Kaolin Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

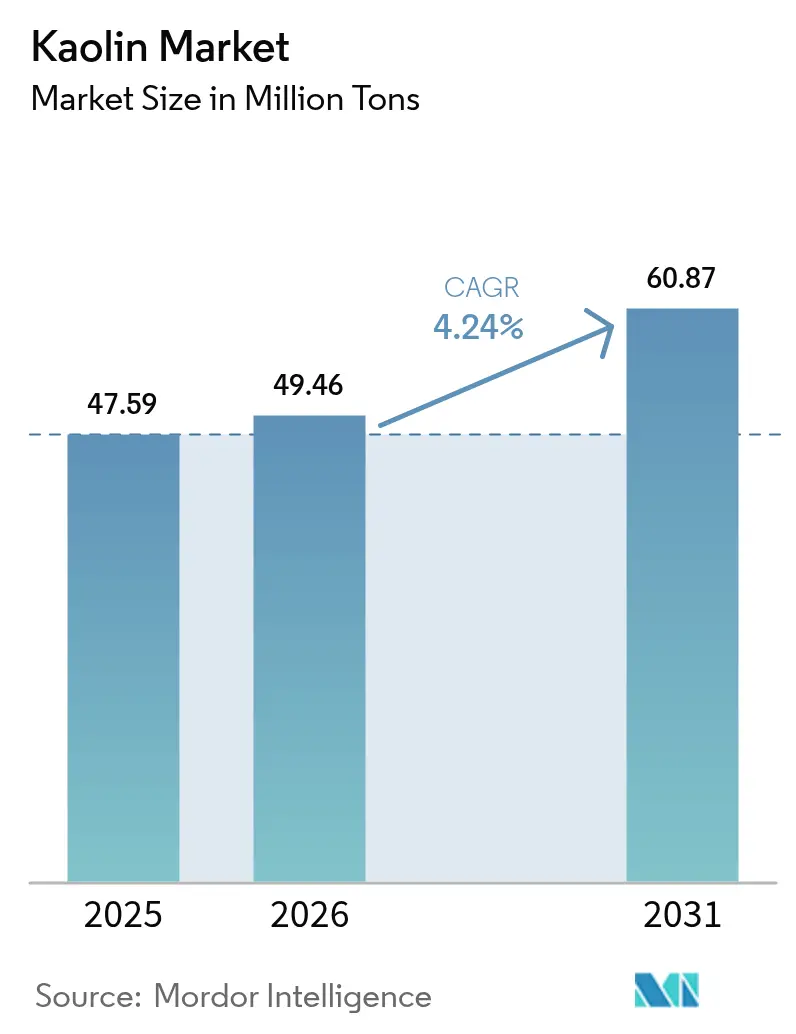

| Market Volume (2026) | 49.46 Million tons |

| Market Volume (2031) | 60.87 Million tons |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

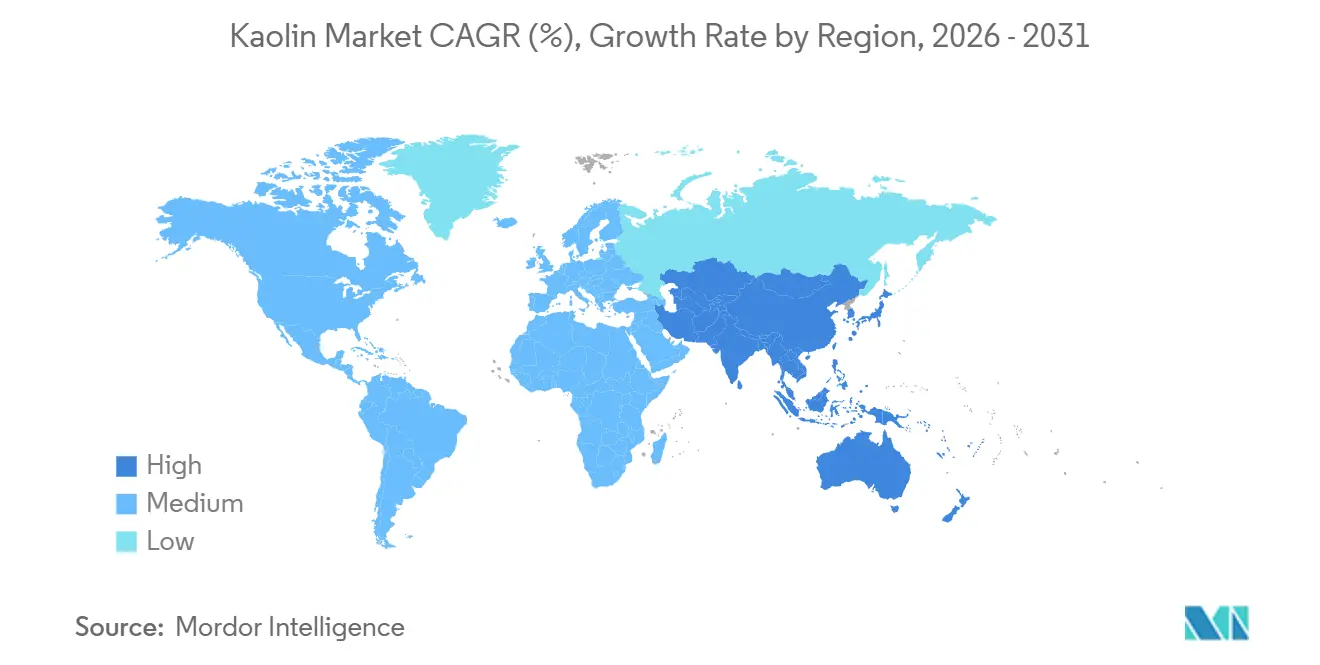

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kaolin Market Analysis by Mordor Intelligence

The Kaolin Market size is expected to grow from 47.59 Million tons in 2025 to 49.46 Million tons in 2026 and is forecast to reach 60.87 Million tons by 2031 at 4.24% CAGR over 2026-2031. Asia-Pacific’s structural pivot toward sanitary-ware and tile manufacturing, battery-separator adoption in electric-vehicle supply chains, and ongoing substitution of titanium dioxide in architectural coatings anchor the upward trajectory of the kaolin market. Processed grades command price premiums because magnetic separation, calcination, and surface treatments yield high-brightness products required in advanced ceramics, packaging papers, and Li-ion battery components. Cost inflation in energy markets raises barriers for European calciners, handing a comparative advantage to North American and Asian producers with cheaper feedstocks. Private-equity interest, exemplified by Platinum Equity’s February 2024 acquisition of Imerys Performance Minerals Americas, is reshaping competitive dynamics by prioritizing operational efficiencies and cash generation. Environmental compliance—ranging from EPA NPDES effluent limits to EU carbon-pricing schemes—remains a decisive factor that can either accelerate beneficiation investments or delay greenfield mines, depending on geography.

Key Report Takeaways

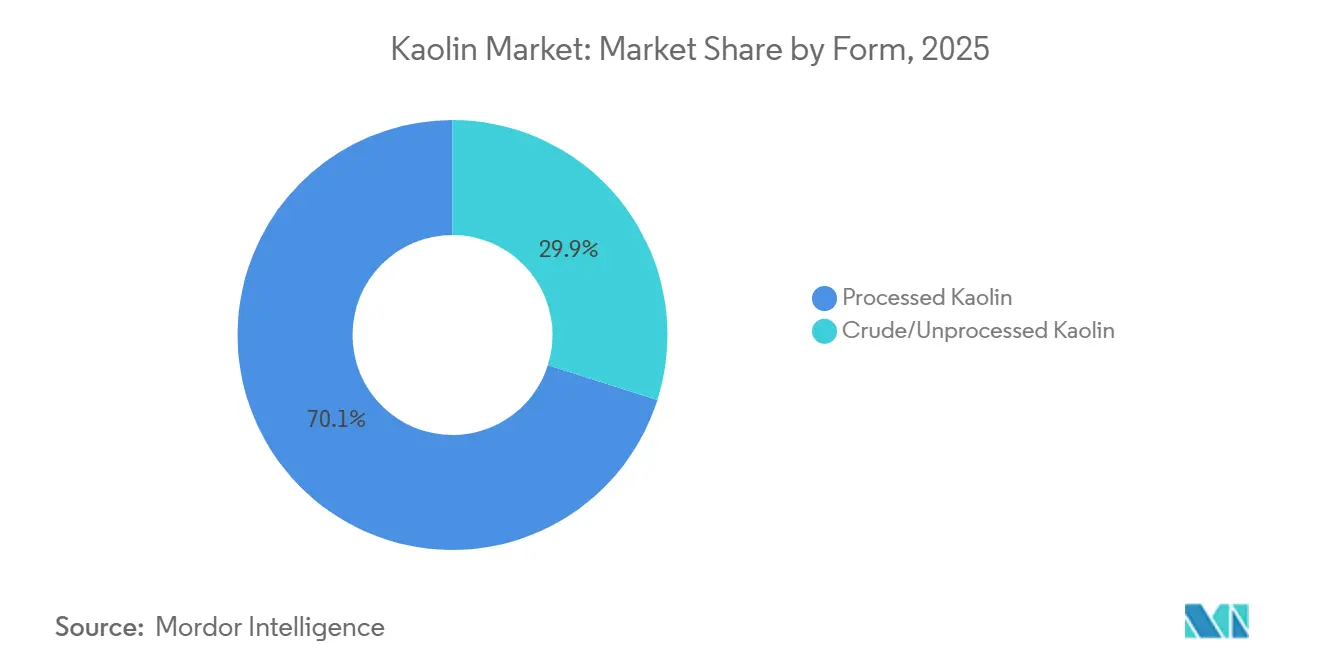

- By form, processed kaolin led with 70.12% of the kaolin market share in 2025, while crude/unprocessed kaolin recorded the fastest projected CAGR at a 4.89% through 2031.

- By grade, hydrous kaolin accounted for 55.45% of the kaolin market share in 2025 and calcined kaolin is advancing at a 4.75% CAGR during 2026-2031.

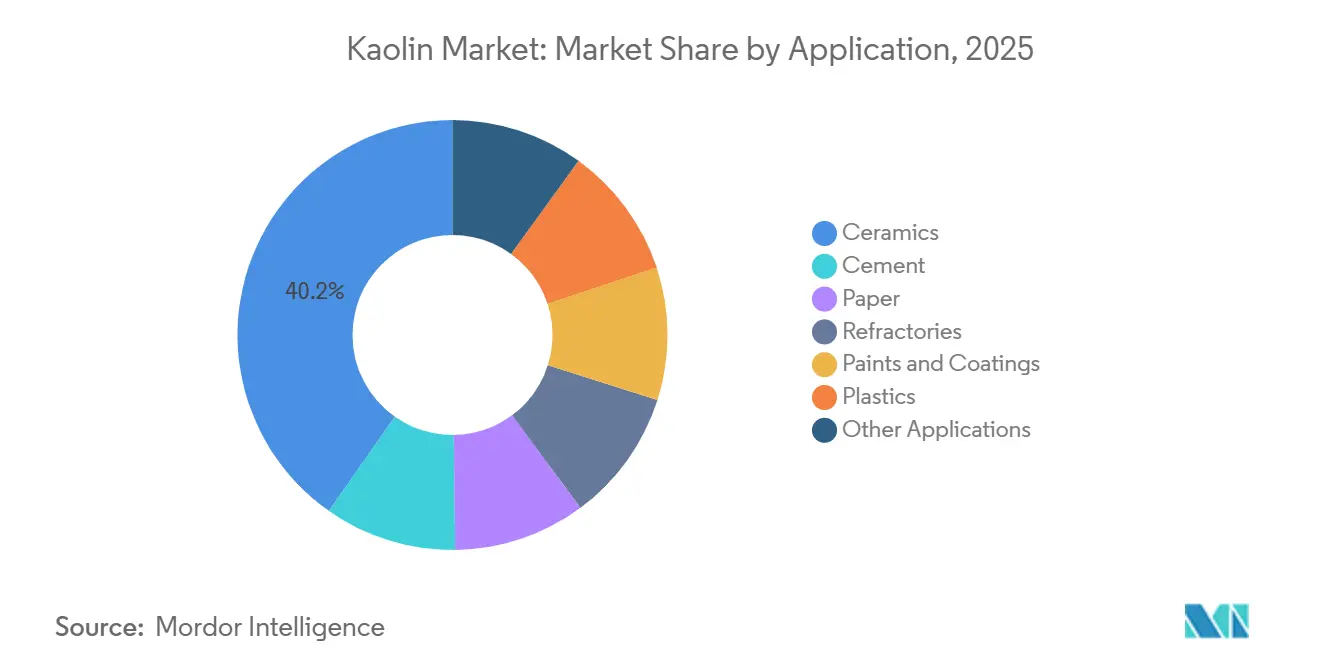

- By application, ceramics held 40.23% of the kaolin market share in 2025 and is forecast to expand at a 4.97% CAGR to 2031.

- By geography, Asia-Pacific captured 43.26% of the kaolin market share in 2025 and is forecast to grow at a 4.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kaolin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming sanitary-ware and tile manufacturing | +1.8% | Asia-Pacific core, spillover to MEA | Short term (≤ 2 years) |

| Shift to high-brightness packaging paper | +0.9% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Growing demand from paper and rubber industries | +0.7% | Global | Short term (≤ 2 years) |

| Cosmetics and personal-care industry growth | +0.4% | Global, concentrated in Asia-Pacific, North America, EU | Medium term (2-4 years) |

| Rapid adoption of calcined kaolin in Li-ion battery separator coatings | +0.6% | Asia-Pacific, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Booming Sanitary-Ware and Tile Manufacturing

China’s tile output exceeds 5 billion m² annually, consuming 12-15 million tons of kaolin, while India’s march toward 3 billion m² by 2026 could lift domestic demand by another 1.5-2 million tons. The mismatch between India’s 8.3 million tons of crude extraction and just 73,000 tons of processing capacity forces tile makers to import high-brightness grades from Malaysia and Indonesia, inflating landed costs by 12-18%. Indonesia and Vietnam are scaling sanitary-ware output to serve mega-projects in the Middle-East, including Saudi Vision 2030 requirements for 8-10 million fixtures. Premium vitreous-china lines require kaolin with less than 1.5% Fe₂O₃, tightening regional supply and driving spot prices for 90%+ brightness grades 22-25% higher since early 2024. Russia’s own shift toward import substitution added another 1 million tons of kaolin demand between 2019 and 2022.

Shift to High-Brightness Packaging Paper

Phasing out PFAS in food-contact paper propels mills to thicken mineral coatings for barrier performance[1]U.S. Environmental Protection Agency, “PFAS Roadmap for Food Packaging,” epa.gov . Kaolin’s plate-like structure enhances printability, but digital inkjet now represents 35-40% of packaging print volume and prefers calcium carbonate’s greater opacity, trimming kaolin’s share to 50-55% in 2025. Delaminated kaolin, just 8-10% of total volume, earns 15-20% premiums for luxury paper stocks, specifically in cosmetics and spirits packaging. Hybrid kaolin-carbonate blends reduced pure-kaolin coat weights by roughly one-third in U.S. and EU mills; however, new Asian machines still specify kaolin-heavy formulations due to sparse carbonate supply chains.

Growing Demand from Paper and Rubber Industries

Global tire output of 1.8 billion units incorporates 3-4 million tons of kaolin, mainly as a semi-reinforcing filler that improves tear and abrasion resistance without the high cost of precipitated silica. Electric-vehicle tires load more kaolin to offset vehicle lightweighting trends. India’s tire sector, rising 7-9% annually, sources from domestic suppliers Ashapura and 20 Microns, which export up to half their kaolin output to Southeast Asia. Specialty paper grades—filtration, medical packaging—need calcined kaolin for low abrasivity, cushioning the kaolin market against graphic-paper declines in Europe and North America.

Rapid Adoption of Calcined Kaolin in Li-ion Battery Separator Coatings

Ceramic-coated separators raise thermal stability and block dendrites in high-energy cells. Calcined kaolin costs USD 800-1,200 per ton versus alumina at USD 1,500-2,200, offering gigafactories a cheaper pathway to meet IEC 62660 safety norms. Facilities in Poland, Michigan, and Jiangsu are qualifying 3-5 g/m² coatings that could need 50,000-. Halloysite sourced from Idaho is also under pilot trials, but volumes remain below 5,000 tons per year.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy intensity and cost inflation in calcination | -0.8% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Stringent mine-site environmental permitting | -0.4% | North America, Europe, Australia | Long term (≥ 4 years) |

| Substitution risk from high-opacity calcium carbonates in digital-print papers | -0.4% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Energy Intensity and Cost Inflation in Calcination

Flash calcination needs 1.2-1.5 MMBtu per ton, leaving producers exposed to natural-gas volatility. Europe’s TTF prices hovered at EUR 35-45 / MWh in 2025, up from EUR 15-20 pre-2022, forcing Sibelco and Imerys to idle 15-20% capacity or raise prices 15-20%. Carbon costs under the EU-ETS add EUR 10-15 per ton of calcined kaolin. U.S. PPI data show kaolin prices rising 18.6% between December 2022 and September 2025 as utilities passed through surcharges. Customers resist further hikes, accelerating partial substitution by calcium carbonate.

Stringent Mine-Site Environmental Permitting

EPA NPDES permits cap TSS at 30 mg/L and selenium at 5 µg/L, adding USD 5-10 million in clarifiers and RO systems per U.S. mine. EU REACH bans nonylphenol ethoxylate dispersants, driving up chemical costs 20-30% and trimming throughput 5-8%. Brazil’s Amazon deposits remain stranded because of indigenous land rights protections despite 200-300 million tons of reserves[2]Brazilian Institute of Environment, “Indigenous Land Mining Regulations,” ibama.gov.br . Permitting stretches 3-5 years for U.S. greenfields, delaying supply and favoring incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Processed Kaolin Commands Premium as Beneficiation Scales

Processed kaolin led the kaolin market size with 70.12% share in 2025, whereas crude/unprocessed kaolin is expanding at a faster 4.89% CAGR to 2031. India’s huge 8.3 million tons of crude output contrasts with scarce domestic processing, compelling tile makers to pay import premiums and highlighting a structural arbitrage within the kaolin market. Beneficiation investments by EICL and 20 Microns will add 200,000-300,000 tons of processed capacity by 2027.

Processed kaolin captures premium end uses—battery separators, high-brightness packaging, cosmetics—because multi-stage magnetic separation, bleaching, and spray drying deliver more than 85% brightness and less than 1% Fe₂O₃. Crude kaolin serves low-end bricks, cement, and agriculture, but is becoming attractive for backward integration in emerging markets craving feedstock security. China’s imports of Ukrainian and Russian crude plunged 40-50% after 2022 sanctions, redirecting flows from Australia and Indonesia and tightening the regional kaolin market.

By Grade: Calcined Kaolin Gains as Battery and Specialty Applications Expand

Hydrous kaolin still controlled 55.45% of the kaolin market share in 2025, but calcined kaolin is outpacing at 4.75% CAGR thanks to batteries and high-opacity coatings. Converting hydrous to calcined at 1,000-1,100 °C removes bound water and lifts brightness to 90-95%, suiting exacting paints and Li-ion separators.

Delaminated and surface-treated grades hold double-digit price premiums for luxury packaging and engineering plastics. Europe’s energy shock idled up to 20% of calcination in 2024-2025, shifting capacity growth toward the U.S. Gulf and Asia, where gas is cheaper. IEC 62660 battery norms should lift calcined-kaolin penetration in EV cells from 30-35% in 2024 to roughly 60-65% by 2027. Hydrous grades face margin pressure from calcium-carbonate substitution in digital-print papers, compelling producers to adopt particle-size control and specialty coatings to defend share within the kaolin market.

By Application: Ceramics Lead While Battery Coatings Emerge

Ceramics accounted for 40.23% of the kaolin market size in 2025 and will climb 4.97% CAGR to 2031. Asia’s urban build-out underpins this lead, with India and China alone adding over 3 billion m² of tile capacity by 2026. Paper demand is declining as graphic grades shrink, but specialty filtration and medical packaging mitigate the drag.

Refractories are linked to steel demand, especially in China, where mullite formation is critical for blast furnaces. Paints substitute calcined kaolin for pricey titanium dioxide, saving 8-12% on formulation cost. Plastics and cement admixtures grow on the back of lightweighting and green-building codes, while cosmetics rise as talc exits some SKUs. Battery separators are expected to add incremental calcined-kaolin demand by 2031.

Geography Analysis

Asia-Pacific commanded 43.26% of the kaolin market in 2025 and is projected to expand at 4.94% CAGR through 2031. China transitions toward higher-purity sanitary-ware and advanced ceramics, pushing brightness premiums up 22-25% since early 2024. India is closing its beneficiation gap via 300,000 tons of new capacity by 2027, aiming to cut import premiums of 12-18%. Japan and South Korea import high-purity grades for electronic substrates, pulling supply from the U.S. and Australia.

In North America, the Georgia kaolin belt anchors domestic supply, exporting 1.6-1.8 million tons to China, Mexico, and Japan. KaMin LLC’s formation after a EUR 1.43 billion carve-out underscores private-equity bets on mature but cash-rich assets. EV battery investments in Michigan and Tennessee are set to lift calcined-kaolin demand regionally. EPA effluent and dust rules add USD 5-10 million capex per mine but create a moat against new entrants.

Europe faces competitiveness challenges as natural-gas costs and carbon prices inflate calcination economics. Sibelco’s 2023 acquisition of Quarzwerke’s kaolin business and waste-heat retrofits illustrate a shift toward scale and energy efficiency. South America’s vast Amazon reserves stay mostly untapped due to stringent permitting, while Middle-East and Africa rely on imports as Saudi Vision 2030 boosts sanitary-ware requirements.

Competitive Landscape

The kaolin market is moderately concentrated; the top five players held about 45-50% combined processed-kaolin capacity in 2025. Imerys refocused on specialty minerals after divesting Performance Minerals Americas, which, combined with Thiele, now trades as KaMin LLC. Sibelco expanded via a 2023 Quarzwerke deal, fortifying its European footprint. 20 Microns, Ashapura, and EICL are scaling in India with backward-integration from tile clients.

Indian tile and Brazilian ceramic manufacturers are enhancing beneficiation capabilities to improve profit margins, while U.S. exporters leverage freight advantages to expand into Mexico and Asia. Specialty applications, such as halloysite from Idaho for separators and pharmaceuticals, and delaminated grades for luxury packaging, highlight the market's focus on niche segments. Technology investments, including waste-heat recovery systems reducing gas consumption by 15-20% and real-time particle-size analytics improving yields by 3-5%, further drive competitiveness. Regulatory compliance with standards like ISO 14001, FDA indirect food contact approvals, and IEC battery standards creates high entry barriers, favoring established players and reinforcing their market positions.

Kaolin Industry Leaders

Imerys

Sibelco

Thiele Kaolin Company

KaMin LLC / CADAM

EICL

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Zeotech secured a five-year agreement valued with a China-based global trading company for the supply of kaolin. The company signed a binding term sheet with Jiangsu Mineral Sources International Trading Co, Limited, one of the largest global traders of kaolin, for the delivery of 950,000 tonnes of direct shipping ore (DSO) kaolin products.

- July 2025: Green 360 Technologies launched a 457-ton bulk calcining process of high-purity kaolin from its Pittong operation in Victoria to produce high-reactivity metakaolin as a substitute for Portland cement. The calcined product, derived from raw ore and reclaimed tailings, was sent for testing by industry and government partners.

Global Kaolin Market Report Scope

Kaolin is a layered silicate mineral commonly known as china clay. It is a soft white clay used to make a wide range of products, including paper, rubber, paint, and many other products. Kaolin is used in coated paper, toothpaste additives, ceramics, food additives, medicine, cosmetics, etc.

The kaolin market is segmented by form, grade, application, and geography. By form, the market is segmented into processed kaolin and crude/unprocessed kaolin. By grade, the market is segmented into hydrous kaolin, calcined kaolin, delaminated kaolin, and other grades. By application, the market is segmented into ceramics, cement, paper, refractories, paints and coatings, plastics, and other applications. The report also covers the market size and forecasts for kaolin in 15 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of volume (Tons).

| Processed Kaolin |

| Crude/Unprocessed Kaolin |

| Hydrous Kaolin |

| Calcined Kaolin |

| Delaminated Kaolin |

| Other Grades |

| Ceramics |

| Cement |

| Paper |

| Refractories |

| Paints and Coatings |

| Plastics |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Processed Kaolin | |

| Crude/Unprocessed Kaolin | ||

| By Grade | Hydrous Kaolin | |

| Calcined Kaolin | ||

| Delaminated Kaolin | ||

| Other Grades | ||

| By Application | Ceramics | |

| Cement | ||

| Paper | ||

| Refractories | ||

| Paints and Coatings | ||

| Plastics | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the kaolin market?

The kaolin market stands at 49.46 million tons in 2026 and is forecast to reach 60.87 million tons by 2031, reflecting a 4.24% CAGR from 2026-2031.

Which region leads demand growth for kaolin?

Asia-Pacific leads, driven by ceramics expansion in China, India, Indonesia, and Vietnam, growing at 4.94% CAGR through 2031.

Why is calcined kaolin gaining traction in batteries?

Calcined grades improve separator thermal stability at lower cost than alumina, and EV gigafactories could need 50,000-80,000 tons annually by 2031.

What is driving investment in beneficiation in India?

A gap between 8.3 million tons of crude output and limited processing capacity pushes tile makers to pay import premiums; new plants aim to close this gap.

Page last updated on: