Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.15 Billion |

| Market Size (2026) | USD 5.36 Billion |

| Market Size (2031) | USD 6.58 Billion |

| Growth Rate (2026 - 2031) | 4.16% CAGR |

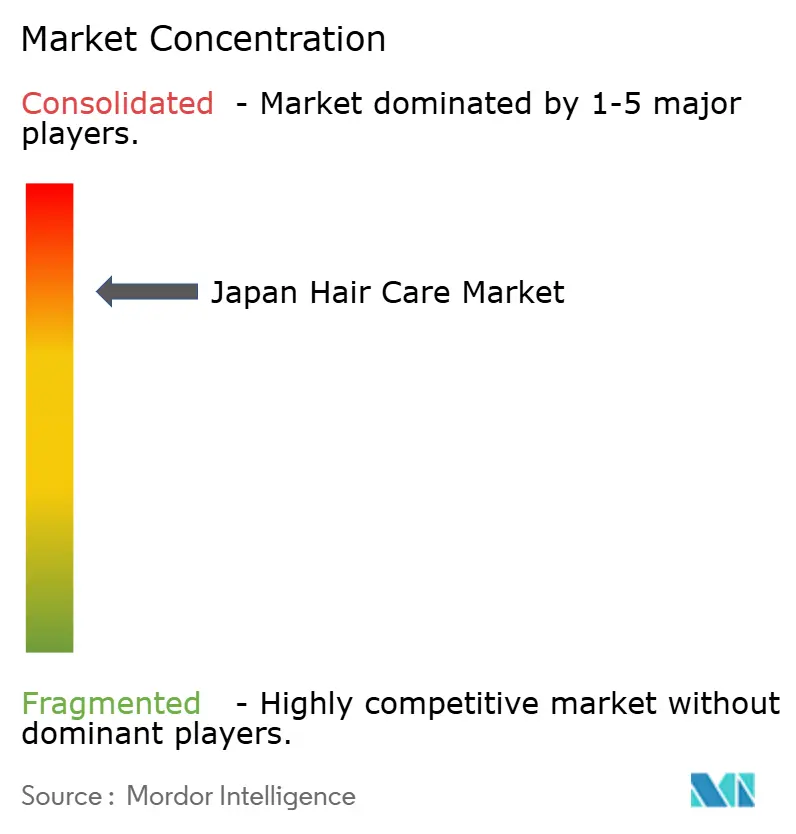

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Hair Care Market Analysis by Mordor Intelligence

The Japanese hair care market size was valued at USD 5.15 billion in 2025 and estimated to grow from USD 5.36 billion in 2026 to reach USD 6.58 billion by 2031, at a CAGR of 4.16% during the forecast period (2026-2031). The steady expansion is propelled by a super-aging population that seeks targeted scalp health and anti-thinning remedies, premiumization that rewards technology-driven formulations, and a regulatory framework that steers brands toward safer, plant-based ingredients. Demand splits between mass and premium lines; mass lines still dominate store shelves, yet premium products grow faster as older consumers use discretionary income on specialist solutions. Digital commerce reshapes the Japanese hair care market as heritage companies enhance direct-to-consumer platforms, while specialty stores retain influence through in-person consultation. Innovation remains brisk: lamella-technology shampoos, non-chemical permanent-style creators, and AI-guided personalization all allow companies to justify higher price points and shorten product-development cycles.

Key Report Takeaways

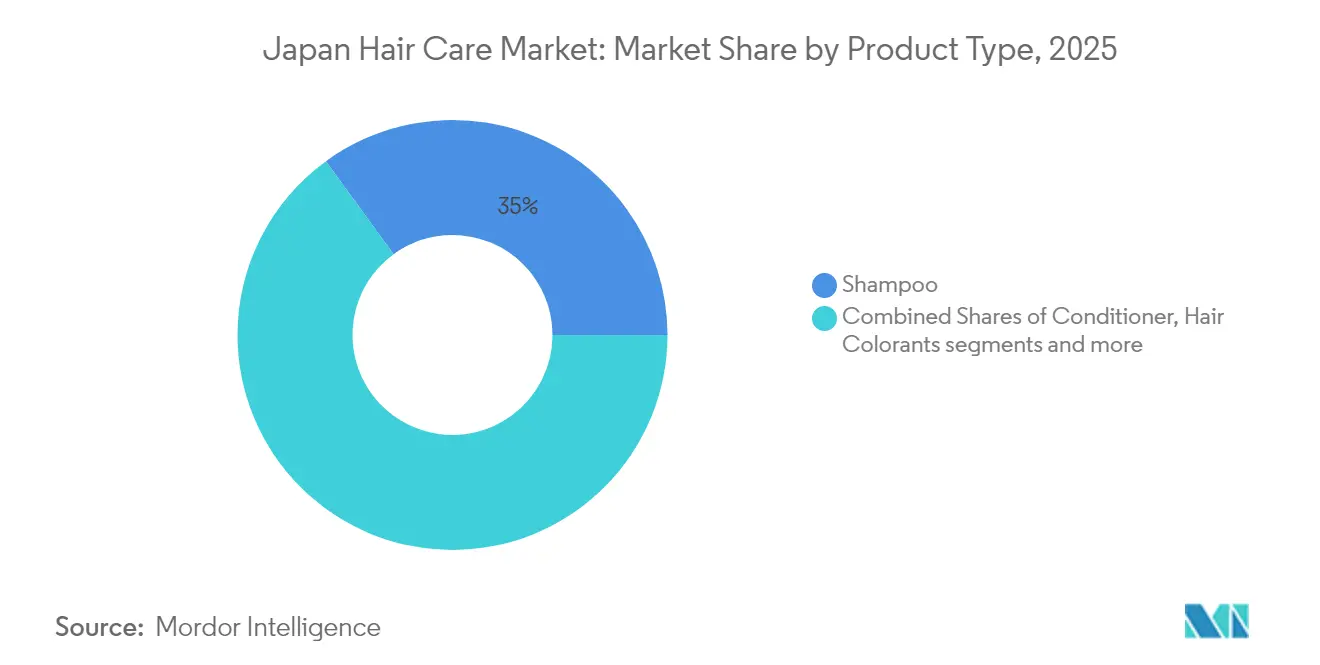

- By product type, shampoo led with 35.02% of Japan hair care market share in 2025, and styling products recorded the top projected growth at a 4.58% CAGR from 2026-2031.

- By category, mass products held 74.93% of the Japanese hair care market share in 2025, while premium products advanced at a 5.41% CAGR through 2031.

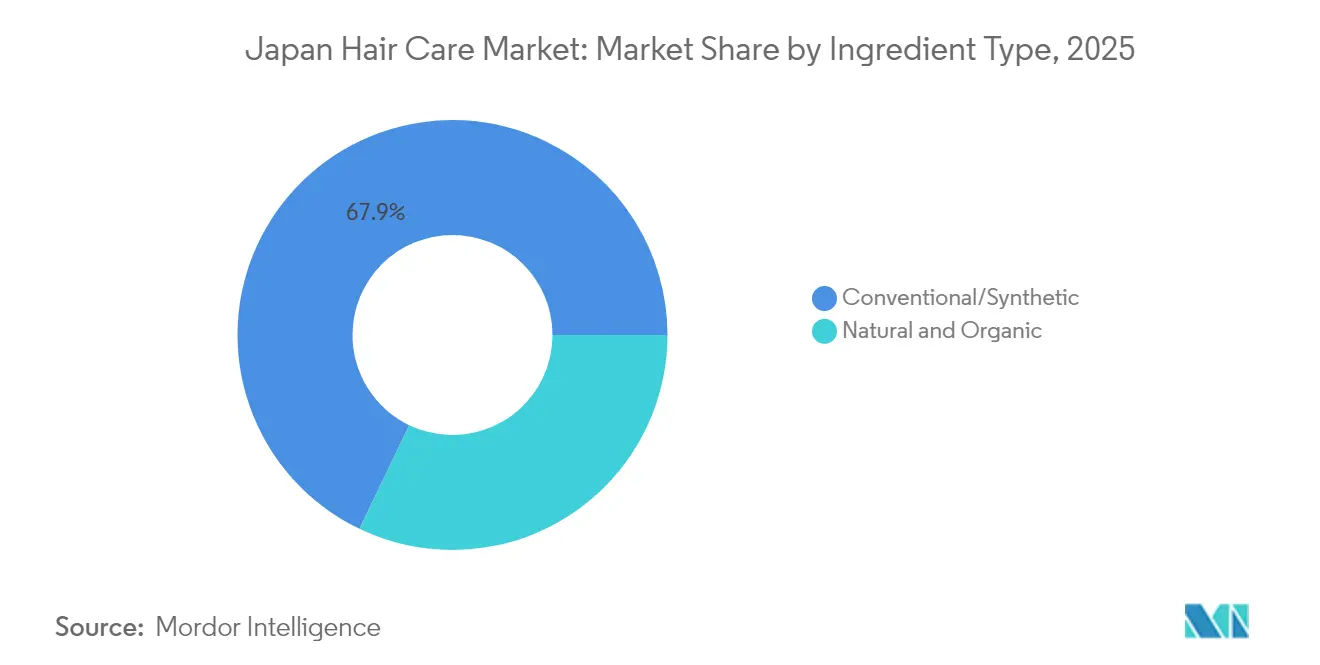

- By ingredient type, conventional formulations accounted for 67.88% of the Japan hair care market size in 2025, whereas natural and organic lines expanded the fastest at a 5.96% CAGR in 2026-2031.

- By distribution channel, specialty stores captured 49.05% of the Japanese hair care market size in 2025, yet online retail is the fastest-growing channel, rising at a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-population demand for anti-thinning and scalp-health solutions | +1.2% | National, with concentration in Tokyo, Osaka metropolitan areas | Long term (≥ 4 years) |

| Shift towards natural and organic products | +0.8% | National, with premium segments in urban centers | Medium term (2-4 years) |

| Technological innovations in product formulations | +0.7% | National, led by Tokyo research and development centers | Medium term (2-4 years) |

| Demand for multi-functional and damage control product | +0.6% | National, particularly in humid regions | Short term (≤ 2 years) |

| Male grooming culture expanding rapidly | +0.5% | Urban centers, expanding to suburban areas | Medium term (2-4 years) |

| Premiumization trend with high-end product offering | +0.4% | Tokyo, Osaka, Nagoya premium retail districts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging-Population Demand for Anti-Thinning and Scalp-Health Solutions

Japan's aging population is transforming the market, creating a growing need for specialized hair care solutions. According to the World Health Organization article published in October 2024, 30% of the population is already over 60 years old [1]Source: World Health Organization, “Ageing and health,” who.int. Research highlights that thinning hair is a significant concern for individuals in their 30s and 40s, with 65% of women in these age groups expressing this issue. In line with this, companies are stepping up with tailored innovations to address these needs. For example, Nakano Seiyaku's LADULLA brand focuses on women aged 50-70 who experience reduced hair volume, using Bond-Fix Complex technology to strengthen hair structure. This demographic shift is driving consistent market growth, supported by the increasing number of older consumers with stable disposable incomes. The focus is no longer just on basic hair care but on overall scalp health. Companies like Kracie are leading the way by developing advanced ingredients, such as Glyceryl Glutamido Glycine Na, to improve internal hair cross-link density and combat the effects of aging on hair.

Shift Towards Natural and Organic Products

Consumers in Japan are increasingly drawn to natural and organic hair care products, reflecting their growing concern about the safety of chemical ingredients and a renewed appreciation for traditional Japanese beauty practices. Ingredients like camellia oil, or tsubaki, are gaining popularity for their ability to deeply moisturize, reduce frizz, and enhance shine. Supporting this shift, Japan's Ministry of Health, Labour and Welfare (MHLW) has banned synthetic ingredients such as hydroquinone and formaldehyde, encouraging manufacturers to innovate with plant-based alternatives and natural preservatives. Companies are responding by offering premium products that align with these preferences. For example, Doshisha's Biorica Botanical series features non-silicone hair oils and shampoos infused with botanical extracts, catering to value-conscious consumers who seek effective, natural solutions.

Technological Innovations in Product Formulations

Japan's hair care industry is harnessing advanced technology to craft unique products that not only command premium prices but also fuel market expansion. A prime example is Kao Corporation's "THE ANSWER" brand, which, leveraging its proprietary lamella platform technology, has boosted moisture retention and shine, leading to sales surpassing 1 million units in just 7 months. Thanks to its digital transformation efforts, Kao has ramped up its product development speed by six times, allowing for swift innovation that aligns with changing consumer preferences. Mandom showcases the industry's technical prowess with its Gatsby Metarubber Bubble Perm Style Creator, a blend of wax and foam that mimics perm-like hairstyles sans chemicals, a feat lauded by the Society of Cosmetic Chemists Japan. Furthermore, the push towards AI and personalized technologies is evident in collaborations like that of Rakuten and L'Oréal Japan, which harness data from Rakuten's vast ecosystem of over 100 million members to deliver tailored beauty solutions.

Demand for Multi-Functional and Damage Control Product

Japan's humid climate and fast-paced lifestyle fuel a growing demand for multi-functional hair care products. Research indicates that over 60% of Japanese women grapple with hair issues during the rainy season, notably frizz and flatness, thanks to the humidity. This has spurred a demand for specialized formulations tailored to counteract these environmental challenges. In response, companies are rolling out innovative solutions. For instance, Lion Corporation's MEGAMIS brand has unveiled a novel three-step hair care regimen [2]Source: Lion Corporation, “MEGAMIS Launch News Release,” lion.co.jp. This routine incorporates a hair serum, applied between shampooing and treatment, ensuring deep penetration of beauty serum ingredients into the hair structure. Furthermore, brands are adopting a multi-functional strategy, crafting products that offer heat and UV protection while retaining moisture. This holistic approach caters to the discerning Japanese consumer, who values both efficiency and effectiveness in their beauty regimen.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over chemical ingredients | -0.6% | National, with heightened awareness in urban areas | Medium term (2-4 years) |

| Adoption of traditional at-home hair care solutions | -0.4% | Rural areas, traditional households | Long term (≥ 4 years) |

| High regulatory standards and ingredient restrictions | -0.3% | National, affecting all manufacturers | Long term (≥ 4 years) |

| Complex distribution system with traditional retail dominance | -0.2% | National, with regional variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health Concerns Over Chemical Ingredients

In Japan, growing consumer awareness about the safety of chemical ingredients is creating challenges for traditional hair care products. This is particularly evident as Japan's Ministry of Health, Labour and Welfare (MHLW) enforces stricter standards compared to many global markets [3]Source: Ministry of Health Labour and Welfare, “Standards for Cosmetics 2024,” mhlw.go.jp. The MHLW has banned certain ingredients, such as hydroquinone, chlorphenesin, and several coal tar dyes, due to concerns over toxicity and potential cancer risks. As a result, manufacturers are under pressure to reformulate their products and find safer alternatives. While these regulations prioritize consumer safety, they also drive up development costs and delay the launch of new products. Companies must navigate complex approval processes and conduct extensive safety testing, which adds to the burden. At the same time, Japanese consumers are becoming more selective, carefully examining ingredient lists and favoring products with natural, recognizable components. To meet these expectations, companies are investing in plant-based preservatives and other natural alternatives. However, these ingredients often come with higher costs and require new formulation approaches, impacting profit margins and pricing strategies.

Complex Distribution System with Traditional Retail Dominance

Japan's distribution system is dominated by specialty stores, creating barriers for new market entrants and restricting pricing flexibility. The traditional retail structure involves multiple intermediaries and established relationships that make market entry difficult, especially for smaller companies with limited resources. While e-commerce continues to grow rapidly, the shift from traditional channels remains slow, as many consumers prefer in-store consultation and product testing. International brands face additional challenges when entering the Japanese market, as they must navigate established distributor networks and build relationships with specialty retailers who typically favor domestic suppliers. The prevalence of traditional retail also affects the adoption rate of new products, as specialty stores often take a conservative approach to product selection and require thorough education about new technologies or ingredients before allocation of shelf space.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoo Dominance Amid Styling Innovation

Japanese consumers rely heavily on shampoo products, which account for 35.02% of the hair care market in 2025. This significant market share reflects how deeply embedded shampoo is in daily hair care routines across Japan. The hair styling segment is experiencing notable momentum, with a projected growth rate of 4.58% CAGR through 2031. This growth is particularly evident in products like Mandom's Gatsby Metarubber Bubble Perm Style Creator, which offers consumers chemical-free styling alternatives.

The Japanese hair care market demonstrates distinct consumer preferences across different segments. Conditioner sales remain robust as consumers adapt to the challenges posed by Japan's humid climate. The hair colorant segment is expanding steadily, primarily due to two key consumer groups: older consumers seeking gray coverage solutions and younger buyers exploring diverse color trends. This market structure highlights how Japanese consumers balance traditional hair care needs with modern innovation, creating opportunities for companies that effectively address both aspects.

By Category: Mass Market Foundation with Premium Acceleration

Japanese consumers continue to favor mass hair care products, which account for 74.93% of the market share in 2025. This preference stems from the practical need for reliable, everyday hair care solutions at accessible price points. However, the premium segment is experiencing notable growth at 5.41% CAGR through 2031, driven by an aging population that has both the means and the desire to invest in advanced hair care solutions.

The market's evolution is visible through strategic product launches and positioning. Nakano Seiyaku's LADULLA brand has successfully connected with women aged 50-70 by offering specialized Bond-Fix Complex technology at premium price points. Similarly, established players like Shiseido adapt to market demands through their Tsubaki line, which spans both premium and standard offerings. This dual-market approach reflects Japan's economic landscape, where urban consumers increasingly gravitate toward premium products, while rural markets maintain their preference for mass market solutions.

By Ingredient Type: Natural Transition Accelerates

Conventional/synthetic ingredients dominate the hair care market with a 67.88% share in 2025. These traditional formulations remain the preferred choice among consumers due to their proven effectiveness and competitive pricing in addressing fundamental hair care requirements.

The natural and organic ingredients segment is experiencing significant momentum, with a projected growth rate of 5.96% CAGR through 2031. This growth stems from increasing consumer focus on chemical safety and the incorporation of traditional Japanese ingredients like camellia oil and yuzu extract. Product innovations such as Utena's Yuzu Oil series demonstrate this market evolution, while manufacturers are developing hybrid formulations that combine natural ingredients with synthetic active compounds to deliver enhanced safety and performance at premium price points.

By Distribution Channel: Specialty Stores Lead Digital Transformation

Japanese consumers continue to rely heavily on specialty stores for their hair care needs, with these retailers commanding 49.05% of the distribution market in 2025. These stores have built their success on offering carefully selected product ranges and providing expert guidance to customers seeking personalized hair care solutions. The trust and relationships built between specialty store staff and customers remain a key factor in maintaining this dominant market position.

The digital transformation of Japan's retail landscape is driving substantial growth in online sales channels, which are advancing at a 7.12% CAGR through 2031. This shift reflects changing consumer preferences, with many Japanese shoppers now turning to social media and digital platforms for product research and purchases. Hair care companies have recognized this trend and are actively strengthening their digital presence through social media engagement and YouTube content. In response to this evolution, specialty retailers are developing comprehensive omnichannel strategies, effectively bridging the gap between traditional in-store experiences and digital convenience to protect and expand their market share.

Geography Analysis

The Japanese hair care market exhibits distinct consumer behavior patterns, with national brands maintaining a strong foothold while regional preferences shape product adoption. The Tokyo metropolitan area, home to a significant high-income consumer base, continues to drive premium product adoption. Similarly, the Osaka and Nagoya metropolitan areas demonstrate robust consumption patterns, where established brands like Kao and Shiseido dominate the market. While rural consumers traditionally favor mass-market products, this distinction is gradually diminishing as e-commerce accessibility improves and the aging population creates uniform demand for specialized products.

Regional climate conditions significantly influence consumer purchasing decisions across Japan. In coastal regions where humidity levels are high, consumers actively seek anti-frizz and humidity-resistant products to address their specific hair care needs. Conversely, inland regions show a stronger preference for moisturizing formulations due to drier environmental conditions. The Kansai region stands out for its consumer affinity towards traditional Japanese ingredients, such as camellia oil and rice water, which companies like Shiseido have successfully incorporated into their Tsubaki brand offerings.

Urban markets, with Tokyo at the forefront, remain the primary testing ground for premium product innovations. This strategic approach is exemplified by Kao's successful launch of "THE ANSWER" brand, which initially targeted metropolitan consumers before implementing a nationwide expansion strategy.

Regulatory Landscape

Japan hair care products are regulated under the Act on Securing Quality, Efficacy and Safety of Products Including Pharmaceuticals and Medical Devices (PMD Act), administered by the Ministry of Health, Labour and Welfare (MHLW), with the Pharmaceuticals and Medical Devices Agency (PMDA) supporting reviews where applicable. In practice, many everyday hair care items (such as shampoos and conditioners) are handled as cosmetics, while certain products with functional claims or actives (including many hair coloring agents and hair growth-related items) fall under the quasi-drug category, shaping both compliance scope and time-to-market.

Cosmetics generally follow a notification and standards-compliance pathway rather than pre-market approval. The MHLW Standards for Cosmetics define ingredient controls, including permitted preservatives, tar colors, and other restricted substances. Quasi-drugs require PMDA-related application and approval processes tied to efficacy, safety, and active-ingredient specifications, and advertising and claims are closely controlled to prevent cosmetics from implying medical effects. Companies entering or expanding in Japan typically operate through a Japanese license holder for manufacturing and marketing, and ongoing formulation maintenance is required as MHLW issues periodic administrative updates to standards and notifications.

Competitive Landscape

The Japanese hair care market is concentrated and demonstrates remarkable balance in revenue distribution nationwide, supported by comprehensive media coverage, deeply rooted beauty standards, and sophisticated logistics networks. While Tokyo maintains its position as the spending leader with early premium product adoption, major urban centers like Osaka and Nagoya exhibit comparable consumer behaviors with slightly lower transaction values. The traditional urban-rural divide in brand preferences continues to diminish as e-commerce platforms democratize product access and the aging population drives uniform demand for specialized solutions like anti-thinning products.

Local weather conditions significantly shape consumer purchasing decisions across Japan's diverse geography. Consumers in humid coastal regions invest heavily in anti-frizz and humidity-control products, while those in drier inland areas show strong preference for moisture-retention treatments. The Kansai region's distinct affinity for camellia-oil formulations has prompted Shiseido to emphasize Tsubaki shampoo lines in their regional marketing strategy. Major retailers actively manage their inventory mix by prefecture, particularly increasing stocks of chlorine-neutralizing products in areas where water mineral content poses specific hair care challenges.

The concentration of specialty beauty stores directly influences regional spending behaviors. Tokyo's central districts benefit from an extensive network of professional beauty advisers who provide personalized guidance on premium products, facilitating faster adoption of innovative formulations such as lamella-platform cleansers. In contrast, rural consumers increasingly depend on digital resources, including online tutorials and virtual consultation services integrated into retail platforms, to make informed purchase decisions.

Japan Hair Care Industry Leaders

L’Oréal S.A.

Shiseido Co., Ltd.

Mandom Corporation

Unilever PLC

Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Premium scalp-health and damage-care positioning continues to create whitespace for differentiated product architectures, particularly where brands can justify higher prices through repair or comfort benefits and ingredient transparency. The market already shows traction for technology-led propositions in Japan, such as lamella-platform shampoos from Kao and chemical-free styling formats from Mandom, enabling brands to tier assortments across mass and premium without depending on shampoo volume alone.

Two execution-led opportunities stand out in channels and supply chain. First, salon-linked engagement and personalization tools can drive repeat purchase through education and recommendation, with Milbon developing digital platforms such as milbon:iD and Smart Salon to connect professional inputs with direct-to-consumer routines. Second, manufacturing and private-brand or contract production capacity is being reinforced for core wash categories, with Miyoshi Yushi announcing construction of a new manufacturing plant to produce Kracie-brand shampoo and body soap, with operations slated for Spring 2027. At an industry level, the METI Cosmetics Industry Competitiveness Strengthening Study Group (5th meeting held in March 2026) also provides a policy forum that can support cross-company initiatives around competitiveness, innovation, and internationalization for Japanese beauty categories, including hair care.

Recent Industry Developments

- July 2026: Shiseido Professional announced the GLACEE COLLECTION for its ULTIST by PRIMIENCE salon hair color brand in Japan, with an August 6, 2026 launch date. The announcement reinforces salon-channel innovation in hair colorants and supports premium service-driven regimens that bundle color with maintenance care.

- January 2026: Mandom Corporation announced Lucido-L Oil-in-Hair Milk under the Argan Rich Oil series, launching on February 23, 2026, featuring natural argan oil and botanical keratin. The launch targets damage-care and smoothing needs in everyday routines, reinforcing Mandom's position in functional leave-in formats beyond core cleansing.

- November 2025: Miyoshi Yushi announced construction of a new manufacturing plant to produce Kracie-brand shampoo and body soap, with operations slated for Spring 2027. This investment signals ongoing domestic fulfillment expansion and potential for faster line extensions and retailer-exclusive programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as retail sales value of hair care products sold in Japan, covering everyday cleansing, conditioning, coloring, styling, and hair and scalp treatment items across online and offline channels.

Scope exclusions: Professional salon services, in-salon chemical treatments billed as services, and hair tools like dryers and irons are excluded from the market value.

Segmentation Overview

- By Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Other Product Types

- By Category

- Premium Products

- Mass Products

- By Ingredient Type

- Natural and Organic

- Conventional/Synthetic

- By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set market boundaries, align category definitions, and build initial input ranges for demand and pricing. The consumer and safety context is taken from Japan's Ministry of Health, Labour and Welfare, industrial and retail indicators are taken from the Ministry of Economy, Trade and Industry, and trade signals come from Japan Customs tariff and trade statistics for selected ingredients and finished goods.

To keep the inputs practical, we also review filings and investor presentations of large personal care companies active in Japan, trade association publications, and patents and patent applications to track formulation and claims trends. Credible press coverage is used to cross-check price moves and channel shifts between drugstores, specialty retail, and online. Where needed, paid subscriptions for company financials and business intelligence, and a patent database, are used to confirm timelines and normalize company reporting formats. These desk sources are illustrative and not exhaustive, and many additional references are reviewed to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work is used to stress test the desk model and close gaps on what is counted as hair care in Japan, how premium and mass lines are priced, and how channel mix is shifting between drugstores, specialty retail, and online. We speak with stakeholders such as brand and category managers, distributors and retailers, ingredient and packaging suppliers, and industry consultants, and then we compare the insights across Japan's major demand centers.

These conversations help us confirm which trends are already affecting sales, such as scalp care claims, anti-thinning focus, and natural and organic positioning, and which assumptions need to be kept conservative in the forecast.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | |

| Mid tier: 59% | Functional/Unit leaders: 40% | |

| Smaller Players: 15% | Managers: 48% |

Market-Sizing & Forecasting

The sizing is built using a top-down approach where Japan-level category totals are reconstructed from consumer goods spending signals, channel mix indicators, and hair care category splits, followed by checks against product-group shares. To keep the totals realistic, the output is corroborated with selective bottom-up approximations, such as sampled price points by product type multiplied by implied volumes, and supplier and channel checks that flag overstated growth.

Inputs that matter in this market include premium versus mass mix, the shift toward natural and organic claims, online retail share changes, product-type momentum (shampoo, conditioner, colorants, styling, and treatments), and price progression patterns driven by pack-size changes and promotional intensity. For forecasting, we use scenario analysis supported by simple time-series smoothing so that near-term channel shifts do not inflate long-range growth, and assumptions are re-tuned based on what industry respondents see in launches and shelf resets. Where bottom-up signals are incomplete for smaller subcategories, gaps are handled through conservative share allocation tied to observed shelf presence and channel concentration.

Data Validation & Update Cycle

Estimates are validated through triangulation across desk indicators, primary feedback, and internal consistency checks, so the final number aligns with realistic pricing and channel behavior. Variance checks are run at product-type and channel level, and any unusual jumps are reviewed again before sign-off, including a re-check of currency timing and base-year alignment.

The report is refreshed annually, and interim updates are triggered when material events occur, such as major pricing rounds, regulatory changes affecting claims, or step changes in online penetration. Before delivery, a final analyst pass is completed so the latest public signals and primary feedback are reflected in the model outputs.

Mordor Intelligence's Japan Hair Care Market Market Size Versus Other Published Estimates

Published market sizes for Japan hair care often do not match because firms draw the market boundary differently and they also use different ways to project pricing and channel shifts. Differences show up quickly when one estimate is strictly retail products, while another also folds in adjacent items that sit near hair care on store shelves.

The table shows a spread that is mainly explained by scope and what gets counted as hair care, and then by how price increases are carried forward in the forecast years. In Mordor Intelligence's model, the sizing stays within hair care product sales in Japan across shampoo, conditioner, colorants, styling, and treatments, and it excludes salon services and hair tools, which can pull other estimates higher or lower depending on what they include.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.15 B (2025) | |

| Industry Report Publisher A | USD 5.00 B (2025) | Uses a broader basket that explicitly includes hair growth items and salon channel sales as a distribution line, which can shift the counted value away from pure retail hair care products and can compress the 2025 total depending on channel allocation. |

| Research Publisher B | USD 2.55 B (2025) | Appears to apply a narrower product and channel scope, with a limited set of channels and category splits, which can undercount specialty retail and online sales and reduce the total market value for the same year. |

Taken together, the comparison points to scope and channel coverage as the biggest drivers of the gap, followed by how pricing is normalized across pack sizes and promotions. By keeping the counting rules tied to clear product types, channel mapping, and practical pricing checks, the estimate remains traceable to inputs that can be reviewed and repeated year to year.

Key Questions Answered in the Report

What is the current size of the Japan hair care market and how fast is it growing?

The Japan hair care market is estimated at USD 5.36 billion in 2026 and expands at a 4.16% CAGR through 2031.

Which product type holds the largest share?

Shampoo commands 35.02% of 2025 sales and remains the backbone of household routines.

Where is the fastest growth occurring within distribution?

Online retail grows at a 7.12% CAGR as consumers embrace virtual advisers and same-day shipping.

Why are natural ingredients gaining traction?

MHLW bans on select synthetics push brands to adopt camellia, yuzu, and other botanicals, fueling a 5.96% CAGR in the natural segment.

How are aging demographics influencing product innovation?

Brands focus on anti-thinning and scalp-health lines that use bond-fix technologies and peptide complexes to meet older consumers’ concerns.

Page last updated on: