KSA OOH And DOOH Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

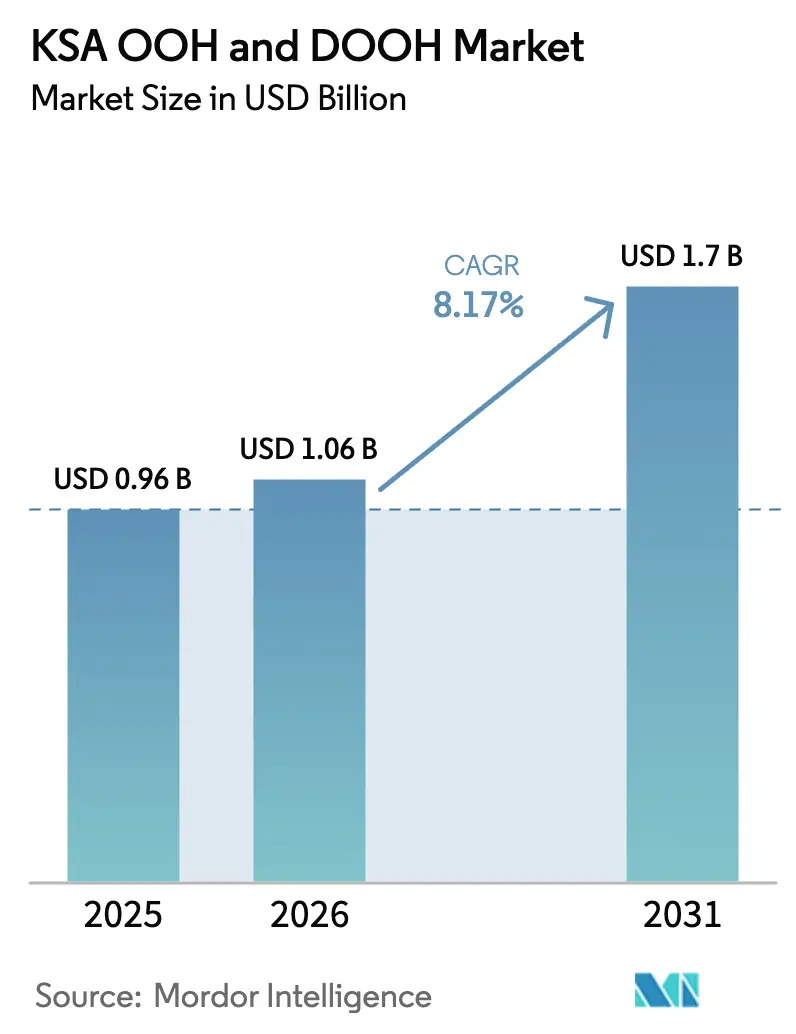

| Base Year Market Size (2025) | USD 0.96 Billion |

| Market Size (2026) | USD 1.06 Billion |

| Market Size (2031) | USD 1.7 Billion |

| Growth Rate (2026 - 2031) | 8.17% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

KSA OOH And DOOH Market Analysis by Mordor Intelligence

The KSA OOH and DOOH market size is expected to grow from USD 0.96 billion in 2025 to USD 1.06 billion in 2026 and is forecast to reach USD 1.7 billion by 2031 at 8.17% CAGR over 2026-2031. Robust digitization programs, nationwide 5G and fiber coverage, and the Riyadh Metro’s large-scale digital screen network are broadening audience reach while compressing campaign lead times. Digital formats already dominate prime roadside and transit corridors, and the pipeline of Vision 2030 giga-projects will keep reallocating ad budgets away from print and static billboards toward data-rich, programmatic-ready inventory. Airports, transit hubs, and retail venues are proving especially attractive because they combine dwell-time with granular audience analytics, allowing advertisers to synchronize outdoor messages with mobile prompts and in-store activations. Competitive intensity is accelerating as local champions defend contracts against global majors deploying self-serve SSPs and AI creative tools that lower the entry barrier for mid-tier brands.

Key Report Takeaways

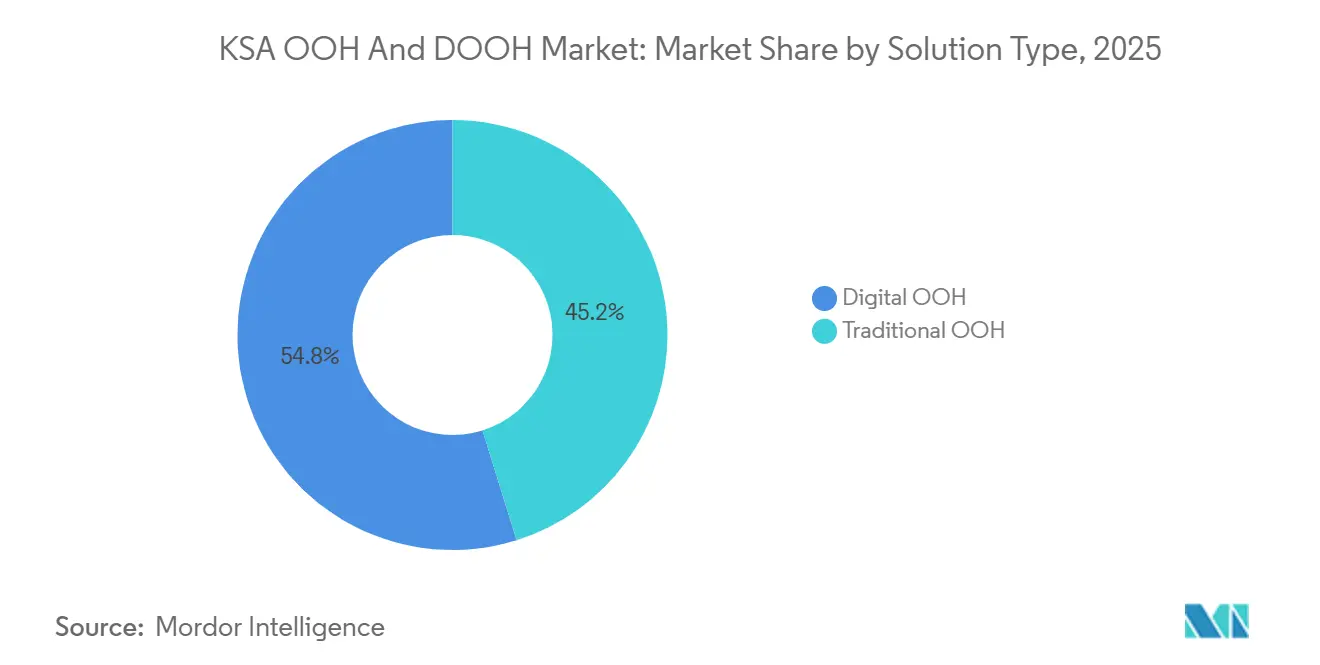

- By solution type, digital OOH led with 54.83% of KSA OOH and DOOH market share in 2025, while programmatic sub-buys are projected to expand at an 8.67% CAGR through 2031.

- By application, transit accounted for 10.34% of the KSA OOH and DOOH market size in 2025 and is advancing at the fastest 10.34% CAGR to 2031.

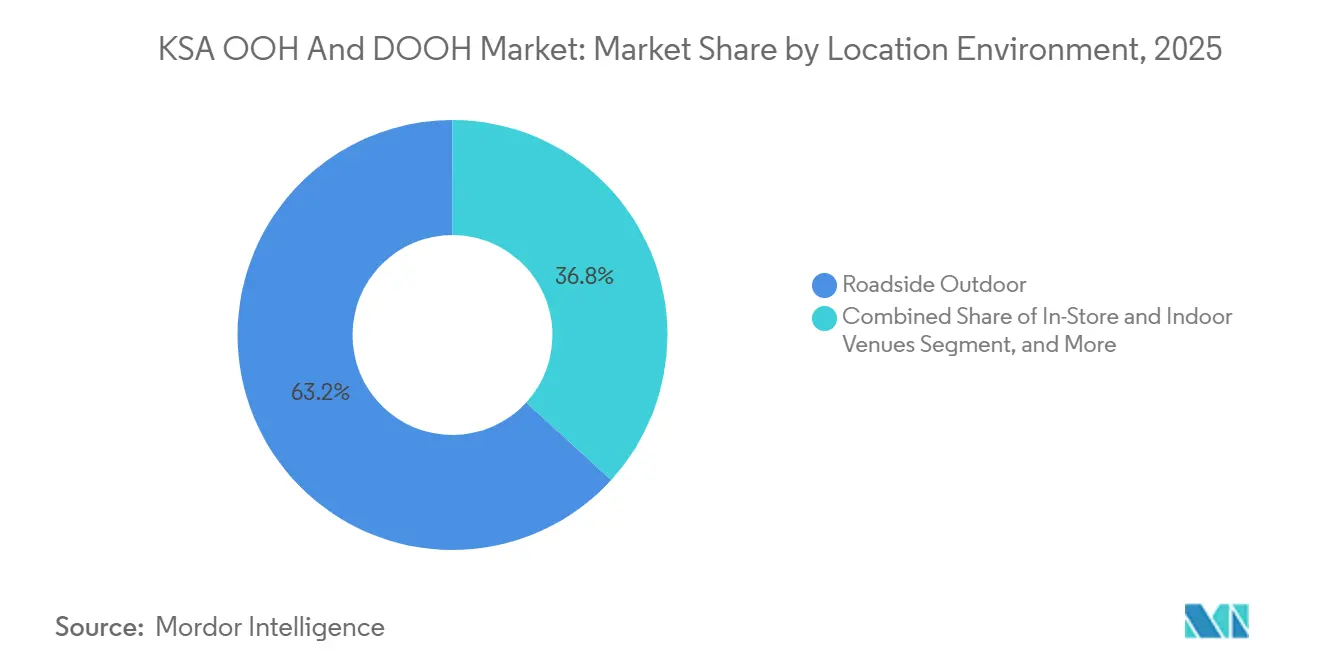

- By location environment, airports recorded the highest projected 12.23% CAGR through 2031, outpacing roadside formats that held 63.21% revenue share in 2025.

- By end-user industry, healthcare represented the quickest 11.16% CAGR to 2031, whereas retail retained the largest 28.37% share of the Saudi Arabia OOH and DOOH market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

KSA OOH And DOOH Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2030 Smart-City Mega Projects Accelerating DOOH | +2.5% | Riyadh, NEOM, The Line, Jeddah | Long term (≥ 4 years) |

| Expansion of 5G and Fiber Enabling Programmatic DOOH | +1.8% | Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Ongoing Shift Toward Digital Advertising | +1.5% | National | Medium term (2-4 years) |

| AI-Driven Audience Analytics Boosting Campaign ROI | +1.2% | Riyadh, Jeddah hubs | Medium term (2-4 years) |

| Growing Development of Public Transport Networks | +1.0% | Riyadh, Medina, Jeddah | Short term (≤ 2 years) |

| Rise of EV-Charging Hubs as New DOOH Inventory | +0.5% | Highway corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vision 2030 Smart-City Mega Projects Accelerating DOOH

Large-scale developments such as NEOM, The Line, and the six-line Riyadh Metro are embedding thousands of connected screens into stations, tunnels, and pedestrian zones. The metro carried more than 18 million passengers within months of its June 2025 launch, providing consistent 15-30 minute dwell windows for contextual ads.[1]MENAFN, “Saudi Signs Media Launches Digital Screen Network Inside Riyadh Metro Carriages,” menafn.com A SAR 10 billion (USD 2.6 billion) partnership between Arabian Contracting and the Saudi Company for Artificial Intelligence is digitizing 80% of new roadside inventory, shrinking permit cycles to under 30 days and positioning the capital as a living lab for advanced DOOH formats.

Expansion of 5G and Fiber Enabling Programmatic DOOH

Saudi Telecom Company, Mobily, and Zain KSA have invested over SAR 35 billion (USD 9.3 billion) since 2024 to blanket key cities with low-latency 5G and gigabit fiber. Real-time connectivity supports dynamic price bidding, weather-triggered creative swaps, and verified impression logging.[2]stc, “2024 Annual Report,” stc.com.sa JCDecaux’s Play+ platform and Broadsign’s SSP integrations now let media buyers assemble nationwide screen plans in minutes, opening premium transit and airport slots to mid-budget brands that previously faced month-long minimum bookings.[3]JCDecaux Middle East, “Saudi Arabia,” jcdecauxme.com

Ongoing Shift Toward Digital Advertising

Digital ad spend surpassed SAR 100 billion (USD 26.6 billion) in 2025, yet 98% of retail transactions still occur offline. Advertisers therefore use DOOH to reconnect online discovery with in-store purchases, exploiting QR codes, app coupons, and Bluetooth beacons. Partnerships between Panda supermarkets, Faden Media, and Alan Media have converted print circular funds into closed-loop, AI-optimized shelf screens that report SKU-level uplift within 48 hours.

AI-Driven Audience Analytics Boosting Campaign ROI

Operators now fuse anonymized Ad IDs, ticketing data, and camera-based counts to predict audience composition down to age and gender brackets without breaching the Personal Data Protection Law. Broadsign’s AI Creative Assistant auto-generates Arabic-English variants that respect cultural norms, trimming design costs by up to 30% and letting advertisers cycle five or six micro-messages per hour rather than one generic loop.[4]Broadsign, “Broadsign Platform Overview,” broadsign.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Maintenance Costs in Harsh Climate | -1.2% | Desert corridors, Riyadh, Jeddah | Short term (≤ 2 years) |

| Stringent Permit and Content Regulations | -0.8% | National | Medium term (2-4 years) |

| Measurement and Attribution Complexity | -0.5% | National | Medium term (2-4 years) |

| Extreme-Heat Hardware Degradation Risk | -0.4% | Roadside highways | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capex and Maintenance Costs in Harsh Climate

Climate-hardened LED modules able to survive 50 °C heat and sandstorms cost around 40% more than temperate-zone displays. Summer midday labor bans also restrict installation windows, inflating project schedules and field service overhead. Incumbents with bulk purchasing power and in-house engineering absorb these premiums, whereas smaller firms face 15-20% higher failure rates that erode the five-year payback on new roadside screens.

Stringent Permit and Content Regulations

The General Commission for Audiovisual Media requires pre-clearance of every creative asset and levies SAR 15,000 (USD 3,998) licenses that renew every three years. Content deemed culturally sensitive can stall for weeks, adding budget uncertainty and pushing time-critical launches back into social or mobile channels. Penalties up to SAR 10 million (USD 2.6 million) for violations compel operators to invest in compliance teams and template libraries, adding 10-15% to creative production costs and slightly depressing programmatic CPM yields.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Programmatic Platforms Accelerate Digital OOH Dominance

Digital formats captured 54.83% of KSA OOH and DOOH market share in 2025 as operators converted static sites to LED and networked players plugged screens into supply-side platforms. JCDecaux’s Play+ roll-out, combined with Broadsign’s AI Creative Assistant, cut booking cycles from days to minutes, enticing FMCG and banking advertisers to test hourly weather or traffic triggers. Traditional static formats still cover secondary highways where fiber remains sparse, but their proportion is projected to shrink toward the mid-30% range by 2031 as 5G blankets tier-2 cities.

Programmatic impressions represented only 8-10% of digital spend in 2025, yet the pipeline of connected roadside poles and airport panels is on track to push that ratio toward 30% before 2028. Arabian Contracting has already digitized two-thirds of its 24,515 faces and aims for 80% by end-2025, underscoring the structural upgrade cycle. The KSA OOH and DOOH market size tied to direct-sold loops will keep growing in absolute terms, but its share of budgets will slide as buyers pivot to auction-cleared impressions that allow tighter dayparting and KPI-linked mid-flight optimization.

By Application: Transit Inventory Gains as Metro and Bus Networks Expand

Billboards retained 45.96% of spend in 2025, yet transit formats are scaling fastest at a 10.34% CAGR, fueled by 2,688 metro carriage screens and municipality-backed bus rollouts in Medina and Jeddah. Six ceiling-mounted panels per carriage ensure every rider sees at least two spot rotations during an average 20-minute commute, yielding verified reach in a brand-safe, distraction-light environment.

Bus shelters, kiosks, and in-vehicle tablets enrich the omnichannel path by pushing promo codes that unlock in-app ride points or nearby mall discounts. Advertisers keen on frequency and recency are therefore shifting sequential storyboards from television to subway journeys. Billboard owners are responding by clustering large-format LEDs at station exits to capture passengers again at street level, but the growth delta favors transit until metro ridership plateaus later in the decade.

By Location Environment: Airports Surge as Giga-Projects Drive Passenger Growth

Roadside corridors still accounted for 63.21% of the KSA OOH and DOOH market size in 2025, reflecting car-centric mobility and decades of concession investment. Airports, however, are racing ahead with a 12.23% CAGR as expansion at King Fahd International and 17 regional fields adds curved LEDs, experiential walkthroughs, and duty-free-linked QR commerce journeys. A 10-year Cluster 2 contract hands Arabian Contracting exclusivity across 18 domestic airports, shifting premium demand toward captive lounges where dwell times top 60 minutes.

Renewables-powered screens and ambient-light sensors help airports meet ESG targets, which multinationals increasingly cite in RFP scorecards. Meanwhile, malls and mixed-use giga-projects such as Qiddiya and Diriyah Gate are layering indoor LEDs above escalators and atrium bridges. Their double-digit growth trajectory keeps them ahead of static roadside structures whose measurement tools are mature but creative limitations inhibit dynamic storytelling.

By End-User Industry: Healthcare Advertising Accelerates as Digital Health Adoption Scales

Retail preserved the largest 28.37% share of KSA OOH and DOOH market size in 2025 thanks to AI-driven in-store networks that substitute print brochures with point-of-purchase promo loops. Yet healthcare leads on velocity with an 11.16% CAGR as the Sehhaty app’s 31 million users prime consumers for telehealth offers displayed in waiting rooms, pharmacies, and hospital atriums. DOOH’s brand-safe, HIPAA-compliant journey mapping is valuable because it respects privacy while linking exposure to pharmacy redemption data.

Automotive manufacturers are next in line, using roadside LEDs and charging-station pillars to demystify EV ownership costs. BFSI brands adopt Bluetooth beacons and gender-segmented creatives to widen credit-card penetration among previously under-banked women, while entertainment promoters leverage stadium-scale displays ahead of esports tournaments and international concerts. Government agencies reserve off-peak loops for public-health reminders, keeping inventory utilization above 80% even in holiday lulls.

Geography Analysis

Riyadh commands nearly half of national spend, combining an 8 million-strong consumer base with the Kingdom’s densest smart-city rollouts. A SAR 10 billion (USD 2.6 billion) digitization pact through 2035 obliges Arabian Contracting to convert four-fifths of new roadside boards to LED, fortifying the city’s leadership in both screen count and programmatic readiness. Seamless fiber in business districts lets advertisers switch creative in under 60 seconds when sudden sandstorms or soccer victories spike topical relevance.

Jeddah contributes roughly one-quarter of expenditure, anchored by a 30 million-passenger airport funneling Hajj and Umrah traffic. A SAR 1 billion (USD 0.26 billion) bridge-and-tunnel LED project plus fresh regulations for bus-mounted displays broaden reach into coastal promenades and heritage alleys. Fiber upgrades empower retailers in Red Sea and Mall of Arabia to integrate in-store signage with roadside countdowns that promise limited-hour flash deals, sustaining footfall even outside pilgrimage seasons.

The Eastern Province adds 15-20% of turnover, with Dammam Airports Company granting a decade-long exclusivity that packs King Fahd International with landmark LEDs and renewable-powered street furniture. Highway EV corridors between Riyadh and Dammam are set to unveil 5,000 charging points by 2030, potentially birthing a new micro-network of 20-minute dwell screens. Tier-2 hubs such as Medina, Taif, and Abha collectively absorb the remainder, aided by bus kiosks that monetize municipal transport subsidies and by NEOM’s pipeline of sensor-rich public plazas slated to go live after 2028.

Competitive Landscape

The KSA OOH and DOOH market maintains moderate fragmentation: the top three players hold around 60% of premium roadside, transit, and airport faces. Arabian Contracting’s contract extension to 2035 cements its municipal stronghold, while JCDecaux leverages global playbooks and its Play+ tech stack to win performance-driven briefs. Rotana Signs intends to triple inventory via a SAR 7 billion program that zeroes in on airport and metro screens, aiming for a 35% share by decade-end.

Smaller specialists survive by owning niche retail and point-of-sale loops paired with privacy-safe attribution dashboards. They also court quick-service restaurants and telecom flash campaigns that value speed over scale. Hardware costs and licensing fees, however, are thinning their margins, accelerating M and A interest from larger concessionaires keen to lock in footfall-rich grocery aisles.

Technology is the chief differentiator. Operators integrated with Broadsign’s AI Creative Assistant cut artwork turnaround to hours, letting brands A/B-test multiple taglines within the same flight. Firms lacking SSP pipes must still rely on fixed loops, limiting CPM upside and rendering them vulnerable when advertisers chase incremental reach rather than total impressions.

KSA OOH And DOOH Industry Leaders

Arabian Contracting Services Co. (AlArabia)

JCDecaux SE

Alliance Media Holdings (Pty) Ltd

Alan Media and Advertising Co.

Saudi Signs Media Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Jeddah Transportation Company issued standards for digital mobile ads on buses and taxis, unlocking regulated in-vehicle inventory.

- February 2026: Arabian Contracting Services, via Faden Media, extended its Riyadh city outdoor advertising contract to Jul 2035, securing a six-month grace period plus a paid year.

- January 2026: Arabian Contracting Services won a 10-year exclusive concession for 18 Cluster 2 airports, expanding its airport footprint.

- June 2025: Saudi Signs Media and Rotana Signs installed 2,688 screens across 448 Riyadh Metro carriages, targeting more than 18 million riders.

KSA OOH And DOOH Market Report Scope

The study tracks the advertising spending on various OOH formats, including billboards (city-light boards), street furniture (city-light posters), transit and transportation (advertising in and on vehicles used for public transportation), and place-based media (media at the point of sale). The scope of the study includes digital and static advertisements placed indoors and outdoors at shopping malls, airports, streets, and transit locations. The commission and production costs of agencies are excluded from the scope of work.

The KSA OOH and DOOH Market Report is Segmented by Solution Type (Traditional OOH, and Digital OOH [Programmatic-DOOH, and Non-Programmatic-DOOH]), Application (Billboard, Transit, Street Furniture, and Other Applications), Location Environment (Roadside Outdoor, Airports, Malls and Transit Hubs, In-Store and Indoor Venues, and Other Location Environments), End-User Industry (Automotive, Retail, Healthcare, Banking and Financial Services, Media and Entertainment, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Traditional OOH | |

| Digital OOH | Programmatic-DOOH |

| Non-Programmatic-DOOH |

| Billboard |

| Transit |

| Street Furniture |

| Other Applications |

| Roadside Outdoor |

| Airports |

| Malls and Transit Hubs |

| In-Store and Indoor Venues |

| Other Location Environments |

| Automotive |

| Retail |

| Healthcare |

| Banking and Financial Services (BFSI) |

| Media and Entertainment |

| Other End-User Industries |

| By Solution Type | Traditional OOH | |

| Digital OOH | Programmatic-DOOH | |

| Non-Programmatic-DOOH | ||

| By Application | Billboard | |

| Transit | ||

| Street Furniture | ||

| Other Applications | ||

| By Location Environment | Roadside Outdoor | |

| Airports | ||

| Malls and Transit Hubs | ||

| In-Store and Indoor Venues | ||

| Other Location Environments | ||

| By End-User Industry | Automotive | |

| Retail | ||

| Healthcare | ||

| Banking and Financial Services (BFSI) | ||

| Media and Entertainment | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

How large will Saudi Arabia's outdoor digital advertising spend be by 2031?

The KSA OOH and DOOH market size is forecast to reach USD 1.57 billion by 2031.

Which format grows fastest in Saudi outdoor advertising?

Airport screens lead with a projected 12.23% CAGR through 2031, reflecting passenger growth and exclusive concessions.

What share of spend already comes from digital formats?

Digital OOH commanded 54.83% of national out-of-home spend in 2025 and continues to expand.

Why are healthcare brands investing in Saudi DOOH?

The Sehhaty app's 31 million users and virtual hospital links let healthcare advertisers connect screen exposure to appointment bookings, driving an 11.16% CAGR for the vertical.

How do harsh climates affect screen owners?

Climate-hardened LEDs cost about 40% more and raise maintenance schedules, slightly trimming operator margins without scale advantages.

What technology trend will shape buying behavior by 2028?

Programmatic SSP integrations are expected to lift auction-cleared impressions to roughly 30% of digital spend, enabling hour-level targeting and real-time creative swaps.

Page last updated on: