening biosafety & noise-emission regulations | -0.4% | Global; stricter enforcement in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Cost of Advanced Systems

Fully-equipped ultracentrifuges often exceed USD 100,000, restricting adoption by small laboratories. A USD 2 billion global secondary-equipment channel now supplies refurbished units with vendor warranties, offering affordable entry points. Leasing and rental plans further spread out expenditure, yet budget constraints persist, especially in Latin America and parts of Southeast Asia.

Tightening Biosafety & Noise-Emission Regulations

The United States imposed export controls on select centrifuges in January 2025, reflecting dual-use concerns.[1]Bureau of Industry and Security, “Controls on Certain Laboratory Equipment and Related Technology To Address Dual Use Concerns About Biotechnology,” federalregister.gov OSHA and CDC guidelines specify containment cups and sound-pressure limits that elevate compliance costs. Vendors now add automated lid interlocks, aerosol-tight seals, and acoustic insulation, but higher safety specifications raise list prices and lengthen procurement cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Equipment Dominance Drives Accessories Innovation

Equipment represented 76.12% of 2025 revenue, confirming users’ primary focus on platform procurement within the laboratory centrifuge market. Ultracentrifuges reach speeds above 100,000 rpm, supporting protein and virus separation for biologics research. Microcentrifuges remain staples of routine assays, while multipurpose units cater to institutions needing rotor flexibility. The laboratory centrifuge market size for accessories is smaller but displays faster momentum as laboratories replace tubes, bottles, and rotor seals after repeated sterilization cycles. Carbon-fiber rotors, lighter yet corrosion-resistant, now enter service contracts that guarantee load balancing and fatigue inspection.

The accessories segment grows at 7.04% CAGR because consumables are replaced more frequently than hardware. Fixed-angle and swinging-bucket formats account for most aftermarket demand, backed by vendor programs that bundle rotor upgrades with calibration services. As high-throughput screens expand, laboratories secure bulk lots of single-use tubes to avoid cross-contamination. Manufacturers thus bank on recurring sales that complement initial hardware margins, reinforcing the resilience of the laboratory centrifuge market.

By Model Type: Benchtop Systems Balance Performance and Space Efficiency

Benchtop units held 61.30% revenue in 2025, favored for daily diagnostic and academic protocols that handle volumes under 500 mL. Their compact footprint aligns with space-limited benches, and recent firmware updates add touch-screen controls plus QR-code maintenance logs. In contrast, floor-standing models realise a 6.49% CAGR by accommodating bags and bottles needed for upstream bioprocess harvests. Programmable ramps and vibration dampers meet GMP validation rules, which lifts their appeal for contract manufacturers.

The laboratory centrifuge market benefits as institutions deploy mixed fleets: benchtops for stat tests, floor units for batch purification. Integration with robotic arms enables unmanned loading, turning traditional floor systems into automated work cells. Vendors now offer hybrid service plans that remotely track rotor cycles across both model lines, minimising downtime while retaining operator familiarity.

By Intended Use: Clinical Applications Drive Volume While Research Accelerates Innovation

Clinical laboratories generated 52.25% of revenue in 2025, highlighting centrifugation’s irreplaceable role in blood‐chemistry, coagulation, and urinalysis workflows. Hospitals value resilient designs, redundant safety locks, and global service coverage. Conversely, the pre-clinical research segment’s 6.28% CAGR shows how biotech start-ups and academia seek higher g-force ranges and programmable gradients to explore novel biomarkers.

These divergent needs push suppliers to maintain dual product lines. Research models add data export and temperature mapping, while clinical versions emphasise cycle repeatability under strict accreditation. Both segments underpin the broader laboratory centrifuge market by committing to recurring rotor inspection contracts that protect accreditation status.

By Application: Diagnostics Leadership Faces Cellomics Challenge

Diagnostics held 36.90% of 2025 revenue, cementing its status as the laboratory centrifuge market cornerstone. Typical protocols include plasma separation for metabolic panels and pathogen pelleting for PCR. Cellomics now grows at 7.29% CAGR because single-cell analytics and CAR-T workflow steps need gentle yet precise spin profiles.

Proteomics and genomics groups modernise ultracentrifuges to enrich organelles and nucleic acids before mass spectrometry or sequencing. Meanwhile, microbiology labs depend on sealed-bucket designs to avoid aerosol exposure. Each application tier extends the serviceable base for calibration and rotor balancing, ensuring consistent expansion of the laboratory centrifuge market.

By End-user: Hospitals Lead While Biotech Accelerates

Hospitals and diagnostic labs owned 46.75% of revenue in 2025, reflecting frequent sample turnover and compliance-driven purchasing cycles. They value warranties that cover weekend callouts and guaranteed spare-part stocks. Biotech and pharma companies grow 6.8% CAGR as gene-therapy pipelines scale, demanding single-use, closed-system centrifuges.

Academic consortia invest in shared core facilities, enabling smaller labs to access ultracentrifugation without full ownership, which broadens the reach of the laboratory centrifuge market. Contract research organisations purchase robotic-ready models to speed client screening campaigns, creating a lively secondary rental channel for midlife units.

By Automation Level: Manual Systems Persist Despite Automation Momentum

Manual and conventional designs constituted 39.70% of 2025 revenue as many clinics still trust hand-loaded spinning for CBC routines. These devices offer intuitive knobs, minimal sensors, and low maintenance costs that suit budget-restricted sites. Fully automated systems, however, rise at 7.18% CAGR as robotics address staffing shortages and reproducibility targets.

ABB and Mettler-Toledo integrate pick-and-place arms that feed racks directly into refrigerated chambers. Vendors also link centrifuge cycle data to laboratory information management systems, supporting electronic audit trails vital for GMP. The layering of AI-based predictive maintenance nudges the laboratory centrifuge market toward service-oriented revenue models.

Geography Analysis

North America retained 36.10% of 2025 revenue, anchored by the United States’ dense cluster of pharmaceutical headquarters, National Institutes of Health grants, and a robust contract manufacturing base. Canada complements with public health labs and a growing biologics ecosystem, while Mexico benefits from near-shoring of medical-device assembly. Federal incentives for advanced manufacturing further stimulate orders for GMP-graded centrifuges that feed into local cell-therapy plants. Laboratories also respond to OSHA and CDC safety directives, prompting upgrades to aerosol-tight lids and acoustic dampening, which sustains the laboratory centrifuge market.

Asia-Pacific posts the fastest 7.68% CAGR. China’s medical-equipment sector reached USD 179 billion in 2024, featuring 138,000 device patents, and state policy favours domestic sourcing.India’s National Medical Devices Policy targets USD 50 billion turnover by 2030 and simplifies regulatory pathways, encouraging multinational and local firms to invest in centrifuge assembly lines. Japan, South Korea, and Australia expand clinical-trial networks that demand high-throughput centrifugation, reinforcing the laboratory centrifuge market across the region.

Europe shows steady growth paced by Germany’s export-oriented device makers, the United Kingdom’s biotech clusters, and France’s hospital modernisation programs. EU directives on eco-design and medical-device regulation encourage adoption of energy-efficient rotors and comprehensive validation records. Sustainability-focused hospitals favor models with 70% lower power draw, aligning procurement with green public-purchasing policies. Collectively, these initiatives keep European demand consistent while opening niches for circular-economy refurbishment services that extend the lifecycle of centrifuge fleets.

Competitive Landscape

Market consolidation remains moderate as leading firms pursue scale in bioprocess purification. Thermo Fisher Scientific will acquire Solventum’s Purification & Filtration unit for USD 4.1 billion, expecting USD 125 million operating synergies by year five.[3]Thermo Fisher Scientific, “Thermo Fisher Scientific to Acquire Solventum's Purification and Filtration Business,” ir.thermofisher.com This transaction broadens Thermo Fisher’s one-stop offering from cell harvest to downstream filtration, bolstering its grip on the laboratory centrifuge market. Beckman Coulter, Eppendorf, and Danaher’s Cytiva division defend share via incremental rotor upgrades and cloud-connected service dashboards.

Automation partnerships reshape competitive positioning. BD teamed with Biosero to mesh flow-cytometer queues with robotic load-unload sequences, demonstrating the appeal of integrated workflows over stand-alone instruments. ABB’s collaboration with Mettler-Toledo on flexible lab cells places industrial robotics inside academic laboratories, pressuring traditional centrifuge makers to supply robot-friendly lids and plate carriers. New entrants concentrate on portable, battery-powered devices for field diagnostics, serving humanitarian missions and veterinary clinics.

Differentiation hinges on after-sales coverage, compliance documentation, and sustainability features. Vendors promote rotor-exchange programs, traceable maintenance logs, and software updates that unlock new acceleration profiles without hardware swaps. Those capabilities shape purchasing criteria for high-value accounts, ensuring that service depth, not only catalog breadth, steers share within the laboratory centrifuge market.

Global Laboratory Centrifuge Industry Leaders

Thermo Fisher Scientific Inc

Andreas Hettich GmbH & Co. KG

HERMLE Labortechnik GmbH

Danaher Corporation (Beckman Coulter, Inc.)

Qiagen NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Beckman Coulter Life Sciences introduced the OptiMATE Gradient Maker, an automated density-gradient instrument that reduces ultracentrifuge preparation time by 75%.

- April 2025: Thermo Fisher Scientific reported Q1 2025 revenue of USD 10.36 billion and unveiled the Cryofuge refrigerated floor models targeting precision medicine laboratories.

- February 2025: Thermo Fisher Scientific agreed to purchase Solventum’s Purification & Filtration business for USD 4.1 billion to expand bioproduction capabilities.

- June 2024: Beckman Coulter launched the Biomek Echo One System, integrating acoustic liquid handling for faster NGS library prep.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the laboratory centrifuge market as the sale of benchtop or floor-standing equipment, together with essential rotors, tubes, and buckets, that use centrifugal force to separate biological or chemical samples for research, diagnostic, or bioprocess tasks.

Scope exclusion: industrial or large-capacity process centrifuges employed in wastewater, mining, or food plants sit outside this definition.

Segmentation Overview

- By Product Type

- Equipment

- Microcentrifuges

- Ultracentrifuges

- Multipurpose/General-purpose

- Accessories

- Tubes & Bottles

- Rotors (fixed-angle, swinging-bucket)

- Buckets/Plates/Consumables

- Equipment

- By Model Type

- Benchtop

- Floor-standing

- By Intended Use

- Clinical

- Pre-clinical/Research

- General Purpose

- By Application

- Microbiology

- Cellomics

- Proteomics

- Genomics

- Diagnostics

- By End-user

- Hospitals & Diagnostic Labs

- Academic & Research Institutes

- Biotech & Pharma Companies

- Contract Testing / CROs

- By Automation Level

- Manual / Conventional

- Semi-automated

- Fully-automated / Robotic

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and pulse surveys with biomedical engineers, lab managers, procurement leads, and regional dealers across North America, Europe, and key Asia-Pacific hubs help refine utilization rates, replacement cycles, and automation preferences, filling gaps left by desk work before final triangulation.

Desk Research

We start by mapping published import-export codes, device listings, and price files from regulators and customs portals such as the U.S. FDA 510(k) database, Eurostat's Comext, and India's DGFT. Trade association yearbooks (IVD, Bio-process International) and health-budget trackers from the WHO and OECD add shipment counts, installed base hints, and test-volume ratios for hospitals and reference labs.

To convert volumes to value, our analysts pull indicative average selling prices from manufacturer SEC filings, D&B Hoovers snapshots, and distributor web catalogs, then validate currency and inflation using World Bank and IMF series. Paid troves, Dow Jones Factiva for announcement frequency and Questel for rotor-design patent velocity, flag technology adoption curves. The sources above are illustrative; several additional datasets were reviewed for completeness and cross-checks.

Market-Sizing & Forecasting

We anchor the global baseline through a top-down test-volume pool that scales hospital diagnostics, academic R&D funding, and biopharma bioprocess batches, which are then benchmarked against sampled ASP × unit shipments from supplier roll-ups. Key model variables include: (1) installed bench-top units per population, (2) average daily sample runs in Tier-II hospitals, (3) NIH-style life-science grant outlays, (4) bioreactor capacity additions, and (5) capital-equipment replacement intervals. A multivariate regression with lagged health-expenditure and R&D-spend predictors extends the series, while bottom-up supplier checks adjust for gray-market leakages.

Data Validation & Update Cycle

Outputs go through variance screens against import data, corporate earnings, and peer models; anomalies trigger re-contact of sources. Two analysts and a research manager sign off, and the workbook refreshes annually, with interim updates for material recalls or step-change technology launches.

Why Mordor's Laboratory Centrifuge Baseline Earns Trust

Published numbers often diverge because firms pick different device mixes, price ladders, and refresh cadences.

In our review, gaps stem mainly from whether accessories are bundled, how benchtop ASP erosion is treated, and the rigor of primary cross-checks; some studies also apply one-size growth rates from broader lab-equipment baskets, while Mordor refines variables to centrifuge-specific drivers and updates figures yearly.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.71 bn (2025) | Mordor Intelligence | - |

| USD 1.82 bn (2024) | Global Consultancy A | bundles centrifuge accessories under wider lab-equipment multipliers |

| USD 2.06 bn (2024) | Trade Journal B | applies uniform ASPs and five-year refresh cycle, limited primary validation |

The table shows how scope and assumption choices swing totals by up to half a billion dollars. By isolating true centrifuge revenue drivers and refreshing inputs every twelve months, Mordor delivers a balanced, reproducible baseline decision-makers can rely on.

Key Questions Answered in the Report

What is the current value of the laboratory centrifuge market?

The market is valued at USD 1.81 billion in 2026 and is forecast to reach USD 2.39 billion by 2031.

Which region is growing the fastest in the laboratory centrifuge market?

Asia-Pacific records the highest 7.68% CAGR to 2031 thanks to large-scale healthcare investments in China and India.

Why are accessories growing quicker than equipment?

Tubes, rotors, and seals are consumables that need regular replacement, pushing accessories to a 7.04% CAGR while equipment fleets last many years.

How is automation influencing centrifuge purchases?

Fully automated systems are expanding at 7.18% CAGR as laboratories address staff shortages and demand reproducible results with minimal manual handling.

Which application segment offers the best growth opportunity?

Cellomics leads with a 7.29% CAGR, driven by single-cell analysis and cell-therapy workflows that require gentle yet precise centrifugation.

Page last updated on: