Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

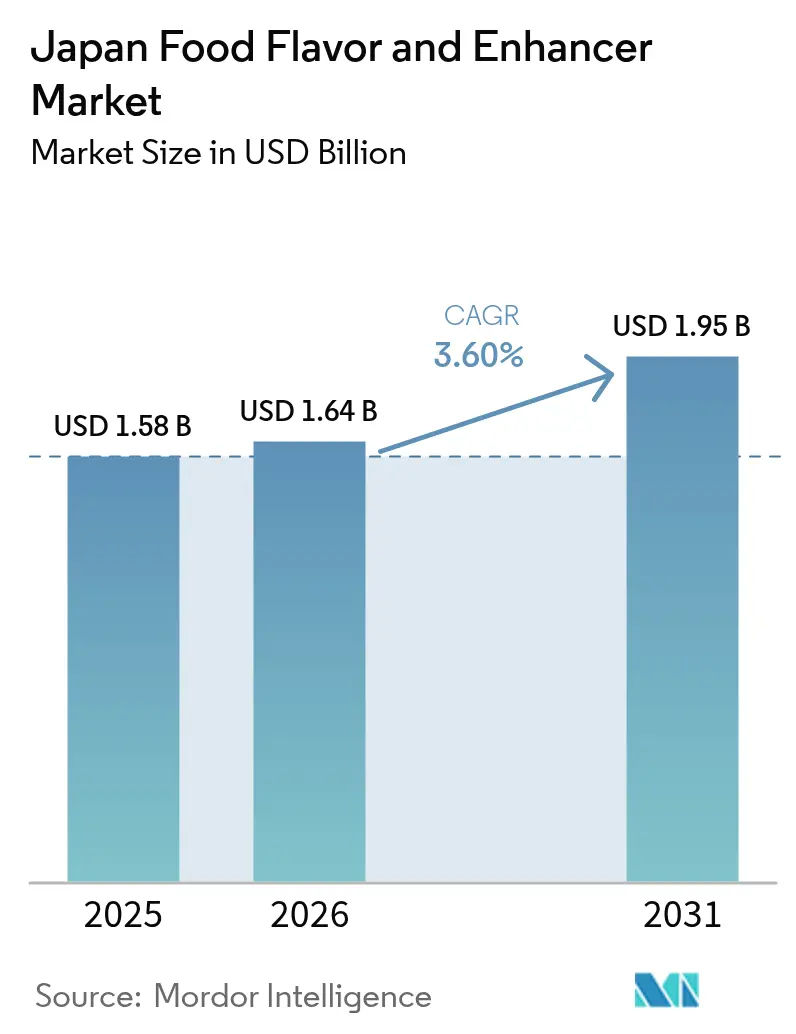

| Base Year Market Size (2025) | USD 1.58 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 1.95 Billion |

| Growth Rate (2026 - 2031) | 3.60% CAGR |

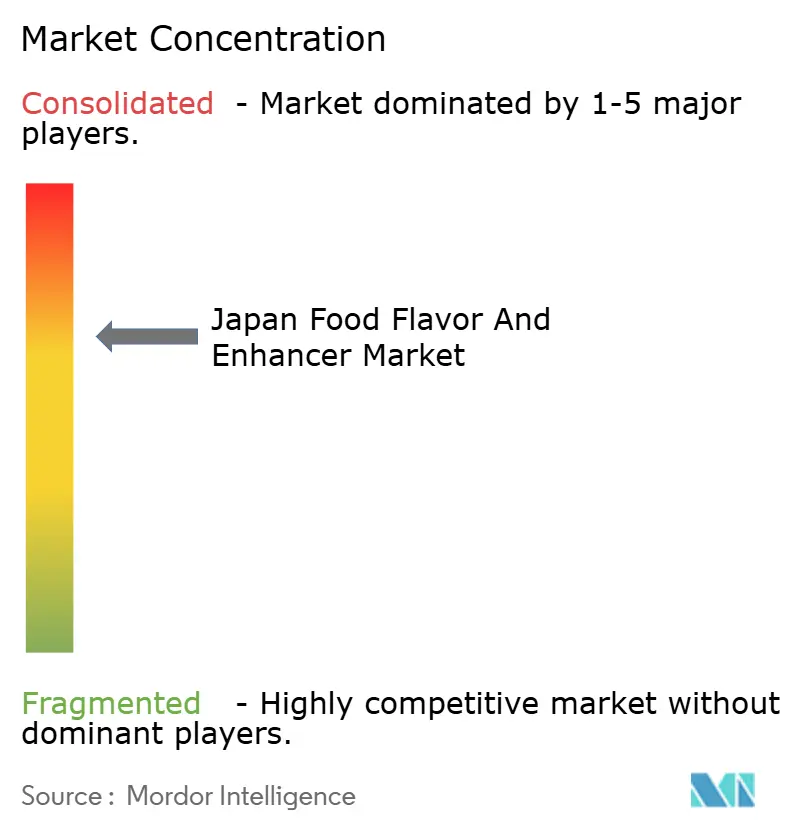

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Food Flavors And Enhancers Market Analysis by Mordor Intelligence

The Japan Food Flavors And Enhancers Market size is expected to grow from USD 1.58 billion in 2025 to USD 1.64 billion in 2026 and is forecast to reach USD 1.95 billion by 2031 at 3.60% CAGR over 2026-2031. This growth is driven by the domestic food-processing industry's transition from volume-based production to a focus on premiumization, clean-label reformulation, and biotech-enabled taste modulation. Regulatory developments are favoring the adoption of biotech-derived ingredients. For instance, Japan's Ministry of Health, Labour and Welfare has expedited safety assessments for kokumi peptides produced through precision fermentation, allowing companies like Ajinomoto and Kyowa Hakko Bio to commercialize compounds that enhance mouthfeel and savory flavors with lower dosages compared to traditional enhancers. Additionally, in 2024, the Consumer Affairs Agency implemented stricter labeling standards, requiring clear differentiation between nature-identical and synthetic origins. This regulatory change has accelerated reformulation efforts and increased demand for traceable botanical extracts.

Key Report Takeaways

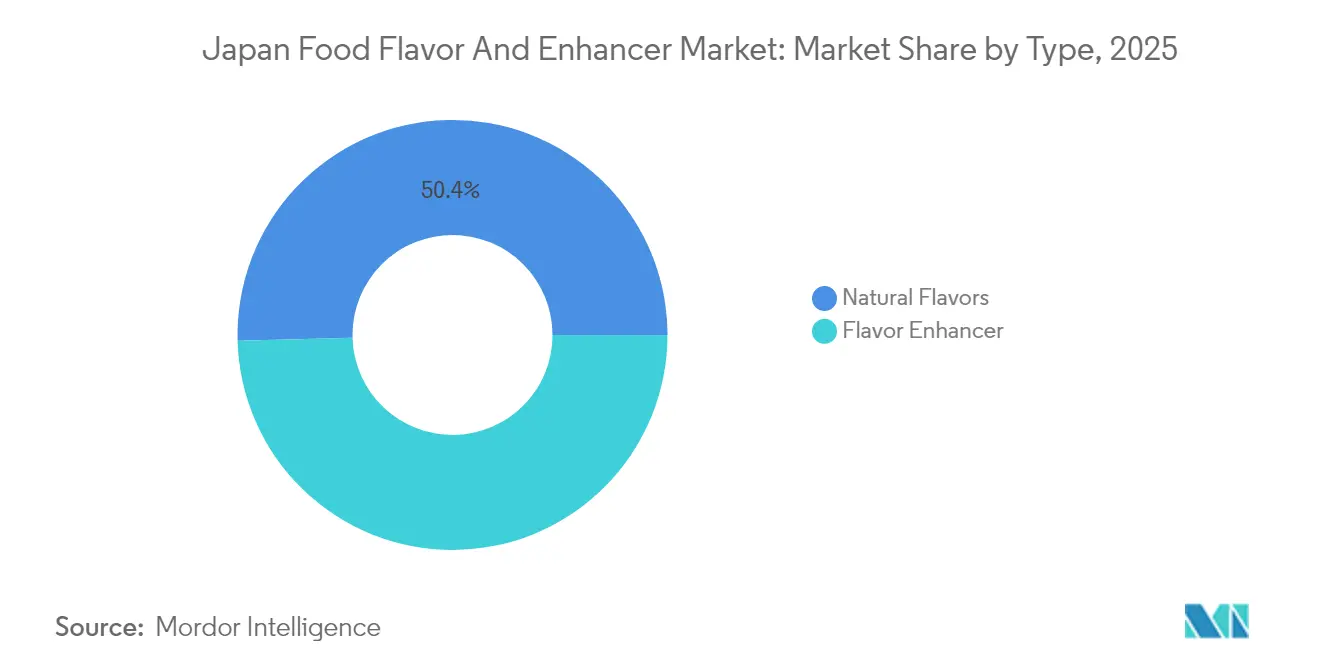

- By type, natural flavors led the Japan Food Flavors And Enhancers Market with a 50.42% share in 2025. The flavor enhancer segment is forecast to post the fastest 5.62% CAGR through 2031.

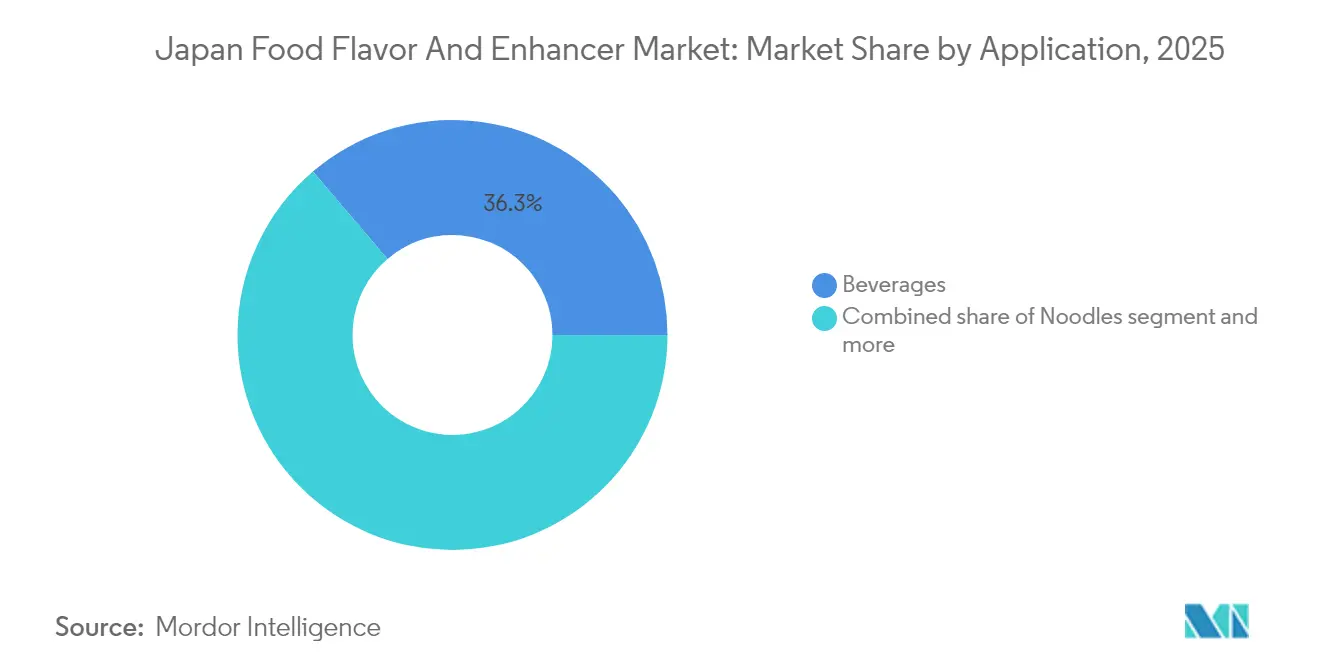

- By application, beverages accounted for 36.25% of the Japan Food Flavors And Enhancers Market size in 2025. The noodles segment is projected to advance at a 6.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Food Flavors And Enhancers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of processed and convenience foods | +0.8% | National, concentrated in Tokyo, Osaka, Nagoya metro areas | Medium term (2-4 years) |

| Rising demand for clean-label natural flavorings | +0.7% | National, with premium adoption in urban centers | Long term (≥ 4 years) |

| Pivot towards plant-based flavor enhancer ingredients | +0.5% | National, early traction in foodservice and retail ready-meals | Medium term (2-4 years) |

| Regulatory fast-track for biotech-derived kokumi peptides | +0.4% | National, led by MHLW approvals | Short term (≤ 2 years) |

| Technological advancements and innovation in flavor formulation | +0.6% | National, research and development hubs in Kanagawa and Osaka prefectures | Long term (≥ 4 years) |

| Expansion of multinational flavor houses in local manufacturing | +0.5% | National, FDI clusters in Ibaraki and Shizuoka | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of processed and convenience foods

The growth of Japan's processed-food and convenience-food industry is a key driver of the country's food flavor and enhancer market. As per the Ministry of Economy, Trade and Industry, in 2024, the processed-food sector recorded shipments worth JPY 20.5 trillion (approximately USD 140 billion), driven by increasing demand for single-serve, ready-to-eat, and microwaveable products. These formats require advanced, thermally stable flavor systems to counteract aroma loss and preserve the depth of umami. Major convenience-store chains, including Seven-Eleven Japan, FamilyMart, and Lawson, collectively updated approximately 70% of their prepared-food SKUs in 2024. Each new product iteration required customized flavor solutions that emphasize clean-label attributes, sodium reduction, and consistent sensory quality after reheating. The rising popularity of premium convenience meals, functional and fortified ready meals, and plant-based bento options has further heightened the demand for advanced flavor enhancers capable of masking off-notes, stabilizing taste, and delivering authentic regional flavors.

Rising demand for clean-label natural flavorings

The Consumer Affairs Agency's labeling reforms, implemented in April 2024, require that any flavor compound synthesized through chemical processes, despite being molecularly identical to a natural precursor, be labeled as "nature identical" [1]Source: Consumer Affairs Agency, Government of Japan, "About functional foods," caa.go.jp. In contrast, extracts derived exclusively from botanical, animal, or microbial sources are designated as "natural." This distinction has driven increased demand for steam-distilled essential oils, cold-pressed citrus extracts, and enzyme-modified dairy flavors. Takasago International and Robertet Group maintain significant supply agreements with growers in Southeast Asia and Madagascar for these segments [2]Source: Takasago, takasago.com. According to retail audits conducted by the Japan Processed Food Wholesalers Association, products labeled with "natural flavor" claims achieved a 12% to 18% price premium over their nature-identical counterparts in yogurt, snack, and beverage categories in 2024. This price differential has encouraged reformulation efforts despite the associated higher input costs.

Pivot towards plant-based flavor enhancer ingredients

The growing preference for plant-based flavor-enhancer ingredients is driving significant growth in Japan's food flavor and enhancer market. This trend is driven by growing health awareness, rising demand for clean-label products, and a cultural preference for naturally derived umami sources. Japanese consumers are paying closer attention to additives, prompting manufacturers to replace synthetic enhancers with alternatives such as yeast extracts, fermented mushroom concentrates, kelp or seaweed derivatives, koji-based modulators, and plant-derived nucleotides. These ingredients provide depth of flavor without the association with chemical additives. This shift aligns with broader dietary trends, including reduced sodium consumption, flexitarian diets, and an interest in fermentation-rich foods, where plant-based enhancers address both flavor and wellness considerations. The rising availability of plant-forward meal options, ranging from convenience-store bentos to frozen entrées, further drives demand for natural savory ingredients that replicate the mouthfeel and umami of animal-based broths. Collectively, these factors establish the transition to plant-based flavor-enhancer ingredients as a significant and long-term growth driver in Japan's food flavor and flavor-enhancer market.

Regulatory fast-track for biotech-derived kokumi peptides

The Japan's food flavor and enhancer market demonstrates significant potential for innovation through the use of biotech-derived ingredients, particularly kokumi peptides, which enhance taste complexity and improve mouthfeel. Regulatory precedents for biotech-derived flavor compounds, such as recombinant valencene, suggest that Japan’s Consumer Affairs Agency (CAA) offers pathways for novel additives, provided they are supported by comprehensive safety and purity data. A regulatory fast-track for kokumi peptides could facilitate their adoption, enabling manufacturers to introduce sustainable, high-quality, and consistent flavor enhancers that meet the market’s increasing demand for clean-label and naturally derived taste solutions. To achieve success, companies must focus on high-purity production, transparent manufacturing processes, and clear communication of benefits, including sustainability and consistent flavor enhancement. This alignment of regulatory compliance and strategic market positioning could enable biotech-derived kokumi peptides to gain a competitive advantage in Japan’s evolving flavor enhancer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply volatility in key natural raw materials | -0.6% | National, acute for importers of vanilla, citrus, tropical botanicals | Short term (≤ 2 years) |

| Health concerns over MSG and sodium-based enhancers | -0.4% | National, strongest among urban millennials and Gen Z | Medium term (2-4 years) |

| High development costs for "functional" or clean-label/natural flavor systems | -0.5% | National, disproportionate burden on SME processors | Long term (≥ 4 years) |

| Consumer skepticism or health concerns around artificial flavors | -0.3% | National, amplified by social-media wellness influencers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply volatility in key natural raw materials

Supply volatility in essential natural raw materials, such as vanilla, cocoa, coffee, and specialty fruits, poses a significant challenge for Japan's food flavor and flavor enhancer market. These ingredients are often sourced from geographically limited regions and are highly susceptible to seasonal variations, climate disruptions, and socio-economic instability in producing countries. For instance, vanilla production in Madagascar, cocoa in West Africa, and specialty fruit extracts from tropical regions frequently experience unpredictable yields, resulting in price fluctuations and supply shortages. Such disruptions create difficulties for flavor houses and food manufacturers in Japan, where maintaining consistency, adhering to high-quality standards, and ensuring traceability are crucial for regulatory compliance and consumer trust. Although synthetic or biotech-derived alternatives present potential solutions, they may face regulatory challenges, involve higher research and development costs, or lack appeal in clean-label products. Consequently, supply instability in key natural raw materials drives manufacturers to implement diversified sourcing strategies, optimize inventory management, and innovate in alternative or stable flavor technologies to mitigate risks and support growth in Japan's flavor enhancer market.

Health concerns over MSG and sodium-based enhancers

Health concerns regarding sodium and MSG are increasingly influencing consumer preferences, posing challenges for traditional flavor enhancers in Japan. Although regulatory authorities have not imposed restrictions, Japan’s Food Safety Commission reaffirmed MSG’s acceptable daily intake as “not specified” in its 2024 risk assessment, consistent with WHO and FDA guidelines. Consumer demand is shifting toward lower-sodium and MSG-free products. This trend reflects a broader generational shift seen globally. For instance, Nissin Foods Holdings reformulated its Cup Noodles brand by reducing sodium, removing added MSG, and eliminating artificial flavors [3]Source: Nissin Foods, nissin.com/jp. These developments indicate that, despite the absence of regulatory limits, manufacturers are under pressure to reformulate products to meet the expectations of health-conscious consumers. However, these alternatives often entail higher costs, regulatory approvals, or modifications to the supply chain, creating challenges for the widespread adoption of conventional sodium-based enhancers in Japan's evolving market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Biotech and Clean-Label Pressures Reshape Flavor Portfolios

The natural flavor segment accounted for 50.42% of revenue in 2025, driven by labeling reforms and retailer mandates emphasizing traceable botanical inputs. Retailers such as Aeon and Ito-Yokado have mandated the use of natural flavors in private-label confections and ready meals, prompting suppliers like Takasago and Robertet to expand their sourcing networks in Southeast Asia. Nature-identical flavors occupy a middle ground, offering cost advantages but facing consumer skepticism. These flavors remain prevalent in budget carbonated beverages and processed snacks. Synthetic flavors, on the other hand, have been largely relegated to industrial bakery products and low-margin confectionery, where cost considerations outweigh clean-label preferences.

The flavor enhancer segment represents the fastest-growing category, with a projected CAGR of 5.62% through 2031. Processors are increasingly adopting yeast extracts, kokumi peptides, and nucleotide blends to deliver flavor depth without relying on MSG. Ajinomoto’s precision-fermented kokumi peptide has achieved full-year inclusion in dairy desserts and savory snacks, showcasing how biotech innovations can support premium product positioning. While development costs remain high, shorter regulatory timelines and R&D tax incentives are reducing barriers for agile start-ups. Assuming a stable supply of botanical oils and protein substrates, natural and biotech-derived solutions are expected to continue gaining market share from synthetic alternatives.

By Application: Beverage Volume Dominates, Noodles Fuel Incremental Growth

Beverages accounted for a 36.25% share of the Japan flavors and flavor enhancers market in 2025, driven by companies like Suntory and Asahi introducing 47 new ready-to-drink coffee and functional-tea SKUs. Flavor houses provided modular citrus, berry, floral, and roasted concentrates, enabling beverage formulators to reduce time-to-market from 14 weeks to 6 weeks. Noodles are projected to grow at a CAGR of 6.08% through 2031, marking the fastest growth in the market. This growth is fueled by premium instant-ramen lines featuring regional broth profiles and plant-based enhancers. Bakery and confectionery volumes stabilized as premium chocolate and artisan bread regained shelf space, necessitating higher flavor loadings per unit.

Savory snacks leveraged regional Japanese flavors. In 2024, Calbee launched several regional and limited-edition flavors, such as the Hokkaido Butter Soy Sauce variant under its “Dream Tag” series and the Kyushu-style Yuzu Pepper flavor in its Kataage Potato range. Soups and sauces remained mature but stable, with reformulation efforts focusing on sodium reduction supported by kokumi peptides. Other applications, including pet food and nutraceuticals, continued to be niche but exhibited high single-digit growth as producers sought solutions for enhancing the palatability of functional ingredients. Overall, innovation in beverages and noodles represents the market’s most consistent growth drivers.

Geography Analysis

Urban areas drive the Japan food flavor and flavor enhancer market, with Tokyo, Osaka, and Nagoya accounting for approximately 55% of processed food consumption. These metropolitan regions host a significant number of convenience stores and premium supermarkets, which prioritize the launch of clean-label and functional products. In contrast, rural prefectures face challenges such as population decline, which leads to consolidation among regional processors and limits growth opportunities for mid-tier flavor suppliers. However, smaller cities in regions like Kyushu and Hokkaido serve as testing grounds for regional flavor profiles, which can later be scaled nationally.

The Consumer Affairs Agency enforces origin transparency for flavor declarations, driving reformulation efforts toward the use of natural extracts. Trade policies are also favorable, with the Regional Comprehensive Economic Partnership enabling tariff-free imports of ASEAN botanicals. This reduces input costs for citrus and spice extracts, supporting the market's shift toward natural ingredients. Regulatory oversight remains centralized under the Ministry of Health, Labour and Welfare. The ministry streamlined biotech ingredient approvals, exemplified by granting kokumi peptides GRAS (Generally Recognized as Safe) status in February 2024. This provides domestic manufacturers with a competitive advantage over European Union counterparts by accelerating product development timelines.

Investment patterns reflect these structural advantages. For instance, Kerry Group’s fermentation plant in Ibaraki and Givaudan’s expansion in Odawara highlight the strategic importance of proximity to Japanese processors and research and development hubs. Domestic companies, such as Takasago and T. Hasegawa, are expanding biotech capacities to maintain market share against multinational competitors. Overall, regulatory clarity, advanced consumer preferences, and the geographic concentration of food manufacturing contribute to a stable yet innovation-driven market environment.

Competitive Landscape

The Japanese food flavor and enhancer market exhibits moderate concentration, with key global players such as Givaudan SA, DSM-Firmenich, International Flavors & Fragrances Inc., Archer Daniels Midland Company, and Kerry Group PLC, alongside domestic leaders like Takasago International Corporation and Ajinomoto Co. Inc. Companies are prioritizing product innovation, focusing on the development of natural flavor enhancers and clean-label flavors, while utilizing artificial intelligence for flavor development and customization.

Strategic efforts are concentrated on three areas: biotech-derived taste modulators, plant-based enhancers, and modular toolkits designed to shorten customer development cycles. Although economies of scale in fermentation and intellectual property create barriers to entry, opportunities remain in plant-based seafood and cultured-meat flavor systems, where proprietary blends are not yet fully established by incumbents.

Integration across the value chain serves as a competitive advantage. For instance, Ajinomoto benefits from in-house fermentation platforms and long-term procurement contracts for amino-acid substrates, ensuring cost efficiency and quality control. Similarly, Givaudan utilizes its global citrus-processing network to maintain a stable supply of high-quality oils while addressing climate-related risks. Overall, sustained investment in research and development, along with strategic partnerships, will continue to shape the competitive landscape of the market.

Japan Food Flavors And Enhancers Industry Leaders

-

Takasago International Corporation

-

International Flavors and Fragrances Inc.

-

Symrise AG

-

Ajinomoto Inc

-

Givaudan SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: T. Hasegawa introduced PLANTREACT, a proprietary flavor technology designed to replicate the savory taste of animal proteins and dairy in plant-based foods. By utilizing advanced reaction-flavor techniques, including Maillard reactions, enzymolysis, and fermentation/biotransformation, PLANTREACT develops natural, clean-label, and heat-stable flavor profiles. This innovation addresses one of the primary challenges in plant-based proteins, improving taste.

- April 2025: Takasago launched a dedicated website for its Vivid Flavors Retroma brand, a flavor technology platform designed to recreate the "retronasal aroma" experience. This technology enables the reintroduction or mimicry of aromas lost during processing, allowing food manufacturers to deliver rich, natural flavor experiences in processed or reformulated foods.

- March 2025: Mitsubishi Corporation and ADM signed a non-binding Memorandum of Understanding (MOU) to explore strategic collaboration across the global agriculture and food supply chain. The partnership focuses on crop sourcing, supply chain efficiency, and distribution. Stable agricultural supply chains can support manufacturers of natural flavors, extracts, and fermentation-based ingredients in managing costs, reducing volatility, and scaling production.

Japan Food Flavors And Enhancers Market Report Scope

Food flavors and enhancers are used to improve the flavor of food and beverage products. The scope of the study includes applications such as bakery and confectionery products, dairy products, beverages, processed foods, and other food and beverage products.

The Japan Food Flavors And Enhancers Market is segmented by type into flavors and flavor enhancers. The flavors segment is sub-segmented into natural, synthetic, and nature-identical flavors. Based on the application, the market is segmented into bakery, confectionery, dairy, beverages, processed food, and other applications.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Type

| Flavors | Natural Flavors |

| Nature-Identical Flavors | |

| Synthetic Flavors | |

| Flavor Enhancers |

Application

| Bakery and Confectionery |

| Beverages |

| Dairy Products |

| Noodles |

| Soups and Sauces |

| Savory Snacks |

| Other Applications |

| By Type | Flavors | Natural Flavors |

| Nature-Identical Flavors | ||

| Synthetic Flavors | ||

| Flavor Enhancers | ||

| Application | Bakery and Confectionery | |

| Beverages | ||

| Dairy Products | ||

| Noodles | ||

| Soups and Sauces | ||

| Savory Snacks | ||

| Other Applications |

Key Questions Answered in the Report

How big is the Japan Food Flavors And Enhancers Market?

The Japan Food Flavors And Enhancers Market size is expected to reach USD 1.64 billion in 2026 and grow at a CAGR of 3.60% to reach USD 1.95 billion by 2031.

Which segment is growing fastest within Japan Food Flavors And Enhancers Market?

Noodles are advancing 6.08% CAGR to 2031 as manufacturers introduce premium regional broths supported by yeast extracts and shiitake-derived enhancers.

Who are the key players in Japan Food Flavors And Enhancers Market?

Givaudan, Takasago International Corporation, International Flavors and Fragrances Inc., Symrise AG and Ajinomoto Inc are the major companies operating in the Japan Food Flavors And Enhancers Market.

How are flavor houses mitigating vanilla supply risk?

Firms are investing in synthetic-biology routes, such as yeast-derived vanillin, and diversifying sourcing while pursuing domestic cultivation grants for alternative aromatics.

Page last updated on: