Bath Fittings And Accessories Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 134.59 Billion |

| Market Size (2031) | USD 146.78 Billion |

| Growth Rate (2026 - 2031) | 1.75% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

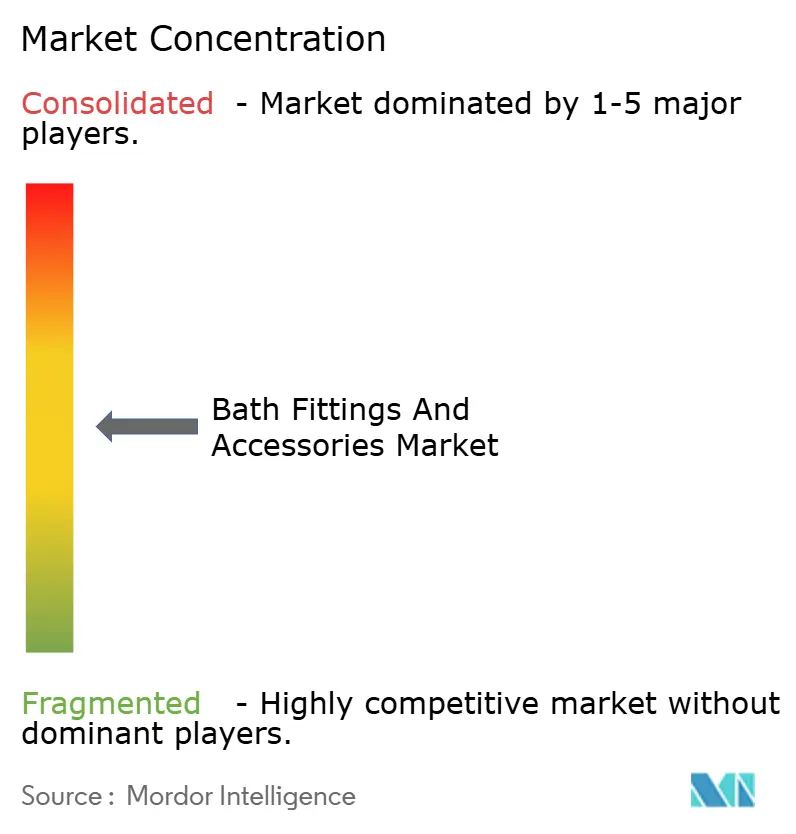

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bath Fittings And Accessories Market Analysis by Mordor Intelligence

The bath fittings and accessories market size is expected to grow from USD 132.27 billion in 2025 to USD 134.59 billion in 2026 and is forecast to reach USD 146.78 billion by 2031 at 1.75% CAGR over 2026-2031. Growth in the bath fittings and accessories market reflects near-term stability with clear drivers tied to hygiene upgrades, water-efficiency codes, and digital buying journeys that simplify configuration and installation planning. A leading product category is positioned to hold the largest share and expand fastest as touchless activation and efficiency labels gain priority in service-intensive facilities and multi-unit properties. Regional dynamics show one core region with the largest contribution, while another accelerates on infrastructure programs and first-time accessorizing in middle-income housing, creating distinct product bundles and price points across channels. Specialty stores maintain an experiential edge through consultative selling and finish validation, while online platforms grow faster as curated kits compress purchase cycles from research to a single digital transaction. End-user profiles balance a large residential base with rising commercial specifications that prioritize contact minimization and antimicrobial surfaces, which reinforces premium adoption pathways in the bath fittings and accessories market.

Key Report Takeaways

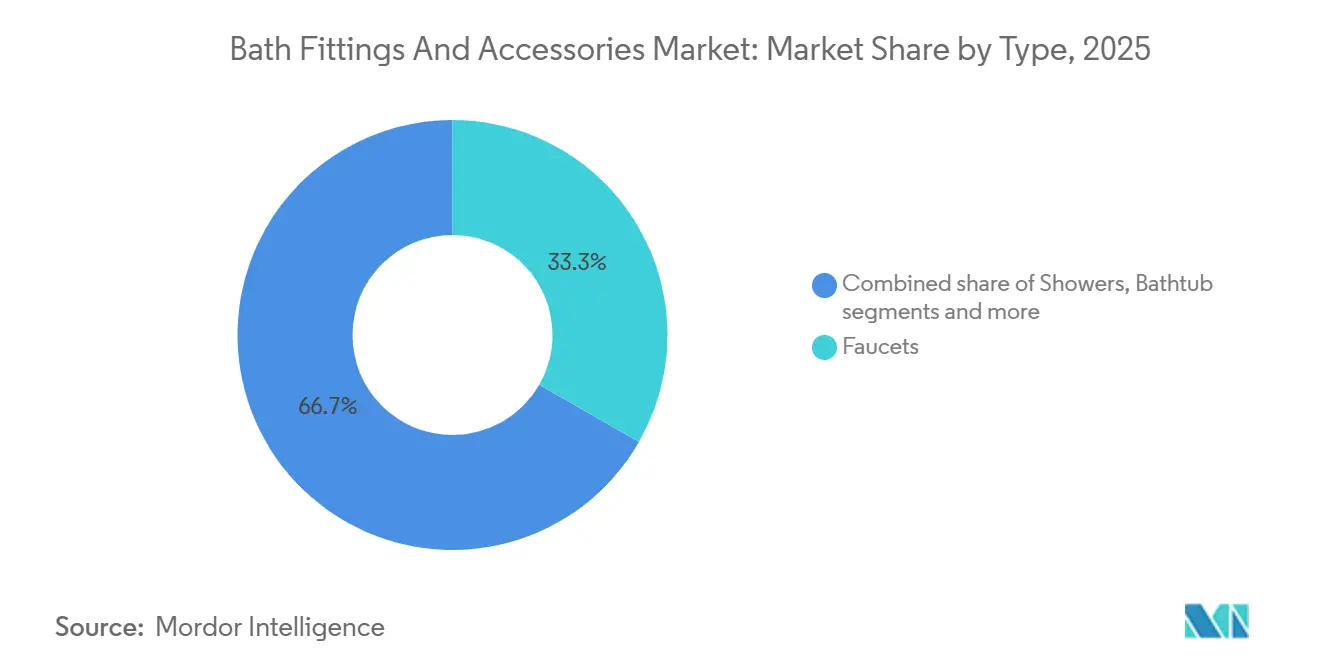

- By type, faucets led with 33.28% revenue share in 2025 in the bath fittings and accessories market, while faucets are also projected to post the highest growth at 11.43% CAGR through 2031.

- By end user, residential accounted for 59.62% share in 2025 in the bath fittings and accessories market, while commercials are set to expand at a 7.11% CAGR to 2031.

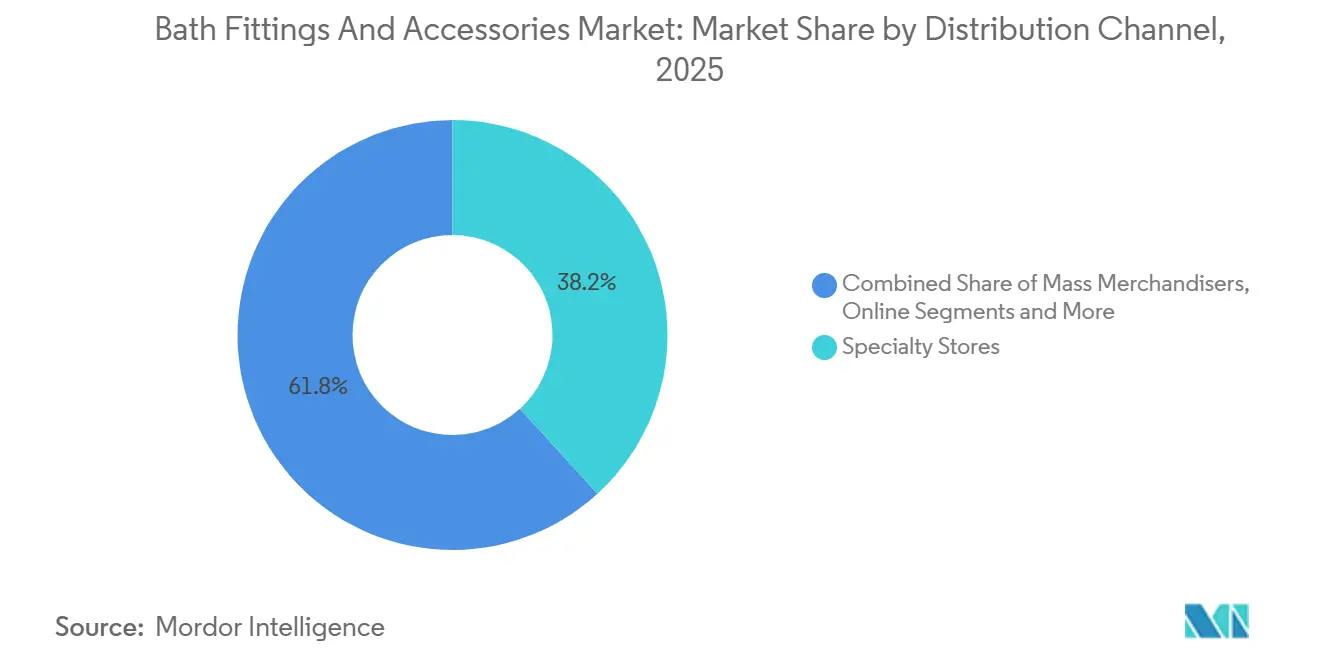

- By distribution channel, specialty stores held 38.21% share in 2025 in the bath fittings and accessories market, while online channels are projected to grow at 14.02% CAGR through 2031.

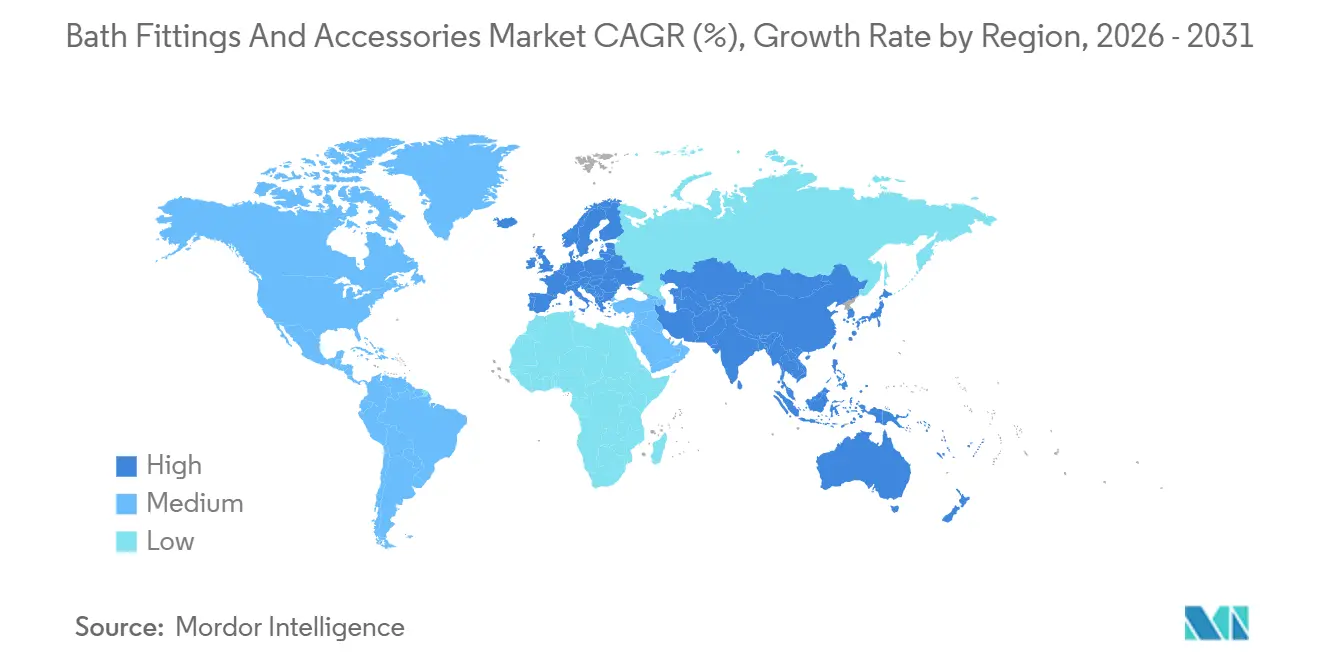

- By geography, Asia-Pacific captured 32.08% share in 2025 in the bath fittings and accessories market, while South America is forecast to record the fastest growth at 9.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bath Fittings And Accessories Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Residential Renovation And R&R Upcycle | + 2.8% | Global, with concentrated intensity in China, Australia, and North America | Medium term (2-4 years) |

| Asia-Pacific Urban Construction and Housing Starts | + 3.1% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Medium term (2-4 years) |

| Hygiene, Touchless, and Safety-Driven Upgrades | + 2.3% | Global, with accelerated adoption in North America, Europe, and the Asia-Pacific hospitality corridors | Short term (≤ 2 years) |

| Omnichannel Shift, Online Assortment Broadening | + 1.9% | Global, led by North America and Europe, with rapid penetration in India and China metro clusters | Short term (≤ 2 years) |

| Aging-In-Place Retrofits (Grab Bars, Slip Resistance) | + 1.6% | North America and Europe, early gains in Japan and Australia | Long term (≥ 4 years) |

| Water-Efficiency-Led Replacements and Specs | + 2.2% | National, with early gains in California, Colorado, Hawaii, and Canadian provinces, progressive adoption in the European Union, and select Asia-Pacific markets. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Asia-Pacific Urban Construction and Housing Starts Drive Infrastructure-Linked Demand

China’s 2025 urban-renewal completions of 27,100 neighborhoods, supported by RMB 133.2 billion (USD 19 billion) in funding, are accelerating replacement of outdated water and sanitary hardware, which anchors near-term orders across faucets, showerheads, sinks, and core accessories in the bath fittings and accessories market. The multi-year renewal program shortens natural replacement intervals into tight procurement windows, lifting volumes through bundled specifications and standardized SKUs for large-scale installs. Corporate relocations and office expansions across key Asia-Pacific metros stimulate commercial restroom buildouts that prioritize touch-free use and antimicrobial finishes, amplifying demand for compatible sub-assemblies and fitting interfaces. Investment resilience in Northeast Asia alongside steady office fit-outs in India sustains multi-unit orders that benefit suppliers with robust project management and regional inventory buffers. The combined effect is a durable base that supports the region’s 32.08% revenue share while laying a longer pipeline for retrofit and maintenance cycles in the bath fittings and accessories market.

Residential Renovation and R&R Upcycle Extends Product Lifecycles into Premium Tiers

Australia’s renovation share reached 40% of residential construction in 2024, and a 46,000-unit gap between new-dwelling completions and underlying demand steered homeowners toward staged bathroom upgrades that prioritize visible impact over structural changes. Cost inflation increased 2024 budgets by 2.8% for detached homes and 5.1% for higher-density projects, pushing value-focused replacements such as walk-in showers, single-lever valves, and frameless enclosures that unlock mid-tier finish premiums. In North America, DIY activity favored local hardware outlets as homeowner traffic shifted toward curated accessory bundles and quick-turn installation guides, reinforcing higher attachment rates for coordinated finishes [1]Home Improvement Research Institute, “Homeowner Project Activity and Channel Shifts 2025,” HIRI, hiri.org. Renovation budgets tolerate moderate price steps for aesthetic cohesion, so brushed-nickel and matte-black kits gain share against base chrome assortments even if unit counts flatten. These patterns support sustained value growth in the bath fittings and accessories market as premium attachments and coordinated suites expand spend per project without reliance on new-build cycles.

Water-Efficiency-Led Replacements and Specs

California’s code enforcement, effective January 1, 2026, reduces allowable flow and flush thresholds, which compels replacements of non-compliant fixtures in residential settings and drives immediate retrofit activity that benefits certified SKUs [2]California Energy Commission, “Building Energy Efficiency Standards, Title 24,” California Energy Commission, energy.ca.gov. The United States Environmental Protection Agency’s WaterSense draft Version 2.0 for faucets proposes a 1.2 gpm maximum at 60 psi, aligning federal labeling with a tightening state landscape and raising the bar for efficiency-centric specifications. Colorado requires WaterSense-labeled faucets, showerheads, toilets, and urinals for products sold under its statute, which channels wholesale restocking toward certified assortments and accelerates turnover of legacy inventory. In response, manufacturers prioritize dual-certified product lines and invest in documentation that simplifies submittals for building inspectors and specifiers. The net effect is a compliance-led demand pulse that sustains premium SKU velocity and underpins the efficiency segment within the bath fittings and accessories market.

Omnichannel Shift and Online Assortment Broadening Collapse Purchase Cycles

Large home-improvement retailers reported double-digit online growth as click-and-collect and direct ship options aligned with how households now plan bathroom upgrades, moving configuration upstream to digital journeys that package faucets, showers, and accessories into ready-to-install sets. Augmented-reality previews, guided finish selection, and project calculators shorten the path from consideration to purchase, while same-day pickup removes friction that historically required multiple showroom visits. Specialty showrooms hold share through consultative selling and exclusive assortments, yet adapt by integrating virtual design support and inventory transparency to defend close rates. Suppliers that can expose accurate stock status, replenish rapidly, and provide robust content gain placement advantages across marketplaces. The bath fittings and accessories market benefits from this shift as conversion efficiency improves and attachment rates increase through curated kits that align with common bath footprints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Big-Box and Wholesale Channel Power Compressing Margins | - 1.4% | Global, with acute pressure in North America and Europe, where concentration is highest | Short term (≤ 2 years) |

| Smart Fixture Maintenance and Cybersecurity Concerns | - 0.8% | Global, with heightened sensitivity in North America, Europe, and the Asia-Pacific premium hospitality segments | Medium term (2-4 years) |

| Long Replacement Cycles for Accessories | - 1.1% | Global | Long term (≥ 4 years) |

| Raw Material Price Volatility (Brass, Steel, Resins) | - 1.6% | Global, with concentrated impact on manufacturers sourcing copper and zinc from Chile, Peru, and Indonesia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Big-Box and Wholesale Channel Power Compressing Margins

Recent earnings commentary from leading home-improvement retailers flagged price sensitivity in core categories, indicating that procurement teams resist supplier hikes and lean on private-label alternatives to defend category margins. Margin performance, paired with unit softness, suggests tighter vendor terms and incentive structures that protect retail profitability but pressure OEM operating leverage. This dynamic squeezes smaller or mid-tier brands that cannot scale tooling and inventory across multiple chains, forcing assortment rationalization or a pivot to specialty showrooms and direct e-commerce. Retailers also shift promotional calendars toward house lines when branded suppliers balk at deeper rebates, tilting shelf economics away from premium SKUs without clear differentiation. The result is a channel-mix constraint that compresses both volume and margin for brands lacking distinct features in the bath fittings and accessories market.

Smart Fixture Maintenance and Cybersecurity Concerns Limit Premium-Tier Adoption

Connected faucets, showers, and toilets that rely on cloud updates and analytics introduce new lifecycle costs and governance risks for hospitality and multifamily operators evaluating build standards. Facility leaders increasingly request third-party security validations, such as UL cybersecurity assessments and adherence to ISO/IEC 27001-aligned data handling, before greenlighting large-scale deployments [3]International Organization for Standardization, “ISO/IEC 27001 Information Security,” ISO, iso.org. Maintenance protocols for networked fixtures also require coordination between building IT and operations teams, which can slow adoption if support models are unclear. In environments with high guest turnover, operators weigh brand reputation risks from data or uptime issues against the value of telemetry and remote diagnostics. These considerations temper near-term penetration of connected SKUs in the bath fittings and accessories market until certification frameworks and support economics mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Faucets Lead Share and Growth on Touchless Mandate Convergence

Faucets captured 33.28% of the bath fittings and accessories market share in 2025 and are projected to expand at 11.43% CAGR through 2031 as operators increase touchless specifications in high-traffic settings to reduce contact transmission. Investments in precision cartridge assembly and automation support quality consistency at higher volumes, illustrated by TOTO’s 2025 United States manufacturing expansion that integrated advanced robotics for ceramic assembly and related high-precision components. Showers remain the second-largest segment on the back of curbless conversions and widespread use of thermostatic mixing valves aligned with ASSE 1016 and CSA B125 anti-scald standards that promote occupant safety. Bathtubs see premium-centric demand concentrated in luxury remodels, while bathroom sinks benefit from style upgrades that stretch replacement intervals across durable materials. Across the bath fittings and accessories market, the balance of code compliance, safety, and hygiene features strengthens the value proposition of premium faucet and shower systems relative to commodity alternatives.

Accessory suites such as towel racks, hooks, and paper holders feature thin unit margins but high attach rates when bundled into coordinated finish programs that incentivize complete-room refreshments. Grab bars continue to gain specification momentum as aging-in-place considerations rise, supported by survey evidence of stronger demand for accessibility features and clear homeowner intent to remain in current residences. ADA-compliant installations require mounting heights between 33 and 36 inches with support designed for a minimum 250-pound load, which shapes both hardware design and installation planning [4]American with Disabilities Act, “2010 ADA Standards for Accessible Design,” U.S. DOJ, ada.gov. For suppliers, coordinated accessory programs create efficient cross-selling flows that lift average order value even when broader replacement cycles lengthen in the bath fittings and accessories market. These dynamics reinforce the bath fittings and accessories industry's emphasis on complete solutions that align code, safety, and design coherently for residential and commercial upgrades.

By End-User: Residential Dominance Meets Accelerating Commercial Specifications

Residential end-users accounted for 59.62% share of the bath fittings and accessories market size in 2025, supported by steady renovation flows and aesthetic-driven upgrades that favor coordinated finish suites. Commercial specifications are forecast to grow at 7.11% CAGR as hotels, airports, healthcare, and education modernize high-contact fixtures, specify antimicrobial coatings, and expand sensor activation to meet hygiene and safety protocols. Smart fixture pilots continue, especially where predictive maintenance and utilization analytics improve uptime, though certification and support questions can slow scale adoption. Residential programs in China’s renewal pipeline add near-term units equipped with modern fixtures and accessories, while remodel-driven finish upgrades raise transaction values even if volumes stabilize. Collectively, these patterns preserve a residential base while gradually lifting the commercial mix in the bath fittings and accessories market.

Distinct durability and lifecycle requirements set the tone for procurement by the end user. Commercial-grade faucets and valves are engineered for significantly higher cycle counts and service life than residential lines, a difference that directs commercial buyers toward bid processes that emphasize total cost of ownership and maintenance intervals. Residential buyers weigh visual outcomes and finish coordination heavily, driving preference for curated collections and elevated finishes at modest premiums that fit staged remodel budgets. Branded collaborations, such as design-forward launches from leading OEMs, keep drawing attention during kitchen and bath weeks and online reveals, which funnel demand to premium lines and support retailer exclusives. Over time, recurring refresh cycles in hospitality and retail, paired with post-warranty service requirements, should keep the commercial segment’s share on a gradual upward path within the bath fittings and accessories market. The bath fittings and accessories industry, therefore, balances aesthetic preferences at home with performance-driven specification in shared-use facilities, shaping product design and channel strategy.

By Distribution Channel: Specialty Stores Hold Share While Online Surges at 14% CAGR

Specialty stores commanded 38.21% of the bath fittings and accessories market size in 2025, using in-person showrooms and design assistance to convert complex decisions into coordinated carts. Online channels are projected to grow at 14.02% CAGR, helped by major retailers that reported strong e-commerce gains and continue to expand digital configuration, content, and pickup options for bath bundles. As DIY interest rotates between big-box, local hardware, and online platforms, traffic gains at hometown outlets reinforce the role of curated accessories and immediate availability in driving convenience-led share shifts. Mass merchants defend price points with private-label assortments, while specialists lean on consultative selling and exclusive SKUs to defend margins and shopper loyalty. For suppliers, accurate inventory visibility, content quality, and rapid restocking influence digital shelf performance across the bath fittings and accessories market.

Beyond these channels, direct-to-builder programs deliver pre-kitted solutions that reduce on-site errors and installation time, which can justify modest premiums where labor is tight and schedules are compressed. Manufacturer-direct platforms from leading brands capture customer data and offer extended warranties or finish exclusives that help differentiate beyond price, especially for premium remodels. Specialty showrooms counter with click-and-collect, installation workshops, and designer programs that protect consultative value, underscoring the multi-format reality of the bath fittings and accessories market. Channel coexistence is likely to persist as shoppers research digitally but still rely on tactile validation for finish and ergonomics in complex bathroom projects.

Geography Analysis

Asia-Pacific held 32.08% of the bath fittings and accessories market share in 2025, anchored by China’s scaled neighborhood renewal and infrastructure replacements that trigger large, coordinated procurement waves across core fixture categories. The region’s office expansions and mixed-use projects sustain commercial specifications for touchless and antimicrobial features that suit high-traffic spaces, aiding volume consistency between residential and non-residential cycles. Australia’s renovation tilt within residential construction, along with a persistent completion gap versus demand, keeps upgrade activity elevated and directs spend toward bath fixtures and accessory refreshes with visible returns. Southeast Asian demand strengthens as first-time homeowners accessorize builder-grade bathrooms with essential hardware sets, reinforcing the role of value-priced coordinated lines in the region’s growth mix. Together, these conditions sustain the region’s contribution to global volumes and support feature-led upgrades within the bath fittings and accessories market.

South America is projected to expand at 9.18% CAGR through 2031, supported by public and private investments in housing and urban amenities that increase installations across faucets, showers, and coordinated accessories. A growing middle-class steer upgrades from base fittings to thermostatic showers and curated accessory suites, while commercial developments specify longer-life cycles to reduce service trips. North America’s replacement-driven profile remains intact but moderates in line with slower housing turnover, a trend reflected in retailer commentary on softness in certain home-improvement categories. Nearshoring in Mexico supports regional assembly footprints and cross-border logistics advantages for leading brands that serve both domestic and the United States channels. These regional currents underpin a stable but competitive outlook across the bath fittings and accessories market.

Europe benefits from manufacturing upgrades and energy-efficient production investment, including recent capital programs that modernize ceramics, casting, and valve lines for scale and energy savings. Mature Western European markets emphasize design and conservation, while Central and Eastern Europe gain share through hospitality and retail expansions that maintain brand consistency across portfolios. In BENELUX and the Nordics, space efficiency and water-saving features guide specification lists, supporting demand for wall-hung and compact solutions. In the Middle East, GCC programs and local manufacturing partnerships advance sustainable sanitary technologies, reinforcing regional availability and compliance readiness. Across Africa, infrastructure replacement needs offset budget constraints, with value-focused imports serving early-stage urban demand, which keeps the bath fittings and accessories market diversified across price tiers and specification levels.

Competitive Landscape

The bath fittings and accessories market shows moderate concentration, with the top five manufacturers controlling more than 50% of global sales, leaving scope for regional specialists and private-label producers to compete on finishing localization, delivery speed, and project customization. LIXIL streamlined its portfolio by exiting commoditized bathing lines in the United States while expanding smart-fixture capabilities through targeted acquisitions, aligning capital toward higher-margin categories. TOTO expanded United States production capacity and integrated advanced robotics to reduce unit labor and improve assembly precision, reinforcing service levels and cost competitiveness. These moves, combined with a disciplined SKU strategy and tighter integration of supply chains, support pricing power where differentiation is recognized in the bath fittings and accessories market. The balance of scale, innovation cadence, and channel coverage remains the key determinant of share stability across top brands.

Direct-to-consumer entrants leverage social platforms and design influence to reach younger homeowners, often focusing on matte-black finishes and industrial motifs that command premiums but may not meet mass-planogram thresholds. Smart-fixture telemetry solutions add value through monitoring and predictive upkeep, though scaled adoption hinges on clear cybersecurity assurances and integration support that reduce operational risk for commercial operators. Leading brands embed privacy-by-design practices and third-party validations to build trust, positioning connected lines for gradual expansion as standards and best practices mature within the bath fittings and accessories market. Competitive posture favors firms that bridge aesthetics, compliance, and data-enabled maintenance with consistent service-level performance.

Innovation focus areas include water efficiency, installation simplicity, and durable finish chemistries. European leaders emphasize dual-flush actuators, greywater concepts, and high-efficiency spray technologies, while premium brands highlight design collaborations and wellness integration. Patent activity and capex commitments underline the long-term commitment to sustainability and performance gains, which is a differentiator in procurement for large commercial projects. Over the forecast horizon, firms that align product roadmaps with regulatory trends and channel digitalization are best placed to defend share in the bath fittings and accessories market.

Bath Fittings And Accessories Industry Leaders

LIXIL Corporation

Kohler Co.

TOTO Ltd.

Roca Group

Geberit AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: TOTO introduced the Aurora WASHLET+ S7A, a one-piece bidet toilet featuring the company's INTEGRAVITY SYSTEM flush engine that combines gravity and vacuum-assist technology to deliver complete bowl evacuation with 1.0 gallons per flush, targeting LEED-certified commercial projects and California Title 24-compliant residential specifications.

- February 2026: Delta Faucet unveiled six collections at KBIS 2026, including the Cordova and Altado kitchen lines with Touch2O and touchless activation, the Noreau pulldown with ProClean Spray, and the Bonacci and Lineax bath collections, expanding its matte-black and contemporary-architecture portfolios to capture incremental share in the premium remodel segment where finish premiums run 20-30% above chrome equivalents.

- January 2026: Kohler extended its strategic partnership with Cognizant to accelerate AI-driven product development and cloud-based supply-chain optimization, deploying machine-learning algorithms to predict regional demand surges for specific faucet finishes and reduce safety-stock holding costs by 12-15%, according to the company's technology roadmap disclosures.

- January 2026: Kohler expanded its Studio McGee collaboration with the Audrine Kitchen Sink Collection, leveraging the design influencers' 3.2 million Instagram followers to drive direct-to-consumer traffic and bypass wholesale margin structures that typically capture 35-40% of manufacturer list prices.

Global Bath Fittings And Accessories Market Report Scope

A complete background analysis of the market studied, which includes an assessment of the parental market, emerging trends by segments and regional markets, significant changes in market dynamics, and a market overview, is covered in the report. The report also features qualitative and quantitative assessments by analyzing data gathered from industry analysts and market participants across key points in the industry’s value chain.

The Bath Fittings and Accessories Market Report is Segmented by Type (Faucets, Showers, Bathtub, Bathroom Sinks, Towel Rack/Ring, Hook, Paper Holder, Grab Bars, and Other Types), End-User (Commercial, and Residential), Distribution Channel (Mass Merchandisers, Specialty Stores, Online, and Other Distribution Channels), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Faucets |

| Showers |

| Bathtub |

| Bathroom Sinks |

| Towel Rack/Ring |

| Hook |

| Paper Holder |

| Grab Bars |

| Other Types |

| Commercial |

| Residential |

| Mass Merchandisers |

| Specialty Stores |

| Online |

| Other Distribution Channels |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Type | Faucets | |

| Showers | ||

| Bathtub | ||

| Bathroom Sinks | ||

| Towel Rack/Ring | ||

| Hook | ||

| Paper Holder | ||

| Grab Bars | ||

| Other Types | ||

| By End-User | Commercial | |

| Residential | ||

| By Distribution Channel | Mass Merchandisers | |

| Specialty Stores | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and forecast for the bath fittings and accessories market?

The bath fittings and accessories market size is USD 132.27 billion in 2025, expected to be USD 134.59 billion in 2026, and projected to reach USD 146.78 billion by 2031 at 1.75% CAGR.

Which product category leads to growth in bath fittings and accessories?

Faucets hold the largest 2025 share at 33.28% and are also the fastest-growing category with an 11.43% CAGR through 2031 due to touchless adoption and efficiency specifications.

Which region is growing fastest in bath fittings and accessories?

South America posts the fastest trajectory with a projected 9.18% CAGR through 2031, while Asia-Pacific holds the largest 2025 share at 32.08%.

How are sales channels shifting in bath fittings and accessories?

Specialty stores remain the largest at 38.21% share, but online channels are expanding fastest at a 14.02% CAGR as curated kits, and click-and-collect compress purchase cycles.

What end users drive most demand in bath fittings and accessories?

Residential remains the largest with 59.62% in 2025, while commercials are accelerating at a 7.11% CAGR on hygiene-led upgrades and code-driven refresh programs.

Who are the major players in bath fittings and accessories?

The top five are LIXIL, Kohler, TOTO, Roca, and Geberit, together controlling about 55.2% of global sales, with regional specialists competing on localization and speed.

Page last updated on: