Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.74 Billion |

| Market Size (2026) | USD 10.16 Billion |

| Market Size (2031) | USD 12.57 Billion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Probiotics Market Analysis by Mordor Intelligence

The Japan probiotics market size was valued at USD 9.74 billion in 2025 and estimated to grow from USD 10.16 billion in 2026 to reach USD 12.57 billion by 2031, at a CAGR of 4.33% during the forecast period (2026-2031). A super-aged population, faster Foods with Function Claims (FFC) approvals, and broad cultural acceptance of fermented foods are steering demand toward daily gut and immune maintenance. Supermarkets still anchor volume, yet online retail subscriptions and vending machine launches are broadening their reach to younger, mobile consumers. Scale players are bolstering factory capacity, direct-to-consumer networks, and proprietary strains to protect share while smaller entrants find room in postbiotic niches. Rising compliance costs following the 2025 FFC labeling proposal and the 2024 Beni-koji recall favor manufacturers that can document strain traceability, clinical validation, and adherence to Good Manufacturing Practice.

Key Report Takeaways

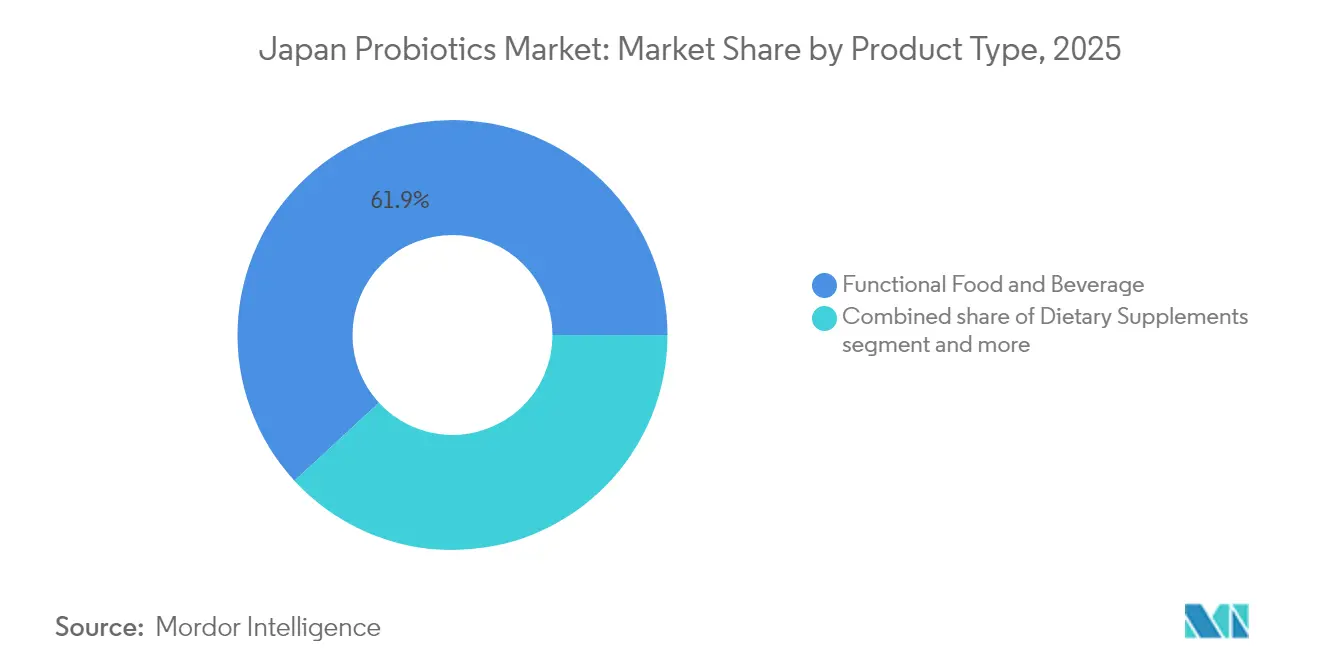

- By type, functional food and beverages led with a 61.85% share of the Japan probiotics market in 2025, while dietary supplements are expected to advance at a 6.35% CAGR through 2031.

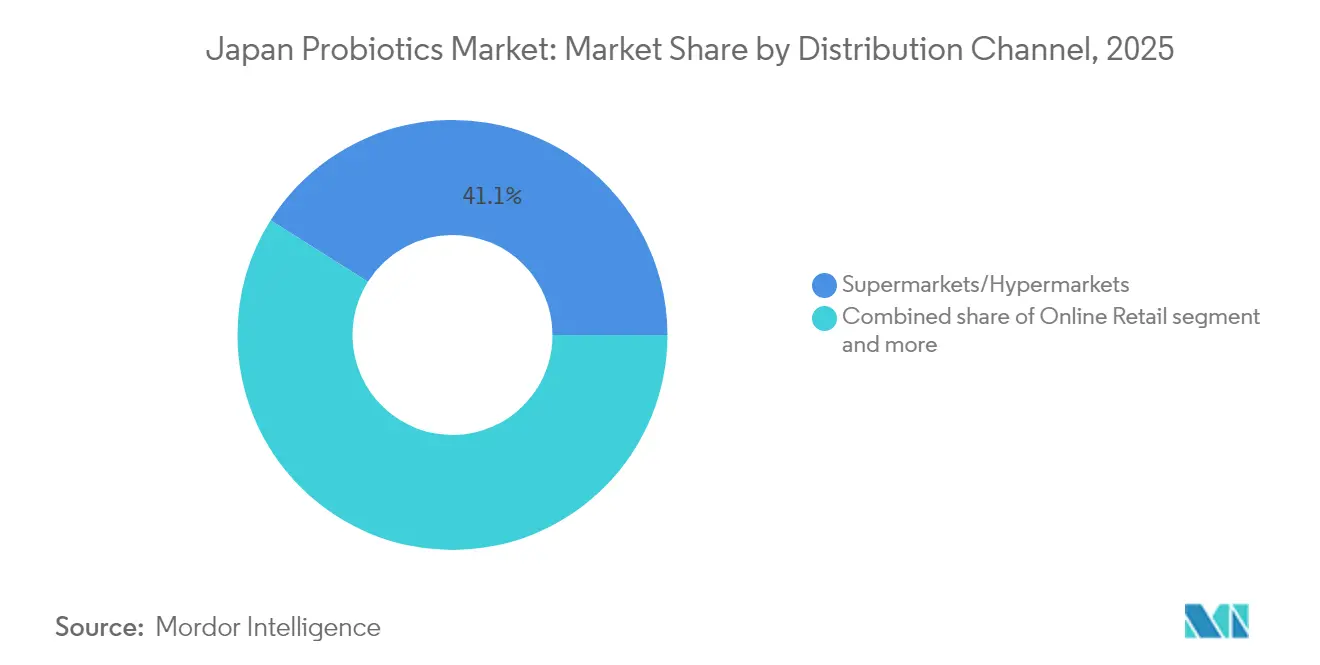

- By distribution channel, supermarkets and hypermarkets held 41.05% share of the Japan probiotics market size in 2025; online retail is projected to expand at a 7.22% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Probiotics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Age-driven focus on preventive gut and immune health | +1.2% | National, concentrated in urban prefectures (Tokyo, Osaka, Kanagawa) with highest elderly ratios | Long term (≥ 4 years) |

| Expansion of FFC/FOSHU health-claim approvals | +1.0% | National, regulatory framework administered by Consumer Affairs Agency | Medium term (2-4 years) |

| Rising health consciousness among consumers | +0.9% | National, accelerated post-pandemic in metropolitan areas | Short term (≤ 2 years) |

| Strong cultural acceptance of fermented foods | +0.8% | National, deeply embedded in dietary patterns across all regions | Long term (≥ 4 years) |

| Expansion of functional and fortified food categories | +1.1% | National, with higher penetration in convenience-store-dense urban centers | Medium term (2-4 years) |

| Innovations in probiotic strains tailored to Japanese consumers | +0.7% | National, research and development concentrated in the Kanto and Kansai industrial clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Age-driven focus on preventive gut and immune health

Nearly 29.3% of Japan’s residents are now aged 65 or older, prompting a shift in policy from treating illness to preventing it through a balanced diet[1]Source: Statistics Bureau of Japan, “Population Estimates,” stat.go.jp. The Health Japan 21 program encourages a higher intake of dietary fiber and fermented products, incorporating probiotics into government-endorsed lifestyle guidance. Yakult’s capacity expansion added 2.85 million bottles per day in January 2024 to supply contracts with municipal health centers that distribute probiotic drinks to seniors. Meiji followed in October 2025 with the world’s first HbA1c-lowering yogurt, targeting 10 million pre-diabetic adults and underscoring that probiotics are moving closer to clinical nutrition. Physicians now prescribe functional foods identified during mandatory Specific Health Checkups, pushing the Japan probiotics market deeper into the healthcare continuum.

Expansion of FFC/FOSHU health-claim approvals

The Foods with Function Claims (FFC) system, launched in 2015, overtook FOSHU in market value by 2020, reaching JPY 546 billion (USD 3.6 billion) by 2022 with 1,412 product registrations in its first three years, allowing manufacturers to self-certify using existing literature and cut time-to-market from 24 months to 60 days[2]Source: Consumer Affairs Agency, “Foods with Function Claims System,” caa.go.jp. This fueled condition-specific probiotic products like Kirin’s iMUSE line, which earned JPY 20 billion (USD 133 million) in 2024 across 59 products from 16 partners without costly clinical trials. Regulatory tightening looms with the Consumer Affairs Agency’s 2025 Proposal 235080082 on adverse-event reporting and labeling, while the 2024 Beni-koji contamination accelerated GMP adoption, raising costs for new entrants. Domestic FFC validation is also enabling exports, as seen with Morinaga’s July 2024 M-63 strain registration in China.

Rising health consciousness among consumers

Post-pandemic surveys show 31% of adults now understand the term “immune care,” more than triple pre-2020 awareness. Kirin’s “Genki na Meneki” partnership sent immunity kits to 20,000 schoolchildren in 2024, linking measurable immune markers with product use and normalizing clinical language in grocery aisles[3]Source: Kirin Holdings, “Kirin Integrated Report 2024,” kirinholdings.com. Shiseido’s inner-beauty probiotic powder for skin hydration and Asahi’s CP2305 postbiotic for stress reduction extend the category beyond digestive wellness, meeting consumer demand for organ-specific benefits. With each new claim, from visceral fat to sleep quality, the Japan probiotics market gains permission to charge premium pricing rooted in clinical outcomes.

Strong cultural acceptance of fermented foods

Japan’s millennium-long fermentation heritage, from miso and natto to tsukemono, primes local palates for probiotics, bypassing the educational hurdles common in Western markets. Yakult’s Lactobacillus casei Shirota drink, launched in 1935, reaches 8 million households weekly via its “Yakult Ladies” service, embedding probiotics into daily routines. Familiar formats, such as ready-to-drink teas and plant-based yogurts with heat-stable postbiotics, continue to evolve while remaining culturally resonant. International entrants often acquire domestic brands or invest heavily in awareness campaigns to catch up, highlighting Japan’s durable local moat.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strain stability and shelf-life challenges | -0.9% | National, acute in rural areas with limited cold-chain infrastructure | Medium term (2-4 years) |

| Limited consumer awareness of advanced probiotic strains | -0.5% | National, more pronounced in aging rural populations | Short term (≤ 2 years) |

| Shelf-life and cold-chain cost pressures | -0.7% | National, disproportionately affects small manufacturers and e-commerce | Medium term (2-4 years) |

| Strict regulatory compliance for health claims | -0.6% | National, administered by Consumer Affairs Agency and MHLW | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strain stability and shelf-life challenges

Maintaining viable probiotic cell counts through manufacturing, distribution, and retail remains a technical bottleneck, with studies showing losses of 0.02–0.13 log CFU per day under typical conditions. Yakult’s 5.5-day and Activia’s 11.3-day distribution dwell times require initial counts of 7.5–9.0 log CFU/g, which raises costs and limits formulation flexibility. Additionally, temperature excursions, especially in humid Japanese summers, further threaten viability. Morinaga’s bifidobacteria powder technology stabilizes strains for ambient distribution but demands expensive spray-drying infrastructure. Postbiotics, such as Kirin’s LC-Plasma and Asahi’s CP2305, avoid viability issues but sacrifice the live-microbe narrative. The lack of standardized viability testing regulations adds compliance uncertainty, complicating cross-border trade and eroding consumer trust.

Limited consumer awareness of advanced probiotic strains

FFC products must now display clearer strain information and maintain adverse-event logs, adding documentation layers and potential label revisions every time rules evolve. Full FOSHU approval still costs USD 1–3 million in clinical studies, steering most innovation toward FFC, even though it offers lower reimbursement in health insurance channels. Export ambitions are hindered by friction because EU and U.S. regulators do not recognize Japan’s claim structure, resulting in redundant trials. Morinaga’s M-63 strain required fresh datasets for China’s approval in July 2024, even after domestic validation, which stretched payback periods for research and development. Small brands that cannot afford to conduct duplicate studies often resort to generic positioning, thereby keeping the Japanese probiotics market concentrated among well-capitalized firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Functional Foods Anchor, Supplements Surge

In 2025, functional food and beverages captured 61.85% of the Japan probiotics market share, a testament to the national preference for health benefits delivered through everyday meals. Supplements, growing at a 6.35% CAGR to 2031, reflect consumer appetite for precise dosing and physician-advised interventions. Yakult’s plant-based factory, opened in October 2024, expands the functional beverage appeal to lactose-intolerant and vegan shoppers. Meiji’s SAVAS Milk Protein yogurt layers sports nutrition onto fermented dairy, proving that hybrid products can defend the dominant food format from supplement encroachment. Still, premium capsules like Otsuka’s equol-producing Lactococcus 20-92 command pharmacy pricing that functional foods rarely achieve, illustrating a bifurcated value pool within the Japanese probiotics market size.

Second-generation formats are reshaping each side of the ledger. Postbiotic teas and probiotic chocolates allow for ambient shelving, unlocking vending machines and confection aisles that were once off-limits to chilled yogurt. Meanwhile, clinical-strength HbA1c-lowering yogurts and bone-density ice creams blur boundaries between meal and medicine, expanding what consumers accept as “food.” These continuous format innovations reinforce the perception that the Japan probiotics market is less a static category and more a technology platform for condition-specific nutrition.

By Distribution Channel: Digital Disrupts, Konbini Adapts

Supermarkets and hypermarkets accounted for 41.05% of 2025 sales, thanks to their broad refrigerated aisles and long-standing ties with leading dairy brands. Yet online retail, scaling at a 7.22% CAGR, introduces subscription packs and label-less six-packs that cut weight and cost for courier networks. Yakult’s e-commerce launch in October 2024 demonstrates how incumbents are adapting packaging to optimize truckload density while preserving brand equity. Convenience stores now offer frozen yogurt cups and single-serve probiotic jellies, generating impulse purchases on commuter routes.

Specialty and drugstores play a significant role in supplement uptake; Meiji’s HbA1c yogurt reaches pharmacists who explain the metabolic benefits and justify the premiums. Vending machines, once excluded by refrigeration needs, now stock LC-Plasma drinks that are stable at ambient temperature, adding a 40-billion-unit channel to the Japanese probiotics market. Rural logistics remain costly, but Kirin’s Fancl acquisition puts 2,500 retail doors within reach of heat-stable formats, pushing functional products into towns where cold-chain trucks run infrequently.

Geography Analysis

Greater Tokyo, Osaka, and Kanagawa drive volume through dense convenience-store grids and high e-commerce penetration, translating urban lifestyles into daily functional food purchases. The Ministry of Health’s Specific Health Checkup program funds probiotic prescriptions for metabolic indicators, turning city clinics into health-claim springboards. Rural prefectures, often with elderly residents exceeding 30%, encounter fewer chilled deliveries; yet, ambient-stable teas and powders close availability gaps, preventing geographic stagnation.

Export spillovers are growing: Yakult debuted Y1000 in Singapore in October 2024, while its Georgia, U.S. factory, slated for 2026, underscores cross-Pacific ambitions. Morinaga’s China-bound M-63 strain and Asahi’s ADM partnership demonstrate that domestic regulatory validation opens Asian gateways if firms can manage redundant local trials. However, differing health-claim rules curb short-term profitability, keeping the Japan probiotics market primarily inward-looking.

Hokkaido and Tohoku, which are colder and have wider delivery distances, favor shelf-stable postbiotics over refrigerated yogurts. Kyushu and Shikoku, which house some prefectures where 30% or more of the citizens are over 65, are seeing a rapid uptake of bone-density and metabolic formulas, exemplified by Meiji’s tofu-sensory YOFU yogurt. Kanto and Kansai clusters host most corporate reesearch and dvelopment labs, benefiting from proximity to universities and regulators, accelerating strain innovation and FFC submissions. Even Okinawa’s longevity culture inspires probiotic blends targeting healthy aging, albeit at modest commercial scale due to small population.

Regulatory Landscape

Probiotic-containing products in Japan are governed under two main health-claim pathways, Foods for Specified Health Uses (FOSHU) and Foods with Function Claims (FFC), overseen through the Consumer Affairs Agency (CAA) framework. FOSHU uses a pre-market approval model with safety and efficacy evaluation supported by the Food Safety Commission of Japan, which creates a higher-barrier route typically aligned to products pursuing government-reviewed claims. FFC is notification-based, where operators submit a notification to the CAA at least 60 days before commercialization and are responsible for scientific substantiation and safety, with supporting evidence published for transparency on the CAA system.

Compliance links to Japan's Food Labeling Standards, which made nutrition labeling mandatory for processed foods in 2015 and shapes how probiotic and postbiotic claims are presented in-market. The FFC structure also includes post-marketing accountability, including evidence maintenance and surveillance practices tied to the program's disclosure requirements. Companies must select a single claim pathway per product because foods cannot carry both FOSHU and FFC labeling simultaneously, which tends to favor manufacturers that can document strain identity, safety evaluation approaches (including FAO/WHO-aligned safety assessment concepts used by Japanese authorities), and consistent label governance across frequent product renewals and line extensions.

Competitive Landscape

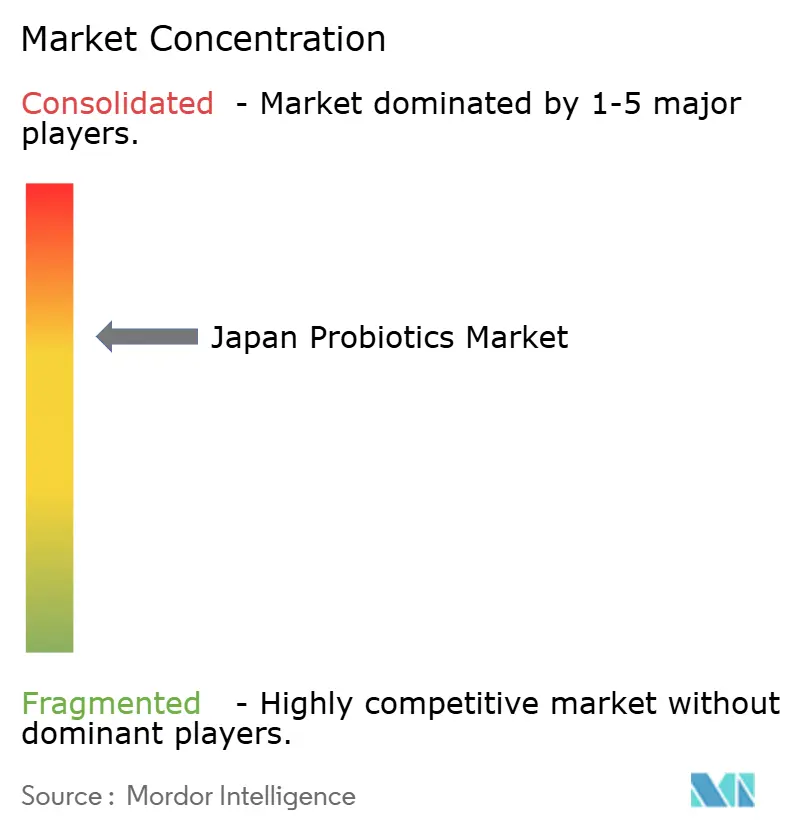

The Japan probiotics market is moderately consolidated, with Yakult Honsha, Meiji Holdings, Morinaga Milk Industry, Danone, and Nestlé collectively dominating. However, these incumbents face increasing pressure from niche entrants leveraging postbiotic formulations and microencapsulation technologies. Yakult’s January 2024 capacity expansion of 2.85 million bottles per day and its October 2024 launch of a plant-based factory demonstrate how leading players defend their market share through vertical integration and format diversification[4]Source: Yakult Honsha Co., Ltd., “Investor Relations,” yakult.co.jp. Similarly, Kirin’s October 2024 acquisition of Fancl, a 2,500-store supplement retailer, signals a strategic pivot toward health science, with the company aiming to grow revenue from this segment to 20% within a decade. Multinationals like Danone, through its May 2024 acquisition of Functional Formularies and March 2024 purchase of Promedica, are capturing plant-based and medical nutrition segments that domestic players historically underinvested in.

Technology and proprietary research remain the primary competitive axis. Morinaga’s viable bifidobacteria powder, which stabilizes strains for ambient distribution, and Meiji’s MI-2 strain, the first globally to achieve an HbA1c-lowering claim, illustrate how incumbents weaponize research and development to defend pricing power. Kirin’s 33 peer-reviewed publications on LC-Plasma and its global patent portfolio reflect a decade-long investment in intellectual property that smaller entrants cannot replicate. Emerging disruptors, such as KINS Corporation, backed by Nippon Express Holdings in April 2024, are targeting underserved microbiome-care and companion-animal probiotic segments where incumbents lack clinical validation or distribution infrastructure.

Regulatory and strategic developments are further shaping the market landscape. The Consumer Affairs Agency’s February 2025 tightening on reporting and labeling is expected to accelerate consolidation, forcing smaller players without compliance infrastructure to exit or be acquired. Strategic partnerships are also proliferating: ITOCHU Corporation’s October 2024 acquisition of a 25% stake in Maypro Group, a U.S. ingredient supplier, positions the Japanese trading house to bridge domestic probiotic manufacturers with international distribution networks. At the same time, white-space opportunities remain in postbiotics, where Asahi’s CP2305 and Kirin’s LC-Plasma portfolios create defensible niches by bypassing cold-chain constraints and enabling ambient distribution.

Japan Probiotics Industry Leaders

Yakult Honsha Co. Ltd

Meiji Holdings

Morinaga Milk Industry Co., Ltd.

Danone

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A practical opportunity is emerging around scalable, evidence-led postbiotic and functional-ingredient platforms that can move across categories (beverages, tablets, powders) while reducing dependence on cold-chain distribution. Kirin has built a commercial base in LC-Plasma, and its annual sales of the proprietary postbiotic material exceeded JPY 28 billion in 2025, indicating that ingredient-led models can generate value beyond single-brand yogurt economics and support broader partner routes. Asahi Group Foods also moved to extend its CP2305 platform internationally via a supply agreement with ADM Wild Valencia (announced February 2025), creating an outlet for Japanese-origin strains or postbiotic materials to reach overseas food, supplement, and ingredient customers using existing distribution infrastructure.

Investment in science and facilities offers a second lever for participants competing in an environment where the Japanese market rewards documented function under FFC and, for select SKUs, the more stringent FOSHU pathway. Kirin announced in February 2026 that it will allocate JPY 3.5 billion in 2026 for new research facilities at its Institute for Technology of Microbial Science, alongside a stated goal of increasing R&D investment to around 1.5 times the 2025 level by 2035. That direction points to a near-to-long-term outlook centered on proprietary strains and published evidence packages, with formats that can be distributed through online retail and ambient channels, including vending and subscription logistics, rather than relying only on refrigerated dairy volume.

Recent Industry Developments

- June 2026: Morinaga Milk Industry published new research on Bifidobacterium longum BB536, including work in the journal Aging linking BB536 yogurt intake plus lifestyle improvements to changes in aging-related markers over a three-month program. The publication pipeline strengthens strain-level differentiation and supports premium positioning for BB536-containing products across yogurt and supplement formats.

- October 2025: Meiji Holdings launched Inner Garden, a personalized gut-health service that combines gut flora testing with tailored daily cocoa drinks formulated with selected fibers and oligosaccharides. The service extends probiotics-adjacent demand from mass functional dairy into personalized nutrition, creating a higher-margin engagement model that can support repeat purchase behavior and new claim-led formulations.

- October 2024: Kirin completed its acquisition of Fancl, adding a large supplement-focused retail footprint in Japan to its health science portfolio. The deal improves access to pharmacy and health-store style distribution for probiotic and postbiotic offerings and supports cross-selling of immune-care concepts alongside existing functional beverage platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Japan probiotics market is the value of products sold in Japan that contain beneficial live microorganisms and are positioned for health benefits, across foods, beverages, supplements, and related uses.

Scope exclusions: We exclude broader digestive health items that do not contain probiotic strains (for example, general vitamins, fibers, or enzymes sold without live culture claims).

Segmentation Overview

- By Type

- Functional Food and Beverage

- Dietary Supplements

- Animal Feed

- Others

- By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores (Pharmacies/Health Stores)

- Online Retail

- Other Distribution Channel

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, map the route to market, and build a clean fact base before any modeling was finalized. We typically start with official statistics and reference material such as Japan's Ministry of Health, Labour and Welfare, the Consumer Affairs Agency (including FOSHU and FFC related public information), Statistics Bureau of Japan consumer spending series, and Japan Customs trade statistics for relevant ingredient flows.

To avoid over-counting, we cross-check information with public company filings and investor presentations, reputable press coverage, trade association websites, and peer-reviewed journals that discuss probiotic strains and usage outcomes. Where helpful, we use paid subscription sources that aggregate company financials, patent activity, and shipment-level import-export records to sanity-check directionality and timing, especially when product launches or labeling changes affect sales. The sources listed here are illustrative only, and many other public references were also used for data collection, cross-verification, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually counted as probiotics in Japan across foods and supplements, and how pricing and channel mix are shifting in real time. Respondent input helped confirm the practical definitions used for probiotic strains and the mapping of pack sizes and price tiers into market value, including how adoption varies across major consumption hubs in Japan. We spoke with a mix of brand owners, ingredient suppliers, channel participants, and domain experts so assumptions on penetration, pack sizes, and premiumization could be checked against current sales behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | |

| Mid tier: 49% | Functional/Unit leaders: 29% | |

| Smaller Players: 14% | Managers: 59% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs Japan demand from category consumption and spend signals, then converts this into probiotics value using validated penetration and price points. We then corroborate the outcome with selective bottom-up checks, such as rolling up a sample of supplier and brand revenues, and testing implied volumes using typical pack sizes and average selling price ranges.

Key inputs used in the model include the split of probiotics between functional foods and beverages versus dietary supplements, the channel mix (convenience stores, supermarkets, specialty health outlets, and online), average price per pack by format, adoption among older consumers, and the pace of claim and labeling activity under FFC and FOSHU aligned products. Where bottom-up references create gaps, we handle them through conservative interpolation anchored to channel share and observed price ladders, then re-check using interview feedback.

Forecasting uses scenario analysis with a light regression layer, where growth is linked to category premiumization, channel shift toward online replenishment, and the expected pace of new product activity. Assumptions are kept practical so the model can be re-run each year using refreshed public indicators and repeated expert checks.

Data Validation & Update Cycle

Outputs are validated through multiple checks, starting with internal consistency tests across channel totals, format mix, and implied per-capita spend. Outliers are flagged and reviewed against independent signals such as ingredient trade direction, pricing movements, and any major regulatory or safety events that could temporarily distort demand.

Before sign-off, assumptions that drive the largest value impact are re-tested with follow-up expert touchpoints, and a separate analyst review is used to confirm that no double counting exists across product forms. The report is refreshed annually, and interim updates are made when material events occur, after which a final pre-delivery sweep is completed so the numbers reflect the latest available information.

Mordor Intelligence's Japan Probiotics Market Market Size Measured Against Other Published Estimates

Published market sizes for Japan probiotics often differ, even when the time period looks similar, because the counted product universe and the pricing logic are not the same. Differences usually come from whether functional foods and beverages are fully included, how online pricing is treated, and how strictly live-culture probiotic products are separated from adjacent digestive health items.

In practice, the biggest gaps tend to come from scope rules and how value is converted to USD, since some estimates lean heavily toward supplements only or apply a narrower channel set, while others use aggressive premiumization assumptions without re-checking pack sizes and discounting patterns.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.74 B (2025) | |

| Industry Research Publisher A | USD 4.27 B (2025) | The smaller figure is consistent with a tighter counted universe and tends to align more with a supplements-led view, which can understate Japan functional foods and beverage sales where probiotics are a routine purchase. |

| Data Platform B | USD 0.50 B (2024) | This estimate is specific to probiotics dietary supplements and excludes the much larger foods and beverages component, so it will not match an all-format Japan probiotics total. |

The spread in the table is mainly explained by whether foods and beverages are counted alongside supplements, and by how channel pricing is normalized, which is why the broader all-format view lands higher when applied consistently, a scope choice reflected in Mordor Intelligence.

Key Questions Answered in the Report

How large is the Japan probiotics market in 2026?

The market is valued at USD 10.16 billion in 2026 and is on track to reach USD 12.57 billion by 2031.

What is driving growth in Japanese probiotics?

An aging society, faster FFC approvals, and strong cultural acceptance of fermented foods form the primary growth engine.

Which segment is expanding fastest?

Dietary supplements are posting the highest growth, advancing at a 6.35% CAGR through 2031.

Are postbiotics important in Japan’s market?

Yes, heat-stable postbiotics like Kirin’s LC-Plasma and Asahi’s CP2305 are opening vending and e-commerce channels by avoiding cold-chain limits.

Which channels are gaining share?

Online subscriptions and convenience-store impulse formats are rising fastest, although supermarkets remain the volume leader.

Page last updated on: