Kubernetes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

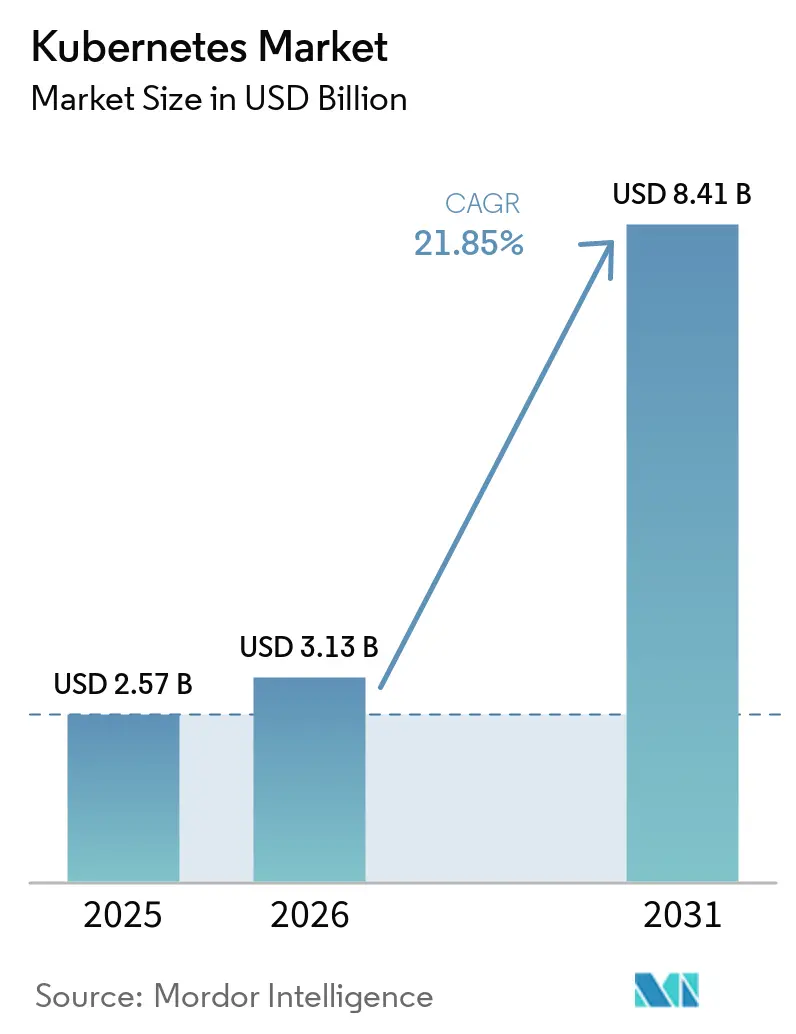

| Market Size (2026) | USD 3.13 Billion |

| Market Size (2031) | USD 8.41 Billion |

| Growth Rate (2026 - 2031) | 21.85% CAGR |

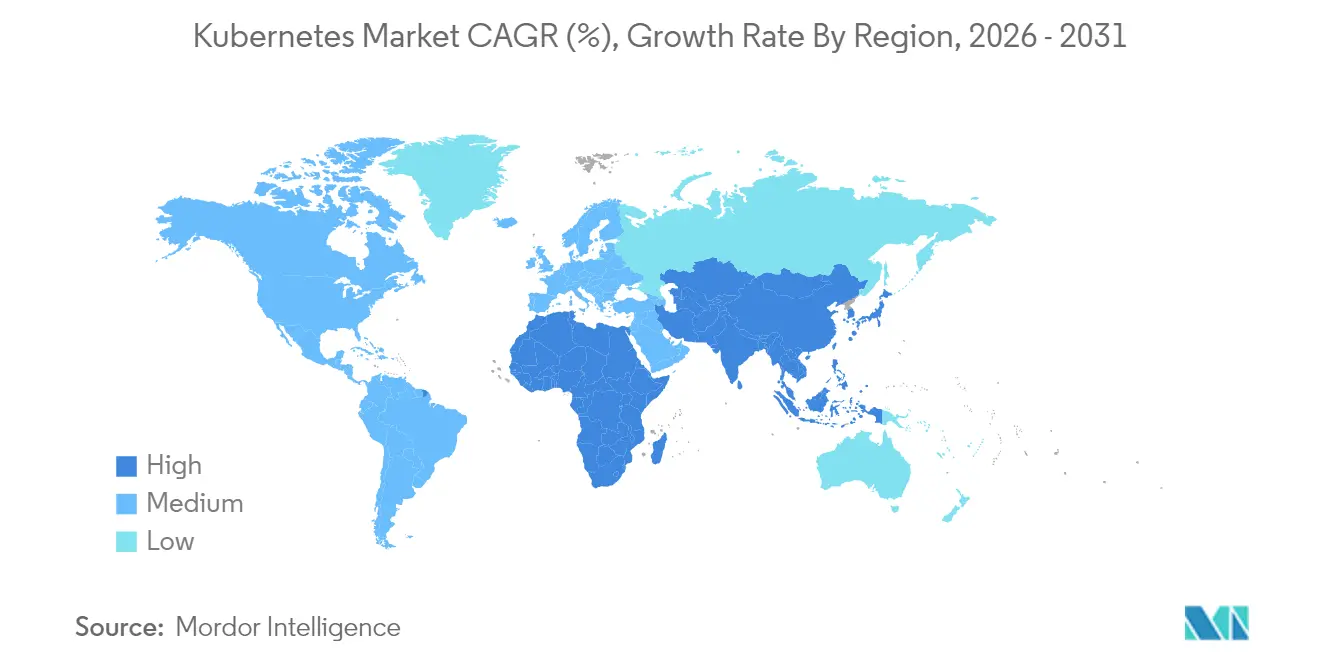

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

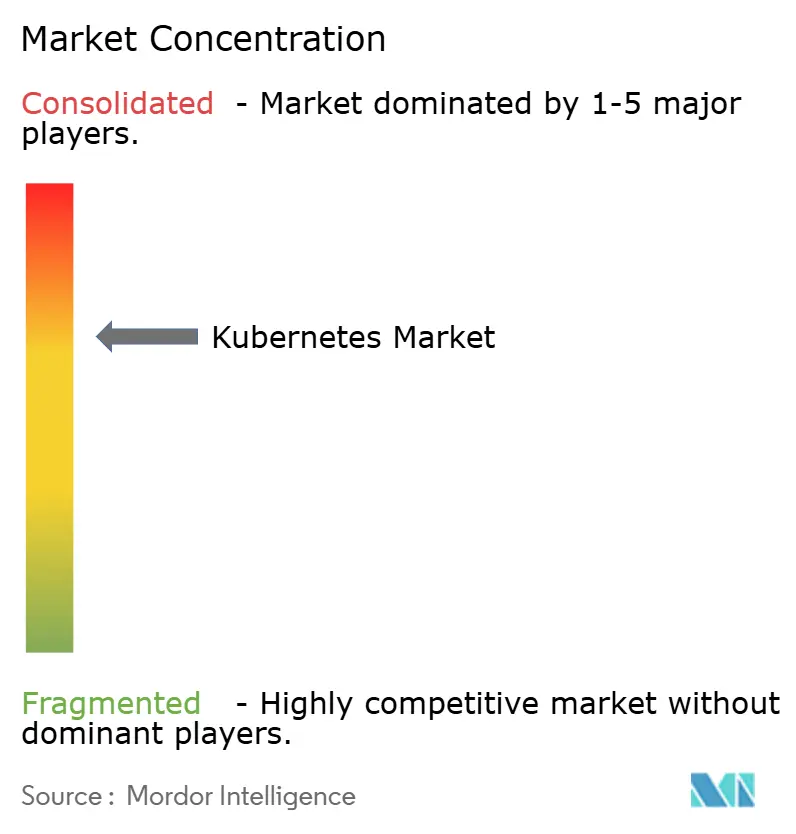

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kubernetes Market Analysis by Mordor Intelligence

The Kubernetes market size is expected to grow from USD 2.57 billion in 2025 to USD 3.13 billion in 2026 and is forecast to reach USD 8.41 billion by 2031 at 21.85% CAGR over 2026-2031. The combination of microservices adoption, escalating AI/ML workloads, and hybrid-plus-multi-cloud strategies is accelerating enterprise uptake. Nearly every large organization now treats Kubernetes as its default container orchestrator, and 96% of enterprises report using or evaluating the platform for production workloads[1]IBM, “State of Kubernetes 2024,” ibm.com. Managed offerings account for most new deployments as buyers prioritize turnkey operations, security hardening, and compliance tooling. North America commands the largest regional position while Asia-Pacific posts the fastest growth, aided by digital transformation mandates and cloud infrastructure investments. Competitive pressure remains intense as hyperscale clouds, platform specialists, and open-source vendors race to simplify operations and bundle advanced controls, especially for AI pipelines and edge roll-outs.

Key Report Takeaways

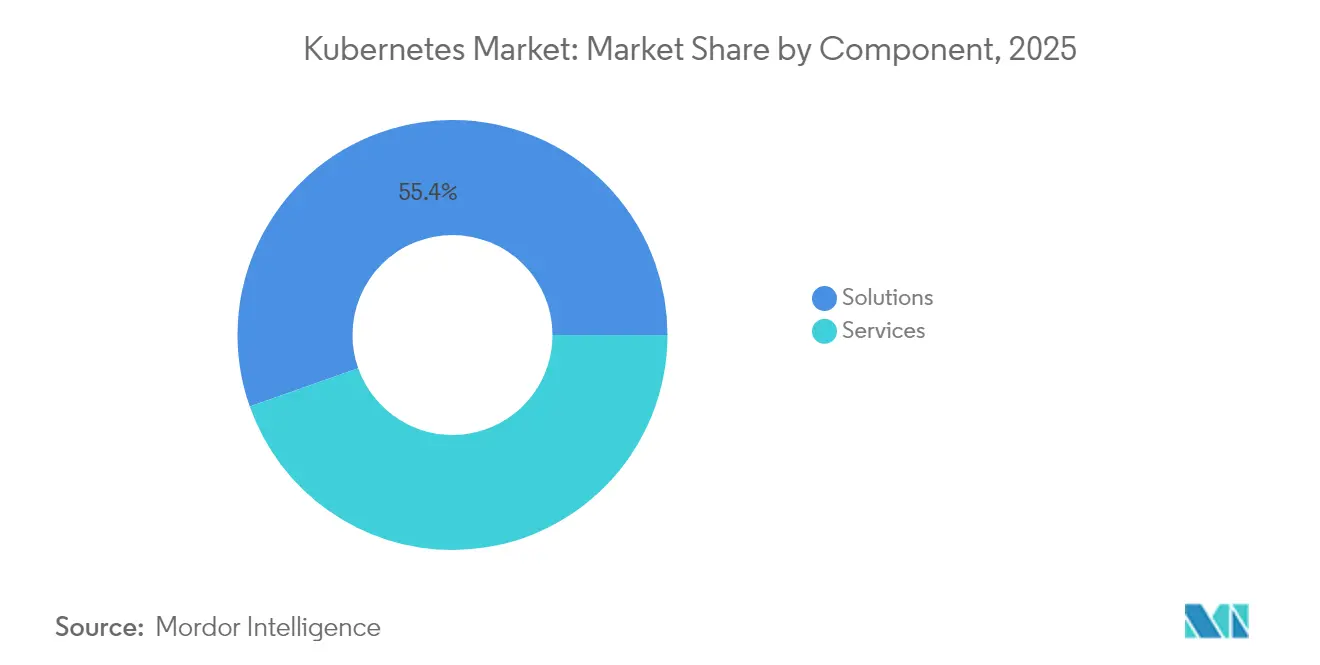

- By component, Solutions led with 55.40% of the Kubernetes market share in 2025; Services are set to expand at a 23.3% CAGR through 2031.

- By deployment model, Managed Kubernetes captured 62.30% of the Kubernetes market share in 2025, while Multi-Cloud Managed options are forecast to rise at 22.4% CAGR.

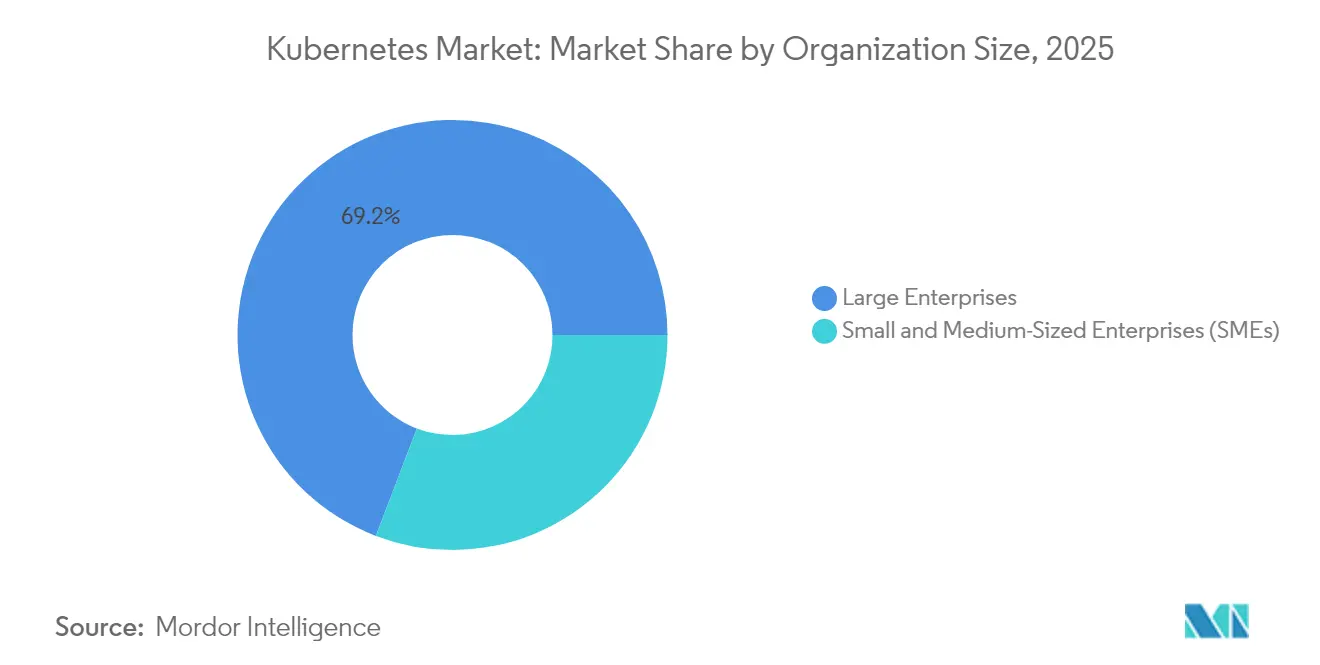

- By organization size, Large Enterprises held 69.20% of the Kubernetes market share in 2025, whereas SMEs are projected to grow at 22.9% CAGR to 2031.

- By end-user vertical, Information Technology and Telecom generated 32.60% revenue in 2025; Healthcare is on track for a 22.2% CAGR.

- By geography, North America commanded 36.40% of the Kubernetes market in 2025 and Asia-Pacific is set for a 22.6% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kubernetes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advent of Microservices | +5.4% | North America and Europe more pronounced | Medium term (2-4 years) |

| Increased Adoption of AI and ML Workloads | +4.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing Demand for Managed Kubernetes Services | +3.9% | Global, sharper in talent-scarce regions | Short term (≤ 2 years) |

| Expansion of Hybrid and Multi-Cloud Strategies | +3.5% | Strongest in North America and Europe | Medium term (2-4 years) |

| Edge-Computing Adoption with Lightweight K8s Distros | +2.9% | Asia-Pacific, manufacturing hubs, telecom-heavy markets | Medium term (2-4 years) |

| Kubernetes-native FinOps Automation Reducing TCO | +2.6% | Global enterprise cloud markets | Short term to medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Advent of Microservices

Organizations are dismantling monoliths in favor of smaller, independently deployable services that demand sophisticated orchestration, and Kubernetes excels at that role. Eighty percent of enterprises plan to build most new applications on cloud-native stacks within five years. Purpose-built design patterns such as sidecar, ambassador, and adapter are mainstream, improving modularity and maintainability. As this design shift continues, the Kubernetes market becomes a strategic backbone for faster release cycles and business agility, transforming platform-engineering priorities across industries.

Increased Adoption of AI and ML Workloads

Compute-intensive AI initiatives benefit from Kubernetes functions such as node autoscaling, GPU scheduling, and service resilience. More than half of surveyed enterprises already run AI/ML workloads in Kubernetes clusters. Sector-specific tools like Kubeflow streamline model training, while a Google, ByteDance, Red Hat collaboration has optimized load balancing and model-server performance for large-language-model inference[2]Red Hat, “Optimizing LLM Inference on Kubernetes,” redhat.com. The result is a wider addressable base for AI-ready infrastructure and an expanding Kubernetes market.

Growing Demand for Managed Kubernetes Services

Operational complexity and a shortage of in-house skills drive enterprises toward managed offerings. Amazon EKS alone holds 30% of the hosted-service slice and reports more than 2 million active customers. Managed providers promise cost savings of up to 40% and uptime gains of 35% by bundling security, compliance, and automated upgrades. As deployments scale across multiple clouds, turnkey services will keep accelerating the Kubernetes market trajectory.

Expansion of Hybrid and Multi-Cloud Strategies

Enterprises spreading workloads across private data centers and more than one public cloud rely on Kubernetes for portability. Google Anthos, AWS EKS Anywhere, and Azure Arc now enable centralized control of distributed clusters. Demand for these wrapper platforms is pushing multi-cloud managed solutions growth, reinforcing Kubernetes market relevance for compliance, latency, and cost-optimization goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Skilled Talent Pool | -2.2% | Higher pressure in emerging markets | Short term (≤ 2 years) |

| Security and Compliance Complexities | -3.1% | Global, acute in regulated sectors | Medium term (2-4 years) |

| Control-Plane Cost Escalation under Autoscaling | -1.8% | Cloud-intensive enterprise markets globally | Medium term (2-4 years) |

| Hyperscaler Dominance Limits OSS Monetisation | -2.4% | North America and Europe open-source ecosystems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Skilled Talent Pool

Specialized know-how remains scarce as 37% of IT leaders report a skills gap across DevOps and DevSecOps. The steep learning curve fuels the rise of dedicated platform-engineering teams and encourages investment in automation. Enterprises also lean on managed service providers to bridge expertise gaps while modernizing workloads previously tied to legacy virtualization stacks.

Security and Compliance Complexities

Sixty-seven percent of enterprises cite security concerns that delay releases, and 37% have suffered revenue loss from incidents. New Azure Kubernetes Service clusters can face probing within 18 minutes of exposure. Companies are onboarding zero-trust controls and network-policy enforcement, complemented by improvements to Gateway API for granular access oversight. Continuous scanning and compliance dashboards are becoming table stakes as regulated industries adopt Kubernetes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Outpace Solutions Growth

Solutions still form the largest slice at 55.40% of the Kubernetes market in 2025, covering core distributions and management add-ons. The Services arm, however, is advancing at a 23.3% CAGR as enterprises seek migration blueprints, performance tuning, and continuous compliance advice. A rising number of consulting engagements focus on vertical use-cases—healthcare, finance, telecommunications - where governance requirements are strict and downtime is intolerable. The Kubernetes market for services is expected to more than double by 2031 as certification programs and domain-specific frameworks attract new integrators.

The surge also reflects widening complexity between Kubernetes feature sets and operator know-how. Cloud4C notes that 59% of adopters deem compliance their chief pain point, creating a pull for specialized audit and remediation services. Managed Kubernetes subscriptions further accelerate consumption by shifting SLA enforcement and upgrade chains to vendors, a pattern especially resonant with resource-constrained teams wanting predictable cost envelopes.

By Deployment Model: Multi-Cloud Momentum Accelerates

Managed offerings dominate with 62.30% of current spend, underpinned by the hyperscalers’ managed Kubernetes services. Growth now clusters around multi-cloud managed variants, projected to climb at 22.4% CAGR. Organizations balancing latency, sovereignty, and spending spread workloads across AWS, Azure, Google Cloud, and on-premises assets, turning Kubernetes into the neutrality layer for policy and placement. Kubernetes market for multi-cloud deployments is reinforced as enterprises insist on avoiding single-provider lock-in and pursue optimized utilization.

Self-hosted clusters retain relevance among firms with bespoke security mandates or mainframe adjacency. Hybrid models serve as stepping-stones, letting teams containerize critical applications internally while bursting peaks to public clouds. Tool vendors are rolling out single-pane dashboards, GitOps pipelines, and policy engines that abstract differences among clouds, a move that compresses operational overhead and widens the Kubernetes market.

By Organization Size: SMEs Accelerate Adoption Curve

Large Enterprises captured 69.20% of outlays in 2025, but SMEs are closing the gap at a 22.9% CAGR. Turnkey Kubernetes-as-a-Service options lower barriers by bundling automated patching, security scanning, and application templates. SMEs adopting through consulting interventions have cut operating costs by up to 40% and improved uptime by 35%.

In parallel, simplified dashboards and low-code policy builders enable smaller teams to operate clusters with minimal headcount. Training programs and community editions of commercial platforms ease on-ramp complexity. As these levers expand, Kubernetes market growth among SMEs is expected to exceed large-enterprise growth, broadening vendor addressable scope.

By End-User Vertical: Healthcare Emerges as Growth Leader

Information Technology and Telecom led spending with 32.60% of 2025 revenue, leveraging Kubernetes for CI/CD acceleration and SaaS uptime. Healthcare, however, posts the fastest CAGR at 22.2% as digital health workloads demand elastic, standards-compliant infrastructure. Hospitals deploying container orchestration report lower system downtime for electronic health records and telemedicine portals while meeting HIPAA and data-sovereignty rules.

Banks and insurers follow closely, driven by the need to handle bursty payment volumes and regulatory audits. Manufacturers integrate Kubernetes into Industry 4.0 stacks for predictive maintenance and IoT analytics, capitalizing on lightweight edge distributions. Public-sector agencies, mindful of sovereignty and budget constraints, embrace open-source tooling to modernize citizen services. Each niche elevates Kubernetes market relevance by showcasing domain-specific performance and resilience gains.

Geography Analysis

North America secured 36.40% of global revenue in 2025, anchored by the United States, which accounts for more than half of Kubernetes users worldwide. Hyperscale cloud footprints, early-mover enterprises, and deep developer communities sustain regional leadership. AI-infused workloads, especially in finance and retail, intensify Kubernetes adoption, and a patchwork of sectoral regulations (HIPAA, FISMA) spurs investment in security automation and policy gateways. Market participants here increasingly deploy multi-cloud blueprints, making Kubernetes the universal substrate for workload portability.

Asia-Pacific is the fastest-growing region with a 22.6% CAGR forecast for 2026-2031. Widespread digitization, 5G buildouts, and cloud data-center expansion in China, India, and Japan ignite demand. CAST AI’s move into India exemplifies provider momentum in the region. Domestic giants such as Alibaba Cloud promote tailored Kubernetes stacks that satisfy local compliance, sustaining momentum. Manufacturing use-cases—smart factories, supply-chain telemetry—further contribute to the Kubernetes market expansion.

Europe commands a substantial slice, buoyed by GDPR-focused security spending and strong open-source culture. Enterprises in Germany, the United Kingdom, and France emphasize hybrid architectures to balance sovereignty and agility. Kubernetes adoption inside the banking and telco segments supports core system modernization. Community collaboration, including Cloud Native Computing Foundation (CNCF) meetups and code events, nurtures a robust contributor base that accelerates enterprise trust. Emerging hubs in the Middle East and Africa and South America, while smaller, display steady uptake as localized cloud availability zones come online, further widening the global Kubernetes market footprint.

Competitive Landscape

At the infrastructure tier, AWS, Microsoft Azure, and Google Cloud collectively hold more than 60% share of managed Kubernetes deployments, driven by deep integration with identity, network, and AI services. AWS EKS alone covers 30% of the managed segment and serves over 2 million customers. Hyperscalers differentiate through AI-optimized nodes, serverless profiles, and cost-optimization calculators.

Specialist vendors such as Red Hat (OpenShift), Rancher (SUSE), and VMware Tanzu focus on enterprise-grade policy engines and multi-cluster governance. January 2025 saw AWS, Azure, and Google jointly unveil Kube Resource Orchestrator to streamline application bundles and lessen YAML complexity. Red Hat introduced OpenShift Lightspeed, an AI assistant that curates best practice manifests and mitigates skills shortages.

White-space competition centers on verticalized offerings for healthcare and finance, where compliance overlays can be monetized. Beyond core orchestration, startups deliver FinOps, security, and cost-optimization modules tightly integrated with Kubernetes APIs. Partnerships between observability suites and platform vendors aim to embed AI-driven remediation directly into cluster operations. As consolidation looms, mergers and acquisitions activity is likely to center on edge-optimized runtimes and policy-driven continuous delivery tooling, influencing overall Kubernetes market structure.

Kubernetes Industry Leaders

Google LLC

Microsoft Corporation

Red Hat, Inc.

IBM Corporation

Docker, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Red Hat shipped RHEL 10 with Red Hat AI Inference Server and Advanced Developer Suite to streamline hybrid-cloud AI operations on Kubernetes.

- May 2025: Plural introduced compliance reports that automate Kubernetes configuration checks against industry benchmarks.

- April 2025: Microsoft contributed new open-source tools at KubeCon + CloudNativeCon Europe to improve AKS security and upgrade automation.

- April 2025: Tigera enhanced Calico to bolster visibility and network policy enforcement across large-scale Kubernetes deployments.

- April 2025: The Kubernetes project released version 1.33, known as Octarine, emphasizing security hardening and AI/ML workload support.

- February 2025: CyberArk and Red Hat hosted a webinar outlining 2025 Kubernetes security best practices based on industry survey insights.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global Kubernetes market as the aggregate value generated when vendors sell commercial Kubernetes distributions, subscription-based managed clusters, enterprise support contracts, and billable consulting or training that is purpose-built for Kubernetes workload deployment, scaling, and lifecycle management across public cloud, hybrid, and on-premise environments.

Scope Exclusion: Revenue from container platforms that operate without a Kubernetes control plane, stand-alone container security tools, and physical server hardware is not counted.

Segmentation Overview

- By Component

- Solutions

- Services

- Managed Services

- Consulting and Support Services

- By Deployment Model

- Self-Hosted Kubernetes

- On-Premise

- Hybrid

- Managed Kubernetes

- Cloud-based Managed

- Multi-Cloud Managed

- Self-Hosted Kubernetes

- By Organization Size

- Small and Medium-Sized Enterprises (SMEs)

- Large Enterprises

- By End-User Vertical

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare

- Media and Entertainment

- Information Technology (IT) and Telecom

- Manufacturing

- Retail

- Government and Public Sector

- Other Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed cloud architects, platform engineering leads, and channel partners across North America, Europe, and fast-growing Asia Pacific to verify pricing tiers, average cluster counts per enterprise, and adoption hurdles. Follow-up surveys with small and mid-size enterprises helped us refine penetration assumptions and check regional variance before locking growth drivers.

Desk Research

We began by mapping the addressable market using open intelligence from the Cloud-Native Computing Foundation, CNCF Annual Survey dashboards, Kubernetes Project release metrics, United States Bureau of Labor Statistics cloud-skills datasets, and International Telecommunication Union cloud traffic indices. Complementary perspectives were gathered from regional trade groups such as the Asia Cloud Computing Association and Europe's Digital Economy reports, as well as company filings and investor presentations that disclose managed-cluster subscriber counts. Our team also accessed D&B Hoovers for vendor financials, Dow Jones Factiva for deal flow, and Questel for patent momentum around container orchestration. These publicly available and paid inputs created the foundational supply-demand map; however, the sources listed are illustrative, and many other references were reviewed during data validation.

Market-Sizing & Forecasting

A calibrated top-down model starts with enterprise software spend, then applies container penetration ratios, cluster density, and average per-cluster spend to size 2024 base revenues, which are subsequently checked with selective bottom-up roll-ups of leading provider disclosures and channel checks. Key variables like cloud infrastructure outlay, DevOps workforce expansion, managed service price erosion, and regulatory cloud mandates feed a multivariate regression that projects demand through 2030. When bottom-up estimates diverge beyond a 7 percent band, we adjust addressable use-case weights before finalizing totals.

Data Validation & Update Cycle

Outputs pass a multi-step peer review where anomalies are flagged, re-contact interviews are triggered for clarifications, and variances against independent market indices are resolved. Reports refresh every twelve months and are reopened earlier when material events occur so clients receive the latest read.

Why Mordor's Kubernetes Baseline Commands Confidence

Published figures often differ because firms choose dissimilar service scopes, currency conversions, or refresh cadences. Our disciplined scope alignment, annual refresh, and dual-path modeling make the baseline dependable for planners who cannot gamble on unvetted assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.57 B (2025) | Mordor Intelligence | |

| USD 2.11 B (2024) | Regional Consultancy A | Omits professional services and uses static price points |

| USD 2.15 B (2025) | Trade Journal B | Counts only platform revenue, excludes managed clusters |

| USD 2.95 B (2025) | Global Consultancy C | Relies on vendor press releases without penetration cross-checks |

The comparison shows how narrower scopes or unchecked inputs compress or inflate totals, whereas Mordor's model ties every dollar to transparent variables that retrace, update, and defend with confidence.

Key Questions Answered in the Report

What is the current Kubernetes market size and growth outlook?

The Kubernetes market size is USD 3.13 billion in 2026 and is expected to reach USD 8.41 billion by 2031, expanding at a 21.85% CAGR.

Which segment of the Kubernetes market is growing fastest?

Managed multi-cloud deployments show the quickest expansion at a 22.4% CAGR as enterprises pursue portability and cost optimization.

Why are Services gaining momentum over Solutions in the Kubernetes market?

Rising complexity, compliance requirements, and skill shortages push enterprises to seek consulting, managed operations, and continuous support, propelling services at a 23.3% CAGR.

Which region offers the highest growth potential for Kubernetes vendors?

Asia-Pacific leads with a 22.6% CAGR thanks to large-scale digital transformation and expanding cloud infrastructure in China, India, and Japan.

What are the key restraints companies face with Kubernetes adoption?

A shortage of skilled talent and heightened security-plus-compliance demands remain the leading barriers, shaving 2.2% and 3.1% off forecast CAGR respectively.

How concentrated is competition within the Kubernetes industry?

The market concentration score is 7, indicating that while hyperscalers command a majority of managed-service revenue, a sizable ecosystem of niche players sustains a competitive landscape.

Page last updated on: