Morocco ICT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 6.95 Billion |

| Market Size (2026) | USD 7.40 Billion |

| Market Size (2031) | USD 10.08 Billion |

| Growth Rate (2026 - 2031) | 6.37% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Morocco ICT Market Analysis by Mordor Intelligence

The Morocco ICT Market size is projected to expand from USD 6.95 billion in 2025 and USD 7.40 billion in 2026 to USD 10.08 billion by 2031, registering a CAGR of 6.37% between 2026 to 2031.

Morocco’s pivot from foundational infrastructure to value-added digital services is gaining momentum as nationwide 5G, hyperscale cloud, and public-sector digitalization programs converge. The simultaneous commercial 5G launch by the three incumbent operators in November 2025 unlocked ultra-low-latency use cases and encouraged enterprises to move workloads from on-premise environments to the cloud. Government funding under the Morocco Digital 2030 strategy is creating a sizable pipeline of e-government and smart-city projects, while Oracle’s dual cloud regions offer the first local hyperscale landing zone for regulated data. At the same time, high-profile cyber incidents have increased spending on advanced security services, especially among financial institutions and critical infrastructure providers.

Key Report Takeaways

- By product type, IT Services led with 34.60% of Morocco ICT market share in 2025, while IT Security recorded the fastest projected CAGR at 8.13% through 2031.

- By enterprise size, large enterprises accounted for 54.34% of spending in 2025, whereas small and medium enterprises are forecast to expand at a 7.32% CAGR through 2031.

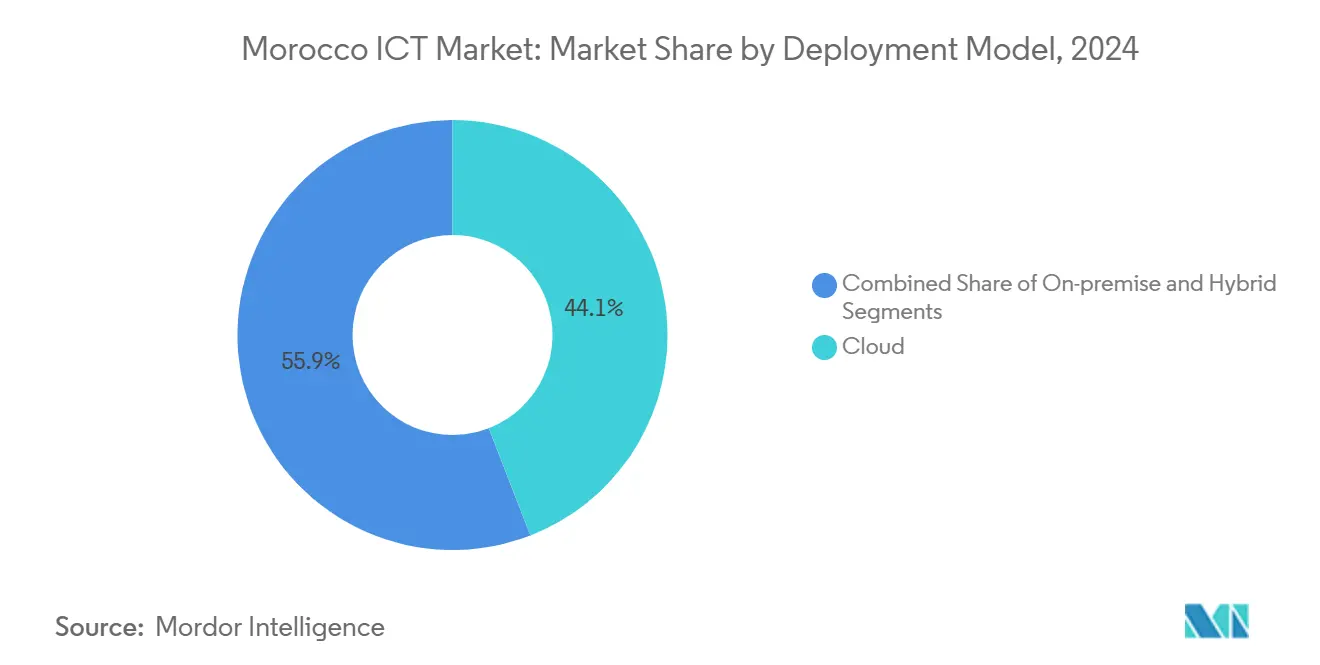

- By deployment model, cloud deployments captured 44.10% of spending in 2025 and are advancing at a 7.90% CAGR between 2026 and 2031.

- By end-user vertical, government and public administration represented 24.60% of demand in 2025, while gaming and esports is projected to grow at 9.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Morocco ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Digital Transformation Across Industries | +1.8% | National, with concentration in Casablanca, Rabat, Tangier, industrial zones | Medium term (2-4 years) |

| Rapid Nationwide 5G Roll-Out | +1.5% | National, targeting 25% coverage by end-2025, 70% by 2030 | Short term (≤ 2 years) |

| Government Programme Morocco Digital 2030 | +1.3% | National, with flagship projects in Rabat-Casablanca corridor | Long term (≥ 4 years) |

| Expansion of E-Commerce and Cash-Lite Payments | +1.0% | National, with higher adoption in urban centers (Casablanca, Marrakech, Rabat) | Medium term (2-4 years) |

| Foreign Hyperscale Data-Centre Investment | +0.7% | Regional, concentrated in Casablanca and Settat cloud regions | Medium term (2-4 years) |

| Rabat-Casablanca Innovation Corridor Growth | +0.5% | Regional, focused on Rabat, Casablanca, and Tangier tech parks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Digital Transformation Across Industries

Automotive, aerospace, and banking organizations have accelerated Industry 4.0 and core-banking upgrades, attracted by export mandates and an accommodative fintech sandbox that approved 12 mobile-money pilots in 2024[1].Source: Renault Group, “Renault Morocco 4.0 Transformation,” renaultgroup.com Renault’s Tangier plant now integrates digital twins and predictive maintenance across 400,000 vehicles per year, while Bank Al-Maghrib’s sandbox has reduced cash transactions to an estimated 65% of retail payments in 2025. Healthcare is catching up as universal coverage creates demand for interoperable clinical systems and spurs new telemedicine rules. The breadth of transformation ensures that IT Services maintain a leading revenue position, yet rising 5G edge deployments are expected to shift some spending toward infrastructure and platform services.

Rapid Nationwide 5G Roll-Out

The July 2025 spectrum auction released 260 MHz of mid-band capacity, enabling all three operators to activate commercial 5G services in November 2025[2]Source: ANRT, “5G Spectrum Auction Results 2025,” anrt.ma. Ericsson’s dual-mode core, supplied to Orange Maroc, supports standalone architecture that lowers latency for industrial IoT at Tanger Med, where automated cranes reduced container dwell time by 18%. Precision-farming pilots in Souss-Massa have cut water use by 22% using sensor-equipped drip irrigation. However, limited fiber in inland regions may delay benefits for rural SMEs, underscoring the need for complementary backhaul investment.

Government Programme Morocco Digital 2030

Backed by USD 1.1 billion, the program targets 240,000 new digital jobs, MAD 100 billion in GDP contribution, and 3,000 startup incubations by 2030. Incentives at Rabat Technopolis include tax holidays and fast-track visas, while a Microsoft-Huawei-Cisco consortium will certify 50,000 cloud and cybersecurity specialists by 2027. Cloud-first procurement rules already guided the tax authority’s migration to Huawei all-flash arrays, trimming return processing time by 40%. Execution risks persist because only 28% of firms maintain a web presence, indicating that supply-side readiness exceeds demand-side maturity.

Expansion of E-Commerce and Cash-Lite Payments

Digital payments hit 97.8 million transactions in the first nine months of 2022, rising 35.3% year-on-year as contactless and QR payments spread to 120,000 merchants[3]Source: Centre Monétique Interbancaire, “Digital Payment Statistics 2022,” cmi.co.ma. E-commerce volumes reached 28.1 million, yet cash-on-delivery still accounts for 48% of orders, revealing lingering trust gaps in escrow mechanisms. Fintech pilots such as Inwi Money and Orange Money now bundle bill payment and micro-insurance, addressing the 8 million unbanked adults identified by the central bank. Growth in gaming and esports further boosts micro-transaction flows, reinforcing demand for secure payment gateways and anti-fraud analytics.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of Skilled ICT Workforce | -1.2% | National, acute in secondary cities and rural provinces | Medium term (2-4 years) |

| High Cyber-Risk and Data-Theft Incidents | -0.9% | National, with higher exposure in BFSI, government, and healthcare sectors | Short term (≤ 2 years) |

| Urban-Rural Digital Divide | -0.6% | Regional, concentrated in the inland and southern provinces | Long term (≥ 4 years) |

| Import-Dependence for ICT Hardware | -0.4% | National, affecting all sectors reliant on servers, networking gear, and semiconductors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Skilled ICT Workforce

Morocco produces 18,000 ICT graduates per year, leaving an annual shortfall of 22,000 specialists needed to reach the 240,000-person target by 2030. Attrition exceeds 25% in Casablanca and Rabat as developers migrate to Gulf economies that offer salary premiums of 40-60%. Vendor-led interventions include Huawei’s plan to train 10,000 students by 2027 and KPMG’s Skills Hub that will add 150 roles by 2029, but these cover less than 5% of projected demand. Unless micro-credential programs scale quickly, talent scarcity could inhibit advanced analytics, AI, and cybersecurity projects.

High Cyber-Risk and Data-Theft Incidents

The April 2025 breach of the National Social Security Fund compromised data for 2 million individuals and 40,000 businesses, prompting a 34% rise in cyber-insurance premiums. Ransomware detections reached 1,076 in 2024, with healthcare and manufacturing victims accounting for 58% of cases. Although Morocco’s 2024 Data Protection Law imposes fines up to MAD 10 million, the data-protection authority has issued only three penalties, signaling weak enforcement. As only 18% of firms hold ISO 27001 certification, the market for managed detection and response services is expected to expand rapidly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Lead, Security Surges

IT Services accounted for 34.60% of the Morocco ICT market size in 2025, reflecting strong demand for consulting, system integration, and managed operations. Enterprises embraced outsourcing to accelerate 5G, IoT, and ERP modernization, while government cloud-first mandates funneled new workloads to service providers. Communication services faced pricing pressure as operators diverted cash to spectrum fees, causing blended ARPU to fall 4% year-on-year. IT Infrastructure growth remained muted because many enterprises deferred capex in favor of cloud subscriptions.

IT Security is expanding at 8.13% CAGR, the fastest among product types, buoyed by regulatory audits and high-profile breaches. The Morocco ICT market benefits as enterprises pivot from basic perimeter tools to advanced endpoint detection and zero-trust architectures, often delivered as managed services. Vendors have localized Arabic natural-language processing models in Oracle’s Casablanca region, reducing chatbot latency by 73%, which lifts demand for AI-enabled customer support solutions. Hardware suppliers still rely on imports, exposing customers to currency volatility and supply-chain shocks, but they retain a foothold in specialized edge and data-center deployments.

By End-User Enterprise Size: Large Firms Dominate, SMEs Accelerate

Large enterprises captured 54.34% of Morocco ICT market share in 2025 thanks to multi-year modernization projects at ministries, utilities, and multinationals. These organizations run complex hybrid architectures that rely on premium support and advanced security, locking in high-value contracts for global integrators.

SMEs are projected to grow at 7.32% CAGR as the Forsa program, the Retail Tech Builder, and fintech pilots lower adoption barriers. Cloud subscription models allow smaller firms to circumvent upfront hardware costs, but only 40% have migrated workloads, primarily because talent shortages and breach fears deter full digitization. Expanding managed-service bundles tailored for micro-enterprises could unlock latent demand and strengthen the Morocco ICT industry ecosystem.

By Deployment Model: Cloud Leads and Accelerates

Cloud deployments held 44.10% of spending in 2025 and are forecast to rise at 7.90% CAGR through 2031, outperforming on-premise and hybrid alternatives. Oracle’s USD 140 million dual-region investment satisfies data-residency rules and introduces more than 50 services, including Autonomous Database and Kubernetes Engine, that underpin modern application stacks.

Hybrid models appeal to banks and ministries that need local processing for sensitive workloads but also require continental disaster-recovery sites. On-premise estates persist in oil and gas and discrete manufacturing, where isolation remains a key ransomware mitigation. Multi-cloud optionality could boost migration velocity, so market observers await potential region announcements from AWS, Microsoft Azure, and Google Cloud.

By End-User Industry Vertical: Government Anchors, Gaming Sprints

Government and public administration represented 24.60% of the Morocco ICT market size in 2025, fueled by cloud-first directives, smart-city deployments, and large-scale digital-identity platforms. Defense and tax agencies are also piloting AI-assisted analytics, reinforcing sustained budget allocation.

Gaming and esports is the fastest growing vertical at 9.10% CAGR. The MAD 500 million Cité du Gaming complex, opening in 2026, will host regional tournaments, incubate studios, and connect Morocco’s 2.5 million gamers to global platforms. Complementary fintech solutions are driving micro-transaction revenue, revealing cross-sell opportunities for payment processors and security vendors.

Geography Analysis

The Rabat-Casablanca corridor accounts for 68% of ICT spending, anchored by Casablanca Smart City and Tangier Tech City projects that bundle IoT traffic management, e-waste monitoring, and green data centers. Strong fiber penetration at 54% supports rapid 5G backhaul and positions the corridor as the preferred location for hyperscale and edge facilities.

Regions outside the corridor average 12% fiber availability, constraining SME cloud adoption in agricultural and mining hubs that generate 28% of national GDP. Projects such as the Noor Ouarzazate renewable-powered data center aim to create distributed compute resources and narrow the latency gap for rural users.

Southern provinces see growing demand for satellite connectivity in logistics and energy exploration. National coverage obligations tied to the 5G licenses should raise 5G population reach from 25% in 2025 to 70% by 2030, gradually balancing urban-rural service quality.

Competitive Landscape

Morocco’s telecom triopoly, Maroc Telecom, Orange Maroc, and Inwi, shares the mobile market almost evenly, yet their MAD 4.4 billion fiber and tower joint venture shifts emphasis from customer acquisition to infrastructure monetization. This collaboration could stabilize margins while raising wholesale revenues.

Global vendors are expanding local footprints: IBM partnered with Atlas Cloud Services to deploy watsonx AI, targeting 30% of ACS revenue from AI within two years. Oracle, Huawei, and Nokia each signed capacity-building or R&D agreements that tie technology investment to workforce development commitments.

Local specialists such as HPS and OnnVision seize white-space in payments processing and managed security. ISO 27001 compliance and data-protection certification remain differentiators, although only 18% of firms hold the credential, suggesting room for new entrants offering turnkey governance and risk solutions.

Morocco ICT Industry Leaders

IBM Corporation

Microsoft Corporation

Oracle Corporation

Salesforce, Inc.

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ericsson completed the first phase of Orange Maroc’s standalone 5G core upgrade ahead of schedule, enabling network slicing for enterprise clients.

- November 2025: Maroc Telecom, Orange Maroc, and Inwi jointly launched commercial 5G services, targeting 25% population coverage by year-end and 70% by 2030.

- July 2025: ANRT concluded its 5G spectrum auction, collecting MAD 2.1 billion in license fees.

- April 2025: IBM and Atlas Cloud Services unveiled a partnership to deploy watsonx AI in Morocco.

Morocco ICT Market Report Scope

The Moroccan ICT market encompasses the integration and uptake of various information and communications technologies (ICT) in the country. These technologies include big data, mobility, storage, outsourcing, and cloud computing. The primary goal is to drive digitization and digital transformation. The market's focus is on tracking the revenue generated from the sale of these technology solutions.

The Morocco ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security, and Communication Services), End-User Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Deployment Model (On-premise, Cloud, and Hybrid), and End-User Industry Vertical (Government and Public Administration, BFSI, Energy and Utilities, Retail E-commerce and Logistics, Manufacturing and Industry 4.0, Healthcare and Life Sciences, Oil and Gas, and Gaming and Esports). Market Forecasts are Provided in Terms of Value (USD).

| IT Hardware |

| IT Software |

| IT Services |

| IT Infrastructure |

| IT Security |

| Communication Services |

| Small and Medium Enterprises |

| Large Enterprises |

| On-premise |

| Cloud |

| Hybrid |

| Government and Public Administration |

| BFSI |

| Energy and Utilities |

| Retail, E-commerce and Logistics |

| Manufacturing and Industry 4.0 |

| Healthcare and Life Sciences |

| Oil and Gas (Up-, Mid-, Down-stream) |

| Gaming and Esports |

| Other Verticals |

| By Products Type | IT Hardware |

| IT Software | |

| IT Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services | |

| By End-User Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Deployment Model | On-premise |

| Cloud | |

| Hybrid | |

| By End-User Industry Vertical | Government and Public Administration |

| BFSI | |

| Energy and Utilities | |

| Retail, E-commerce and Logistics | |

| Manufacturing and Industry 4.0 | |

| Healthcare and Life Sciences | |

| Oil and Gas (Up-, Mid-, Down-stream) | |

| Gaming and Esports | |

| Other Verticals |

Key Questions Answered in the Report

How large will Morocco’s ICT spending be by 2031?

The Morocco ICT market is forecast to reach USD 10.08 billion by 2031, expanding at a 6.37% CAGR.

Which product category is growing the fastest?

IT Security is the fastest-growing category, advancing at 8.13% CAGR through 2031 as organizations enhance defenses after recent cyber incidents.

What role does 5G play in enterprise adoption?

The synchronized nationwide 5G launch in 2025 is enabling low-latency use cases such as port automation and precision agriculture, accelerating cloud and IoT uptake.

Why is cloud deployment outpacing on-premise models?

Oracle’s dual cloud regions satisfy data-residency rules and introduce over 50 services, prompting many organizations to shift workloads to subscription models with lower upfront costs.

Page last updated on: