Thermal Barrier Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.55 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermal Barrier Coatings Market Analysis by Mordor Intelligence

Thermal Barrier Coatings market size in 2026 is estimated at USD 1.26 billion, growing from 2025 value of USD 1.21 billion with 2031 projections showing USD 1.55 billion, growing at 4.19% CAGR over 2026-2031. Sustained demand stems from hotter‐running gas turbines, weight-sensitive aerospace engines, and new hypersonic platforms that all rely on advanced ceramic-metal stacks for reliable insulation. Greater fuel-efficiency targets in commercial aviation, the need to curb CO₂ from industrial power generation, and persistent investments in ultra-high temperature research programs underpin the upward curve of the thermal barrier coatings market. Competitive intensity is shaped by mid-sized fragmentation as legacy suppliers introduce smart-spray factories while newer entrants chase niche, low-volume applications. Meanwhile, supply chain resilience for yttria-stabilized zirconia and rare-earth stabilizers remains a strategic priority after a multi-year run of price volatility.

Key Report Takeaways

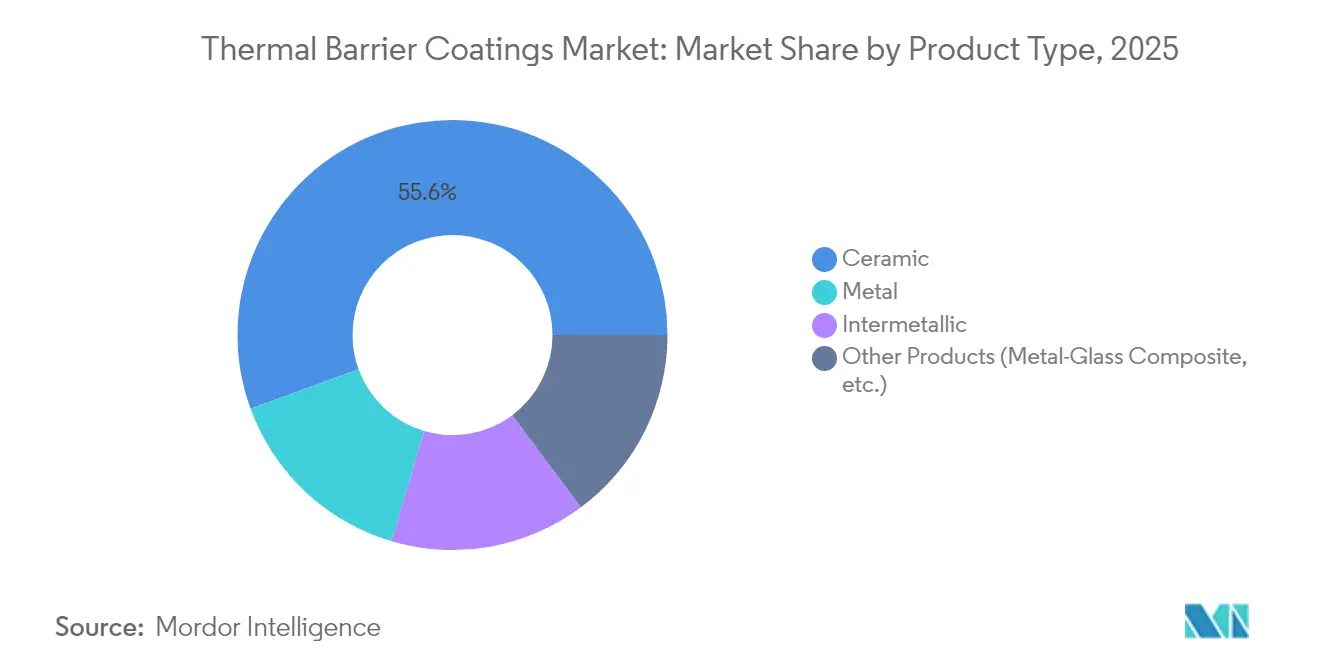

- By product type, ceramic top coats led with 55.58% of the thermal barrier coatings market share in 2025, while metal bond coats are projected to rise at a 5.74% CAGR through 2031.

- By coating technology, air plasma spray captured 41.20% revenue share in 2025; plasma spray-PVD is poised for the fastest growth at 5.33% CAGR to 2031.

- By coating material, yttria-stabilized zirconia accounted for 61.55% share of the thermal barrier coatings market size in 2025, whereas rare-earth zirconates show the strongest outlook at a 5.82% CAGR.

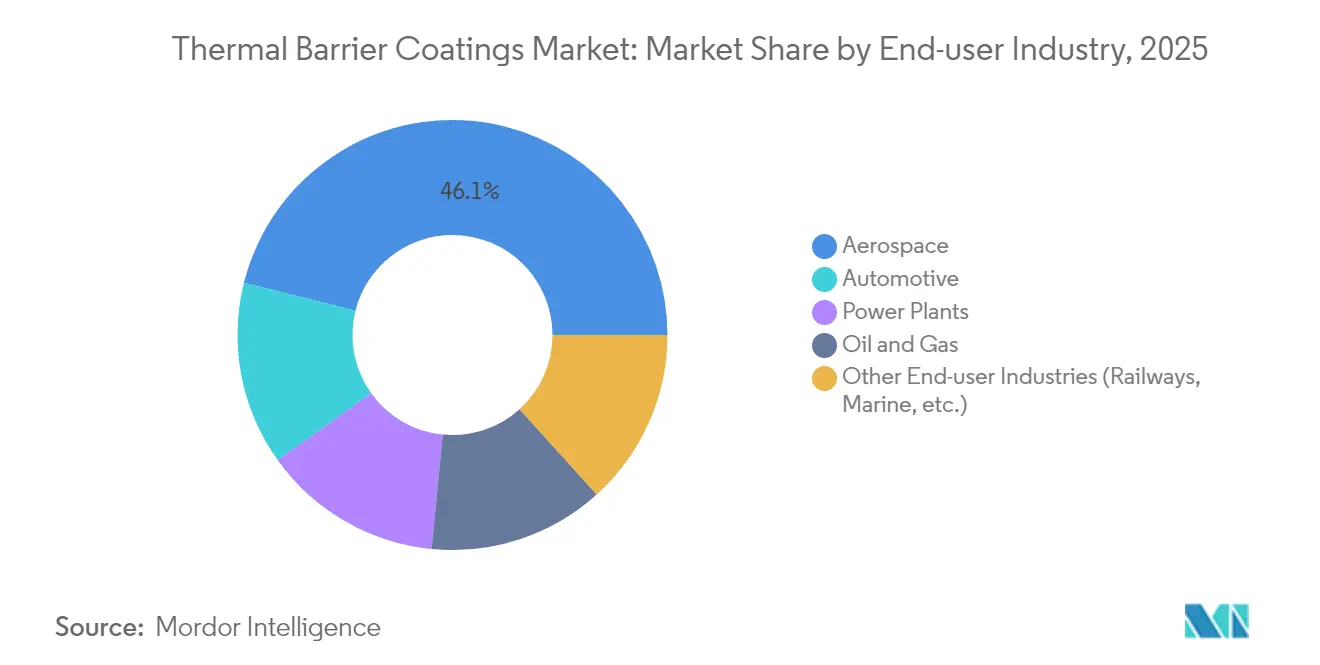

- By end-user industry, aerospace held 46.10% share in 2025 and the automotive segment is advancing at a 6.78% CAGR to 2031.

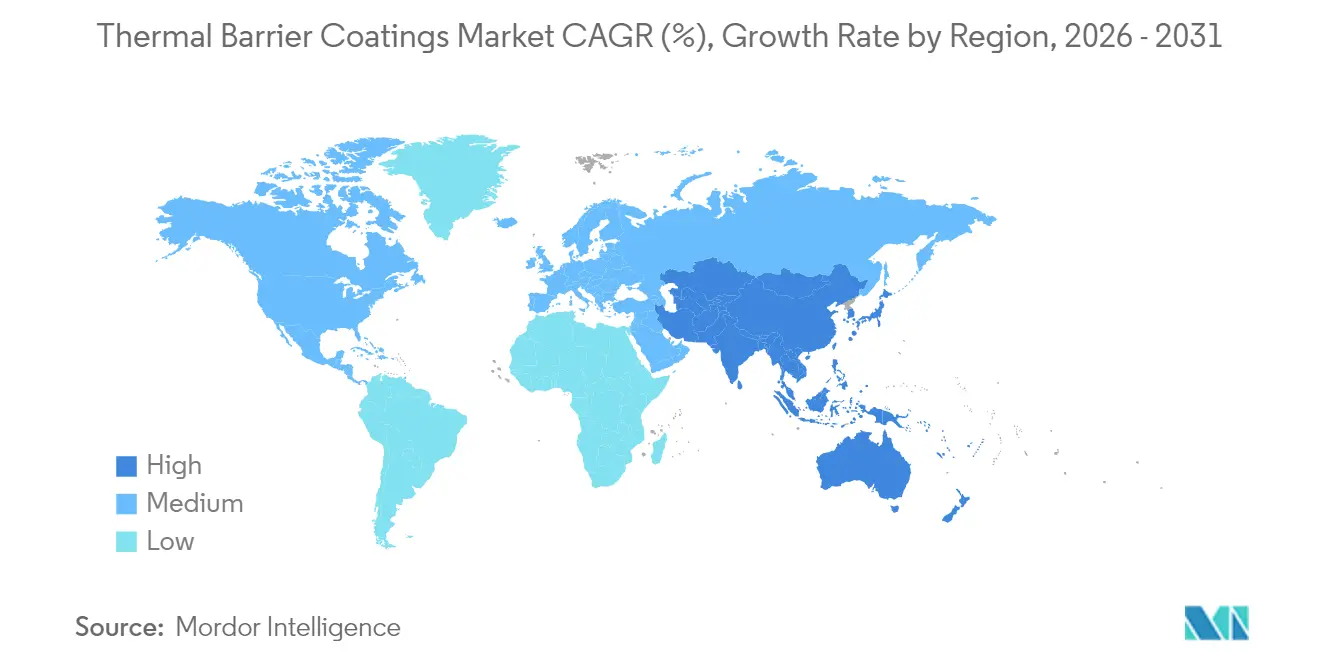

- By geography, Asia-Pacific owned 34.90% of the thermal barrier coatings market size in 2025; the region also leads growth momentum with a 4.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermal Barrier Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher aerospace engine temperatures | +1.2% | North America, Europe | Medium term (2-4 years) |

| Industrial gas-turbine build-out | +1.0% | Asia-Pacific, Middle East & Africa | Long term (≥ 4 years) |

| Automotive efficiency programs | +0.8% | Global, early Europe & North America | Short term (≤ 2 years) |

| Hypersonic vehicle R&D | +0.6% | North America, Europe | Long term (≥ 4 years) |

| Expansion in marine and defense fleets | +0.4% | Global naval powers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand from Aerospace Engines

Next-generation turbofan cores now burn near 1,650 °C, forcing turbine hot sections to adopt multi-layer ceramics that can survive intense thermal cycling. Rare-earth zirconates deliver lower lattice thermal conductivity than conventional 8YSZ, prompting new patents in double-layer architectures that keep metal temperatures below critical thresholds[1]Southwest Research Institute, “Advanced Thermal Barrier Coatings for High-Temperature Applications,” swri.org. GE Aerospace earmarked USD 1 billion in 2025 for ceramic matrix composites and allied coatings, signaling that fuel-neutral propulsion hinges on robust thermal management. Sustainable aviation fuels add complexity because new flame chemistries alter heat flux in combustors, raising the value of smart coatings with in-situ health sensors.

Rising Installation of Industrial Gas Turbines

Combined-cycle plants in China, India, and the Gulf are running at >1,500 °C to chase mid-fifties thermal efficiency, so inlet air cooling and hydrogen-capable combustors are sharpening the focus on strain-tolerant coatings. Every percentage point of turbine firing-temperature gain trims fuel cost, which propels the thermal barrier coatings market as utilities modernize fleets to stabilize grids dominated by renewables. Vendors now field functionally graded stacks that dampen thermal shock when ramping from idle to full load in under ten minutes.

Efficiency Push in High-Performance Automotive and Motorsport Engines

Motorsport laboratories have proved that thin ceramic linings cut piston crown heat rejection, enabling OEMs to downsize radiators without breaching NOx limits. Piston-ring TiSiCN nanocomposites also show lower friction, unlocking measurable fuel-economy gains in test cycles[2]Society of Tribologists and Lubrication Engineers, “Nanocomposite Coatings Reduce Engine Friction,” stle.org . As mainstream hybrids and battery-electric vehicles adopt higher-voltage power electronics, localized hot spots demand similar barrier solutions to safeguard silicon carbide inverters and extend battery life.

Hypersonic Vehicle Thermal-Protection R&D Programs

Mach-5 plus flight pushes leading-edge temperatures to 2,000 °C, a realm where hafnium carbide or zirconium diboride paint-like films are mandatory. The U.S. Air Force awarded Canopy Aerospace USD 2.8 million in 2024 to mature transpiration-cooled panels that bleed fluid through porous ceramics for active shielding. Optical-fiber networks embedded in the coat now relay real-time strain and heat-flux data, guiding design refinements for repeatable re-entry cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile zirconia and rare-earth costs | -0.8% | Global importers | Short term (≤ 2 years) |

| Stricter plasma-spray emission limits | -0.5% | Europe, North America, spreading in Asia | Medium term (2-4 years) |

| Emergence of alternate materials | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Zirconia and Rare-Earth Stabilizers

Global zircon sand output slipped by 28% during 2020 and has not fully recovered, exposing coat producers to price spikes that erode margin[3]U.S. Geological Survey, “Mineral Commodity Summary – Zirconium and Hafnium,” usgs.gov. Yttrium remains heavily concentrated in Chinese mines, where output reached only 45 t in 2022 against nameplate capacity of 1,500 t, maintaining geopolitical risk for the thermal barrier coatings market. Leading suppliers have turned to strategic stock builds and alternate dopants such as gadolinium to cap exposure.

Tightening HSE Norms on Plasma-Spray Shop Emissions and Dust

California’s Airborne Toxic Control Measure caps hexavalent chromium and nickel particle release, obliging coat shops to add sealed booths, multi-stage filtration, and personal monitoring to pass audits [4]California Air Resources Board, “ATCM for Thermal Spraying Operations,” arb.ca.gov. Under the UK COSHH framework, similar rules are rolling out across Europe, pushing small shops toward costly retrofits or outsourcing. These compliance burdens can stall adoption for smaller tier-two suppliers despite robust end-market demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ceramic Dominance Drives Innovation

Ceramic top coats contributed 55.58% to the thermal barrier coatings market in 2025, underscoring the unmatched thermal insulation offered by yttria-stabilized zirconia systems. The thermal barrier coatings market size for ceramic products is expected to keep expanding as aerospace primes qualify double-layer stacks that pair gadolinium zirconate with 8YSZ for better CMAS resistance.

Metal bond coats, while only a sub-layer, register the quickest growth at 5.74% CAGR, thanks to new MCrAlY chemistries that form uniform alumina scales and delay spallation. Intermetallic and graded coats are spreading in power-plant retrofit programs where component lives stretch beyond 25,000 h. High-entropy alloy coats remain a research subject but they promise phase stability across wider temperature bands.

By Coating Technology: Plasma Spray Evolution

Air plasma spray held 41.20% share in 2025, favoured for its wide material window and economical throughput across turbine vanes, shrouds, and combustor panels. Digital twin models now adjust torch current in real time to keep porosity within ±1%, supporting the quality-centric aerospace supply chain.

Plasma spray-PVD is climbing at a 5.33% CAGR because its low-pressure vapour plume deposits columnar microstructures that flex with thermal cycles. Electron-beam PVD stays the premium choice for single-crystal blades in wide-body engines, whereas HVOF dominates wear-resistant coatings in oil and gas valves. Solution precursor plasma spray and CVD occupy niches where dense, crack-free films are mandatory.

By Coating Material: Zirconia Leadership Under Pressure

Yttria-stabilized zirconia commanded 61.55% of the thermal barrier coatings market share in 2025 because it balances thermal conductivity, phase stability, and production cost. Continuous development seeks to slow its tetragonal-to-monoclinic transformation above 1,200 °C by adding alumina or silica scavengers.

Rare-earth zirconates are expanding at 5.82% CAGR as OEMs validate lanthanum and gadolinium systems for 1,400 °C turbine front stages. Alumina-rich mullite serves diesel turbochargers where sulphur attack is severe, while MCrAlY bond coats gain chrome levels to fight hot corrosion in high-sulphur fuels. High-entropy alloy formulations remain experimental but early coupons have survived 2,000 thermal cycles without delamination.

By End-User Industry: Aerospace Leadership with Automotive Momentum

The aerospace sector absorbed 46.10% of global demand in 2025, reinforcing the centrality of strict thrust-to-weight and fuel-burn targets. High-bypass engines on new wide-body aircraft rely on coatings to hit 60,000 h time on wing.

Automotive volumes are smaller yet clock the steadiest 6.78% CAGR, mainly through turbocharger hot-side housings and cylinder liners in downsized petrol engines. Battery-electric drivetrain makers now coat stator end-turns to insulate copper from hot inverter spray, opening a new adjacency beyond combustion engines. Power plant OEMs retain a baseline outlook as LM6000 and H-class units undergo life-extension overhaul every five years, keeping demand even in mature fleets.

Geography Analysis

Asia-Pacific held a 34.90% share of the thermal barrier coatings market in 2025 and is set to grow at 4.98% CAGR to 2031. The region gains from China’s 50-GW gas-turbine build-out program and Japan’s vertically integrated aero-engine supply chain that coats both domestic and export components. South Korea’s shipyards adopt ceramic stacks on dual-fuel LNG engines, and India’s private aerospace ecosystem adds independent spray shops dedicated to single-aisle jets.

North America benefits from its strong aerospace tier base, standing as the largest spender on hypersonic R&D. The U.S. Department of Energy funds ultra-high temperature research that explores yttrium-aluminium-garnet variants suited for 1,700 °C turbine inlet temperatures. Canada supports coatings for regional-jet programs in Montréal, while Mexico’s Bajío cluster coats turbo parts for global auto OEMs, feeding integrated supply chains.

Europe remains technology-rich despite lower installed capacity growth. Germany’s carmakers retrofit turbocharger lines with in-house spray booths to protect intellectual property. The UK and France channel Horizon Europe grants to phase-shifting ceramic research. Eastern Europe’s lower labour cost lures contract coaters, but compliance with REACH regulation obliges rapid investment in abatement systems. Emerging regions such as the Middle East leverage large gas-turbine aftermarket deals, whereas South America applies coatings on heavy-fuel power units to mitigate sulphidation.

Competitive Landscape

Market is moderately consolidated, with the top five companies generating about two-thirds of revenue. OC Oerlikon Management AG and Honeywell International Inc. leverage vertically integrated powder production, smart-spray factories, and data analytics to enhance engine on-wing time through IoT-enabled coating life models. Tier-two specialists focus on niches like hypersonic nose tips and Formula One exhaust manifolds, while universities license advanced formulations to start-ups exploring rare-earth zirconates and high-entropy alloys. Joint ventures, such as MTU Aero Engines and Oerlikon’s collaboration to improve torch parameters, are rising. Patent filings emphasize self-healing oxide dispersions and fibre sensors to detect delamination risks. Pricing depends on powder purity, spraying uptime, and meeting NADCAP or ISO standards. Regional content rules in defense contracts drive global players to establish local lines, while cost pressures from raw materials push leaders toward backward integration, particularly in zirconia refining, to maintain competitiveness.

Thermal Barrier Coatings Industry Leaders

Honeywell International Inc.

Saint-Gobain

OC Oerlikon Management AG

Linde Plc.

Bodycote

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: OC Oerlikon Management AG and MTU Aero Engines advanced their collaboration to develop a smart thermal spray factory, integrating digital processes to enhance aerospace component production with improved efficiency, quality, and transparency. The project includes system integration, data-driven anomaly detection, predictive maintenance, and process optimization through cross-functional teamwork.

- March 2023: Zircotec company launched a ceramic thermal barrier coating called Thermohold. This technology can be applied to various substrate materials, including metallic surfaces like cast iron, steel alloys, aluminum, and titanium, composite materials like carbon-fiber-reinforced polymers (CFRPs), and high-temperature plastics.

Global Thermal Barrier Coatings Market Report Scope

Thermal barrier coatings (TBCs) are high-tech materials that coat turbines or airplane engines to protect them from severe heat during high-temperature processes. Yttria-stabilized zirconia is a common oxide used as a TBC.

The thermal barrier coatings market is segmented by product, end-user industry, and geography. By product, the market is segmented into metal (bond coat), ceramic (top coat), intermetallic, and other products. The market is segmented into automotive, aerospace, power plants, oil and gas, and other end-user industries by end-user industry. The report also covers the market size and forecasts in 16 countries across major regions. Market sizing and forecasts for each segment are based on revenue (USD).

| Metal |

| Ceramic |

| Intermetallic |

| Other Products (Metal-Glass Composite, etc.) |

| Air Plasma Spray (APS) |

| High-Velocity Oxygen Fuel (HVOF) |

| Electron-Beam PVD (EB-PVD) |

| Chemical Vapor Deposition (CVD) |

| Plasma Spray-PVD (PS-PVD) |

| Solution Precursor Plasma Spray (SPPS) |

| Yttria-Stabilized Zirconia (8YSZ) |

| Rare-Earth Zirconates (GdZrO, LaZrO) |

| Alumina and Mullite |

| MCrAlY Bond Coats |

| High-Entropy Alloy Coats |

| Aerospace |

| Power Plants |

| Automotive |

| Oil and Gas |

| Other End-user Industries (Railways, Marine, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Metal | |

| Ceramic | ||

| Intermetallic | ||

| Other Products (Metal-Glass Composite, etc.) | ||

| By Coating Technology | Air Plasma Spray (APS) | |

| High-Velocity Oxygen Fuel (HVOF) | ||

| Electron-Beam PVD (EB-PVD) | ||

| Chemical Vapor Deposition (CVD) | ||

| Plasma Spray-PVD (PS-PVD) | ||

| Solution Precursor Plasma Spray (SPPS) | ||

| By Coating Material | Yttria-Stabilized Zirconia (8YSZ) | |

| Rare-Earth Zirconates (GdZrO, LaZrO) | ||

| Alumina and Mullite | ||

| MCrAlY Bond Coats | ||

| High-Entropy Alloy Coats | ||

| By End-user Industry | Aerospace | |

| Power Plants | ||

| Automotive | ||

| Oil and Gas | ||

| Other End-user Industries (Railways, Marine, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the thermal barrier coatings market by 2031?

The thermal barrier coatings market is forecast to reach USD 1.55 billion by 2031 based on current growth projections.

Which product category holds the largest share today?

Ceramic command 55.58% of 2025 revenue owing to their superior insulation properties.

Which region leads both size and growth?

Asia-Pacific accounts for 34.90% of global revenue and is expected to grow at a 4.98% CAGR through 2031, driven by gas-turbine build-outs and aerospace investment.

Which coating technology is growing the fastest?

Plasma spray-PVD shows the highest forecast CAGR at 5.33% because its columnar microstructures withstand thermal shock better than conventional methods.

How are regulations affecting coating producers?

Stricter emission limits in Europe and North America require costly ventilation and filtration upgrades, influencing production economics for plasma-spray shops.

Page last updated on: