Kenya Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.28 Billion |

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 1.54 Billion |

| Growth Rate (2026 - 2031) | 3.17% CAGR |

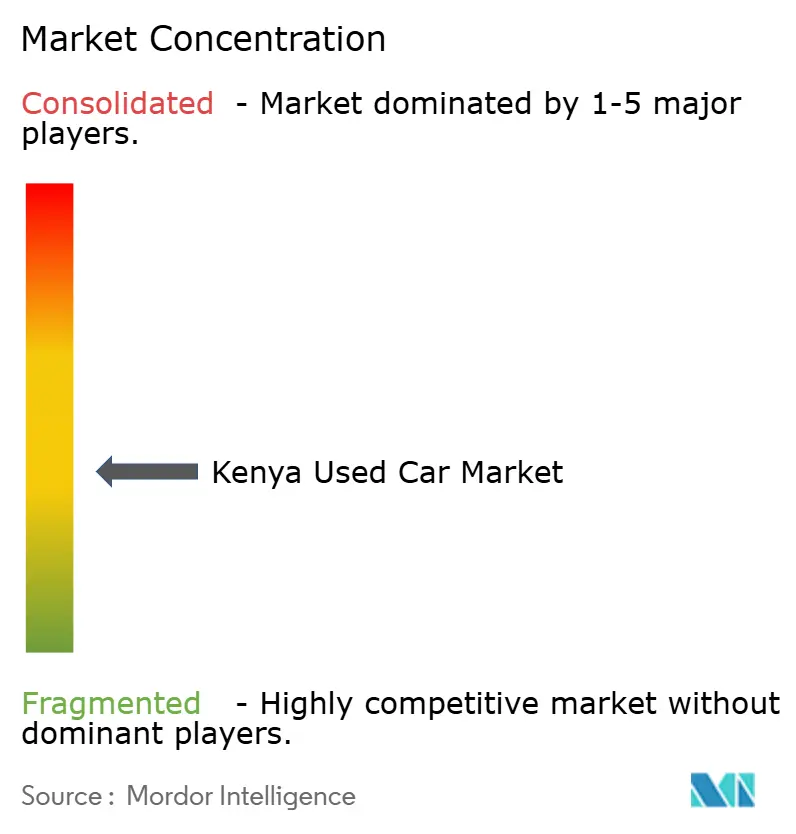

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya Used Car Market Analysis by Mordor Intelligence

The Kenya used car market size is expected to grow from USD 1.28 billion in 2025 to USD 1.32 billion in 2026 and is forecast to reach USD 1.54 billion by 2031 at 3.17% CAGR over 2026-2031. Consumer migration to online platforms, the prominence of Japanese right-hand-drive imports, and regulatory age limits shape demand patterns and dealer strategies. While traditional informal dealerships still dominate vehicle sales, organized channels are steadily gaining ground, driven by better financing options and stronger regulatory compliance that boost buyer confidence. Interest in hybrid and electric vehicles is growing, supported by government targets and a rising number of registered EVs. Japan continues to be the leading source of vehicle imports, maintaining supply despite stricter age limits introduced by Kenya. Stable currency conditions help dealers manage costs and plan inventory more effectively, especially in markets heavily reliant on imports.

Key Report Takeaways

- By vehicle type, hatchbacks captured 42.36% of the Kenyan used car market share in 2025, whereas SUVs and MPVs marked the fastest growth at 4.44% CAGR through 2031.

- By vendor type, unorganized dealers held 62.63% of the Kenya used car market share in 2025, while organized channels recorded the highest projected growth at 5.04% CAGR through 2031.

- By fuel type, petrol models led with 72.71% share of the Kenya used car market size in 2025; hybrid and electric vehicles are advancing at an 8.61% CAGR to 2031.

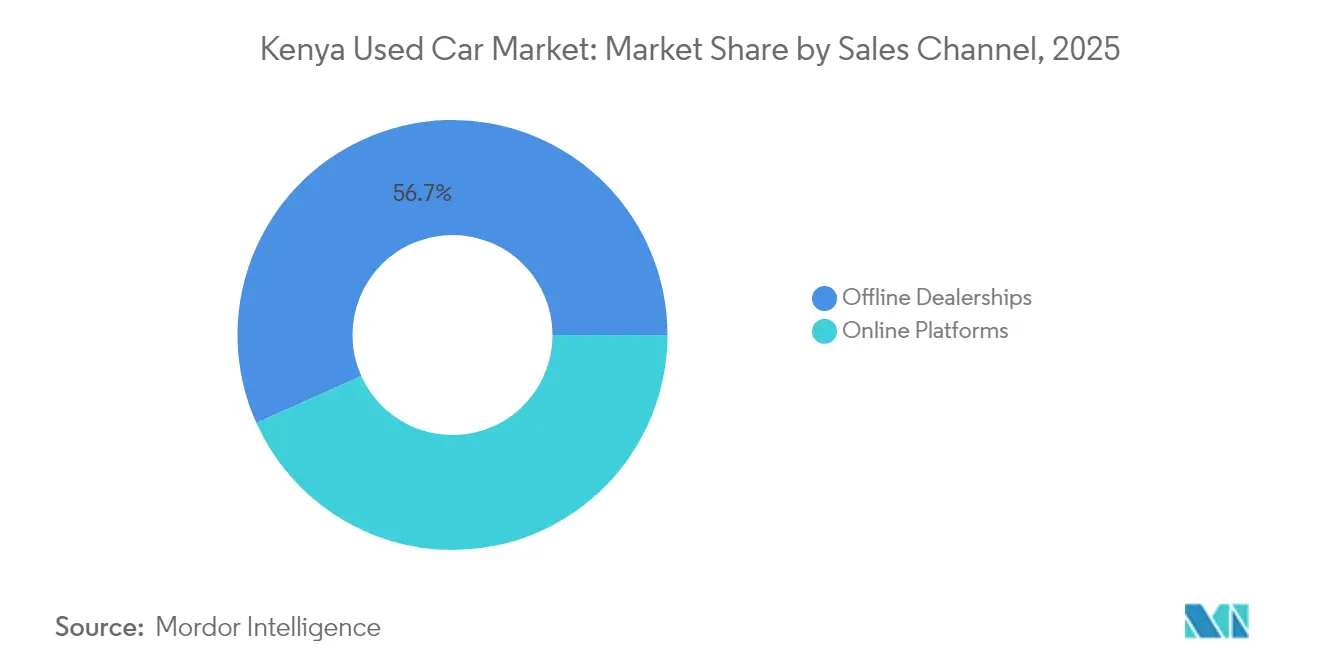

- By sales channel, offline dealerships retained a 56.72% share in 2025, yet online platforms are set to rise at an 8.14% CAGR through 2031.

- By vehicle age, the 5–8-year bracket commanded 50.73% of the Kenya used car market size in 2025, yet the 0–3-year segment is projected to expand at a 5.55% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide used car market outlook captures this forward trajectory.

Kenya Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Middle-Class Preference for Affordable Second-Hand Imports | +0.8% | Nairobi, Mombasa, Kisumu | Medium term (2–4 years) |

| Online B2C Platforms & Fintech Car Loans Expanding Access | +0.6% | Urban centers, secondary cities | Short term (≤ 2 years) |

| Ex-Japan RHD Hybrids Lowering Ownership Costs | +0.5% | National, early adoption in cities | Medium term (2–4 years) |

| Ride-Hailing and Delivery Fleets Driving Low-CAPEX Demand | +0.4% | Nairobi, Mombasa, Nakuru, Eldoret | Short term (≤ 2 years) |

| Refurbished Ex-Corporate Fleets Entering from East Africa | +0.3% | Regional hub distribution | Long term (≥ 4 years) |

| Duty-Free Re-Export via Mombasa FTZ Boosting Trade Flow | +0.2% | Coastal cross-border trade | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Middle Class Favoring Second-Hand Imports

New vehicle registrations declined as more buyers turned to used cars that better match tighter household budgets. Inflation has reduced disposable income, making reliable pre-owned imports—mainly from Japan—an attractive alternative. Although new vehicles carry high tax burdens, much of this cost is absorbed before they enter the used market, improving affordability. These dynamics are reshaping consumer preferences and reinforcing the role of used vehicles in meeting mobility needs. Monthly motor insurance plans introduced by CIC Insurance lowered upfront ownership barriers, broadening accessibility for middle-income earners. The result is consistent transaction volume for second-hand cars even as new sales retract.

Expansion of Ride-Hailing and Delivery Fleets Demanding Low-CAPEX Vehicles

Uber counts 363,000 active riders in Kenya, creating a steady need for cost-efficient, durable vehicles[1]“2025 Africa Fact Sheet,”, Uber Technologies, uber.com. Fare adjustments of 10–20% in 2024 improved driver margins, encouraging vehicle acquisition for platform work. NTSA’s commission cap at 18% further protects take-home pay and stimulates fleet growth. Age rules of 2009+ in Nairobi fit the sweet spot for imported 8–15-year models, keeping older units relevant. Parallel e-commerce expansion fuels demand for pickups and vans, linking logistics growth to the Kenya used car market.

Growing Supply of Refurbished Ex-Corporate Fleets from East Africa

Large organizations across East Africa retire fleets sooner to meet ESG goals, releasing well-maintained stock into regional auctions centered in Kenya. Importers refurbish these units and remarket them with limited mileage history, appealing to buyers seeking reliable alternatives to high-mileage Japanese imports. Kenya’s status as a valuation hub means refurbishers source spares quickly and in bulk, compressing turnaround times. The trend feeds a pipeline of quality inventory that differentiates organized dealers from informal rivals.

Duty-Free Re-Export Window via Mombasa Free-Trade Zone

Three new Export Processing Zones at Bonje, Bombululu, and Mavoko, declared in February 2023, grant duty-free privileges that importers leverage to stage vehicles for re-export to Uganda and Tanzania[2]“Kenya EPZ Expansion,”, UNCTAD, unctad.org. The mechanism lowers total landed cost for onward buyers and positions Kenya as East Africa’s clearing center. While a modest contributor, the window diversifies revenue sources for dealers facing domestic age-limit constraints, bolstering long-term growth prospects for the Kenyan used car market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proposed Up to 5-Year Age Limit on Imports | -0.7% | National | Short term (≤ 2 years) |

| Stricter Emissions Tests and Euro-4 Enforcement | -0.5% | National, Mombasa port focus | Medium term (2–4 years) |

| Currency Depreciation Raising CIF Vehicle Costs | -0.3% | Import-dependent zones | Short term (≤ 2 years) |

| Low-Cost Chinese CKD Assembly Undercutting Used-Car Demand | -0.2% | Urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tougher Emissions Tests & Impending Euro-4 Standard Enforcement

Upcoming alignment with regional environmental standards will restrict the import of older, less efficient engines, increase inspection requirements, and extend clearance times at key entry points like Mombasa port. Retrofitting borderline vehicles to meet compliance may become costly, making some models unaffordable. However, vehicles that meet the new standards will likely retain higher resale value, which could lead to a market shift favoring those with verified environmental credentials.

Low-Cost Chinese CKD Assembly Eroding Used-Car Appeal

In collaboration with Toyota-linked dealerships, BYD has made a significant market entry by launching several models. These offerings come with competitive advantages, including attractive warranties and financing options. Despite withdrawing local tax incentives for assembled vehicles, BYD's economies of scale might still uphold its pricing edge. As new electric cars become available at prices comparable to used imports, buyer preferences will likely shift. This is particularly true for those emphasizing long-term reliability, which could transform demand within crucial segments of the used car market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Hatchbacks Lead Despite SUV Momentum

Hatchbacks represented 42.36% of the Kenyan used car market in 2025, underscored by Toyota Vitz and Honda Fit models that align with urban parking constraints and lower running costs. SUVs and MPVs show a 4.44% CAGR to 2031 as rising disposable income and aspirational preferences lift demand for perceived safety and versatility. Sedans retain appeal among corporate fleets that favor formal aesthetics, while light commercial vehicle uptake tracks agricultural output and e-commerce distribution demand.

Light commercial vehicles, led by Toyota Hilux and Isuzu D-Max, benefit from parts availability and robust chassis suited to mixed-terrain logistics routes. Chinese entrants offer lower sticker prices but face skepticism over resale value and service coverage. Continued infrastructure upgrades widen delivery routes, translating into incremental demand for pickups and vans throughout the Kenyan used car market.

By Vendor Type: Unorganized Dominance Faces Digital Disruption

The unorganized segment held a 62.63% share in 2025, leveraging minimal overheads and direct sourcing links to Japan. However, the organized dealers’ 5.04% forecast CAGR reflects gains from warranty programs, structured financing, and compliance advantages that appeal to risk-averse buyers. Withholding tax obligations on digital platforms force greater transparency, nudging informal operators either to formalize or lose online visibility.

Banks regularly prefer collateral from registered dealers, channeling credit toward organized players and reinforcing their inventory purchasing power. Meanwhile, unorganized dealers retain agility in price negotiation and can source niche models fast, keeping them relevant in the Kenyan used car market even as digital disruption mounts.

By Fuel Type: Petrol Dominance Meets Hybrid Acceleration

Petrol units held 72.71% of the 2025 volume, supported by a wide refueling infrastructure and simple maintenance. Hybrid and electric vehicles, registering an 8.61% CAGR, gain impetus from the Draft Electric Mobility Policy’s green plates and prospective duty incentives. Diesel remains essential for long-haul and high-torque needs but faces public perception challenges over emissions.

Toyota Prius and Honda Insight imports enjoy mature aftermarket support, minimizing parts scarcity risk. The Kenya used car market size for hybrids is projected to grow alongside charging infrastructure rollouts and sustained fuel price volatility that magnifies operational savings.

By Sales Channel: Digital Platforms Challenge Traditional Dealerships

Offline dealerships kept a 56.72% share in 2025 because many buyers value physical inspection and immediate vehicle release. Yet online channels, expanding at 8.14% CAGR, aggregate multi-dealer inventories and integrate financing that compresses consumer search costs. NTSA’s digital number plate issuance, resumed in May 2025, reduces fraud risk and dovetails with online verification workflows.

Dealers are experimenting with hybrid models where listings originate online, but final transactions conclude in showrooms, preserving the experiential component. The Kenya used car market benefits as heightened transparency limits price distortions and broadens geographic reach for both buyers and sellers.

By Vehicle Age: Mid-Age Preference Shifts Toward Newer Models

Vehicles aged 5–8 years held 50.73% of 2025 transactions, offering an equilibrium between depreciation savings and acceptable reliability. The 0–3-year cohort posts a 5.55% CAGR as eight-year age caps force importers upmarket and banks offer longer tenures on newer collateral. Vehicles above eight years old lose import eligibility yet continue circulating domestically, reinforcing multilayer resale activity inside the Kenyan used car market.

Ride-hailing standards align closely with 8—to 15-year-old vehicles, sustaining demand even as import restrictions tighten. Financing structures increasingly link loan term to vehicle age, nudging consumers toward younger assets and supporting residual value retention for lenders.

Geography Analysis

Kenya is East Africa’s principal vehicle gateway, with Mombasa Port handling the lion’s share of right-hand-drive Japanese imports. Coastal counties in Kenya's used car market benefit from direct access to clearing services and trade-zone incentives that trim overall landed costs. Nairobi, the nation’s economic hub, concentrates high-frequency retail turnover and hosts the largest aggregation of ride-hailing demand, driving continuous replenishment of mid-age vehicle stock.

Inland regions like Eldoret and Nakuru display a growing appetite as infrastructure upgrades improve connectivity, enabling dealers to extend supply chains beyond traditional coastal-to-capital corridors. Uganda and Tanzania depend on Kenya for re-exports, though varying age-limit rules create differential pricing windows. EPZ facilities at Bonje and Bombululu allow importers to warehouse units duty-free before distribution, amplifying Kenya’s role as a regional distribution center.

Ethiopia’s budding assembly capacity portends future supply competition, yet Kenya’s legacy of aftermarket expertise, financial-service integration, and regulatory transparency supports sustained dominance. Mobile money and branchless banking facilitate cross-border transactions, shortening settlement cycles for Ugandan and Tanzanian buyers purchasing through Kenyan online platforms. This regional pull adds a buffer to domestic cyclical swings and strengthens long-run stability across the Kenyan used car market.

The used car market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Africa. This is complemented by country-specific insights for South Africa, Egypt, Brazil, Bangladesh, Kuwait, Canada, Qatar, and Oman, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Market competition remains fragmented. Autochek’s consolidation of Cheki Kenya illustrates digital-scale advantages, including AI-based pricing tools that inform buyer budgets and dealer floor-planning strategies. The January 2025 shutdown of CMC Motors Group reveals vulnerability among legacy distributors unable to pivot quickly to used-car-oriented models or meet compliance costs.

Organized players emphasize warranties, refurbishment standards, and document automation to differentiate themselves. Unorganized importers lean on price under-cutting and quick turnover, but face intensifying scrutiny under KEBS validation and NTSA plate digitization. BYD’s partnership with Toyota-affiliated dealerships introduces a fresh competitor that can offer new EVs at prices approaching late-model hybrids, potentially reshaping value comparisons for urban buyers.

Financing alliances, such as KCB’s extended-tenor loans and NCBA’s mobile credit scoring, increasingly dictate dealership throughput. Digital marketing via social media and automotive classifieds enhances lead generation efficiency, while aftermarket service bundling sustains revenue post-sale. Overall, strategic positioning hinges on compliance prowess, financing integration, and digital visibility across the Kenyan used car market.

Kenya Used Car Industry Leaders

Gigi Motors Limited

Toyota Kenya (Automark)

Jiji Kenya

Autochek Africa

Peach Cars

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: KEBS has implemented a KSh 12,000 validation fee on each imported vehicle, increasing compliance costs and intensifying oversight measures. This fee aims to ensure that imported vehicles meet the required standards and regulations, thereby enhancing the quality and safety of vehicles entering the market.

- July 2025: Suzuki Motor Corporation, through its corporate venture capital fund, Suzuki Global Ventures, has made an investment in Cordia Directions, Ltd. Cordia Directions, a Japanese start-up, operates Peach Cars, a platform facilitating the trade of used cars in Kenya and the broader East African region, which is poised for future growth.

Kenya Used Car Market Report Scope

A used car, a pre-owned vehicle, or a second-hand car is a vehicle that has previously had one or more retail owners. On the other hand, a certified pre-owned (CPO) vehicle is a pre-owned vehicle that has been extensively inspected (pre-purchase inspection) and expertly reconditioned. The term 'used' refers to the fact that the car has been driven and may have accumulated some wear and tear over its lifetime.

The scope of Kenya's used car market is segmented by vehicle type and vendor. By vehicle type, the market is segmented into hatchbacks, sedans, sport utility vehicles, and multi-purpose vehicles. By vendor, the market is segmented into organized and unorganized.

For each segment market sizing and forecast have been done on the basis of value (USD).

| Hatchbacks |

| Sedans |

| Sport Utility Vehicles and Multi-Purpose Vehicles |

| Light Commercial Vehicles (Pick-ups and Vans) |

| Organized |

| Unorganized |

| Petrol |

| Diesel |

| Hybrid & Electric |

| Online Platforms |

| Offline Dealerships |

| 0-3 Years |

| 3-5 Years |

| 5-8 Years |

| Above 8 Years |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| Sport Utility Vehicles and Multi-Purpose Vehicles | |

| Light Commercial Vehicles (Pick-ups and Vans) | |

| By Vendor Type | Organized |

| Unorganized | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid & Electric | |

| By Sales Channel | Online Platforms |

| Offline Dealerships | |

| By Vehicle Age | 0-3 Years |

| 3-5 Years | |

| 5-8 Years | |

| Above 8 Years |

Key Questions Answered in the Report

What is the forecast value of the kenya used car market by 2031?

The kenya used car market is projected to reach USD 1.54 billion by 2031.

Which vehicle age bracket is growing fastest in Kenya’s second-hand sector?

Units aged 0–3 years are forecast to expand at 5.55% CAGR between 2026 and 2031 due to tighter import age rules and improved financing.

How dominant are online platforms in Kenya’s used vehicle sales?

Online channels held 43.28% of 2025 transactions and are growing at 8.14% CAGR as buyers seek transparency and integrated financing.

How does the eight-year import age limit impact supply?

The January 2025 rule removes the oldest inventory categories, raising average vehicle prices and benefiting organized dealers able to finance newer stock.

What recent policy supports EV adoption in Kenya?

The Draft Electric Mobility Policy issued in March 2025 introduces green number plates and targets a 5% EV share, signaling favorable treatment for electric imports.

Page last updated on: