Asia-Pacific Commercial HVAC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

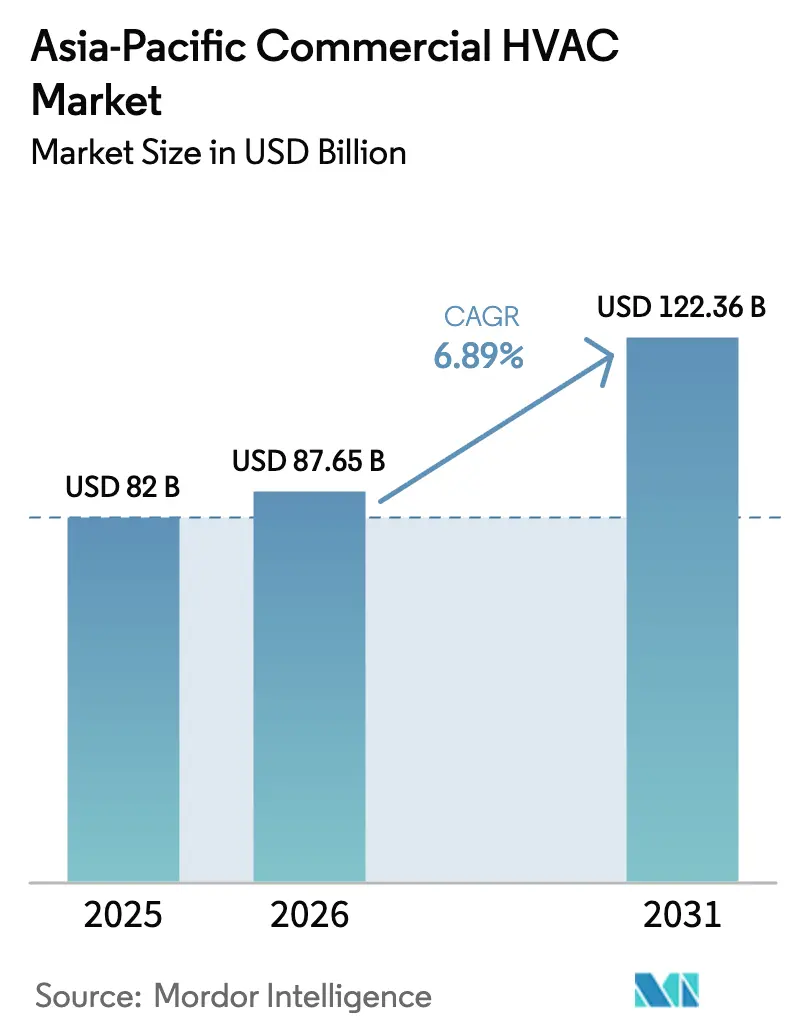

| Base Year Market Size (2025) | USD 82 Billion |

| Market Size (2026) | USD 87.65 Billion |

| Market Size (2031) | USD 122.36 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

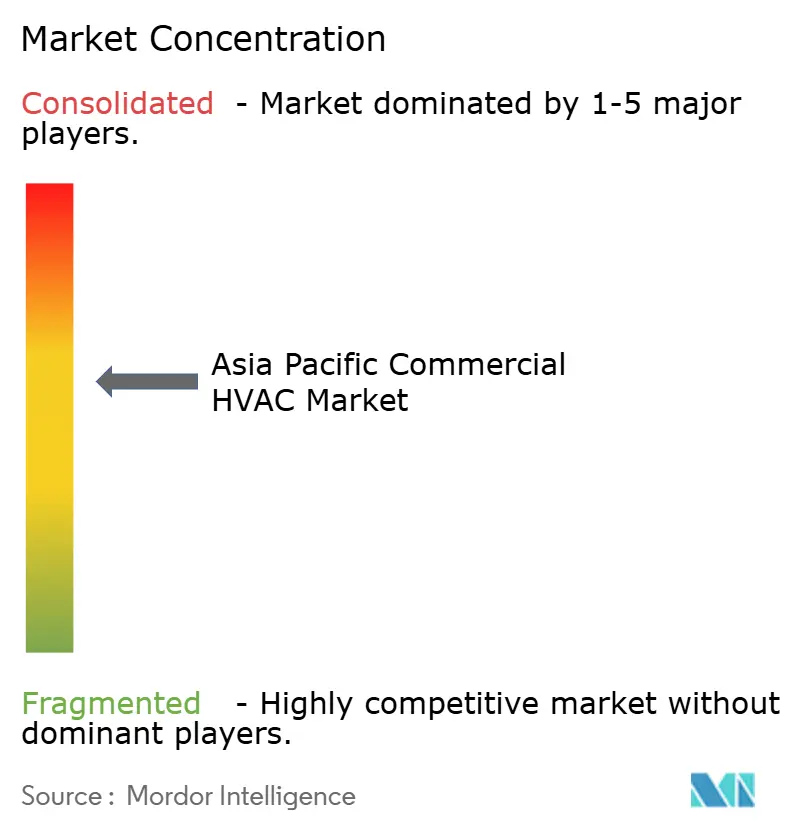

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Commercial HVAC Market Analysis by Mordor Intelligence

The Asia-Pacific commercial HVAC market size was valued at USD 82 billion in 2025 and estimated to grow from USD 87.65 billion in 2026 to reach USD 122.36 billion by 2031, at a CAGR of 6.89% during the forecast period (2026-2031). Urbanization, green-building codes, and net-zero targets are pushing developers and owners toward low-carbon heating and cooling, while stricter refrigerant regulations accelerate equipment replacement cycles. Rapid data-center growth, government heat-pump incentives, and AI-enabled controls continue to reshape product development and service models across the region. Multinational suppliers scale R&D around low-GWP refrigerants, and Chinese manufacturers leverage cost leadership to penetrate export markets. Supply-chain constraints and technician shortages add near-term friction yet also expand the services opportunity as owners outsource lifecycle risk.

Key Report Takeaways

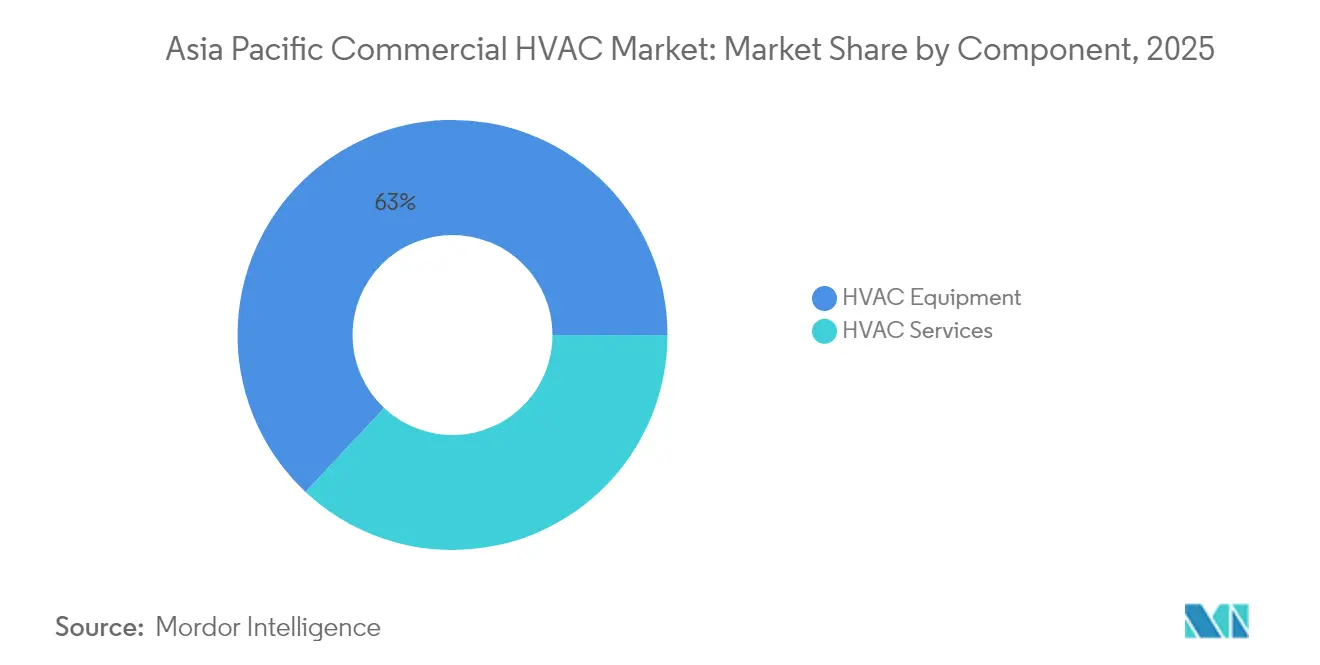

- By component, HVAC equipment led with 63.02% revenue share in 2025 in the Asia-Pacific commercial HVAC market; services are projected to expand at an 8.29% CAGR through 2031.

- By system type, cooling and ventilation held 48.10% of Asia-Pacific commercial HVAC market share in 2025, while heat-pump solutions are poised for a 7.98% CAGR to 2031.

- By end-user sector, offices and commercial buildings accounted for 37.05% of the Asia-Pacific commercial HVAC market size in 2025; data centers record the fastest growth at 7.77% CAGR.

- By refrigerant and technology, traditional HFC systems retained 54.20% share in 2025 in the Asia-Pacific commercial HVAC market, yet low-GWP alternatives are set to rise at an 8.17% CAGR.

- By country, China captured 40.15% share in 2025 in the Asia-Pacific commercial HVAC market, whereas India is expected to grow at a 7.85% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Proportional positioning is established by comparing regional contributions against the global total, including that of Asia. The commercial hvac market share in our global report expresses these relative weights.

Asia-Pacific Commercial HVAC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid policy-driven phase-out of high-GWP refrigerants | +1.5% | Global, with early implementation in Australia, Japan | Medium term (2-4 years) |

| Accelerating green-building certification adoption | +0.8% | APAC core, strongest in Singapore, Hong Kong, Australia | Long term (≥ 4 years) |

| Surge in data-center construction and cooling demand | +1.2% | China, India, Singapore hub markets | Short term (≤ 2 years) |

| Urban district-cooling and heating network investments | +0.9% | Singapore, Hong Kong, select Chinese tier-1 cities | Long term (≥ 4 years) |

| Corporate net-zero commitments driving HVAC retrofits | +1.1% | Japan, South Korea, Australia corporate sectors | Medium term (2-4 years) |

| Government stimulus for regional heat-pump manufacturing | +0.7% | China, India manufacturing bases | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Phase-Out of High-GWP Refrigerants

Asia-Pacific governments are translating Kigali Amendment pledges into national policy, compelling an 80–85% reduction in HFC use before 2045. Australia is already tracking toward an 85% decline by 2036, while China froze HFC production and consumption in 2024. This brings forward replacement cycles, compressing payback periods and creating a USD 15 billion addressable pool for low-GWP systems. Japan’s METI budgeted USD 2.8 billion in 2024 to help domestic OEMs redesign product lines, effectively positioning local brands as export hubs for compliant technology.[1]“Budget Details for Heat-Pump Promotion,” Ministry of Economy, Trade and Industry, meti.go.jp

Accelerating Green-Building Certification Adoption

Mandatory and voluntary green-rating schemes such as Singapore’s Green Mark and Hong Kong’s BEAM Plus continue to expand the premium segment for high-efficiency HVAC. Singapore now requires Green Mark on all new commercial assets above 2,000 m², guaranteeing a pipeline for variable-refrigerant-flow (VRF) and smart-control upgrades that cut energy use by 30–50%. Developers realize 15–25% rental uplifts on certified buildings, converting sustainability into topline pricing power.

Surge in Data-Center Construction and Cooling Demand

Hyper-scale providers are building more than 150 new facilities across Asia-Pacific through 2025, with China and India leading capacity additions. Cooling can consume 30–40% of facility power, and AI workloads elevate thermal loads further, spurring uptake of liquid, immersion, and direct-to-chip designs. LG Electronics booked USD 720 million in regional data-center cooling orders in 2024 alone.[2]Corporate Newsroom, “LG Scores Major Data-Center Cooling Orders,” LG Electronics, lg.com

Urban District-Cooling and Heating Network Investments

Marina Bay in Singapore operates the world’s largest underground district-cooling grid, saving 40% energy over stand-alone chillers and expanding toward 1,000 RT by 2025. Similar guidelines emerged in Hong Kong in 2024 to serve dense business districts. China earmarked USD 12 billion to pilot combined cooling, heating, and power networks in top-tier cities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortage and wage inflation | -0.6% | China, India, Australia installation markets | Short term (≤ 2 years) |

| High upfront cost of advanced HVAC systems | -0.4% | India, Southeast Asia price-sensitive markets | Medium term (2-4 years) |

| Supply-chain volatility for semiconductors and compressors | -0.3% | Global, with acute impact on India, Southeast Asia | Short term (≤ 2 years) |

| Regulatory uncertainty on next-gen refrigerants | -0.2% | APAC developing markets, regulatory transition zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortage and Wage Inflation

Australia projects a 15,000-technician gap by 2025, with HVAC wages rising 25% per year. China and India each face pipeline constraints for VRF and low-GWP installations, lengthening project lead times and raising service premiums. Carrier invested USD 8 million in a Singapore training hub to certify 10,000 workers annually.

High Upfront Cost of Advanced HVAC Systems

Low-GWP units cost 15-30% more than HFC models, and VRF can command a 40–60% price premium. Capital-sensitive developers in India often opt for basic split systems despite higher lifecycle energy expenses. Singapore’s Energy Efficiency Grant helps offset up to 70% of qualifying upgrade costs, narrowing payback periods for SMEs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Traction in an Equipment-Heavy Base

Asia-Pacific commercial HVAC market size for equipment reached USD 51.68 billion in 2025, equal to 63.02% of overall revenue. Services, however, post the strongest pipeline, advancing at 8.29% CAGR as owners outsource predictive maintenance and energy-performance contracting. Daikin’s Applied Service Network now spans 15 countries, guaranteeing energy savings and transferring operational risk to the provider.

In parallel, Johnson Controls lifted its regional services share to 40% of turnover in 2025. Digital twins, remote diagnostics, and ISO 50001 mandates amplify the need for specialized outsourcing, making the services slice the prime value-accretion zone through 2031.

By System Type: Heat Pumps Edge Toward the Mainstream

Cooling and ventilation equipment represented 48.10% of Asia-Pacific commercial HVAC market share in 2025, anchored by tropical climates and urban heat islands. Heat-pump systems are closing the gap with a 7.98% CAGR, supported by incentives and advanced compressor designs that boost COP in hot, humid conditions. Mitsubishi Electric’s variable-speed, vapor-injection heat pumps deliver 30% higher efficiency than legacy models.

Automation and controls also scale quickly as hybrid work patterns require granular occupancy management. Post-pandemic indoor-air-quality priorities add further impetus for demand-controlled ventilation and real-time monitoring.

By End-User Industry: Data Centers Outpace Traditional Sectors

Offices remained the largest slice with 37.05% Asia-Pacific commercial HVAC market size in 2025. Yet data centers log the fastest pace at 7.77% CAGR, fueled by hyperscale cloud, AI inference, and 5G edge nodes. Direct-to-chip liquid cooling shifts the technological frontier, and equipment vendors partner with IT integrators to co-design thermal envelopes.

Healthcare stays resilient as infection-control standards translate into higher ACH (air-change rates) and HEPA-level filtration, extending value propositions for premium air-handling units. Hospitality retrofits pick up on the back of tourism recovery and rising consumer expectations for indoor air quality.

By Refrigerant and Technology: Low-GWP Systems Scale Quickly

Traditional R-410A/R-32 equipment held 54.20% share in 2025, yet tightening quotas spur a rapid mix shift. Asia-Pacific commercial HVAC market share for low-GWP systems will cross 40% by 2031 if current uptake trends hold. Australia’s 85% phase-down target has already catalyzed accelerated HFO adoption.

Variable refrigerant flow and heat-pump hybrids increasingly ship pre-charged with lower-impact gases, and OEMs spend heavily on proprietary blends to balance flammability, efficiency, and global-warming potential.

Geography Analysis

China’s commercial HVAC revenue approached USD 32.92 billion in 2025, with Gree and Midea jointly holding more than 60% domestic share. Ongoing urban migration injects relentless baseline demand, and Beijing’s 2024 HFC freeze advances the shift to compliant refrigerants. Export-oriented component supply chains, however, face scrutiny under diversification strategies unfolding across the rest of Asia-Pacific.

India generated double-digit unit growth in room air conditioners between 2020 and 2024, reflecting rising disposable incomes and harsher urban heat indexes. The Asia-Pacific commercial HVAC market size for India is projected to compound rapidly as the data-center pipeline and government-backed infrastructure accelerate construction cycles. Technician-training bottlenecks and financing gaps remain the primary headwinds.

Japan and South Korea anchor the premium technology cohort. METI’s USD 2.8 billion heat-pump subsidy portfolio in 2024 catalyzes domestic demand and global exports. Australia leads in policy-driven HFC reduction, using utility-funded rebates that cut capex by up to 70% for qualifying retrofits. Collectively, these mature economies account for a smaller volume base yet punch above their weight in innovative deployments.

Mordor Intelligence examines the commercial hvac market across diverse other regional markets as well, including Europe, North America, and Middle East and Africa, while also offering granular country-level perspectives for Japan, China, South Korea, France, Germany, and Canada and more.

Competitive Landscape

Top five suppliers control about 60% of regional sales, signaling a moderately concentrated arena ripe for niche disruption. Daikin secures multi-country dominance through compressor vertical integration, low-GWP R&D spend above USD 500 million annually, and a growing energy-performance contracting arm. Chinese titans Gree and Midea exploit economies of scale, 18-month product-refresh cycles, and aggressive overseas pricing to challenge incumbents.

LG Electronics and Samsung differentiate via consumer-electronics user-experience DNA, embedding IoT telemetry and AI fault prediction into commercial portfolio. Patent activity climbed 40% year-on-year in 2024 as firms lock in IP around variable refrigerant flow, heat-recovery ventilation, and cloud-based optimization. Vertical specialists in data-center thermal management and district-cooling services find white-space opportunities that command premium margins.

Strategic mergers continue: Bosch’s USD 8.1 billion acquisition of Johnson Controls-Hitachi in July 2024 broadened smart-building competencies. Meanwhile, Trane’s energy-as-a-service contracts in Oceania shift value from capex to opex, mirroring broader sector evolution toward outcome-based models.

Asia-Pacific Commercial HVAC Industry Leaders

Daikin Industries, Ltd.

Midea Group Co., Ltd.

Carrier Global Corporation

Mitsubishi Electric Corporation

Samsung Electronics Co., Ltd. (HVAC Division)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Daikin Industries formed a USD 25 million joint venture in Taiwan to produce air-handling units for Southeast Asia.

- December 2024: Daikin partnered with Rechi Precision in India, investing USD 1.8 million to localize compressor output under the PLI scheme.

- November 2024: Daikin partnered with Rechi Precision in India, investing USD 1.8 million to localize compressor output under the PLI scheme.

- October 2024: LG Electronics unveiled a USD 720 million data-center cooling expansion plan across Asia-Pacific.

Asia-Pacific Commercial HVAC Market Report Scope

Commercial HVAC involves heating and cooling large properties, such as commercial buildings, restaurants, rental properties, hospitals, schools, etc. As a result of the scale, commercial heating and air conditioning differ significantly from their residential counterpart in terms of size, capacity, and operational complexity. The study tracks the revenue accrued through the sale of HVAC by various players in Asia-Pacific. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The Asia-Pacific commercial HVAC market is segmented by type of component (HVAC equipment [heating equipment and air conditioning/ventilation equipment] and HVAC services), end-user industries (hospitality, commercial buildings, public buildings, and other end-user industries), and country (China, India, Japan, and Rest of Asia-Pacific). The report offers market forecasts and size in value (USD) for all the above segments.

| HVAC Equipment |

| HVAC Services |

| Heating Equipment |

| Cooling and Ventilation Equipment |

| Control and Automation Devices |

| Hospitality |

| Offices and Commercial Buildings |

| Retail and Shopping Centers |

| Public and Institutional Buildings |

| Data Centers and ICT Facilities |

| Healthcare Facilities |

| Other End-user Industries |

| Traditional HFC Systems (R-410A/R-32) |

| Low-GWP Refrigerant Systems (HFO, Propane) |

| Variable Refrigerant Flow (VRF) Systems |

| Heat-Pump-based Systems |

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Component | HVAC Equipment |

| HVAC Services | |

| By System Type | Heating Equipment |

| Cooling and Ventilation Equipment | |

| Control and Automation Devices | |

| By End-user Industry | Hospitality |

| Offices and Commercial Buildings | |

| Retail and Shopping Centers | |

| Public and Institutional Buildings | |

| Data Centers and ICT Facilities | |

| Healthcare Facilities | |

| Other End-user Industries | |

| By Refrigerant and Technology | Traditional HFC Systems (R-410A/R-32) |

| Low-GWP Refrigerant Systems (HFO, Propane) | |

| Variable Refrigerant Flow (VRF) Systems | |

| Heat-Pump-based Systems | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size and five-year outlook for Asia Pacific commercial HVAC?

The Asia-Pacific commercial HVAC market is valued at USD 87.65 billion in 2026 and is projected to reach USD 122.36 billion by 2031, reflecting a 6.89% CAGR.

Which component segment is expanding the fastest across the region?

Services, covering predictive maintenance and energy-performance contracts-are rising at an 8.29% CAGR, outpacing the equipment base.

Why are low-GWP refrigerants gaining traction in Asia Pacific commercial HVAC?

Kigali Amendment targets are phasing down HFCs, creating a USD 15 billion opportunity for low-GWP systems and compressing equipment replacement cycles.

Which end-user sector shows the highest growth momentum?

Data centers and ICT facilities lead with a 7.77% CAGR as hyperscale and AI workloads drive demand for advanced cooling solutions.

How do skilled-labor shortages influence project timelines and costs?

A regional shortfall of certified technicians, 15,000 in Australia alone, pushes wages up 25% annually and stretches installation schedules for complex systems.

Page last updated on: