Japan Faucets Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

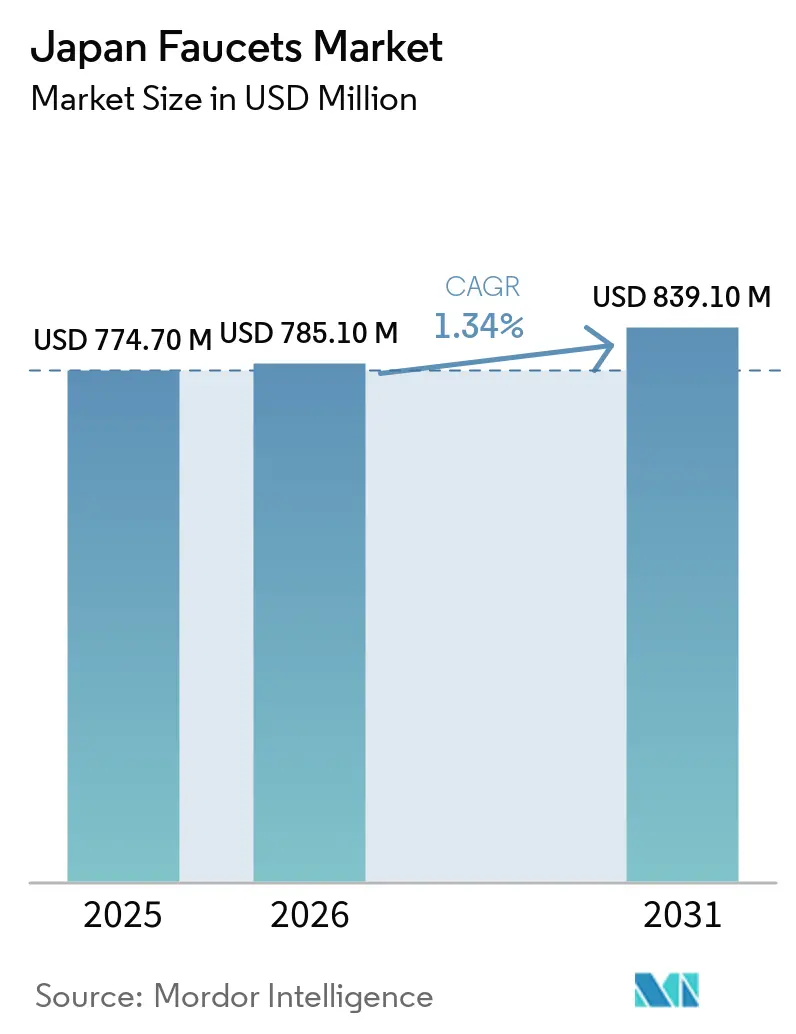

| Base Year Market Size (2025) | USD 774.70 Million |

| Market Size (2026) | USD 785.10 Million |

| Market Size (2031) | USD 839.10 Million |

| Growth Rate (2026 - 2031) | 1.34% CAGR |

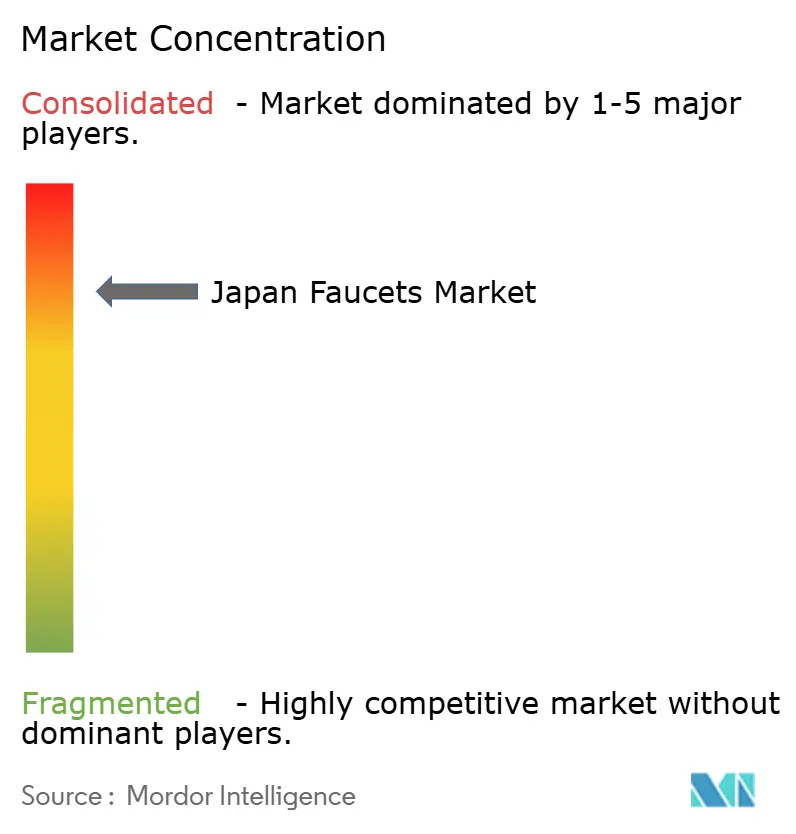

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Faucets Market Analysis by Mordor Intelligence

The Japanese faucets market size stood at USD 785.1 million in 2026, up from USD 774.7 million in 2025, and is projected to reach USD 839.1 million by 2031 at an 1.34% CAGR. Growth in the Japanese faucets market is supported by a steady renovation cycle and a shift toward touchless, water-saving designs in both residential and commercial settings. Cartridge-based mechanisms remain the core product foundation due to their reliability and maintenance advantages, while brass specifications are expanding in higher-duty applications that value corrosion control and alignment with compliance requirements. Energy- and water-efficiency labeling in company lineups is now a norm, as reflected in LIXIL’s water-and-energy-saving faucet sales ratio of 94.5% in the fiscal year ended March 2025, with a target of 100% by fiscal 2031[1]NSE.OR.JP https://www.nse.or.jp/listing/search/files/140120250620594754.pdf. The top five producers hold a strong combined position, which concentrates channel influence, helps standardize specifications, and supports national deployment for large-scale replacement programs in the Japanese faucets market.

Key Report Takeaways

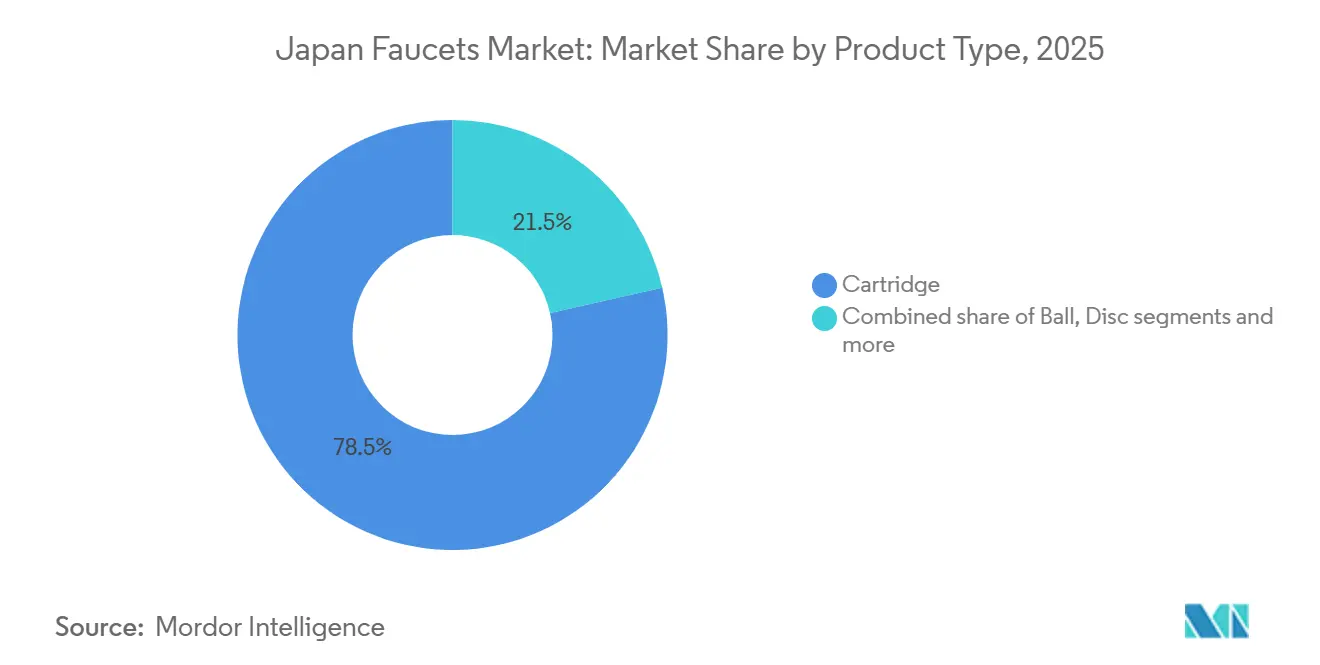

- By product type, cartridge-based mechanisms led with a 78.52% of the Japanese faucets market share in 2025, while compression mechanisms are the fastest-growing, advancing at a 2.97% CAGR through 2031.

- By material, chrome led with a 42.25% of the Japanese faucets market share in 2025, and brass is the fastest-growing material at a 4.03% CAGR through 2031.

- By technology, manual units held the largest 2025 share, and automatic faucets are the fastest-growing at a 3.43% CAGR through 2031.

- By installation type, deck-mount units led with a 71.15% of the Japanese faucets market share in 2025, while wall-mount units are the fastest-growing at a 4.30% CAGR through 2031.

- By application, bathroom sink faucets held a 68.51% of the Japanese faucets market share in 2025, while kitchen sink faucets are the fastest-growing at a 2.83% CAGR through 2031.

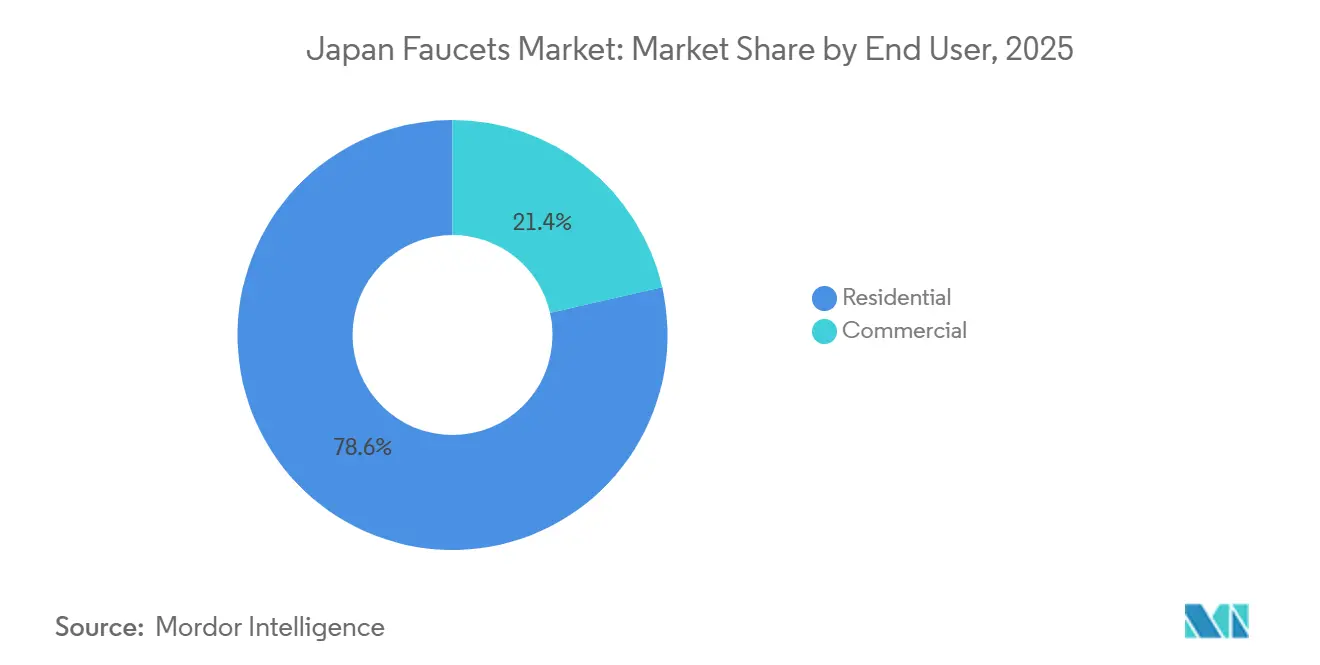

- By end-user, residential accounted for 78.56% of the Japanese faucets market share in 2025, and commercial installations are the fastest-growing at a 2.70% CAGR through 2031.

- By distribution channel, B2C/Retail captured a 74.48% of the Japanese faucets market share in 2025, while B2B/Project channels are the fastest-growing at a 2.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Faucets Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation-driven replacement cycles in aging housing stock | 0.6% | National, concentrated in Kanto, Kansai, and Chubu metropolitan rings | Medium term (2-4 years) |

| Hygiene-driven adoption of touchless/sensor faucets in commercial settings | 0.3% | Urban commercial hubs (Tokyo, Osaka, Nagoya) spilling to the regional | Short term (≤ 2 years) |

| Energy- and water-saving labeling/subsidies accelerating faucet upgrades | 0.2% | National, amplified in prefectures with local co-funding | Long term (≥ 4 years) |

| Tourism-led hotel and F&B refurbishments are sustaining commercial demand | 0.1% | Tourism corridors (Kanto, Kansai, Kyushu), resort zones | Medium term (2-4 years) |

| Aging population needs: universal design, thermostatic/anti-scald, lever ease | 0.1% | National, early gains in aged-heavy prefectures (Akita, Shimane) | Long term (≥ 4 years) |

| Digital/online B2C enablement expanding long-tail replacement SKUs | 0.04% | National, accelerated in metro e-commerce penetration zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renovation-Driven Replacement Cycles in Aging Housing Stock

Replacement-led demand is the core engine of the Japanese faucets market and reflects the aging profile of the national dwelling stock. LIXIL disclosed steady domestic water-technology growth in fiscal 2025 despite softer new-housing activity, underscoring how large dealer networks and showroom engagement convert latent replacement intent into orders. The rollout of product lines pre-configured with water- and energy-saving features also lowers decision friction during renovations and helps standardize specifications for installers. Showroom-led journeys, remote consult formats, and bundle-ready bathroom suites align with homeowner expectations for turnkey refreshes in kitchens and bathrooms. This pattern is accretive to mix because accessory upgrades often accompany faucet replacements, which lifts average transaction values in the Japanese faucets market.

Hygiene-Driven Adoption of Touchless or Sensor Faucets in Commercial Settings

Touchless operation has moved from a niche choice to a default specification for many public and institutional facilities, and that change is now visible in the commercial replacement mix. TOTO’s bathroom systems increasingly integrate electrolyzed-water features that target mold and bacteria suppression, and these systems pair naturally with sensor-activated faucets to reduce contact points. LIXIL’s portfolio has also emphasized hands-free operation across core lavatory ranges, allowing building owners to standardize on recognized domestic brands and service networks[2]NEWSROOM.LIXIL.COM https://newsroom.lixil.com/20250404_impact_briefing. As office retrofits, schools, hospitals, and hospitality assets update their restrooms, facility managers are prioritizing reduced-contact fixtures that support cleanliness and throughput without adding new maintenance complexity. The cumulative effect is a visible pivot toward sensor faucets across high-traffic facilities, which supports sustained growth in the Japanese faucets market even as new builds soften.

Energy- and Water-Saving Labeling and Subsidies Accelerating Faucet Upgrades

The integration of energy- and water-saving features at the product-design stage is shifting upgrade economics in favor of modernized faucet lines. LIXIL reported that 94.5% of domestic faucet sales carried water- and energy-saving attributes in fiscal 2025 and set a path to reach 100% by fiscal 2031, which signals a full portfolio conversion across mainstream price bands. TOTO’s disclosures show avoided-water metrics trending higher as water-saving designs scale across fixtures, and those metrics align with broader retrofit goals that value resource efficiency. JWPA’s standards and the Japan market’s certification pathways provide manufacturers with clear reference points for flow control, safety, and quality, making it easier for buyers to compare options on consistent criteria. Specialty components such as high-efficiency nozzles have also advanced, including pulsating-flow technologies commercialized through large-format retail partners, which increases visibility and adoption. Together, these factors reinforce replacement intent and compress payback expectations, which support volume and value momentum in the Japan faucets market over the forecast window.

Tourism-Led Hotel and Food-Service Refurbishments Sustaining Commercial Demand

Hotel and food-service refurbishments are replenishing the commercial pipeline after prior deferrals, and bathroom experiences are now a differentiator in guest satisfaction metrics. LIXIL’s international water-technology operations emphasize premium faucets and showers in hospitality, and this discipline informs domestic project specifications for color finishes, touchless operation, and thermostatic control. Property owners are moving to standardize fixture families across portfolios to simplify maintenance and spares, boosting tender sizes and creating ripple effects for distributors. In parallel, restaurant chains and transport hubs are adopting touchless faucets to align with cleanliness protocols and improve user throughput. These factors combine to support a steady commercial-refresh cadence that underpins the Japan faucets market outlook through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining new housing starts are dampening first-install demand | -0.5% | National, the steepest drop in outlying prefectures beyond core metros | Medium term (2-4 years) |

| Installer/labor shortages are creating project backlogs and higher install costs | -0.3% | National, acute in rural aging communities | Short term (≤ 2 years) |

| Compliance/certification timelines (JIS/JWWA, environmental labels) extend time-to-market | -0.1% | National delays are concentrated in small/medium manufacturers | Medium term (2-4 years) |

| Legacy plumbing interfaces in older buildings raise retrofit complexity | -0.06% | Kanto, Kansai pre-1981 building stock | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining New Housing Starts Dampening First-Install Demand

A downshift in new housing construction removes first-install faucet placements and presses more weight onto the renovation channel. TOTO’s Japan Housing Equipment Business indicated pressure on faucet-related revenue in the first half of fiscal 2025, consistent with lighter new-build pipelines during that period. Distributor and installer feedback points to a mix pivot toward replacements rather than greenfield installations, which alters order profiles and puts a premium on retrofit-friendly designs. This context reinforces the role of showrooms and dealer consultations in helping homeowners select standardized, compliant models that minimize downtime. The Japanese faucets market adapts to this reality by leaning into bundled bathroom upgrades and lifecycle-cost narratives that fit the economic profile of remodels.

Installer and Labor Shortages Creating Project Backlogs and Higher Install Costs

Skilled installer availability remains tight in many prefectures, which raises the total cost of ownership for replacement projects. Project sequencing must account for limited contractor slots and regulatory overtime limits, thereby encouraging building owners and households to consolidate multiple fixture changes into a single visit. Manufacturers are responding with easier-to-fit assemblies and cleaner wiring integration for sensor faucets to reduce labor hours and callbacks. Well-known brands that provide robust service coverage and documentation also gain an advantage, as installers favor lines with predictable fitment and readily available spares. The near-term effect is slower project throughput and higher per-job costs, which can defer discretionary upgrades and temper near-term volume in the Japan faucets market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cartridge Supremacy Anchored in Field-Proven Ceramic-Disc Engineering

Cartridge faucets held the lead with 78.52% in 2025, reflecting long-standing installer preference for single-lever operation and quick cartridge swaps that reduce downtime in tight residential spaces. The compression segment is expanding from a smaller base at a 2.97% CAGR, where heritage aesthetics or restoration projects mandate cross-handle sets and specific visual cues that align with period design. Ball and disc subtypes remain niche in Japan due to their complex components and alignment with specialized institutional or laboratory environments. Ongoing innovation is visible in automatic faucet integration within familiar cartridge bodies, which supports touchless adoption without revising rough-in assumptions or adding bulk at the sink. Taken together, these characteristics sustain cartridge leadership and a favorable maintenance profile, reinforcing buyer confidence in the Japanese faucets market.

Cartridge share depth is reinforced by standardized parts logistics across national distributors, which keeps spares accessible and supports fast-cycle service calls. Product development that embeds thermostatic control within cartridge stacks has also gained traction in care settings where anti-scald performance is a procurement requirement. The Japan faucets market share leadership for cartridge-based mechanisms in 2025 reflects an installed base advantage that reinforces itself through installer familiarity and homeowner trust. As brands refresh core lines, familiarity with lever feel, valve travel, and temperature stability complements hygiene-focused variants to maintain segment durability. This creates continuity for homeowners who want upgraded features without retraining on new controls, which further anchors cartridge primacy.

By Material: Chrome Retains the Visual Baseline as Brass Gains on Durability and Compliance

Chrome accounted for 42.25% of the 2025 mix, supported by a polished aesthetic, established consumer expectations, and favorable price points in mid-market bathrooms and commercial washrooms. Brass is the fastest-rising material, with a 4.03% CAGR, because facility owners and premium residential buyers value its corrosion resistance and compliance with water-contact standards that guide municipal procurement and sensitive environments. Association specifications have tightened around water-contact safety, and those frameworks encourage buyers to choose known brass formulations from established producers. Major brands continue to invest in corrosion control and dezincification resistance in high-exposure settings, which helps brass maintain a performance edge in coastal or high-humidity areas. Stainless steel and engineered plastics fill defined niches where antimicrobial properties or weight and handling profiles trump other criteria, but they remain secondary in terms of national market share.

Purchasing teams have become more sensitive to lifecycle durability, and that favors brass in applications where frequent use or cleaning chemicals impose cumulative stress. Companies are documenting material provenance and testing in integrated reports and product literature, which helps buyers validate choices against internal standards. This transparency aligns with procurement policies in facilities that manage vulnerable populations, such as elderly care, hospitals, and schools, and it accelerates acceptance of brass assemblies in those channels. Given these tailwinds, brass retains its growth advantage while chrome remains the default visual baseline in the Japanese faucets industry. Together, both materials define the core of mainstream choice sets while higher-spec alternatives address niche environments.

By Technology: Manual Dominance Yields Share to Sensor-Equipped Designs

Manual faucets continued to lead unit volumes in 2025 due to familiarity, lower upfront cost, and the large installed base of lever-operated residential sinks. Automatic faucets are growing at a 3.43% CAGR as public-facility standards and institutional preference for reduced-contact fixtures drive broader adoption. LIXIL’s 2026 portfolio updates integrate automatic faucets with concealed wiring and upgraded counters, a design focus that eases installation and clarifies value for residential remodels. TOTO’s integrated bathroom systems also reflect hygiene-forward features, and these systems often bundle well with sensor faucets for cohesive user experiences. This shift indicates that touchless capability is becoming a baseline expectation in high-traffic environments and a rising consideration in homes within the Japanese faucets market.

Consumer hesitations around maintenance and power supply have eased as product generations have improved battery life, concealed wiring, and error-proof fitment. In parallel, facility operators see operational benefits from consistent water temperature and controlled flow, which pair naturally with touchless activation. The Japanese faucets market size for automatic faucets is projected to expand at a 3.43% CAGR as public and commercial standards normalize around contact reduction and resource efficiency. Manual designs will remain entrenched in value tiers and rental properties, but specification momentum favors automatic in new institutional projects and in higher-spec remodels. This balance supports a gradual mix shift rather than a disruptive pivot, which stabilizes channel inventories and installer routines.

By Installation Type: Deck-Mount Pragmatism Versus Wall-Mount Space Efficiency

Deck-mount faucets led with a 71.15% share in 2025, supported by standardized vanity tops and factory-drilled dimensions used across modular bathroom systems. Wall-mount installations are growing at a 4.30% CAGR due to space-saving goals, universal-design compliance around knee clearance, and a preference for easy-to-clean surfaces without base seals. Manufacturers have aligned product families with both approaches, enabling designers to maintain visual consistency while meeting layout constraints. In institutional bathrooms, wall-mount shower and lavatory faucets also facilitate accessibility outcomes and simplify sanitation. This dual-track structure allows the Japanese faucets market to service both mainstream replacements and modernized layouts that emphasize floor clearance.

Deck-mount’s fitment speed and parts familiarity protect its share, especially in high-volume residential replacements where labor availability is tight. Renovation-focused product refreshes that package sinks and storage with compatible faucet rough-ins further simplify deck-mount choices. Wall-mount growth accelerates in compact apartments and in premium remodels, where the visual impact of floating sinks and clear counters is a selling point. As installers gain confidence with rough-in kits and distributors stock compatible spares, barriers to wall-mount adoption continue to ease. That steady improvement keeps the installation mix dynamic without displacing the practical advantages of deck-mount in the Japanese faucets industry.

By Application Type: Bathroom Sinks Anchor Volume as Kitchens Pull Up Value

Bathroom sink faucets held a 68.51% share in 2025, reflecting multiple lavatory points per dwelling and institutional adoption of touchless lavatory fixtures in high-traffic washrooms. Kitchen sink faucets are expanding at a 2.83% CAGR as pull-out sprays, filtered-water variants, and premium finishes gain adoption in remodels. New bathroom solutions that integrate sanitation features, like electrolyzed-water cleaning within the bath suite, reinforce demand for coordinated lavatory faucets in institutional and residential settings[3]JP.TOTO.COM https://jp.toto.com/company/press/2025_11_26. The kitchen line benefits from feature-driven pricing that lifts average selling prices more than unit counts alone, which supports value growth. This application split keeps the Japanese faucets market balanced across volume-driven lavatory needs and value-oriented kitchen upgrades.

Bathroom replacement cycles run shorter due to wear, cleaning abrasion, and evolving hygiene expectations, which leads to steady lavatory reorder activity. Kitchen faucets often anchor larger remodel scopes and coordinate with sink, countertop, and appliance decisions, which supports bundled sales. DG TAKANO’s water-saving nozzle platform illustrates the premium tier’s innovation arc, with pulsating-flow performance framed by measurable water-reduction claims and retail partnerships that raise product visibility[4]PRTIMES.JP https://prtimes.jp/main/html/rd/p/000000770.000082557.html. The Japan faucets market size for kitchen applications is set to grow at a 2.83% CAGR over 2026-2031, driven by this premiumization path and the continued refresh of legacy system kitchens. Both the lavatory and kitchen segments, therefore, contribute distinct growth mechanics that reinforce overall market resilience.

By End-User: Residential Volume Anchor and Commercial Hygiene Premium

Residential end-use held 78.56% of volume in 2025, supported by multiple fixtures per dwelling and predictable replacement intervals for lavatory and kitchen use points. Commercial installations are growing at a 2.70% CAGR as hotels, offices, schools, hospitals, and transport hubs complete refurbishments that emphasize touchless functionality and temperature stability. LIXIL’s domestic mix in fiscal 2025 reflected renovation-driven gains, which align with a broad pivot toward replacements rather than greenfield installations across Japan’s building stock. Facility managers in commercial settings benefit from standardized fixtures and service models that simplify preventive maintenance and lifecycle planning. These patterns support steady throughput for both channels in the Japanese faucets market.

Residential demand is concentrated in B2C retail and showroom consults, where homeowners compare finishes, lever feel, and sensor responsiveness. Commercial demand flows through project channels and specifications that value compliance certifications and throughput performance in high-traffic contexts. The Japan faucets market size for commercial placements is projected to expand at a 2.70% CAGR as touchless operation, thermostatic protection, and water-saving credentials become standard bid requirements. Both channels reinforce each other because product learnings in public facilities shape homeowner expectations, and residential adoption validates mainstream price points for sensor designs. The result is a self-reinforcing path toward higher-spec baselines across use cases in the Japanese faucets industry.

By Distribution Channel: B2C Showrooms and Marketplaces Lead While B2B Projects Scale

B2C/Retail captured a 74.48% share in 2025, reflecting the central role of showrooms, home-improvement stores, and online marketplaces in residential replacements. B2B/Project channels are expanding at a 2.23% CAGR as hotels, offices, schools, and medical facilities coordinate larger-scale tenders with standardized specifications and spares. LIXIL’s showroom strategy now adds remote consultation capacity to raise appointment availability, a move that increases shopper access without expanding physical footprints. Retailers with robust buy-online-pickup options strengthen the convenience case for homeowners who prefer to inspect products in-store. These channel dynamics fit the renovation-led demand profile that defines the Japanese faucets market.

B2B projects prioritize brand families with transparent documentation and national service coverage to protect uptime in demanding environments. Partnerships that streamline estimates for simple replacements further reduce friction for homeowners and small businesses and align with the push to complete low-complexity swaps efficiently. The Japanese faucets market benefits from these parallel tracks because B2C captures the high-frequency residential cycle while B2B aggregates large orders that stabilize factory utilization. As more assortments include standardized sensor and thermostatic options, both channels can offer clear upgrades at consistent price steps. That clarity supports faster decisions and healthier sell-through velocities across regions.

By Geography: Kanto’s Scale Advantage and Kyushu’s Growth Outperformance

Kanto accounted for 36.18% of national revenue in 2025, reflecting high household density, deeper renovation budgets, and broad commercial building footprints concentrated around the Tokyo metropolitan area. The Japanese faucets market share, led by Kanto, is heavily skewed toward showroom-driven purchases and institutional refurbishments that require certified, reduced-contact fixtures. Major brands operate multiple flagship locations that help set specification preferences for the rest of the country. Kanto’s commercial demand skews toward projects with standardized fixture families and strong after-sales coverage. Together, these conditions sustain Kanto’s position as the strategic pivot for the Japanese faucets market.

Kyushu is the fastest-growing region, with a 2.71% CAGR, driven by urban vitality in Fukuoka and a healthy pipeline of hotel and public infrastructure refurbishments. The region’s project mix favors thermostatic shower valves and touchless lavatory taps in hospitality and transit applications, which pushes higher average selling prices. Rural revitalization efforts and the renovation of legacy housing stock also contribute to steady faucet replacements across smaller municipalities. Local distributors with close relationships with installers provide reliable access to parts and compatible assemblies, which is important in remote areas. That consistency makes Kyushu a durable contributor to national growth momentum.

Kansai and Chubu record stable renovation throughput aligned with commercial activity and manufacturing footprints, while Tohoku’s older population mix emphasizes accessibility and anti-scald features in replacements. In each of these regions, specification patterns track toward sensor operation, compatible thermostatic assemblies, and finish durability that withstands institutional cleaning. As brands align assortments and service networks, regional buyers gain similar upgrade pathways that are tuned to local installer availability and procurement preferences. The result is a harmonized baseline for faucet upgrades across regions that still respects unique project constraints and budget profiles. This harmonization supports predictable planning for factories and distributors across the Japanese faucets market.

Competitive Landscape

The Japanese faucets market is characterized by a high concentration among the top five producers, whose combined share of more than 60% reflects brand heritage, specification credibility, and nationwide service and dealer coverage. LIXIL’s water- and energy-saving share reached 94.5% of domestic faucet sales in fiscal 2025, and the company is targeting 100% by fiscal 2031, illustrating how large incumbents can align full portfolios with efficiency-led demand. TOTO’s integrated bathroom roadmap builds on hygiene and water-management features, including electrolyzed-water systems for mold and bacteria control that dovetail with touchless faucet operation. These capabilities reinforce procurement confidence and enable incumbents to set the pace for specification norms in institutional and premium residential segments.

Strategic moves continue to modernize assortments and manufacturing footprints. LIXIL refreshed bathroom and washroom portfolios for April 2026, including automatic faucets integrated into custom vanities and coordinated counter finishes, which support renovation-ready value propositions in Japan. The company also underscored its international growth thesis for hospitality and commercial channels, and those product-design learnings feed back into domestic lineups. TOTO’s product innovation pipeline continues to expand the sanitation and resource-efficiency envelope in bathroom systems, and those advances translate into differentiated faucet bundles selected by public facilities and private developers. Smaller specialists use retail partnerships and distinctive component claims to carve out niches in premium kitchen lines and eco-focused replacements.

Compliance and certification together act as a moat that rewards experience with Japanese standards and water-contact safety benchmarks. JWPA’s published standards and related pathways for testing and verification reduce ambiguity for buyers and simplify decision-making around safety and flow performance. Companies that publish clear, auditable product impact metrics, including avoided-water disclosures and environmental documentation, strengthen their positioning for institutional bids. The result is a competitive terrain where scale, documentation, and service coverage translate into durable share positions across the Japanese faucets market.

Japan Faucets Industry Leaders

LIXIL Corporation

TOTO Ltd.

KVK Corporation

SANEI Ltd.

KAKUDAI MFG. Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: LIXIL launched refreshed bathroom and washroom product lines effective April 1, 2026, including automatic faucets integrated into Custom Vanity enhancements and new finishes coordinated with the SATIS toilet series.

- November 2025: TOTO announced “Bathroom Clear Keep,” an electrolyzed-water feature for system bathrooms to suppress mold and stains, which aligns with hygiene-first bathroom designs that pair well with touchless faucets.

- August 2025: TOTO launched a redesigned Bedside Flush Toilet with an instant-heating Washlet and a compact hand-wash basin integration that supports elderly users and care environments.

- April 2025: LIXIL shared progress on portfolio and geographic initiatives, including continued profitability improvements in water-technology and renovation-led mix in Japan.

- October 2024: DG TAKANO, Yamada Denki, and Whipsaw announced an exclusive sales agreement for the meliordesign 5a kitchen faucet featuring the Bubble90 water-saving nozzle, highlighting premium kitchen innovation.

Japan Faucets Market Report Scope

A faucet is a kind of plumbing fixture where a knob, valve, or orifice controls the water flow. The components of a tap include the handle, the cartridge, the spout, the aerator, the mixing chamber, and the water inlets. The Japanese faucets market is segmented by product type, technology, material used, application, and end-user. By product type, the market is segmented into ball, disc, cartridge, and compression. By technology, the market is segmented into manual and automatic. By material used, the market is segmented into stainless steel, bronze, plastic, and other materials used (copper and zinc). By application, the market is segmented into bathroom and kitchen. By end user, the market is segmented into residential and commercial. The report offers the market size for the Japanese faucets market in value terms in USD for all the abovementioned segments.

| Ball |

| Disc |

| Cartridge |

| Compression |

| Chrome |

| Stainless Steel |

| Brass |

| Polytetra Methylene Terephthalate (PTMT) Plastic |

| Other Materials |

| Manual |

| Automatic |

| Deck Mount |

| Wall Mount |

| Kitchen Sink Faucets |

| Bathroom Sink Faucets |

| Residential |

| Commercial |

| B2C/Retail Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Local Hardware Stores | |

| B2B/Project |

| Kanto |

| Kansai |

| Chubu |

| Kyushu |

| Tohoku |

| By Product Type | Ball | |

| Disc | ||

| Cartridge | ||

| Compression | ||

| By Material | Chrome | |

| Stainless Steel | ||

| Brass | ||

| Polytetra Methylene Terephthalate (PTMT) Plastic | ||

| Other Materials | ||

| By Technology | Manual | |

| Automatic | ||

| By Installation Type | Deck Mount | |

| Wall Mount | ||

| By Application Type | Kitchen Sink Faucets | |

| Bathroom Sink Faucets | ||

| By End-User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Local Hardware Stores | ||

| B2B/Project | ||

| By Geography | Kanto | |

| Kansai | ||

| Chubu | ||

| Kyushu | ||

| Tohoku | ||

Key Questions Answered in the Report

What is the Japan faucets market size and growth outlook to 2031?

The Japanese faucets market size was USD 774.7 million in 2025 and is projected to reach USD 839.1 million by 2031 at a 1.34% CAGR over 2026-2031.

Which product category leads in Japan, and why?

Cartridge-based faucets lead due to single-lever convenience, reliable ceramic-disc performance, and standardized spares that simplify maintenance across residential and institutional settings.

Where is regional demand strongest in Japan?

Kanto leads with 36.18% share, supported by dense housing stock, strong commercial footprints, and flagship showroom coverage that shapes national specification trends.

What features are driving premiumization in commercial installations?

Touchless operation, thermostatic temperature control, and water-saving performance dominate specifications, often paired with integrated sanitation features in bathroom systems.

How are leading companies aligning with efficiency-led demand?

LIXIL reported 94.5% of domestic faucet sales carried energy- and water-saving attributes in fiscal 2025 and targets 100% by fiscal 2031, signaling full portfolio conversion.

Which end-user segment is growing faster and why?

Commercial installations are growing faster due to hygiene-focused refurbishments across hotels, offices, schools, hospitals, and transport hubs, with sensor and thermostatic features set as defaults.

Page last updated on: