Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

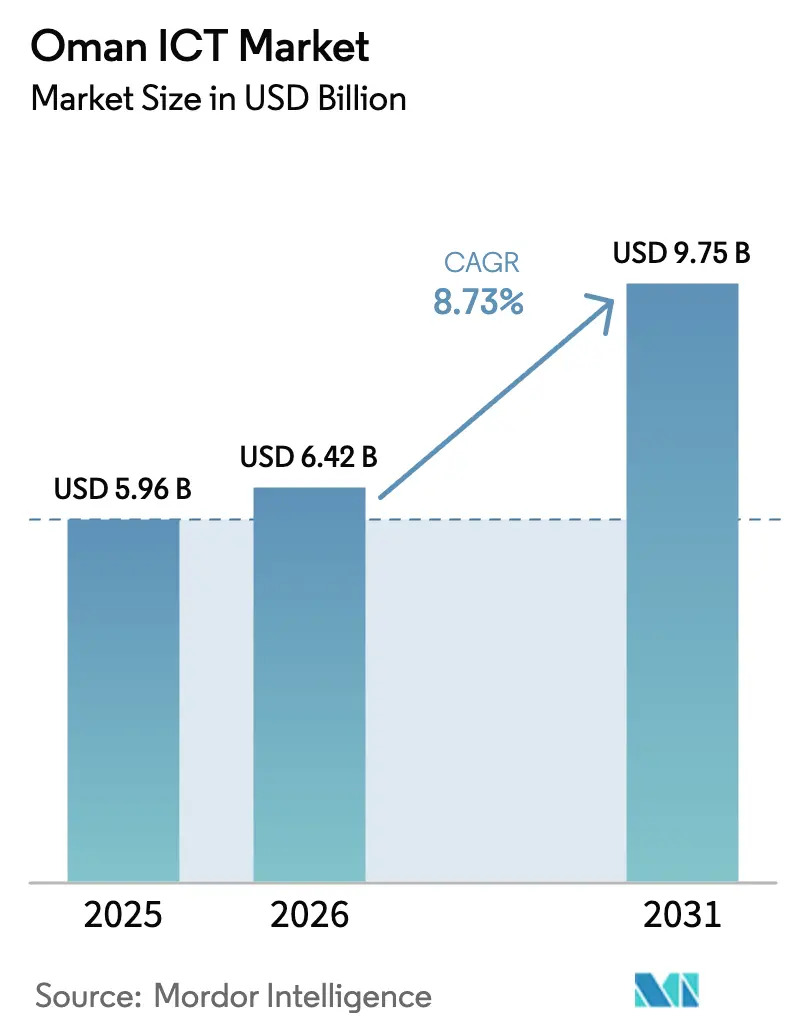

| Base Year Market Size (2025) | USD 5.96 Billion |

| Market Size (2026) | USD 6.42 Billion |

| Market Size (2031) | USD 9.75 Billion |

| Growth Rate (2026 - 2031) | 8.73% CAGR |

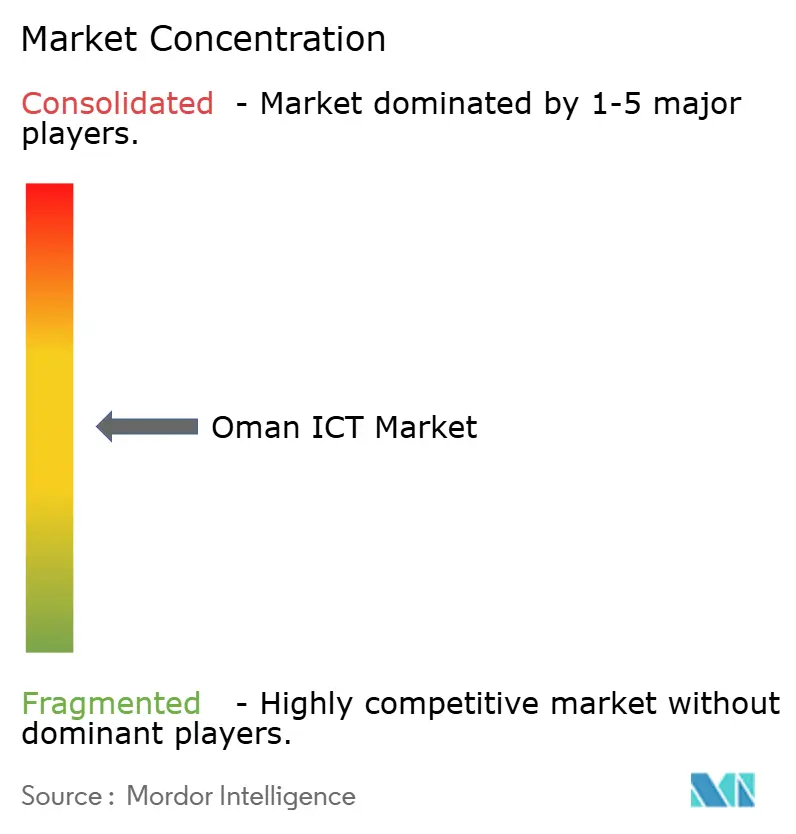

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman ICT Market Analysis by Mordor Intelligence

The Oman ICT market size is expected to increase from USD 5.96 billion in 2025 to USD 6.42 billion in 2026 and reach USD 9.75 billion by 2031, growing at a CAGR of 8.73% over 2026-2031. Robust public-sector digitization programs, sovereign-cloud mandates, and the emergence of a domestic semiconductor cluster are widening demand beyond legacy connectivity and driving premium spending on cloud, cybersecurity, and artificial intelligence. Momentum is strongest in segments that lower operating costs for ministries, shorten time-to-market for banks and retailers, and improve data-sovereignty compliance for multinational firms. Vendors that bundle professional services with cloud, analytics, and edge solutions are winning larger deals because enterprises are grappling with complex hybrid architectures. Competition is healthy but not fragmented; three mobile operators dominate access networks while a handful of sovereign-cloud providers control hyperscale computing capacity.

Key Report Takeaways

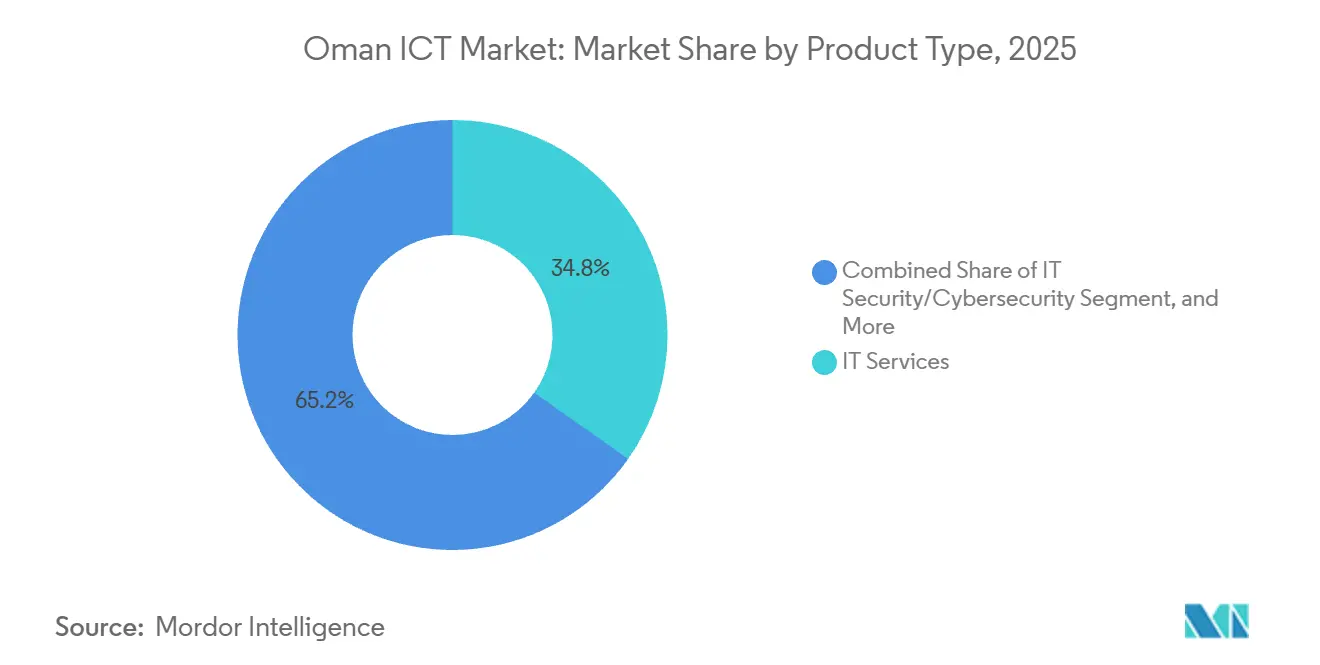

- By product type, IT services led with 34.78% revenue share in 2025, while IT security and cybersecurity is projected to record a 9.12% CAGR through 2031.

- By enterprise size, large enterprises contributed 54.21% of market share in 2025, whereas small and medium-sized enterprises are set to post a 9.42% CAGR over the same horizon.

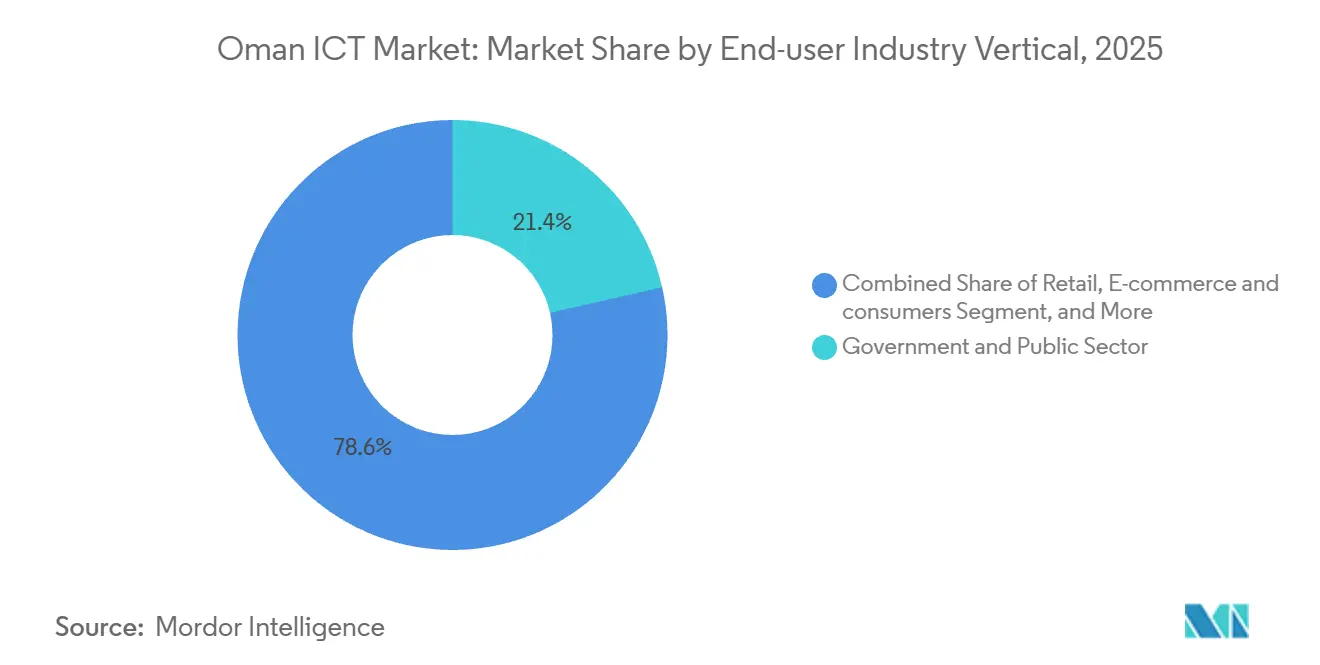

- By end-user industry, the government and public sector accounted for 21.44% of market share in 2025 expenditure, but retail, e-commerce, and consumers are forecast to expand at a 9.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Oman ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Digital Transformation Program and Vision 2040 | +2.1% | National, early gains in Muscat and Dhofar governorates | Medium term (2-4 years) |

| Nationwide 5G and Fiber Broadband Expansion | +1.8% | National, prioritizing urban centers and industrial zones | Short term (≤ 2 years) |

| Growing Cloud Adoption and Data Center Investments | +1.5% | National, concentrated in Muscat, Ibri, Salalah, Duqm | Medium term (2-4 years) |

| Rising Internet Penetration and Smartphone Usage | +1.2% | National | Short term (≤ 2 years) |

| Green AI Data Centers and Oman Digital Triangle Initiative | +1.0% | Barka, Duqm, Sur | Long term (≥ 4 years) |

| National Semiconductor Program Spurring Local Tech Manufacturing | +0.9% | Salalah and Muscat | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Digital Transformation Program and Vision 2040

Oman’s Vision 2040 and the Tahawul transformation roadmap have shifted public procurement toward shared digital platforms, reducing duplication and favoring vendors that can deliver end-to-end suites. Twenty-five of 36 Tahawul projects were delivered by November 2024, and 74% of priority public services moved online, signaling a decisive break from siloed IT systems.[1]Oman.om, “Tahawul Project Status Update,” oman.om The Oman Business Platform processed 2.8 million transactions by September 2025, which validates citizens' appetite for frictionless e-services and lifts demand for workflow automation tools. Digital Transformation Management Company, an ITHCA subsidiary, leveraged this shift by winning 12 government contracts in 2024, underscoring that scale advantages accrue to firms that master public-sector processes. The National Open Data Portal launched in September 2025 with more than 350 datasets, opening a pipeline for analytics and AI workloads hosted on sovereign clouds. Oman’s UN E-Government Development Index improved to 0.8576 in 2024, confirming infrastructure readiness and lowering deployment risk for systems integrators.

Nationwide 5G and Fiber Broadband Expansion

Vodafone Oman completed over 2,572 5G sites by February 2025 and exceeded 98% population coverage, demonstrating that accelerated roll-outs can reset competitive baselines and push enterprises toward low-latency IoT applications.[2]Vodafone Oman, “Network Achievements 2025,” vodafone.om Omantel’s January 2026 upgrade to 5G Standalone introduced network slicing and Voice-over-5G, enabling differentiated enterprise SLAs for autonomous port logistics and public-safety analytics. Oman Broadband Company achieved 93.4% fiber coverage in Muscat by 2024, but only 45.2% in other urban areas, highlighting regional gaps that open opportunities for wholesale access platforms. The open-access model eases capital outlay for smaller service providers and accelerates multi-tenancy adoption. Ooredoo’s 2Africa subsea cable landing connects Oman to a 45,000-km global network, lowering bandwidth costs and supporting hybrid-cloud strategies for multinationals.

Growing Cloud Adoption and Data Center Investments

Mandatory data-residency rules are fragmenting the hyperscaler field and rewarding providers that localize capacity. Oman Data Park launched Oracle Cloud Infrastructure’s secondary dedicated region in Ibri in October 2025, providing automatic failover over 10 Gbps links to Muscat and guaranteeing compliance for regulated workloads. Omantel’s agreement with AWS in March 2024 created a Cloud Center of Excellence that trains local architects to align global platforms with national rules. OQ partnered with SAP in May 2025 to run S/4HANA in a local private cloud, illustrating how industrial firms are re-platforming ERP stacks inside sovereign facilities. Power remains a gating factor; Oman Data Park’s capacity will double to 20 MW by 2030, and its joint project with Solar Wadi adds 1.4 MW of solar generation to offset the 10-fold power draw of AI racks. The Oman Digital Triangle agreement with the International Data Center Authority in September 2025 targets gigawatt-scale green centers in Barka, Duqm, and Sur, signaling that renewable energy and coastal access will define the next wave of capacity.

Green AI Data Centers and Oman Digital Triangle Initiative

Oman is channeling large-scale AI compute into purpose-built, green facilities that integrate solar, wind, and seawater cooling. The Digital Triangle’s three planned data centers will aggregate up to one gigawatt of capacity, dwarfing the country’s existing 40 MW footprint and positioning Oman as an alternative landing point for African and South Asian workloads. Early designs specify PUE targets below 1.3 and direct-subsea fiber links, enabling hyperscalers to meet both carbon and latency mandates. Local municipalities in Barka, Duqm, and Sur have earmarked land adjacent to renewable-energy farms, lowering power transmission losses and accelerating permitting cycles. Domestic equipment suppliers expect a pull-through effect on battery storage, modular hydrogen fuel cells, and high-density cooling rigs. Investors view the project as a hedge against power-price shocks that threaten inland data centers in neighboring Gulf economies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute Shortage of Advanced ICT Skills | -1.3% | National, most acute in AI, cybersecurity and data science | Medium term (2-4 years) |

| Heightened Cybersecurity and Data Privacy Concerns | -0.9% | National, spillover to cross-border data flows | Short term (≤ 2 years) |

| Regulatory Uncertainty on Data Localization and Telecom Law Revisions | -0.6% | National, affecting multinational enterprises | Medium term (2-4 years) |

| Funding Gap for Growth-Stage Tech Startups | -0.5% | National, Muscat startup ecosystem | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Advanced ICT Skills

Omanisation in the ICT sector climbed to 62.02% in 2024, yet enterprises still depend heavily on expatriate specialists for AI, cybersecurity, and data engineering projects. The Makeen program aims to upskill 10,000 Omanis by the end of 2025, but focuses on entry-level literacy rather than advanced model fine-tuning or zero-trust design. Omantel Academy, launched in January 2026, plans to create 1,200 training slots and 500 new jobs over four years, but this figure pales in comparison to the 1,728 ICT positions created in Q3 2024 alone, suggesting a supply deficit more than threefold. The Irtiqa leadership scheme focuses on mid-career officials at 57 ministries, leaving junior engineering roles unfilled and forcing systems integrators to import talent. An IMF assessment in April 2025 concluded that Oman must invest more to match Gulf peers on digital skills, confirming that labor scarcity remains a binding constraint.[3]IMF, “Oman Economic Assessment 2025,” imf.org

Heightened Cybersecurity and Data Privacy Concerns

Cyber-fraud incidents jumped 50% in H1 2025, and Royal Oman Police data showed a 35% quarter-on-quarter rise in fraud cases driven by deepfakes and spoofed e-commerce sites. The Oman Computer Emergency Response Team handled 136 events in the first nine months of 2024, but private-sector disclosure is voluntary, creating an information gap that hampers risk underwriting. The Telecommunications Regulatory Authority mandated 72-hour breach notifications in September 2024, yet penalty schedules are still pending, leaving compliance budgets uncertain. Healthcare networks are vulnerable; over 50% of facilities lack picture-archiving systems, and 60% operate on sub-500 Mbps links, exposing patient data to ransomware. Although Oman achieved Tier-1 status on the ITU Global Cybersecurity Index, small and medium enterprises without 24/7 SOC coverage remain easy targets, hindering digital service adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cybersecurity Outpaces Legacy IT Services

IT services generated 34.78% of 2025 Oman ICT revenue, anchored by enterprise resource planning rollouts, multicloud migration consulting and managed networks. The Oman ICT market size attribution emphasizes how change-management projects and application modernization remain profit pools. Managed security and cloud-platform support drive sticky recurring fees that differentiate integrators from hardware resellers.

The IT security segment is forecast to deliver a 9.12% CAGR, expanding its Oman ICT market share as data-localization mandates and ransomware events fuel zero-trust spending. Hardware margins narrow because buyers shift to operating-expense cloud capacity, while software-as-a-service for customer relationship management and supply-chain analytics gains traction. Communication services face price compression but offset this through wholesale capacity tied to new submarine cables.

By Enterprise Size: SME Digitalization Accelerates

Large enterprises captured 54.21% of spending in 2025 as state energy, banking and telecom entities launched multi-year cloud, Internet of Things and AI programs. These flagship projects bundle infrastructure, applications and managed services in five-year contracts, reinforcing vendor lock-in but ensuring steady cash flows.

Small and medium-sized enterprises are projected to grow at a 9.42% CAGR, lifting their Oman ICT market share by 2031. Future Fund Oman’s USD 364 million allocation subsidizes cloud subscriptions and e-commerce platforms. Visa research showed 65% of digital-payment retailers saw higher revenue, proving that point-of-sale digitalization translates into turnover gains. SMEs gravitate toward subscription bundles that package inventory, payments and analytics, reducing integration burden.

By End-User Industry Vertical: Retail And E-Commerce Surge

Government and public sector delivered 21.44% of expenditure in 2025 after automating 267 services and centralizing tenders online. These projects underpin the Oman ICT market through guaranteed multi-year maintenance budgets and steady refresh cycles.

Retail, e-commerce and consumers are forecast to register a 9.65% CAGR through 2031, driven by smartphone ubiquity, a national payment gateway and supportive e-commerce legislation. Oil and gas entities such as Petroleum Development Oman invested over USD 1 billion in predictive analytics, Internet of Things sensors and private 5G networks. Banking adopts cloud-native cores to launch mobile products and comply with anti-money-laundering rules, while manufacturing and utilities rely on IoT telemetry for process optimization.

Geography Analysis

Muscat continues to host most fiber routes, data center racks, and enterprise headquarters, making it the anchor of the Oman ICT market. Oman Broadband passed 427,904 homes in the capital by 2024 versus 464,431 elsewhere, indicating an infrastructure gap that second-tier cities are racing to close. The Digital Triangle pact of September 2025 will plant green, gigawatt-scale data centers in Barka, Duqm, and Sur, shifting capacity toward coastal hubs with easy access to subsea cables.

Salalah is morphing into a compute hub after Ooredoo’s 2Africa cable landing in 2024, which trims latency to East Africa and South Asia and invites CDN and cloud-interconnect providers. Duqm’s special economic zone pairs industrial IoT pilots with edge nodes, creating field labs for logistics, petrochemicals, and metals. The government’s open-access fiber regulation reduces capex for new entrants, which should lift coverage outside Muscat to near parity over the forecast period.

Within the Gulf Cooperation Council, Oman positions itself as a neutral, sovereign cloud corridor. Its ITU Tier-1 cybersecurity status and growing hyperscale footprint attract enterprises wary of data concentration in the UAE and Saudi Arabia. Cross-border ventures such as the SONIC corridor with STC and bilateral agreements with Meeza, Salam, and BNet further embed Oman in regional data routes. As these links deepen, the Oman ICT market will benefit from transit fees, interconnect traffic, and managed services export opportunities.

Competitive Landscape

Competition is healthy but not fragmented. Three licensed mobile players split access revenues, yet differentiation is rising. Vodafone Oman seized roughly 10% of the market share within two years and won 11 of 14 Opensignal quality awards in January 2025, proving that aggressive capex and local financing can disrupt incumbent duopolies. Omantel’s 5G Standalone launch in January 2026 delivers voice over 5G and sub-10 ms slices, enabling premium SLAs for autonomous vehicles and telehealth. Ooredoo Oman leads on network availability at 97.6% and leverages the 2Africa cable for wholesale bandwidth.

In sovereign cloud, Oman Data Park controls more than 70% of public-sector workloads and partners with Oracle for a dual-region footprint, creating high switching costs for ministries. AWS, Microsoft, and Huawei must pursue joint ventures or dedicated regions to penetrate regulated verticals, as seen in the Omantel-AWS Cloud Center of Excellence. Niche disruptors include ITHCA portfolio firms such as Onsor Technologies, which delivered 600 IoT charging carts to schools, and Space Communication Technologies, which reached break-even in 2024 with satellite broadband subscribers.

Cybersecurity demand is concentrating with providers that run domestic SOCs. Incumbents bundle 24/7 monitoring with cloud hosting and fiber links, crowding out pure-play resellers. Barriers to entry climbed after TRA required operator permits and local data residency for Levels 3-4 data, effectively shielding domestic data centers from offshore rivals but also raising compliance stakes for hyperscalers.

Oman ICT Industry Leaders

IBM Corporation

Microsoft Corporation

Huawei Investment & Holding Co., Ltd.

Oracle Corporation

Wipro Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Omantel completed a nationwide 5G Standalone upgrade that enables voice over 5G, reduced-capability IoT devices, and low-latency network slicing for autonomous port operations and public-safety analytics.

- January 2026: Omantel launched Omantel Academy, pledging 1,200 advanced ICT training slots and 500 jobs over four years to mitigate talent shortages.

- October 2025: Oman Data Park opened Oracle Cloud Infrastructure’s secondary dedicated region in Ibri, linked to Muscat with redundant 10 Gbps circuits for real-time failover.

- September 2025: The government inked a pact with the International Data Center Authority to develop the Oman Digital Triangle, three interconnected green data centers in Barka, Duqm, and Sur.

Oman ICT Market Report Scope

The study tracks key market parameters, underlying growth drivers, and major vendors operating in the industry, which supports market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from various types, such as hardware, software, IT services, and telecom services, used in various end-user industries across Oman. In addition, the study provides an overview of the Oman ICT market and key vendor profiles.

The Oman ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security/Cybersecurity, and Communication Services), Enterprise Size (Small and Medium-sized Enterprises, and Large Enterprises), End-user Industry Vertical (BFSI, Government and Public Sector, Oil and Gas, IT and Telecom, Retail E-commerce and Consumers, Manufacturing and Industrial, Energy and Utilities, Healthcare, Other End-user Industry Verticals). The Market Forecasts are Provided in Terms of Value USD.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | Application Security |

| Cloud Security | |

| Data Security | |

| Network Security | |

| Endpoint Security | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Identity and Access Management (IAM) | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| BFSI |

| Government and Public Sector |

| Oil and Gas |

| IT and Telecom |

| Retail, E-commerce and consumers |

| Manufacturing and Industrial |

| Energy and Utilities |

| Healthcare |

| Other End-user Industry Verticals (Includes Transportation, Logistics, Education, Hospitality etc.) |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | Application Security | |

| Cloud Security | ||

| Data Security | ||

| Network Security | ||

| Endpoint Security | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Identity and Access Management (IAM) | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | BFSI | |

| Government and Public Sector | ||

| Oil and Gas | ||

| IT and Telecom | ||

| Retail, E-commerce and consumers | ||

| Manufacturing and Industrial | ||

| Energy and Utilities | ||

| Healthcare | ||

| Other End-user Industry Verticals (Includes Transportation, Logistics, Education, Hospitality etc.) | ||

Key Questions Answered in the Report

How large is the Oman ICT market in 2026 and what is the growth outlook to 2031?

The Oman ICT market size reached USD 6.42 billion in 2026 and is projected to hit USD 9.75 billion by 2031, registering an 8.73% CAGR.

Which product category is expanding fastest?

IT security and cybersecurity is expected to grow at a 9.12% CAGR driven by data-localization mandates and escalating ransomware risks.

What fuels SME technology spending in Oman?

Future Fund Oman subsidies, a national payment gateway and affordable SaaS bundles are propelling SME ICT outlays at a 9.42% CAGR.

How will number portability affect telecom competition?

Full rollout in 2026 will lower switching costs and push carriers to differentiate with bundled 5G, cloud storage and cybersecurity services.

Why are data-center operators investing in solar power?

Renewable cooling cuts operating expenses 10-15% and aligns with environmental, social and governance mandates for carbon-neutral hosting.

What talent gap threatens ICT project timelines?

Only 8% of the workforce possesses advanced ICT skills, creating project delays and higher costs for AI, blockchain and analytics deployments.

Page last updated on: