Egypt Used Car Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 7.53 Billion |

| Market Size (2030) | USD 9.20 Billion |

| Growth Rate (2025 - 2030) | 4.09% CAGR |

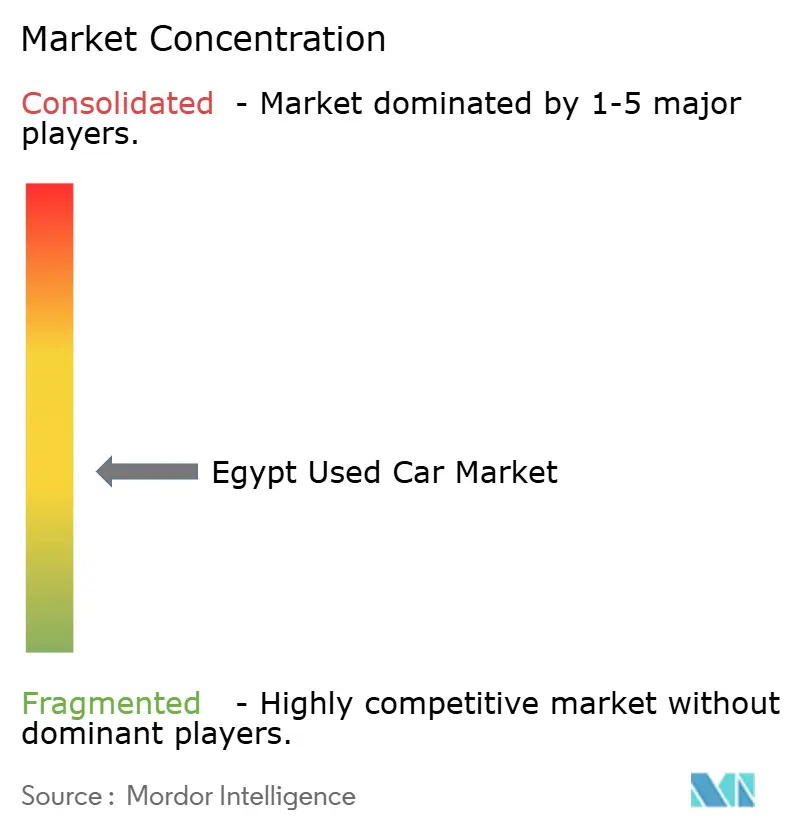

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Used Car Market Analysis by Mordor Intelligence

The Egyptian used car market size stands at USD 7.53 billion in 2025 and is projected to reach USD 9.20 billion by 2030, reflecting a 4.09% CAGR during 2025-2030 period. Demand strength endures despite currency swings and subsidy reforms as value-seeking households pivot toward affordable pre-owned mobility. Organized retail formats, digital platforms, and OEM trade-in pipelines are expanding supply while fintech-enabled installment plans broaden access, supporting steady unit velocity. Competitive intensity sharpened in early 2025 following Dubizzle’s purchase of Hatla2ee, signaling a platform-led consolidation wave that could narrow pricing spreads and lift professional standards.

Key Report Takeaways

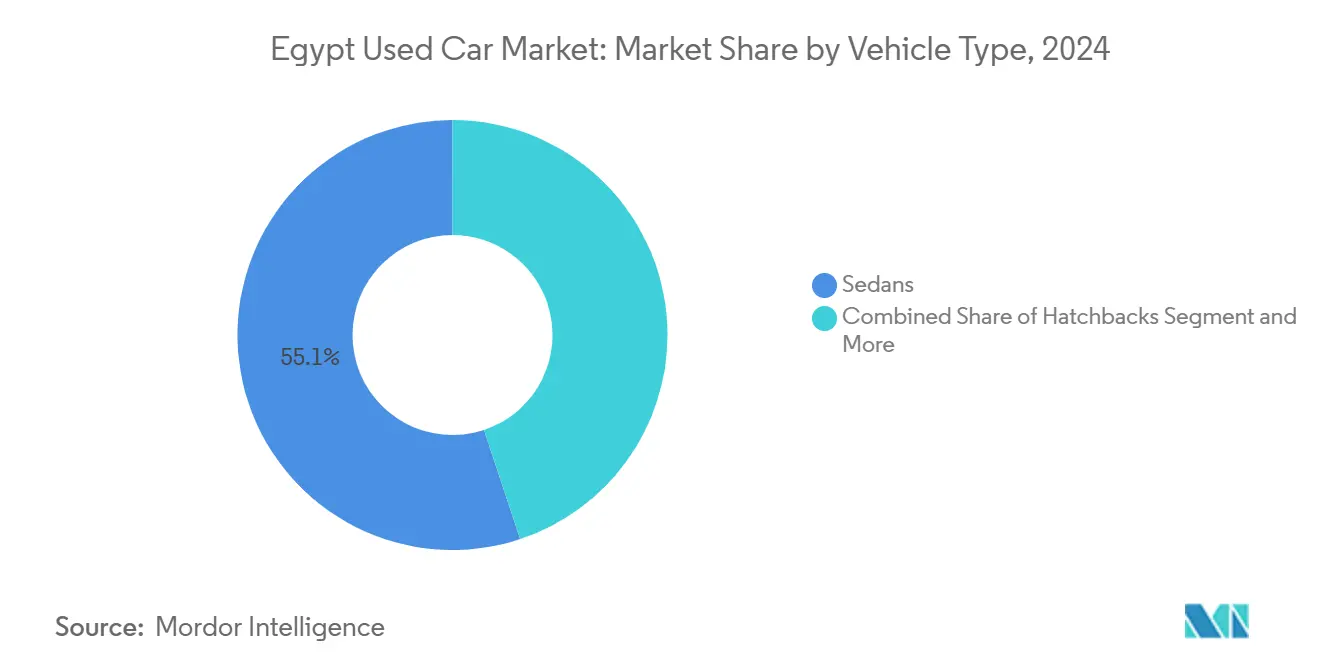

- By vehicle type, sedans led with 55.12% of the Egyptian used car market share in 2024; SUVs and MPVs are forecast to expand at a 4.97% CAGR through 2030.

- By vendor type, unorganized sellers held 71.33% of the Egyptian used car market share in 2024, while organized channels are advancing at a 5.62% CAGR to 2030.

- By fuel type, gasoline cars commanded an 85.22% share of the Egyptian used car market size in 2024; electric models are set to grow at a 7.85% CAGR through 2030.

- By sales channel, offline dealerships captured 63.18% share of Egypt used car market size in 2024; online platforms recorded the fastest growth at 7.08% CAGR.

- By vehicle age, models between 5-8 years controlled 42.55% of the Egyptian used car market share in 2024; vehicles below 3 years exhibited the highest 4.63% CAGR.

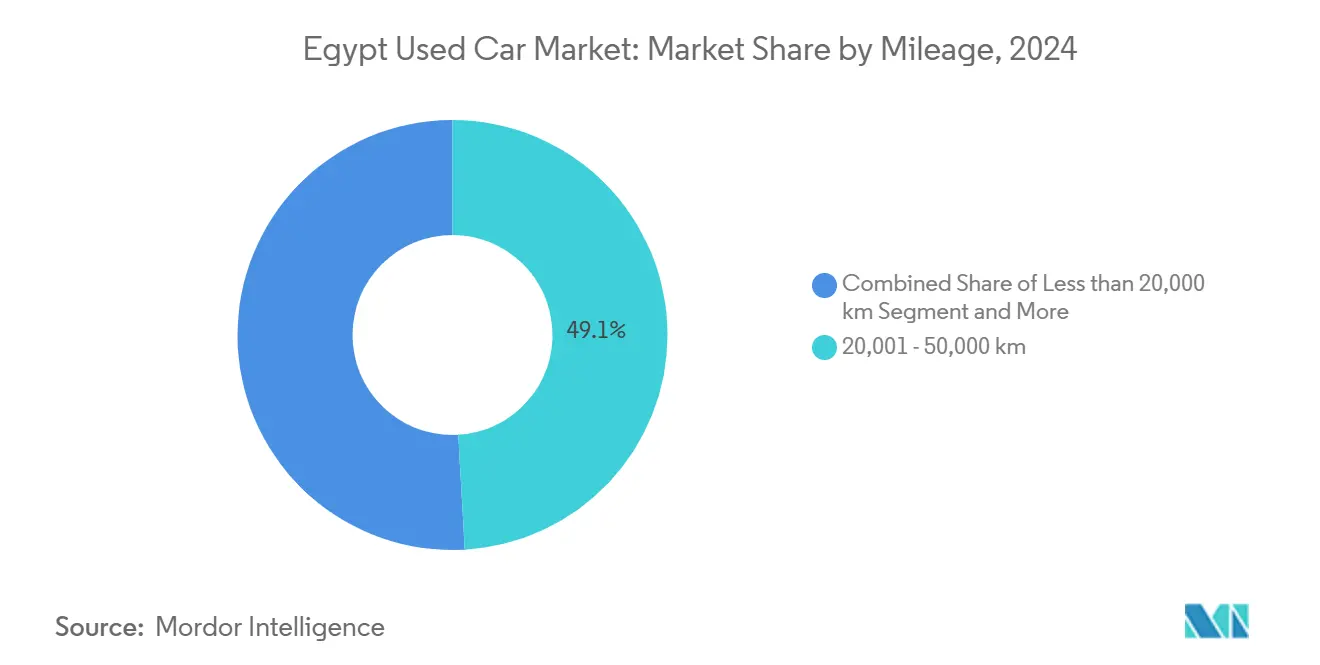

- By mileage, the 20,001-50,000 km band accounted for a 49.14% of the Egyptian used car market share in 2024; Less than 20,000 km inventory will rise at a 6.11% CAGR.

- By price band, transactions below USD 10,000 represented 54.46% of Egypt used car market size in 2024; the USD 10,001-30,000 tier is growing at a 5.12% CAGR.

The pace and direction of global change depend on shifts occurring across countries and regions simultaneously, not within any one of them alone. The global used car market outlook research of Mordor Intelligence reflects this combined progression.

Egypt Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fuel Subsidy Phase-Out Boosts CNG | +0.8% | Greater Cairo, Alexandria | Medium term (2-4 years) |

| Fintech Enables Installment Plans | +0.7% | Urban areas | Short term (≤ 2 years) |

| VC Backed Digital Retailers | +0.6% | Cairo, Alexandria, Giza | Short term (≤ 2 years) |

| OEM Trade-In Schemes Increase Supply | +0.5% | Urban centers with OEM networks | Medium term (2-4 years) |

| EV Import Waiver Under 3 Years | +0.4% | Affluent urban districts | Long term (≥ 4 years) |

| AI Driven Pricing Engines | +0.3% | Major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fuel Subsidy Phase-Out Accelerating CNG Conversions

Gradual fuel-price liberalization lifted gasoline costs relative to compressed natural gas, prompting cost-sensitive buyers to favor CNG-ready units. Dealers now bundle conversion kits with 5-8-year-old inventory, extending earnings lifecycles and pushing resale premiums above comparable gasoline cars. A streamlined regulatory path and expanding CNG service centers augment the conversion value proposition, placing Egypt ahead of regional peers in alternate-fuel uptake.

OEM-supported Trade-in Schemes to Revive New-car Sales and Feed Used Supply

Manufacturers such as Mansour Automotive formalized trade-in programs that refresh showroom traffic while stocking certified pre-owned lots [1]“Trade-In Program Overview,” Mansour Automotive, almansourauto.com. General Motors' production milestone of 1 million units and the new Chevrolet Optra line enlarge the pool of late-model vehicles cycling back into resale channels. Integrated warranties and standardized refurbishment raise buyer confidence and create data feedback loops that refine future pricing and product design.

Entry of VC-backed Digital Retailers (e.g., Sylndr) Boosting Liquidity and Price Transparency

Sylndr’s USD 7.5 million seed raise in 2024 framed investor confidence in data-driven marketplaces that shrink information gaps through algorithmic pricing and verified history reports. Digital entrants weave financing, inspection, and logistics into one interface, accelerating deal cycles and setting new customer-service benchmarks. The February 2025 Dubizzle-Hatla2ee deal crystallized platform leadership, confirming scale and network effects as durable competitive levers.

Growing Availability of Installment-based Fintech for Used-Car Purchases

Egypt’s licensed fintech count is enabling point-of-sale credit via platforms such as valU, MNT-Halan, and Fawry. Central Bank rule changes now permit debt-service ratios up to 50%, stimulating loan volumes yet elevating consumer leverage risk. Regulatory law 5-2022 sets oversight parameters, but uneven enforcement could temper growth if defaults rise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency Drives Price Volatility | -0.9% | Import-dependent segments | Short term (≤ 2 years) |

| Tight Lending Caps Vehicles | -0.5% | Lower-income segments | Long term (≥ 4 years) |

| Limited Title Transfer Digitalization | -0.4% | Rural and secondary cities | Medium term (2-4 years) |

| Fragmented Vehicle Inspection Standards | -0.3% | Governorates outside Greater Cairo | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency-Driven Price Volatility Discouraging Discretionary Purchases

Rapid Egyptian-pound swings inject double-digit price uncertainty for imported models, stalling buyer decisions and raising dealer carrying costs. Economist projections of constrained consumer spend amplify risk for premium tiers. Larger dealers hedge exposure, but independents absorb margin hits or pare inventory, slowing transaction velocity across the Egyptian used car market.

Tight Bank Lending Caps on Vehicles Above Eight Years Old

Commercial banks limit tenors and LTV ratios for cars older than eight years, squeezing credit to budget-focused households that rely on mature inventory. Fintech substitutes charge higher rates, inflating total cost and steering some customers toward informal lenders or purchase delay, dampening volume in the largest age cohort.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Challenge Sedan Dominance

Sedans retained 55.12% of the Egyptian used car market share in 2024, yet SUV and MPV transactions are projected to outpace at a 4.97% CAGR through 2030 as drivers seek higher ground clearance and status appeal. The segment upswing leans heavily on affordable Chinese nameplates such as Geely Emgrand that lower entry thresholds. Local assembly of the Jeep Grand Cherokee L adds supply depth, signaling Egypt’s potential as a regional SUV hub [2]“Jeep Grand Cherokee L Assembly Resumes in Egypt,” Stellantis Press, stellantis.com.

Second-order effects include better parts availability and dealer familiarity that sustain residual values, prompting urban middle-income households to budget higher fuel spend for perceived safety and family capacity. Meanwhile, hatchbacks hold steady among city commuters whose parking constraints favor compact footprints. This multisegment balance will diversify the Egyptian used car market across body styles.

By Vendor Type: Organized Channels Gain Ground

Unorganized sellers managed 71.33% of Egypt's used car market size in 2024, but organized dealers and platforms are advancing at a 5.62% CAGR, fueled by rising consumer demand for warranties, financing, and transparent pricing. AI-driven fraud detection endorsed by the Insurance Federation empowers professionally run lots to combat counterfeit documentation, enhancing buyer trust.

Digital marketplaces bridge gaps for lone sellers by offering inspection, escrow, and logistics, nudging informal actors into semi-formal ecosystems. As platform consolidators exemplified by Dubizzle scale technology and marketing reach, bargaining power should shift toward organized channels, gradually diluting the unorganized share across the Egyptian used car market.

By Fuel Type: Electric Vehicles Emerge Despite Gasoline Dominance

Gasoline cars remain ubiquitous at 85.22% of Egypt's used car market size in 2024; nonetheless, EV sales show a 7.85% CAGR thanks to a tariff-free corridor for nearly new imports. Early adopters cluster in affluent Cairo suburbs where charging infrastructure co-develops with private-sector investment. CNG retrofits form a parallel low-carbon path, using subsidy reforms to cut running costs for high-mileage owners.

Hybrid models serve cautious buyers, blending conventional refueling familiarity with incremental efficiency gains. Diesel persists in commercial fleets where torque and range still outweigh environmental concerns. Collectively, these shifts diversify energy exposure across the Egyptian used car market, aligning with broader national sustainability goals.

By Sales Channel: Digital Transformation Accelerates

Offline dealerships held 63.18% of the Egyptian used car market size in 2024, valued for physical inspection and immediate delivery. Yet, online platforms clock a 7.08% CAGR as mobile-first millennials embrace end-to-end digital journeys. Hatla2ee’s suite of valuation tools, financing gateways, and doorstep delivery illustrates rising service integration [3]“Increasing Mobile Traffic and Dealer Integration,” Hatla2ee, hatla2ee.com.

Blended “click-and-brick” models dominate buyer preferences: research and credit pre-approval occur online, while final paperwork and handovers occur at partner showrooms. This hybrid reduces search friction and sustains offline dealer relevance, forging a complementary channel structure across the Egyptian used car market.

By Vehicle Age: Newer Vehicles Command Premium Growth

Models between 5-8 years captured 42.55% of the Egyptian used car market share in 2024, balancing price and reliability for mass buyers. Vehicles younger than 3 years, however, post the fastest 4.63% CAGR, propelled by OEM trade-ins and remaining factory warranties that reassure tech-savvy consumers. Bank lending caps on cars older than eight years funnel credit toward newer cohorts, indirectly steering demand upward.

EV import incentives confined to less than 3-year models further tip interest toward recent vintages. Older vehicles above eight years stay relevant for cash buyers and rural users but face headwinds from maintenance costs and restricted financing options, tempering growth within that tranche.

By Mileage: Low-Mileage Vehicles Drive Premium Growth

Inventory in the 20,001-50,000 km bracket held a 49.14% of the Egypt used car market share during 2024, mirroring standard replacement cycles. Yet cars with sub-20,000 km mileage grow quickest at 6.11% CAGR, prized for minimal wear and longer warranty tails. Digital verification tools reduce odometer fraud, enhancing confidence in low-mileage listings.

High-mileage vehicles appeal to commercial operators and budget-limited drivers who value function over aesthetics. Mileage segmentation thus provides a price-stratified ladder, sustaining liquidity across multiple buyer personas in the Egyptian used car market.

By Price Band: Mid-Market Segment Drives Growth

Transactions below USD 10,000 remained dominant, accounting for 54.46% of the Egyptian used car market's size in 2024, yet the USD 10,001-30,000 range accelerates at a 5.12% CAGR as middle-class earnings rise and installment credit spreads. Currency volatility nudges some shoppers to lock in value at mid-tier levels that balance desirable features with manageable debt loads.

Luxury transactions above USD 30,000 stay niche but stable, concentrated among corporate executives and expatriates in Cairo and Alexandria. Transparent pricing on digital platforms narrows negotiation bandwidth, equalizing access to information across all price bands.

Geography Analysis

Greater Cairo accounts for a significant share of Egypt's used car market activities, leveraging dense population, diversified employment, and the highest organized-dealer footprint. Superior inspection centers and faster title processing reduce transaction friction, creating virtuous cycles of inventory turnover and customer repeat rates.

Alexandria ranks next, benefiting from port-adjacent import flows and an industrial workforce that underpins steady demand for reliable personal transport. The Suez Canal corridor emerges as a growth node as logistics and free-zone projects elevate disposable income and road freight traffic, spurring both passenger and light-commercial-vehicle resale.

Upper Egypt markets remain volume light; buyers gravitate to older, low-priced units amid limited banking outreach. Red Sea governorates feature unique fleet demand from hospitality enterprises, motivating specialized dealers to stock low-mileage SUVs and vans suited to resort shuttle operations. Rural Nile Delta towns, driven by agricultural economies, sustain steady pickup and utility-vehicle turnover. Organized-dealer density tapers outside major metros, prolonging reliance on peer-to-peer sales. Nonetheless, government e-governance programs aim to unify title-transfer portals nationwide, potentially smoothing geographic disparities in the long term. For now, regional heterogeneity in income, infrastructure, and digital literacy keeps the Egypt used car market multifaceted.

Mordor Intelligence examines the used car market across diverse other regional markets as well, including Africa, while also offering granular country-level perspectives for Nigeria, Kenya, New Zealand, Norway, Myanmar, Switzerland, Sri Lanka, and Belgium and more.

Competitive Landscape

The Egyptian used car market remains moderately fragmented as unorganized sellers dominate volume, yet competitive gravity is shifting toward capital-backed platforms and dealer groups. Dubizzle’s February 2025 acquisition of Hatla2ee crowned a clear digital front-runner, combining extensive listings, advanced analytics, and integrated finance to lock in network advantages.

Mansour Automotive scales its “Trade-In” program to capture downstream resale profits while reinforcing new-car sales funnels. General Motors Egypt and Stellantis leverage local production lines to seed certified pre-owned pipelines and stabilize residual values, tightening synergy between manufacturing and remarketing arms.

Technology constitutes the chief battleground: AI-powered pricing, mobile-first customer journeys, and automated fraud detection differentiate contenders. White-space opportunities persist in rural market digitization, commercial vehicle leasing, and EV battery refurbishment. Market share realignment is expected as efficiency-seeking consumers migrate toward transparent, warranty-backed inventory, squeezing margins for informal actors.

Egypt Used Car Industry Leaders

Sylndr

Dubizzle Egypt (OLX Cars Egypt)

Fabrika (GB Auto)

Mansour Auto Trade

Abou Ghaly Motors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sylndr raised USD 15.7 million Series A funding to expand its tech-driven end-to-end platform.

- February 2025: Dubizzle acquired Hatla2ee, consolidating the nation’s largest digital automotive marketplace and accelerating ecosystem integration.

Egypt Used Car Market Report Scope

| Hatchbacks |

| Sedans |

| SUVs and MPVs |

| Organized |

| Unorganized |

| Gasoline |

| Diesel |

| Hybrid |

| Electric |

| Other Alternative Fuels |

| Online Platforms |

| Offline Dealerships |

| Below 3 Years |

| 3 - 5 Years |

| 5 - 8 Years |

| Above 8 Years |

| Less than 20,000 km |

| 20,001 - 50,000 km |

| Above 50,000 km |

| Less than USD 10,000 |

| USD 10,001 - USD 30,000 |

| Above USD 30,000 |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| SUVs and MPVs | |

| By Vendor Type | Organized |

| Unorganized | |

| By Fuel Type | Gasoline |

| Diesel | |

| Hybrid | |

| Electric | |

| Other Alternative Fuels | |

| By Sales Channel | Online Platforms |

| Offline Dealerships | |

| By Vehicle Age | Below 3 Years |

| 3 - 5 Years | |

| 5 - 8 Years | |

| Above 8 Years | |

| By Mileage | Less than 20,000 km |

| 20,001 - 50,000 km | |

| Above 50,000 km | |

| By Price Band | Less than USD 10,000 |

| USD 10,001 - USD 30,000 | |

| Above USD 30,000 |

Key Questions Answered in the Report

How large is the Egyptian used car market in 2025?

The Egyptian used car market size is USD 7.53 billion in 2025 and is projected to reach USD 9.20 billion by 2030.

What is the forecast CAGR for used-car sales in Egypt?

The sector is expected to post a 4.09% CAGR between 2025 and 2030.

Which vehicle segment is growing fastest in Egypt?

SUVs and MPVs exhibit the highest growth, advancing at a 4.97% CAGR through 2030.

How dominant are online platforms in Egyptian used-car sales?

Offline dealerships still hold 63.18% share, but online channels are expanding rapidly at a 7.08% CAGR.

Page last updated on: