Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

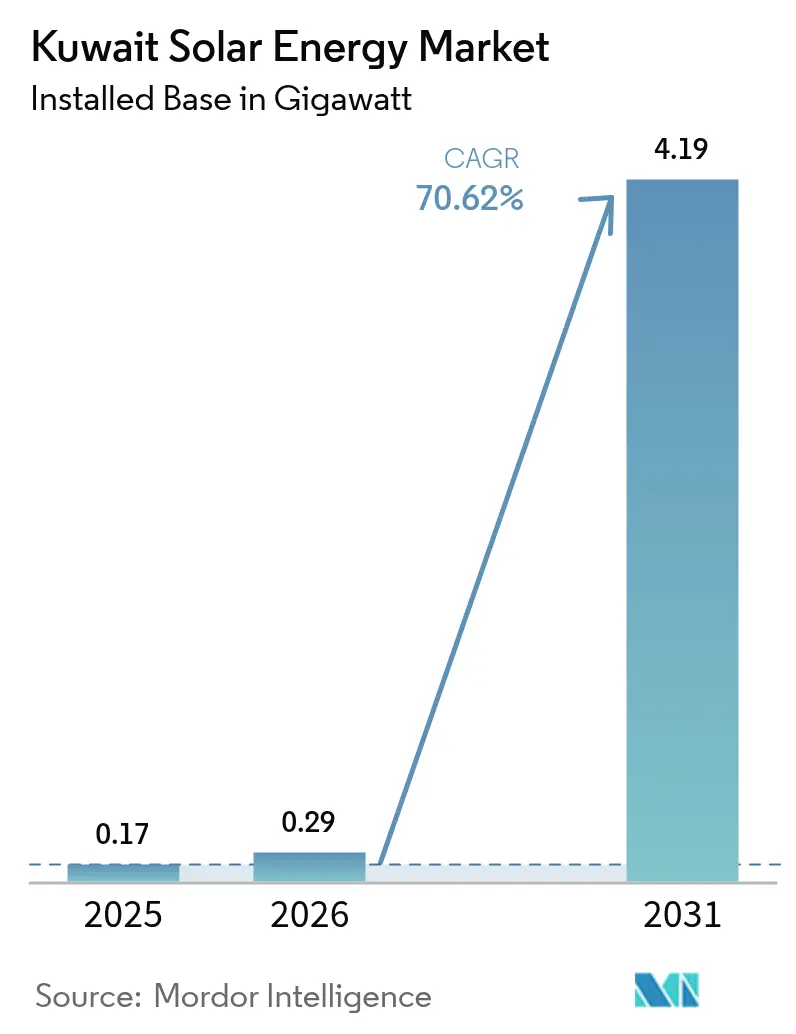

| Base Year Market Size (2025) | 0.17 gigawatt |

| Market Volume (2026) | 0.29 gigawatt |

| Market Volume (2031) | 4.19 gigawatt |

| Growth Rate (2026 - 2031) | 70.62% CAGR |

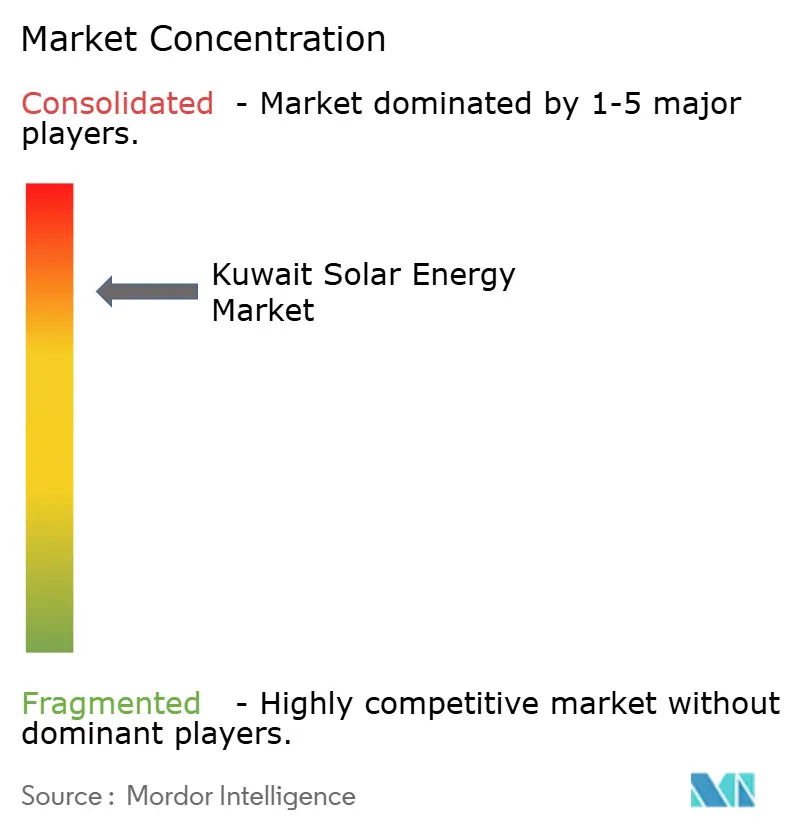

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait Solar Energy Market Analysis by Mordor Intelligence

Kuwait Solar Energy Market size in 2026 is estimated at 0.29 gigawatt, growing from 2025 value of 0.17 gigawatt with 2031 projections showing 4.19 gigawatt, growing at 70.62% CAGR over 2026-2031.

Momentum comes from a policy push to curb Kuwait’s 870 gCO₂/kWh emission intensity, a figure that far exceeds the 2021 global average of 573 gCO₂/kWh.[1]Energies Journal, “Solar-Powered Cellular Base Stations in Kuwait,” mdpi.com The Al-Shagaya renewable complex, now planned at 4,800 MW, will supply roughly 26-27% of national capacity once first‐phase commissioning starts in 2028. Record-low PV module prices have pushed expected winning tariffs toward the sub-USD 25/MWh range, further improving project economics. Yet ultra-low retail power tariffs of about 0.7 cents/kWh distort distributed-generation payback, leaving grid-scale PPAs as the dominant business model.[2]Oxford Institute for Energy Studies, “Kuwait Energy Subsidies and Tariff Reform,” oxfordenergy.org Grid reliability needs are equally forceful; peak demand in August 2023 sat within 5% of installed capacity, prompting a 500 MW emergency import request and accelerated solar procurements.

Key Report Takeaways

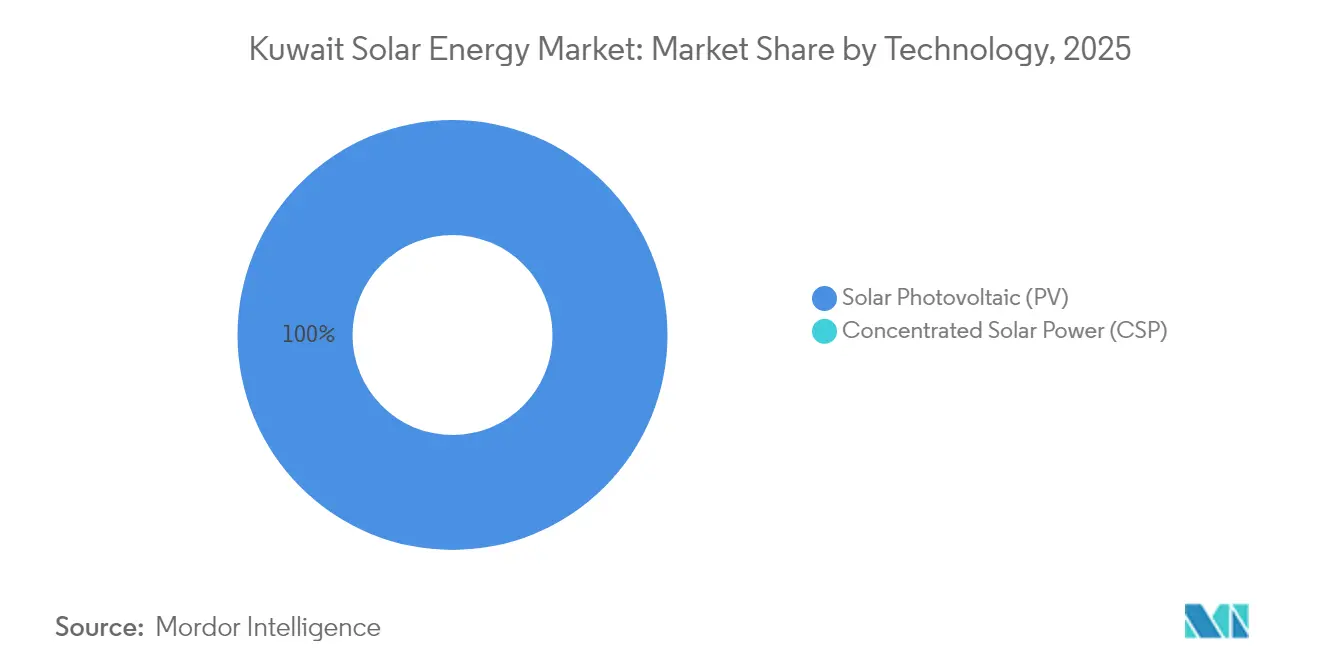

- By technology, solar photovoltaic held 100.00% of the Kuwait solar energy market share in 2025, while the segment is forecast to sustain a 70.62% CAGR through 2031.

- By grid type, on-grid installations accounted for 80.35% of the Kuwait solar energy market size in 2025; off-grid systems are advancing at an 78.25% CAGR to 2031.

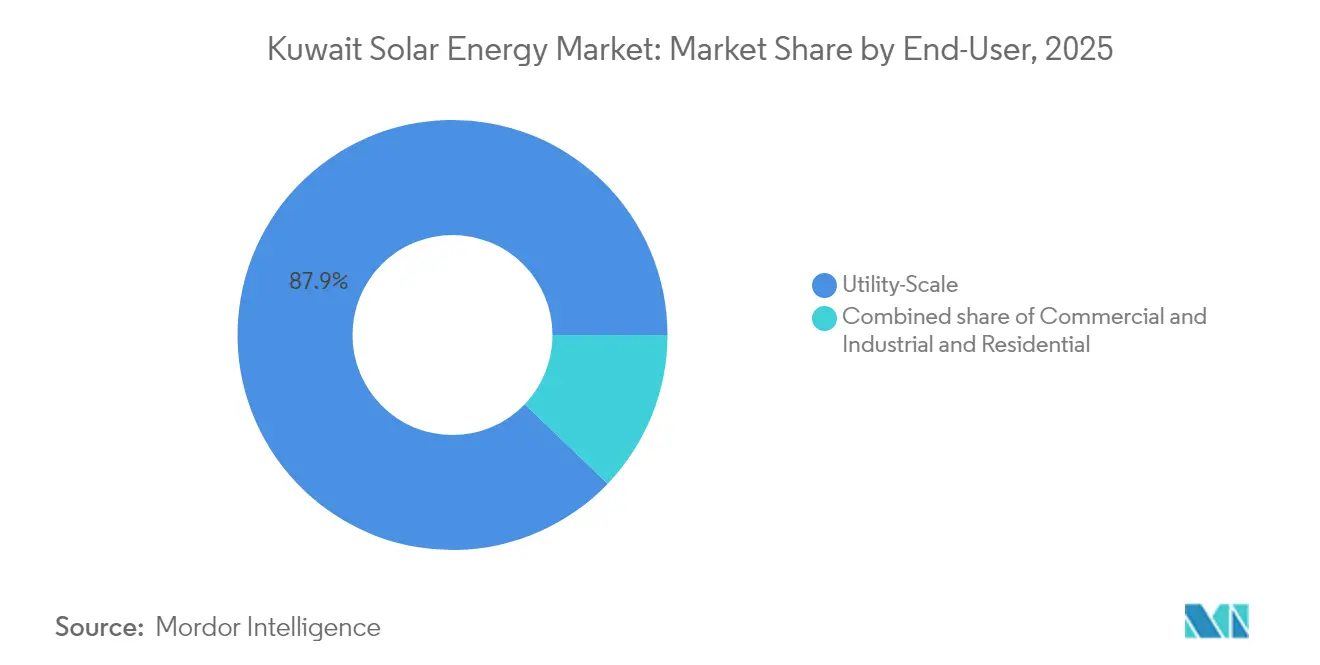

- By end-user, utility-scale projects led with 87.85% of the Kuwait solar energy market share in 2025; residential capacity is projected to grow fastest at 80.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kuwait Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-high DNI & GHI enable world-class yields | +12.5% | Western desert zones (Shagaya, Al-Dibdibah) | Medium term (2-4 years) |

| National 15% renewables-by-2030 target | +18.0% | National, focused in Jahra Governorate | Short term (≤ 2 years) |

| Record PV price declines | +10.2% | National, with regional benchmarking influence | Short term (≤ 2 years) |

| Peak-summer blackouts | +14.8% | Urban load centers (Kuwait City, Ahmadi, Hawalli) | Short term (≤ 2 years) |

| Solar steam for oil-field EOR | +6.3% | Northern and western oil fields | Long term (≥ 4 years) |

| Mandatory solar-ready building code | +4.5% | National, early uptake in public facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-High DNI & GHI Enable World-Class Solar Yields

Kuwait records 1,900-2,100 kWh/m²/year of global horizontal irradiance and near-cloudless skies for nine months each year, placing the country in the top decile for photovoltaic performance. IEA-PVPS findings show bifacial modules on single-axis trackers can lift energy yield by 35% and cut levelized cost by 16% in Kuwait’s high-albedo deserts.[3] International Energy Agency PVPS, “Bifacial Photovoltaic Systems,” iea-pvps.org Phase III of the Shagaya complex is expected to realize capacity factors above 25% thanks to these conditions. Dust deposition of 216-339 t/km²/year can, however, slash output by up to 48% after 6 g/m² buildup, pushing operators toward robotic dry-cleaning and anti-soiling coatings. These mitigation measures raise O&M costs by roughly 15-20% compared with less arid sites.[4]Kuwait Institute for Scientific Research, “Grid Integration Studies,” kisr.edu.kw

National 15% Renewables-by-2030 Target & Shagaya Program

The government’s 22,100 MW renewables target, equal to 15% of forecast demand, frames near-term growth. An RFP for 1,100 MW in Shagaya Phase III Zone 1 was issued in June 2025, with bids due in September 2025 and a 30-year PPA that strengthens bankability. Prequalification for an additional 500 MW Zone 2 followed in May 2025, underscoring a phased rollout. Negotiations underway to develop Phases 4-5 totaling 3,400 MW suggest Shagaya will exceed the interim 2 GW milestone. Compliance with IEC 62109-1:2021 and IEC 62446-1:2021 reduces lender risk and aligns Kuwait with international standards.

Record PV Price Declines Drive Sub-USD 25/MWh Tariffs

PV module costs fell below USD 0.10/W in 2024, paving the way for bids in the low-USD 20/MWh range in regional tenders that Kuwait aims to emulate. EY and DNV were hired to advise on the 1,100 MW tender, signaling rigorous due diligence requirements. Yet a subsidized retail tariff of 0.7 cents/kWh leaves utility PPAs 35-40 times pricier than household electricity, stalling rooftop adoption. This dual-price environment entrenches sovereign guarantees as the linchpin of the Kuwait solar energy market. Distributed segments, therefore, remain contingent on subsidy reform or net-metering incentives.

Peak-Summer Blackouts Force Fast-Track Capacity Additions

Peak demand in August 2023 nearly matched installed capacity, forcing a 500 MW import arrangement through the GCC Interconnection Authority. Solar production coincides with midday air-conditioning loads, offering a natural hedge against such stress. KISR modeling indicates that integrating 15% variable renewables requires battery storage sized for 70% peak shaving and 30% smoothing at a 3.5-hour window. Although storage is not mandated, the 30-year PPA allows hybrid solutions to evolve as penetration rises. The Shagaya Phase III timeline reflects this urgency, with COD targeted for 2027-2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-low retail power tariff subsidies | −8.7% | National, most acute in small-scale segments | Medium term (2-4 years) |

| Fragmented oversight delays tenders | −5.2% | National, affects all utility-scale procurement | Short term (≤ 2 years) |

| Dust & soiling losses raise water demand | −3.8% | Western and northern desert zones | Long term (≥ 4 years) |

| Remote-site grid bottlenecks in northern desert | −2.9% | Oil-field districts and far-western Shagaya areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-Low Retail Power Tariff Subsidies Distort Economics

Residential tariffs averaging 0.7 cents/kWh undercut even the cheapest solar PPA by roughly fortyfold, erasing payback for rooftop systems. Government subsidy outlays approach USD 5-7 billion per year, complicating fiscal sustainability. Multilateral lenders recommend phased tariff hikes toward 3 cents/kWh to unlock self-consumption models, but political consensus remains elusive. A 2024 building-energy study confirmed that net-zero-energy commercial designs are not viable under current prices. Consequently, the residential segment’s forecast 83.6% CAGR will depend on regulatory mandates such as the 2019 solar-ready code rather than market payback.

Fragmented Oversight Delays Tenders

Renewable governance is split between MEWRE, KAPP, and KISR, often adding 12-18 months to tender cycles compared with neighboring GCC markets. Shagaya Phase III illustrates the lag: conceived in 2022, prequalified in early 2024, and tendered only in June 2025. While KAPP now leads procurement, the absence of a unified renewables commission means grid codes, net-metering, and REC frameworks remain patchy. Developers thus navigate uncertain inverter ride-through and reactive-power rules, elevating project risk. Direct bilateral partnerships, such as the planned 3,400 MW Chinese-backed Shagaya Phases 4-5, could bypass competitive PPP channels and fragment oversight further.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominates, CSP Sidelined

Solar photovoltaic commanded 100% of the Kuwait solar energy market in 2025, a lead set to persist with a 70.62% CAGR through 2031. The Kuwait solar energy market size for PV is projected to climb from 170 MW to 4,190 MW across the forecast horizon, while CSP remains absent from current procurement. Bifacial modules and single-axis trackers, now standard for desert sites, boost yields by 35% and cut costs by 16%. The 50 MW legacy CSP unit at Shagaya offered valuable operational data but highlighted water-intensive cooling drawbacks in an arid climate.

Developers shortlisted for the 1,100 MW tender, ACWA Power, Masdar, TotalEnergies, EDF Renewables, Jinko Power, and Trung Nam, collectively operate more than 30 GW of PV yet little CSP, underscoring technology preference. Huawei’s SUN2000 inverters already comply with the KUWAIT_MV800 grid code, ensuring faster commissioning for PV projects. Battery storage, favored over molten-salt thermal storage, aligns with KISR’s optimal 3.5-hour window and supports evening ramp requirements.

By Grid Type: Utility Anchors, Off-Grid Surges

On-grid systems held 80.35% share in 2025, reflecting sovereign-backed PPAs that underpin most capacity. Off-grid projects, however, are set to match utility-scale growth with an 78.25% CAGR, driven by oil-field electrification and telecom applications. Kuwait Oil Company’s plan to integrate 17 GW of renewables for enhanced oil recovery illustrates the off-grid potential.

Transmission remains a chokepoint: a new 400 kV line linking Shagaya to Al-Sulaibiya will be fully subscribed by the first 1,100 MW tranche, prompting urgent reinforcement needs. Off-grid solutions bypass these constraints; JCE Energy’s 2024 solar-powered chemical-injection units eliminated diesel and cut maintenance cycles from weekly to quarterly. Portable-cabin studies further show 24.1% reductions in cooling electricity use when PV is integrated.

By End-User: Utility Leads, Residential Awakens

Utility-scale capacity represented 87.85% of the Kuwait solar energy market in 2025, anchored by the Shagaya complex’s bankable PPA framework. Residential installations, though tiny today, are forecast to race ahead at 80.15% CAGR thanks to the 2019 solar-ready building code and emerging net-metering pilots. The Kuwait solar energy market size attributed to rooftop systems is thus expected to rise sharply, but will still trail utility-scale totals until tariff reform narrows cost gaps.

Commercial and industrial uptake lags due to the 0.7 cents/kWh tariff, yet leases such as the 2024 TotalEnergies–Al Masaood deal hint at third-party ownership pathways. KISR’s rooftop PV-plus-battery modeling shows achievable payback once tariffs climb above 3 cents/kWh, reinforcing the role of subsidy reform. Kuwait Oil Company’s 1 GW renewable-to-hydrogen initiative aligns with this trajectory by channeling solar toward industrial decarbonization rather than grid displacement.

Geography Analysis

Utility-scale deployment clusters in Jahra Governorate’s western desert, where Shagaya’s 2,000-plus kWh/m² irradiance and abundant land create optimal conditions. Dust levels of up to 339 t/km²/year necessitate robotic cleaning, raising O&M budgets by about 20%. A 400 kV overhead line awarded to Larsen & Toubro for KWD 1.45 million (USD 4.7 million) will evacuate power from the first 1,100 MW block, but further grid work is needed for subsequent phases.

Northern oil fields, Raudhatain, Sabriya, and Burgan, form an emerging off-grid cluster as diesel generators give way to solar-battery hybrids. JCE Energy’s solar chemical-injection units prove the technical viability of remote electrification. Yet weak transmission northward means surplus daytime energy cannot easily flow to load centers, underscoring the need for updated grid codes and stability studies.

Urban corridors, Kuwait City, Ahmadi, Hawalli, consume most electricity but offer limited space for ground-mount arrays. Rooftop PV trials have reduced cooling loads in portable structures by 24.1%, demonstrating feasible gains even in dense settings. The Ministry’s pledge to include distributed generation in future procurements hints at dedicated mechanisms for urban participation.

Regulatory Landscape

Kuwait does not have an independent power-sector regulator. The Ministry of Electricity, Water and Renewable Energy (MEWRE) combines policymaking, grid-connection oversight, and technical standards-setting, while the Kuwait Authority for Partnership Projects (KAPP) structures and runs IPP/PPP procurements for utility-scale solar projects such as Shagaya Phase III (1,100 MW Zone 1 under a long-tenor PPA framework). Renewable projects also operate within Kuwait's PPP and power-project company frameworks, including Law No. 39 of 2010 for establishing joint-stock companies for power and desalination, which influences ownership, tendering, and offtake arrangements.

For compliance, developers and EPCs must meet MEWRE electrical installation regulations and specifications (including MEW/R-1 and MEW/S-1), along with on-grid interconnection guidelines for rooftop PV where applicable. Environmental permitting remains a gating item at the project level, with Environmental Impact Assessments required by the Public Authority for Environment. Recent legal and policy direction has also opened a route for oil-sector entities to build solar plants to meet internal demand, reinforcing parallel demand from industrial self-generation alongside the dominant MEWRE-backed PPA model.

Competitive Landscape

Six shortlisted consortia, led by ACWA Power, Masdar, TotalEnergies, EDF Renewables, Jinko Power, and Trung Nam, dominate current tenders, indicating moderate concentration. ACWA Power alone brings 12 GW of regional solar, while Masdar’s 20 GW portfolio signals deep GCC expertise. EY’s role as financial adviser and DNV’s technical oversight aim to preserve competitive tension and enforce bankability.

Future market structure may shift if the 3,400 MW Chinese partnership for Shagaya Phases 4-5 proceeds outside KAPP’s PPP framework, potentially limiting access for non-Chinese developers. Off-grid niches remain less consolidated, with equipment vendors such as Huawei and integrators like JCE Energy providing modular solutions. The Kuwait solar energy industry is therefore balancing sovereign-backed megaprojects with a fragmented landscape of remote applications.

Kuwait Solar Energy Industry Leaders

Kuwait Institute for Scientific Research (KISR)

Kuwait Oil Company

Alternative Energy Projects Co. (AEPCo)

Kuwait National Petroleum Company

Life Energy Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Utility-scale solar continues to be anchored by the Shagaya Renewable Energy Park program, where Phase III Zones 1 and 2 (1,600 MW combined) support near-term contracting activity under KAPP-led PPP structures and long-tenor PPAs. Enabling infrastructure is also expanding in parallel. In 2026, MEWRE moved to contract major 400 kV overhead line works to evacuate renewable output from Shagaya, including a USD 158.7 million award (Al Shagaya to Al Wafra) and a USD 274.56 million contract (Shagaya transformer station to Subiya Power Station). These grid packages extend the scope beyond generation into substations, transmission lines, and grid-integration services tied to bankable solar buildout.

Industrial self-generation adds to the opportunity set alongside public tenders. State-linked hydrocarbon operators have been advancing internal solar programs, including a Kuwait Petroleum Corporation plan referenced in early 2026 for up to 2 GW of solar for industrial operations. Kuwait National Petroleum Company has also discussed adding battery storage to a solar-powered LPG bottling facility to support round-the-clock operations. This creates demand for behind-the-meter PV, storage, and control systems that reduce reliance on constrained summer grid supply, even as subsidized retail tariffs continue to limit the standalone economics of mass-market rooftop solar without broader incentive design.

Recent Industry Developments

- July 2026: Alternative Energy Projects Company (AEPCo) announced an intention to raise capital, with Kamco Invest and Burgan Bank referenced as managers, to fund expansion of its solar business in Kuwait and the wider MENA region. The plan targets balance-sheet capacity to pursue a larger project pipeline and compete more actively across utility and private-sector segments.

- June 2026: Kuwait National Petroleum Company outlined plans to integrate battery storage at its solar-powered Umm Al-Aish LPG bottling plant to support 24-hour operations without depending on the national grid. The project underscores growing momentum for PV-plus-storage in industrial applications where reliability and operational continuity carry a premium.

- July 2024: Kuwait Oil Company hired KBR to design a long-term roadmap covering renewables and hydrogen, framing a large internal demand pool for off-grid and industrial solar applications. The engagement reinforced the role of oil-field electrification and decarbonization programs as a parallel driver to KAPP-procured grid-scale solar.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the installed solar power capacity in Kuwait, measured in gigawatts, and it covers solar PV and solar thermal where applicable across grid-connected and off-grid projects.

Scope exclusions: We exclude broader renewable power sources (such as wind) and we do not count electricity generation value or power retail revenues as part of this market.

Segmentation Overview

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the Kuwait solar buildout and policy pipeline before any sizing assumptions were set. We reviewed public energy plans and procurement announcements, then cross-checked them with power system statistics to separate what is operating from what is planned.

Common inputs came from sources such as Kuwait government energy publications, IRENA renewable capacity statistics, IEA energy balances, UN Comtrade trade data for solar equipment proxy signals, and peer-reviewed journals that discuss solar performance in desert climates. Company annual reports, investor presentations, and reputable press releases were also referenced, and a paid subscription for company financials and intelligence was used selectively to sanity-check ownership structures and project participation. These examples are not exhaustive, and other public sources were consulted to fill data gaps, validate assumptions, and clarify timelines.

Primary Interviews and Surveys

Primary work focused on validating what is actually getting commissioned in Kuwait and what is delayed, resized, or re-phased. We spoke with a mix of project developers, EPC and O&M participants, equipment channel partners, and large power offtake stakeholders, then aligned responses back to the desk-based project list.

Since Kuwait is a single-country market, the outreach was designed to cover different project types and customer groups rather than regional splits. That structure helped us confirm grid connection status, expected commissioning dates, and typical system configurations used locally.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | |

| Mid tier: 59% | Functional/Unit leaders: 31% | |

| Smaller Players: 16% | Managers: 57% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where national installed-capacity reporting and the published project pipeline were used to reconstruct the demand pool in gigawatts, then each step was adjusted using commissioning evidence and developer feedback. After forming the market total, we added selective bottom-up checks, such as sample project roll-ups by technology type and approximate capacity-by-project type comparisons, to confirm the total stayed realistic.

Key model inputs included awarded and announced project capacities, commissioning and grid-connection timelines, utility-scale versus behind-the-meter mix, PV dominance in current deployments, and the practical pace of land allocation and permitting. Where public sources were silent, gaps were handled by applying conservative delay factors and phased commissioning schedules that were checked through interviews, and then reviewed again during the validation step.

Forecasting used scenario analysis, since the Kuwait solar market is shaped by a limited number of large projects and policy decisions. The scenarios were anchored on expected procurement cadence, typical slippage in commissioning dates, and near-term construction readiness signals shared by respondents.

Data Validation & Update Cycle

Outputs were checked against independent signals such as public capacity totals, known project milestones, and import proxies for major solar components, then variances were investigated before sign-off. If an estimate appeared out of line, we revisited the project list, re-checked unit conversions, and re-contacted sources to confirm whether a project was delayed, resized, or moved to a later phase.

The report is refreshed annually, and interim updates are added when there are material award announcements or schedule changes that can shift the near-term installed base. Before delivery, a final analyst pass is completed so the latest public updates are reflected in the model narrative and numbers.

Mordor Intelligence's Kuwait Solar Energy Market Estimate Compared With Other Published Estimates

Published estimates for Kuwait solar can look far apart because some studies size the market in installed capacity, while others convert the story into USD value using their own cost and revenue assumptions. Differences also show up when one source counts announced projects at full nameplate capacity, but another only counts commissioned capacity.

The table shows the spread clearly, and in Mordor Intelligence's model the market size is expressed as installed solar capacity in GW for the base year. This avoids mixing equipment pricing cycles and power price assumptions into the core market total.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.17 B (2025) | |

| Regional Consultancy A | USD 0.28 B (2024) | Sized in USD value and not in installed GW, so the estimate is influenced by assumed EPC costs, imported equipment pricing, and how services and storage are bundled. |

| Industry Publisher B | USD 0.13 B (2024) | PV-only value framing with a narrower inclusion set, and the base year appears tied to booked project activity rather than the full installed base at year-end. |

Looking across the three figures, most of the gap comes from the unit of measure and what is treated as market value versus physical capacity. When the scope is kept to installed GW and checked against commissioning timelines, the result is easier to trace back to real projects and update when schedules change.

Key Questions Answered in the Report

How fast will installed capacity grow in the Kuwait solar energy market by 2031?

Capacity is expected to surge from 170 MW in 2025 to 4,190 MW by 2031, reflecting a 70.62% CAGR.

What is driving the sharp rise in utility-scale projects?

A 22,100 MW renewables target, peak-summer blackout risk, and record-low PV prices are accelerating tenders such as the 1,100 MW Shagaya Phase III Zone 1 project.

Why are rooftop installations still limited in Kuwait?

Residential tariffs of 0.7 cents/kWh make self-consumption uneconomic, so rooftop growth awaits tariff reform or net-metering incentives.

Which technology dominates the Kuwait solar energy market?

Photovoltaic systems hold 100.00% share, as concentrated solar power is absent from the current procurement pipeline.

Where are most new solar plants being built?

Jahra Governorate’s western desert hosts the 4,800 MW Shagaya complex, benefiting from high irradiance and available land.

How are oil fields using solar energy?

Kuwait Oil Company is piloting off-grid PV-battery systems for chemical injection and enhanced oil recovery, reducing diesel use and emissions.

Page last updated on: