Jojoba Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

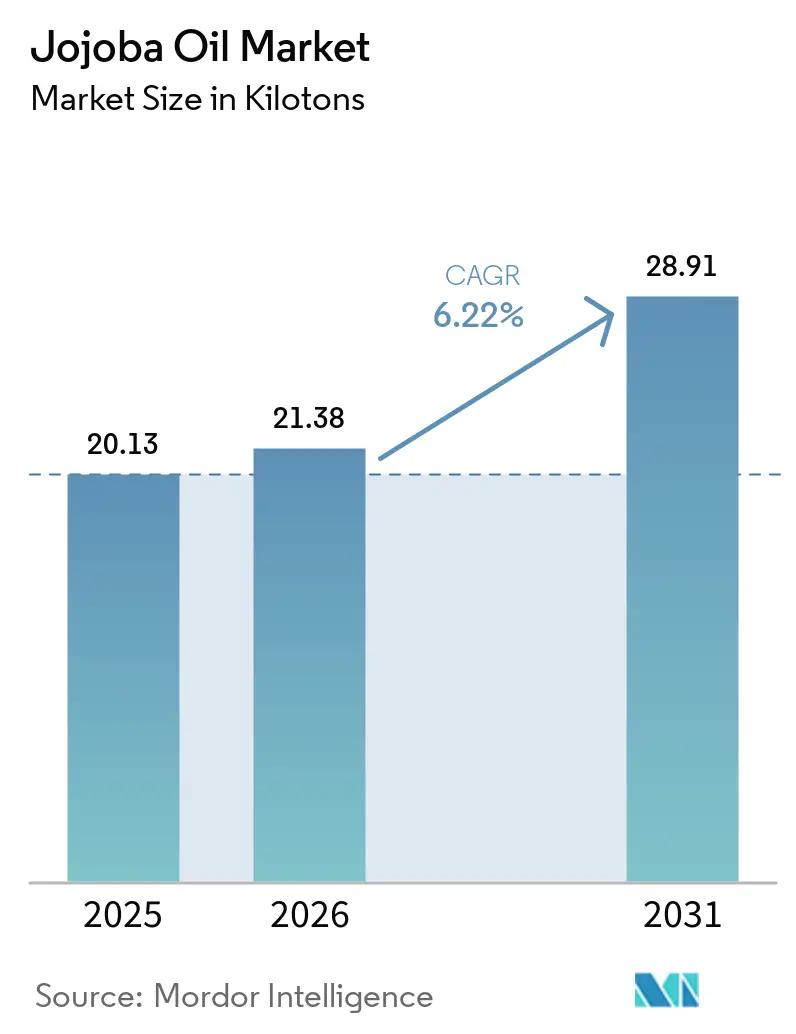

| Market Volume (2026) | 21.38 kilotons |

| Market Volume (2031) | 28.91 kilotons |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

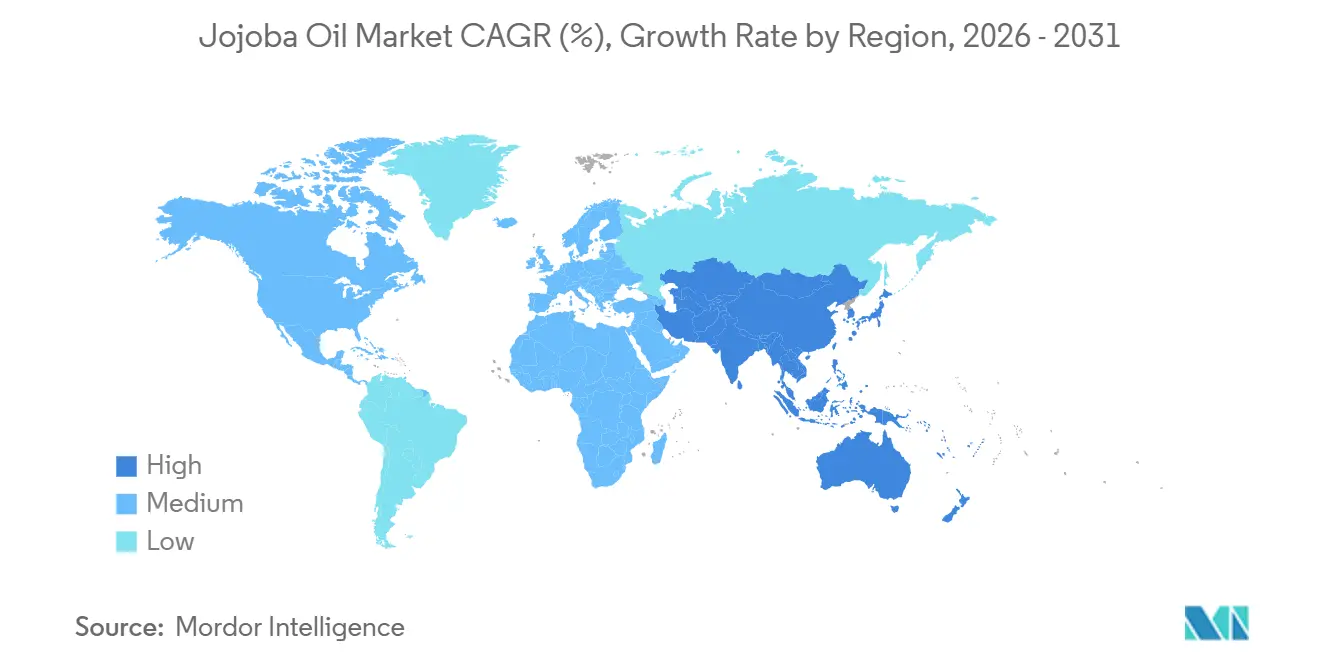

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jojoba Oil Market Analysis by Mordor Intelligence

The Jojoba Oil Market size was 20.13 kilotons in 2025 and is estimated to grow from 21.38 kilotons in 2026 to reach 28.91 kilotons by 2031, at a CAGR of 6.22% during the forecast period (2026-2031). Consumer-facing brands are revising clean-label charters, and jojoba’s wax-ester chemistry delivers the oxidative stability and sebum-mimetic glide those charters demand. Cold-pressed grades dominate because they preserve tocopherols that resonate with COSMOS and Ecocert audits, while hydrogenated offshoots are finding a foothold as plastic-bead replacements. On the industrial side, aerospace and minimum quantity lubrication (MQL) machining facilities are shifting toward bio-lubricants that can tolerate 300°C sump temperatures without polymerizing. Vertically integrated growers are lowering logistics risk for North American formulators by pairing Arizona acreage with blockchain tools that confirm Fair for Life custody in real-time.

Key Report Takeaways

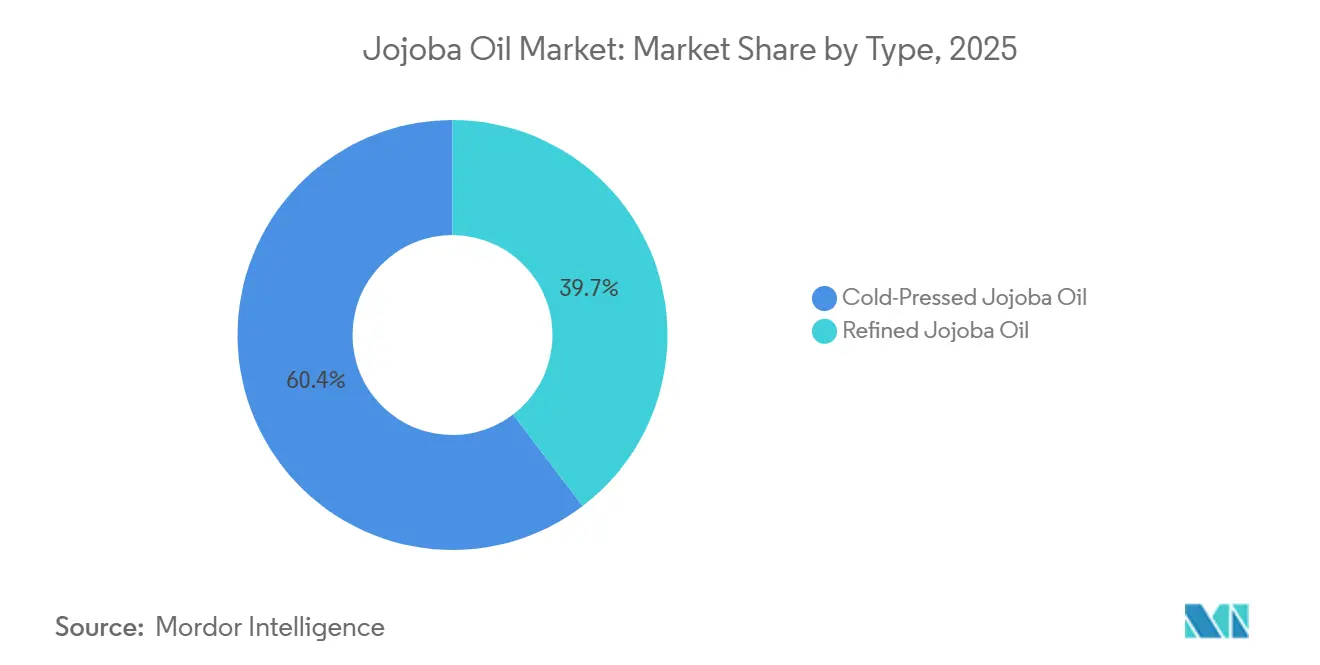

- By type, cold-pressed jojoba oil led with 60.35% volume share in 2025, and the same segment is projected to advance at a 6.48% CAGR through 2031.

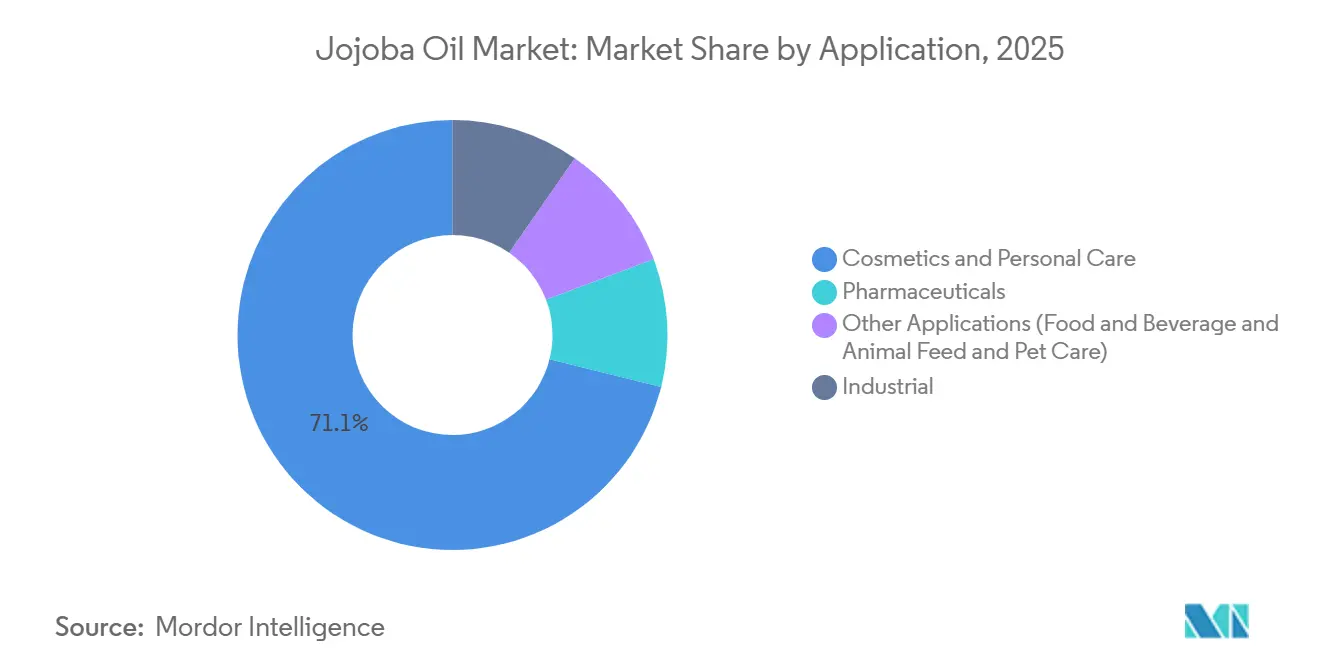

- By application, cosmetics and personal care accounted for 71.12% of the Jojoba Oil market size in 2025, while pharmaceuticals are expected to be the fastest-growing channel at 6.78% CAGR to 2031.

- By geography, Asia-Pacific commanded 46.68% of the Jojoba Oil market share in 2025 and is on track to expand at a 6.82% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Jojoba Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clean-beauty and organic personal-care boom | +2.1% | Global, strongest in North America and EU | Medium term (2-4 years) |

| Cross-industry demand for high-temperature bio-lubricants | +1.3% | North America, Europe, APAC industrial hubs | Long term (≥ 4 years) |

| Premiumization in men’s grooming and scalp-care niches | +1.0% | North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| Blockchain-enabled farm-to-flask traceability premiums | +0.7% | EU, North America specialty channels | Medium term (2-4 years) |

| Policy-led agri-investments in arid-land cash crops | +0.9% | Middle East, South America (Argentina), Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clean-Beauty and Organic Personal-Care Boom

Formulators are displacing silicones with jojoba because the oil’s wax-ester backbone mirrors human sebum, offering occlusion without pore blockage. Fair for Life certification, renewed by Jojoba Desert in 2026, allows retailers such as Whole Foods to attach 15%-25% shelf premiums[1]Personal Care Magazine Staff, “Sustainable Emollients Gain Shelf Premiums,” personalcaremagazine.com. EcoVadis Platinum status, secured in September 2025, amplifies acceptance among procurement teams at L’Oréal that are under Scope 3 scrutiny. Cold-pressed organic grades already hold 60.35% of the jojoba oil market, and EU Cosmetics Regulation EC 1223/2009 further narrows the field for synthetic emollients.

Cross-Industry Demand for High-Temperature Bio-Lubricants

Thermal stability above 300°C makes jojoba a drop-in fluid for aerospace actuators and MQL machining rigs that must meet EPA (Environmental Protection Agency) Vessel General Permit limits on petroleum discharge. Tribological studies report friction coefficients as low as 0.08, besting synthetic esters in boundary regimes. North American OEMs (original equipment manufacturers) accept the 2x cost premium because longer drain intervals reduce disposal fees that OSHA (Occupational Safety and Health Administration) categorizes as hazardous.

Premiumization in Men’s Grooming and Scalp-Care Niches

Beard oils priced between USD 14 and USD 46 per ounce rely on jojoba for fast absorption, a low comedogenic index of 2, and oxidative stability that allows aluminum-free stick formats to survive gym lockers. Direct-to-consumer subscriptions anchor volume predictability, while influencer videos drive repeat purchase among 25- to 40-year-old urban consumers.

Blockchain-Enabled Farm-to-Flask Traceability Premiums

QR codes on lotion bottles now lead to ledgers that show seed origin, cold-press timestamps, and Fair Trade audits, enabling 10%-20% price lifts in EU specialty aisles. Jojoba Desert’s January 2025 rollout of predictive analytics shortens lead times and produces audit trails that satisfy COSMOS traceability rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost and limited cultivation zones | -1.4% | Global, acute where arid zones are absent | Long term (≥ 4 years) |

| Price volatility from fragmented spot trading | -0.8% | Global, spillover to Argentina and Peru | Short term (≤ 2 years) |

| Emerging synthetic biotech wax-ester substitutes | -0.6% | North America and EU research clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Production Cost and Limited Cultivation Zones

Jojoba only thrives where annual rainfall sits below 400 mm, so growers wait 5 years for payback, a lag that keeps supply tight and capital shy[2]Home & Personal Care Middle East & Africa, “Biotech Wax Esters Enter Pilot Scale,” hpcimea.com. Production outlays run 3x higher than soybeans, and water scarcity in Arizona and La Rioja raises yield risk each season. Expansion into new geographies is hindered by the need for varietal trials, soil amendments, and pollinator management, delaying supply responses by half a decade or more.

Price Volatility from Fragmented Spot Trading

Absence of a liquid futures contract leaves buyers exposed to 20%-30% quarterly swings. January 2025 saw Jojoba Desert urge clients toward bulk container orders to cut packaging and stabilize shipment cycles. Fragmentation also impedes quality standardization; cold-pressed, refined, bleached, and hydrogenated grades trade at different premiums, yet the absence of universally accepted specifications allows adulteration and grade misrepresentation, eroding buyer confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cold-Pressed Dominance Reflects Clean-Label Imperatives

Cold-pressed variants commanded 60.35% of the Jojoba Oil market size in 2025 and are pacing a 6.48% CAGR to 2031 as brands align with COSMOS (Cosmetic Organic and Natural Standard) and USDA (United States Department of Agriculture) Organic seals. The segment’s volume leadership springs from vitamin E retention and the golden hue that consumers equate with minimal processing. Hydrogenated offshoots, produced from cold-pressed feedstock, are absorbing demand for plastic-free exfoliants.

Refined grades fill cost-sensitive SKUs in mass-market lotions and hydraulic fluids, yet trail with a growth clip. Solar-powered presses adopted by La Rioja cooperatives are closing cost gaps and reinforcing cold-pressed traction, underlining why the jojoba oil market continues to split between premium organic and functional industrial demand.

By Application: Pharmaceutical Velocity Outpaces Cosmetic Volume

Cosmetics held 71.12% share of the Jojoba Oil market size in 2025, driven by moisturizers and conditioners that leverage sebum mimicry for barrier repair. Pharmaceuticals, however, are forecast for the fastest 6.78% CAGR during the forecast period (2026-2031) as micro-emulsion vehicles enhance dermal drug delivery by up to 60%.

Industrial niches, MQL machining, and EV drivetrains are small but rising because OEMs need bio-fluids that remain shear-stable at 10,000 rpm. Food-grade and pet-care remain ancillary yet benefit from jojoba’s GRAS (Generally Recognized As Safe) status and hypoallergenic reputation, reinforcing application diversity that shields the jojoba oil market from single-sector cyclicality.

Geography Analysis

Asia-Pacific held 46.68% of volume in 2025 and is on track for a 6.82% CAGR to 2031. China’s NMPA expedited organic-ingredient clearance, enabling indie clean-beauty brands to launch jojoba-rich serums within 90 days. India’s Ayurvedic formulators integrate jojoba into scalp oils to combat humidity-driven barrier loss, and K-beauty routines in Seoul favor lightweight ampoules that showcase the oil’s quick absorption.

North America benefits from Arizona and California farms that cut lead times to four weeks, insulating buyers from Red Sea route risks. The men’s grooming wave, with beard oils at USD 46 per ounce, is amplifying SKU counts in direct-to-consumer channels. Canada’s natural-products hubs in British Columbia rely on jojoba for therapeutic massage oils that meet Health Canada natural-health product rules.

Europe enforces EC 1223/2009, nudging formulators away from synthetic emollients toward Fair for Life-certified jojoba. Germany, the UK, and France anchor demand as L’Oréal and Beiersdorf upscale anti-aging portfolios. Nordic hair-care lines adopt jojoba to offset hard-water tangling, and Italy ties the oil to reef-safe after-sun lines that capitalize on Mediterranean tourism.

Competitive Landscape

The Jojoba Oil market is moderately concentrated. Start-ups engineering yeast-based wax esters threaten to undercut land-based production by 2028, but regulatory hurdles under the European Union (EU) Novel Food statutes slow their entry. Incumbents are hedging by co-developing hybrid blends that combine agricultural and fermented fractions, preserving quality narratives while diversifying feedstock risk.

Jojoba Oil Industry Leaders

Vantage Specialty Chemicals Inc.

Eco Oil Argentina S.A

Jojoba Desert

Purcell Jojoba

Inca Oil SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The Oman Agriculture Development Company (OADC), a subsidiary of the state-owned Oman Food Investment Holding Company (Nitaj), launched an initiative to cultivate commercially valuable jojoba trees. The project aims to plant jojoba trees over a 1.2 million m² desert expanse in Rima, in the Wilayat of Haima. This initiative can boost the Jojoba Oil market substantially.

- April 2025: Jojoba Desert unveiled two new ingredient lines under its latest product category: JD ESTERS. This launch signifies an expansion of JD's innovation portfolio, providing formulators with sustainable, high-performance solutions derived from oil-free hydrogenated jojoba oil.

Global Jojoba Oil Market Report Scope

Jojoba oil is a liquid wax extracted from the seeds of the Simmondsia chinensis plant. It is primarily used as a non-comedogenic, nutrient-rich moisturizer for skin, hair, and acne treatment, often called a carrier oil or liquid wax.

The Jojoba oil market is segmented by type, application, and geography. By type, the market is segmented into cold-pressed jojoba oil and refined jojoba oil. By application, the market is segmented into cosmetics and personal care, pharmaceuticals, industrial, and other applications (food and beverage and animal feed and pet care). The report also covers the market size and forecasts for jojoba oil in 17 countries across major regions. The market sizes and forecasts are provided in terms of volume (tons).

| Cold-Pressed Jojoba Oil |

| Refined Jojoba Oil |

| Cosmetics and Personal Care |

| Pharmaceuticals |

| Industrial |

| Other Applications (Food and Beverage and Animal Feed and Pet Care) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Cold-Pressed Jojoba Oil | |

| Refined Jojoba Oil | ||

| By Application | Cosmetics and Personal Care | |

| Pharmaceuticals | ||

| Industrial | ||

| Other Applications (Food and Beverage and Animal Feed and Pet Care) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will global demand for jojoba oil be by 2031?

The Jojoba Oil Market size was valued at 20.13 kilotons in 2025 and is estimated to grow from 21.38 kilotons in 2026 to reach 28.91 kilotons by 2031, at a CAGR of 6.22% during the forecast period (2026-2031).

Which product type is growing fastest?

Cold-pressed grades are leading, expanding at a 6.48% CAGR for the forecast period (2026-2031) as clean-label audits intensify.

What is driving pharmaceutical adoption of jojoba oil?

Micro-emulsion drug-delivery systems employ jojoba’s wax esters to raise dermal bioavailability by up to 60%.

Why is Asia-Pacific the largest regional market?

China, India, and ASEAN leverage clean-beauty imports and Ayurvedic scale-up, accounting for 46.68% of 2025 volume.

Page last updated on: