Home and Property Improvement

9th JuneA Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

The Global Hot Tub Market Report is Segmented by Product Type (Acrylic/Portable, Inflatable/Rotomolded, and More), Seating Capacity (2–3, 4–7, 8–7, 8+ Person), End-User (Residential, Health & Fitness Clubs, and More), Distribution Channel (Specialty Retail, Online/E-commerce, and More), and Geography (North America, South America, Europe, Asia-Pacific, MEA). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

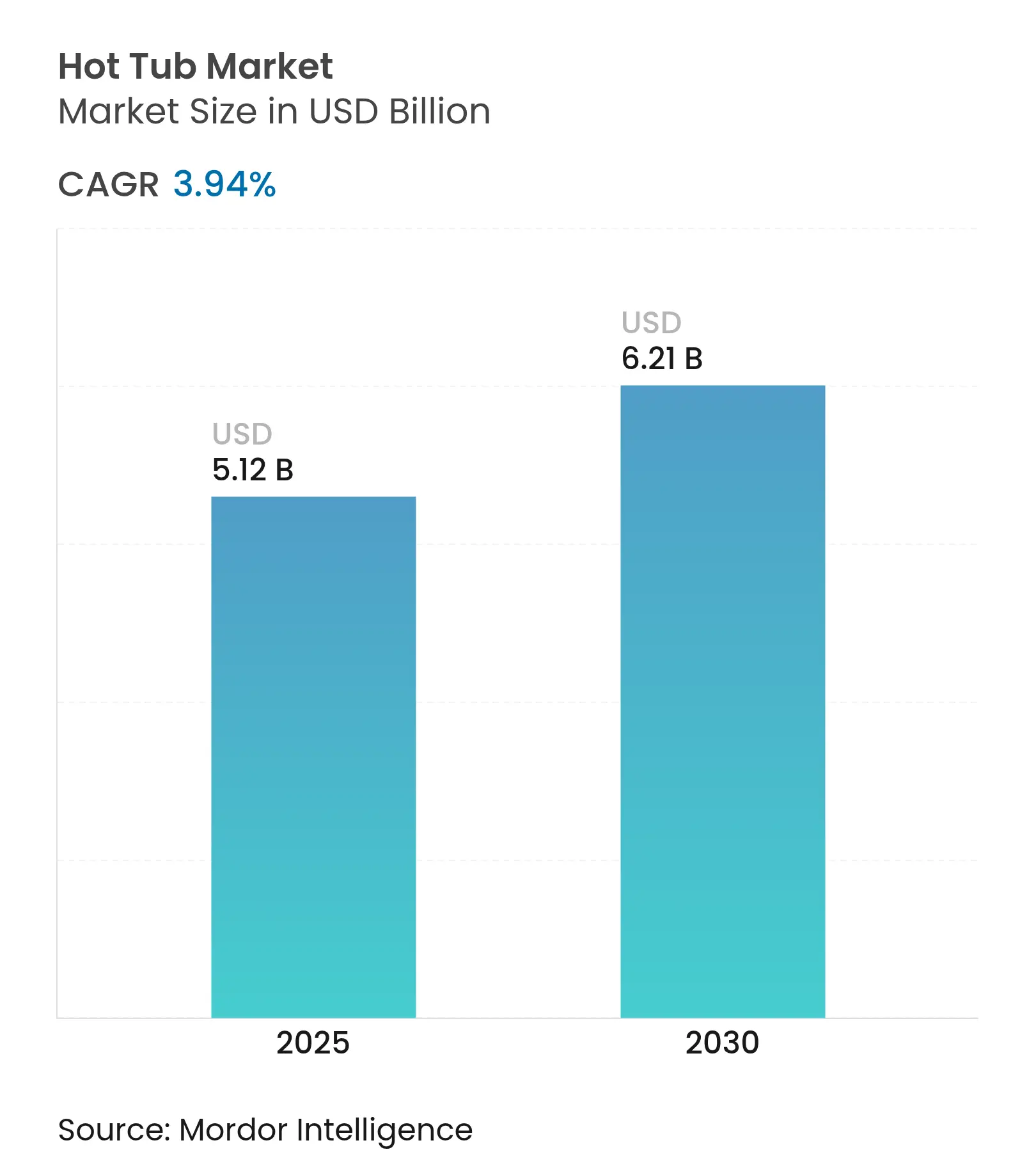

| Market Size (2025) | USD 5.12 Billion |

| Market Size (2030) | USD 6.21 Billion |

| Growth Rate (2025 - 2030) | 3.94 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The growth outlook is steady rather than spectacular, yet the headline rate disguises rapid shifts in energy regulation, demographic structure, and channel behavior that are creating pockets of outsized opportunity. California will prohibit gas heating for new pool and spa installations beginning January 2026, while the South Coast Air Quality Management District plans to retire 700,000 legacy gas-fired pool heaters over three decades, accelerating adoption of electric and renewable heating systems. North America still controls 37.56% of 2024 revenue, but Asia-Pacific delivers the fastest 6.11% CAGR through 2030 as Japan’s senior share reaches 29.3% of the population and policymakers position hydrotherapy as preventive healthcare.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising consumer spending on home wellness

& outdoor living upgrades

Rising consumer spending on home wellness

& outdoor living upgrades

| +1.2% | North America, Europe, Japan | Medium term (2–4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

North America, Europe, Japan

|

Impact Timeline

:

Medium term (2–4 years)

|

Integration of energy-efficient &

smart-connected features

Integration of energy-efficient &

smart-connected features

| +0.8% | North America, EU, expanding in APAC | Long term (≥ 4 years) | |||

Hospitality & vacation-rental

adoption boosting occupancy & ADR

Hospitality & vacation-rental

adoption boosting occupancy & ADR

| +0.6% | Tourism-focused regions worldwide | Short term (≤ 2 years) | |||

Product innovation in swim-spa hybrids is

broadening use cases

Product innovation in swim-spa hybrids is

broadening use cases

| +0.4% | North America core, spreading to APAC | Medium term (2–4 years) | |||

Aging population seeking hydrotherapy for

chronic pain relief

Aging population seeking hydrotherapy for

chronic pain relief

| +0.3% | Japan leads, North America & Europe follow | Long term (≥ 4 years) | |||

Remote-work lifestyle driving backyard

sanctuary investments

Remote-work lifestyle driving backyard

sanctuary investments

| +0.2% | Urban and suburban centers globally | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Consumer Spending on Home Wellness & Outdoor Living Upgrades

Lockdown-era behavior persists as homeowners elevate outdoor spaces into multifunctional sanctuaries that merge recreation, health, and hospitality. Dealers in the United States report wellness products now outpacing grills and patio furniture in both dollar volume and attachment-rate growth. Luxury travelers have shifted expectations, with 73% prioritizing wellness amenities when selecting accommodations, and that commercial mindset spills over into residential remodeling budgets. Japan’s 29.3% senior ratio drives bathroom retrofits that combine electric floor heating, low-threshold entries, and grab bars to reduce fall incidents; 55% of survey respondents cite bathing safety concerns, elevating hot tubs from indulgence to necessary adaptation[1]Panasonic Housing Solutions, “Heat Safe Style Launch,” prtimes.jp. Outdoor kitchens, pergolas, and fire features often accompany spa installations, lifting total project spending and supporting specialty retailer margins. Financing packages offered through dealer networks mitigate sticker shock, extending accessibility to mid-income households and sustaining unit velocity even during inflationary cycles.

Integration of Energy-Efficient & Smart-Connected Features

California’s flexible-demand controls, effective September 2025, allow utilities to manage pump runtimes remotely, turning internet-enabled control systems from optional extras into compliance essentials. Hayward Holdings credits its SmartPad™ ecosystem for an 8% year-on-year net sales lift to USD 228.8 million in Q1 2025, confirming that connectivity now underpins tangible revenue gains [2]Hayward Holdings, “Q1 FY25 Results,” investor.hayward.com. Variable-speed pumps, thermal-blanket covers, and AI-based water-chemistry dosing collectively reduce operating costs, a selling point that resonates with both eco-conscious consumers and commercial facility managers tasked with meeting corporate ESG targets. Hotels indicate a 92% penetration rate for energy-optimized spa systems as they align capital improvements with sustainability branding, ensuring the premium for smart-enabled tubs is increasingly viewed as a prerequisite rather than a luxury line item. This regulatory and behavioral alignment suggests that intelligent, energy-efficient spas will define the baseline specification for new builds and retrofits alike.

Hospitality & Vacation-Rental Adoption Boosting Occupancy & ADR

Hot-tub-equipped accommodations consistently outperform comparable listings on leading rental platforms, driving higher occupancy and average daily rates that recoup installation costs in as few as two high-season cycles. Global hotel occupancy surpassed 72% in 2025, providing operators with cash flow to reinvest in wellness zones that entice guests to stay longer and spend more on ancillary services. The Aquatic Trends Report 2025 notes that 28.4% of aquatic venues already operate hot tubs, and health clubs lead at 59.3% penetration, reinforcing spas as central to revenue diversification strategies[3]Emily Tipping, “Aquatic Trends Report 2025,” Recreation Management, recmanagement.com. Recreation centers also report that hydrotherapy classes attract new membership segments, extending utilization beyond passive soaking. Commercial adoption feeds back into consumer psychology: travelers experience premium hydrotherapy on vacation and subsequently seek to replicate the experience at home, creating a virtuous sales cycle for manufacturers.

Product Innovation in Swim-Spa Hybrids Broadening Use Cases

Manufacturers are compressing lap pools and hydrotherapy into single chassis designs that measure under 20 feet, offering upstream resistance currents for aerobic training alongside jet-massage seating. Watkins Wellness refreshed its Highlife® range with sculpted shells that adjust buoyancy zones, catering to both active swimmers and relaxation seekers. Nanobubble purification developed by Jacuzzi minimizes surface tension and oxidizes contaminants at the sub-micron scale, reducing chlorine demand and extending water-change intervals from quarterly to biannual cycles. Swim-spa hybrids resonate with urban property owners who lack backyard acreage but desire full-body workouts, and they appeal to aging athletes needing low-impact exercise modalities. Dealers leverage these dual-function narratives to upsell from basic four-seat tubs into higher-margin hybrid systems, widening the hot tub market size without cannibalizing core acrylic sales.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High upfront cost & complex

installation requirements

High upfront cost & complex

installation requirements

| -0.9% | Global, sharper in emerging markets | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.9%

|

Geographic Relevance

:

Global, sharper in emerging markets

|

Impact Timeline

:

Short term (≤ 2 years)

|

Tariff / input-cost volatility for

acrylic & electronics

Tariff / input-cost volatility for

acrylic & electronics

| -0.7% | North America, EU supply chains | Medium term (2–4 years) | |||

Water-use restrictions in drought-prone

regions

Water-use restrictions in drought-prone

regions

| -0.3% | Western North America, Australia, Mediterranean | Long term (≥ 4 years) | |||

Shift toward minimalist walk-in showers

Shift toward minimalist walk-in showers

| -0.2% | Space-constrained urban markets worldwide | Medium term (2–4 years) | |||

| Source: Mordor Intelligence | ||||||

High Upfront Cost & Complex Installation Requirements

Base units often represent only half of the final invoice once electrical upgrades, concrete pads, crane lifts, and permit fees accumulate. Dealers advised that power-panel expansions can add USD 1,500–3,000, while delivery cranes in congested city centers routinely exceed USD 900 per hour. Such surcharges deter price-sensitive shoppers and push some buyers toward lower-ticket inflatables, which connect to standard outlets and require no site prep. Compliance with the CDC’s Model Aquatic Health Code adds another layer of cost for commercial venues, mandating secondary sanitation that increases both CapEx and operational complexity [4]Centers for Disease Control and Prevention, “2024 Annex to the Model Aquatic Health Code,” cdc.gov. Retailers simultaneously face labor scarcity; 63% raised wages in 2024 to secure technicians, further inflating project budgets. Financing programs and manufacturer rebates alleviate some pressure yet cannot fully offset psychological barriers associated with high-ticket discretionary purchases.

Tariff / Input-Cost Volatility for Acrylic & Electronics

Acrylic sheets, derived from petrochemicals, swing in tandem with global energy prices, while semiconductor chip shortages lengthen lead times for control boards. Latham Group disclosed that tariffs influence up to 20% of raw material inputs, compressing margins despite lean manufacturing gains that improved gross margin by 190 basis points. Distributors such as Pool Corporation reference freight surcharges and currency fluctuations when issuing 2025 earnings guidance, highlighting the unpredictability embedded in cost-of-goods sold. Large manufacturers lock in multi-year resin contracts and invest in domestic electronics assembly to dampen volatility, yet smaller brands lack similar hedging capacity, exposing them to sudden price shocks that can disrupt production schedules and strain dealer relationships.

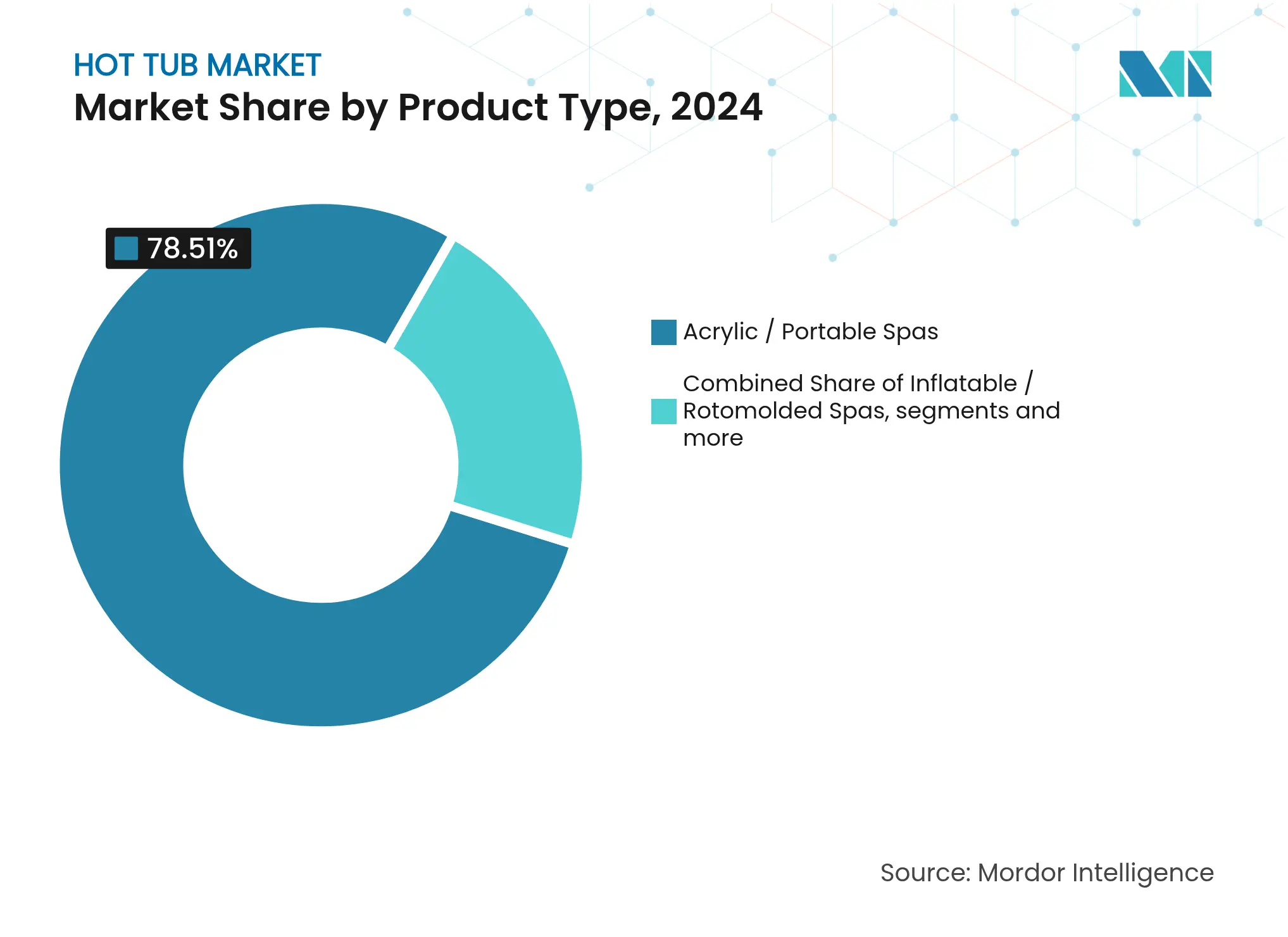

By Product Type: Acrylic Leadership Meets Inflatable Disruption

Acrylic portable spas controlled 78.51 % of the hot tub market share in 2024, anchored by multi-layer shells, diverse jet arrays, and customizable cabinetry options. Manufacturers capitalize on the segment’s premium positioning to bundle LED lighting, Bluetooth sound, and Wi-Fi diagnostics that elevate average selling prices. The hot tub market size, attributable to inflatable and rotomolded models, though smaller, is climbing at a 5.12% CAGR as consumers prioritize affordability, quick setup, and easy relocation. In-ground custom installations serve design-build architects catering to ultra-high-net-worth clients who demand seamless integration with landscape architecture. Swim-spa hybrids stretch category boundaries by drawing fitness enthusiasts and space-constrained urban dwellers who need all-season exercise without the cost of full pools. Smart/IoT categories continue to evolve as California-style demand-response programs spread; embedded sensors now trigger leak alerts, water-balance prompts, and energy-consumption reports direct to mobile apps, creating data-driven service opportunities for dealers.

Manufacturing strategy reflects this dichotomy. Premium players such as Watkins Wellness maintain acrylic dominance by refining production efficiencies; modular molds allow quick color swaps, reducing changeover time and enabling limited-edition finishes that command price premiums. Conversely, inflatable specialists leverage viral digital marketing campaigns and warehouse club partnerships, generating flash-sale volumes that erode acrylic-price elasticity. Suppliers anticipate rising environmental compliance costs for acrylic production and therefore explore bio-based resins and recycled content to defend sustainability credentials without compromising performance. Technological leapfrogs—such as nanobubble purification that cuts sanitizer consumption—allow traditional acrylic models to defend relevance even as lower-cost formats proliferate.

Note: Segment shares of all individual segments available upon report purchase

By Seating Capacity: Compact Formats Gain Momentum

Units seating 4–7 people retained the largest slice of demand at 43.56% in 2024, balancing family utility with manageable operating costs. Yet 2–3-seat configurations are accelerating at 4.51% CAGR, mirroring global urbanization and household downsizing trends. Compact tubs heat faster, draw lower amperage, and often run on 120-volt circuits, reducing installation hurdles. Japanese seniors, conscious of slip risks, favor two-person tubs equipped with integrated rails and lower thresholds, an adaptation aligned with national strategies to mitigate bath-related injuries among older adults.

Larger eight-plus-seat models cater to ski resorts, luxury chalets, and corporate wellness retreats where group experiences enhance perceived value. The mid-range six-seat cohort remains a staple for suburban households, yet the market is bifurcating toward either ultra-compact personal spas or dual-purpose swim-spa systems that accommodate both workout regimens and social gatherings. Energy-efficiency frameworks that peg consumption to water volume provide latent momentum for smaller capacities, reinforcing the shift toward compact designs.

By End-user: Vacation Rentals Reshape Commercial Dynamics

Residential buyers still account for 64.23% of the 2024 market value, bolstered by culture-driven associations between backyard leisure and ownership pride. Nevertheless, vacation rentals and boutique hotels deepen penetration at a 5.91% CAGR because spa amenities directly translate into revenue metrics such as higher booking premiums and improved average daily rates. Commercial operators calculate payback periods in fewer than 24 months when occupancy reaches regional high-season benchmarks. Health clubs and recreation centers also integrate hot tubs to diversify program offerings; hydro-massage sessions, contrast-bath recovery, and aquatic circuit classes add incremental revenue streams.

Rehabilitation facilities in aging economies adopt clinical-grade spas with adjustable lift seats and programmable temperature bands, targeting chronic-pain relief and post-surgery therapy markets. End-user diversification cushions the hot tub market against macro-economic headwinds: when discretionary residential spending tightens, commercial retrofits, funded through operating budgets and governmental healthcare initiatives, compensate.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

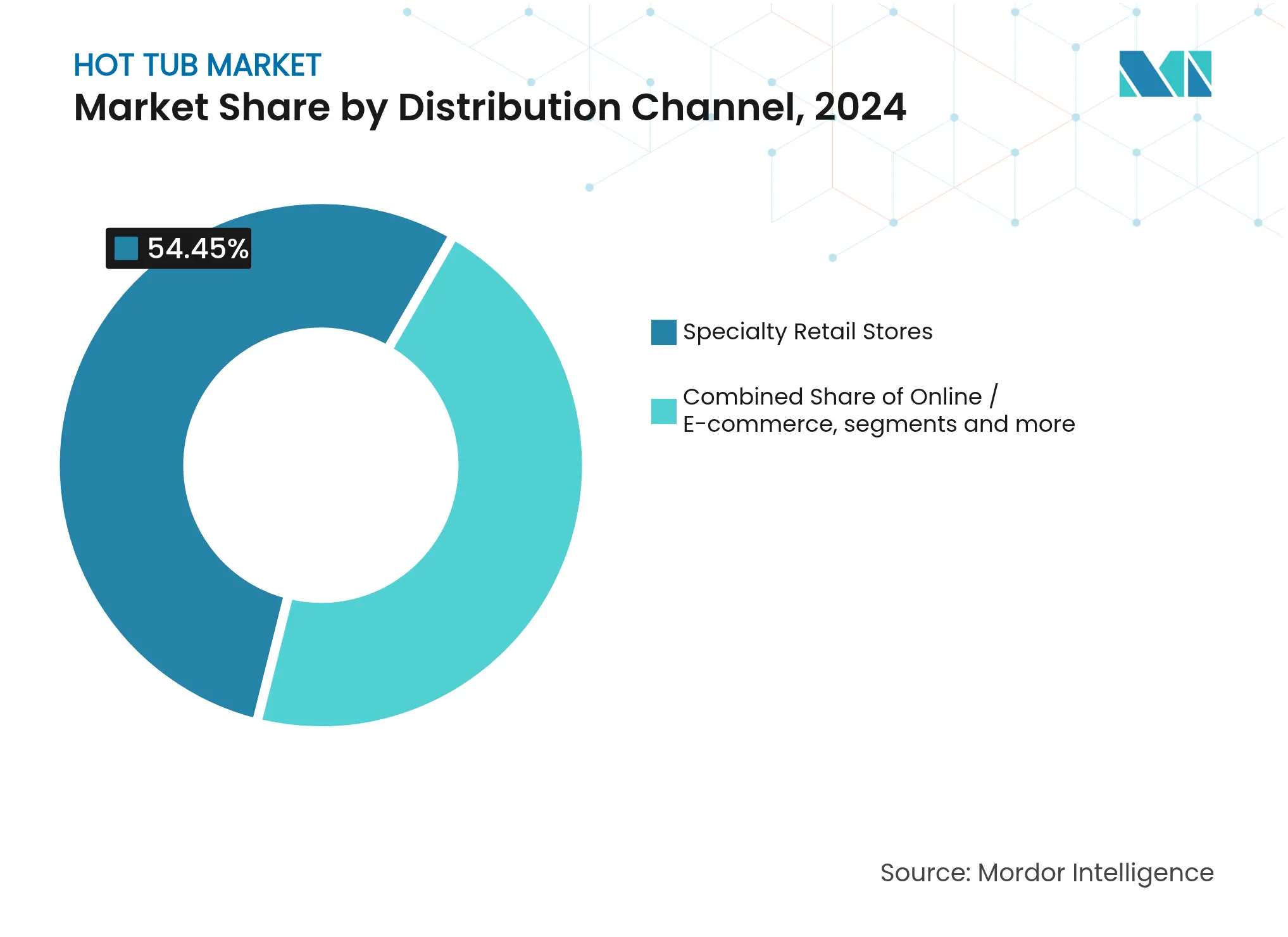

By Distribution Channel: Digital Transformation Accelerates

Specialty retailers currently deliver 54.45% of global units, leveraging immersive showrooms and white-glove installation services to justify value-added pricing. However, online channels record a 4.94% CAGR as consumers move initial research, feature comparison, and financing pre-qualification online before setting foot in a store. Retailers with robust e-commerce portals see higher close rates because digital touchpoints qualify leads and reduce sales cycle friction. Big-box and warehouse clubs expand category reach by stocking private-label inflatables and value-line roto molds; although gross margins are thin, manufacturers gain volume and brand visibility.

Builder and contractor channels benefit from housing-start recoveries and backyard-living megaprojects that integrate spas with outdoor kitchens, shade structures, and fire features. Direct-to-consumer web shops run by manufacturers compress channel costs but require localized service networks to fulfill warranty obligations, creating delicate balancing acts between traditional dealers and emerging online customer bases.

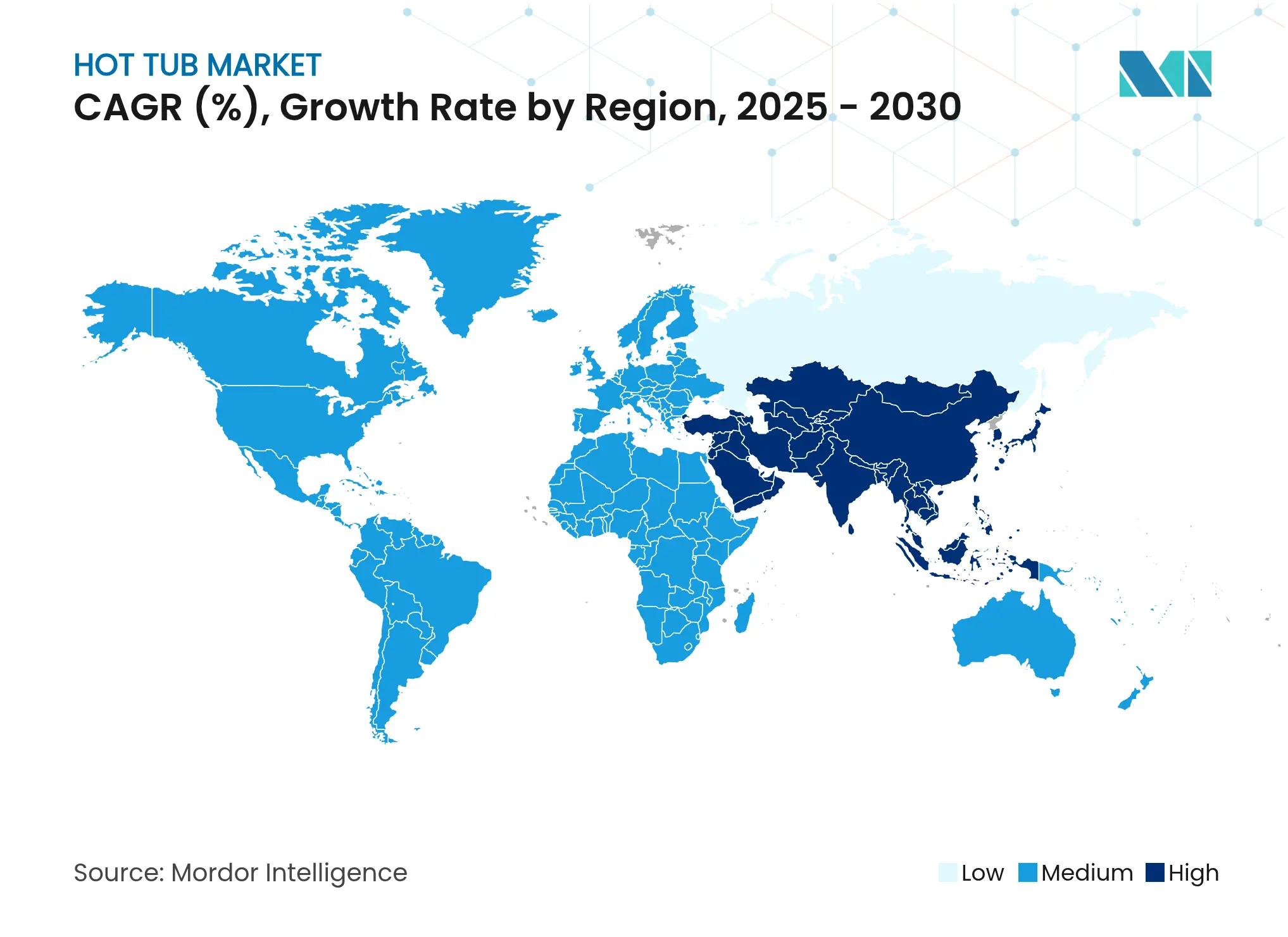

North America held 37.56% of the 2024 hot tub market share, supported by high disposable income, established service networks, and a sizable installed base needing replacement. Yet looming energy mandates shift product development toward plug-and-play heat-pump and solar-ready configurations. California’s 2026 gas-heater ban, together with variable-speed pump requirements effective September 2025, means North American manufacturers must reengineer plumbing systems for higher head pressures and integrate cloud-based remote-management dashboards as standard. Canada offers moderation, with milder regulation but similar consumer affluence, while Mexico provides cost advantages for near-shoring component supply and tapping a burgeoning middle class.

Asia-Pacific is the dynamo, advancing at a 6.11% CAGR through 2030. Japan’s demographic realities drive government and private insurers to endorse hydrotherapy as a preventive modality, aiming to reduce the projected 190 trillion-yen national healthcare tab by 2040. Studies such as the HEIJO-KYO project reveal cardiovascular stress during unsupervised hot bathing among older adults, prompting demand for safer, professionally engineered tubs with temperature governors and anti-entrapment features. China expands simultaneously as a manufacturing hub and an emerging consumer base, with middle-class households upgrading from communal bathhouses to private balconies equipped with compact spas. Australia’s cultural emphasis on outdoor living sustains premium sales, while South Korea’s high smart-home penetration rates create fertile ground for IoT-enabled spas.

Europe registers consistent mid-single-digit growth, propelled by stringent energy directives that compel hoteliers and resort operators to retrofit spas with efficient pumps and thermal covers. Germany and the Nordic region rely on saunas as wellness staples, and cross-selling of hydrotherapy complements entrenched sauna culture. The Mediterranean faces water-scarcity challenges that motivate low-volume, high-efficiency spa designs. South America sees upside potential in Brazil’s tourism corridors and Chile’s resort developments; however, currency volatility and import duties complicate capital budgeting. The Middle East and Africa are frontier arenas where luxury hospitality projects such as Red Sea developments in Saudi Arabia embed spas into branded residences, yet the broader consumer market remains constrained by income disparities and high imported-product pricing. Geographic diversification therefore steadies aggregate growth even as individual regions navigate idiosyncratic economic and regulatory cycles.

Market Concentration

Industry consolidation is moderate but intensifying, highlighted by MAAX Spas’ 2025 acquisition of L.A. Spas, which created one of North America’s three largest manufacturers by output. Masco-owned Watkins Wellness leverages 1.5 million lifetime unit installations to feed dealer loyalty programs and capture lucrative chemical and parts aftermarket revenue. Jacuzzi Group differentiates through nanobubble purification that decreases sanitizer consumption and reinforces eco-branding, while Hayward Holdings packages SmartPad™ automation with proprietary pumps and heaters to lock in system sales. Vertical integration becomes a hedge against acrylic and chip volatility; Latham Group’s fiberglass pool operations secure resin bulk-purchase economies, demonstrating how adjacent categories bolster bargaining power.

Channel strategy is another differentiator. Jacuzzi balances specialty dealer exclusives with big-box placements at Home Depot and Costco to maximize reach without alienating core installers. Start-ups in the inflatable space use influencer marketing and flash-sale events to rack up volume, but often falter on after-sales service, creating acquisition targets for legacy brands looking to broaden entry-level offerings. Compliance capabilities also sort contenders: the CDC’s Model Aquatic Health Code revisions and California energy codes impose engineering documentation and factory audits that smaller entities struggle to absorb. Intellectual-property portfolios, service-network breadth, and capital access will set the pace of share shifts throughout the decade.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts (Value, USD Bn)

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Hot tubs are a pool of water used for relaxation and hydrotherapy. A hot tub is designed to be used by more than one person at a time. It is usually heated by natural gas or electricity. However, other types of hot tubs such as submersible wood-fired hot tubs and solar hot tubs are also available in the market. The market is segmented into portable hot tubs and fixed hot tubs. by end-user, the market is segmented into residential and commercial, by geography, the market is segmented into North America, Europe, Asia-Pacific, Latin America, and Middle-East, and Africa. The report offers market sizing and forecasts for hot tubs in value (USD million) for all the above segments.

A Leading Sanitaryware Company’s Journey in Saudi Arabia

4 Min Read

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.