Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

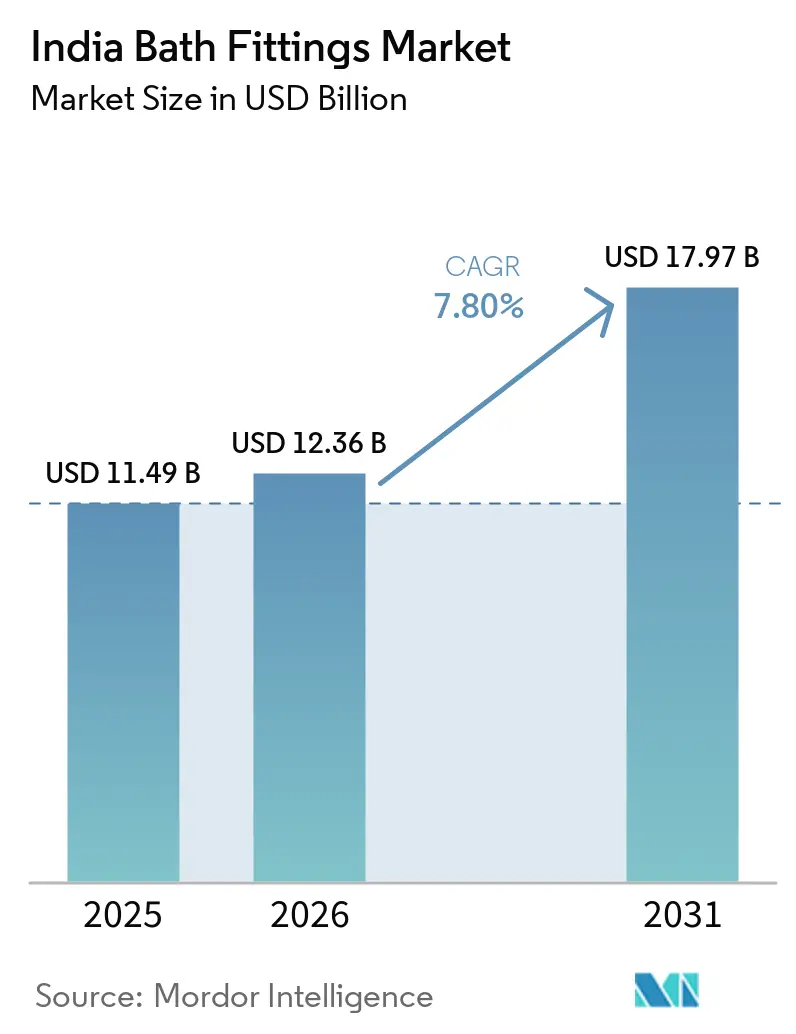

| Base Year Market Size (2025) | USD 11.49 Billion |

| Market Size (2026) | USD 12.36 Billion |

| Market Size (2031) | USD 17.97 Billion |

| Growth Rate (2026 - 2031) | 7.80% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Bath Fittings Market Analysis by Mordor Intelligence

The India bath fittings market size is expected to increase from USD 11.49 billion in 2025 to USD 12.36 billion in 2026 and reach USD 17.97 billion by 2031, growing at a CAGR of 7.8% over 2026-2031. Momentum in the Indian bath fittings market in 2026 is anchored by housing completions under Pradhan Mantri Awas Yojana - Urban (PMAY-U) that include mandated tap and sanitation facilities, which lock multiyear replacement and upgrade cycles into the installed base. Apart from this, hotel construction reached record highs, 906 projects and 118,334 rooms in Q4 2025, which raises order visibility for mid-upscale and luxury fixtures in 2026[1]Hospitality Biz India, “Global Hotel Construction Pipeline Hits Record High at End of 2025: Report,” Hospitality Biz India, hospitalitybizindia.com. Green building programs and water-efficiency standards, including IGBC water savings credits and BIS IS 17650 star ratings, are shaping product specifications toward certified low-flow faucets and showers. Organized brands continue to gain share through exclusive stores and project partnerships, while premiumization trends in metros and tier-2 cities keep average selling prices elevated without overreliance on commodity cost tailwinds.

Key Report Takeaways

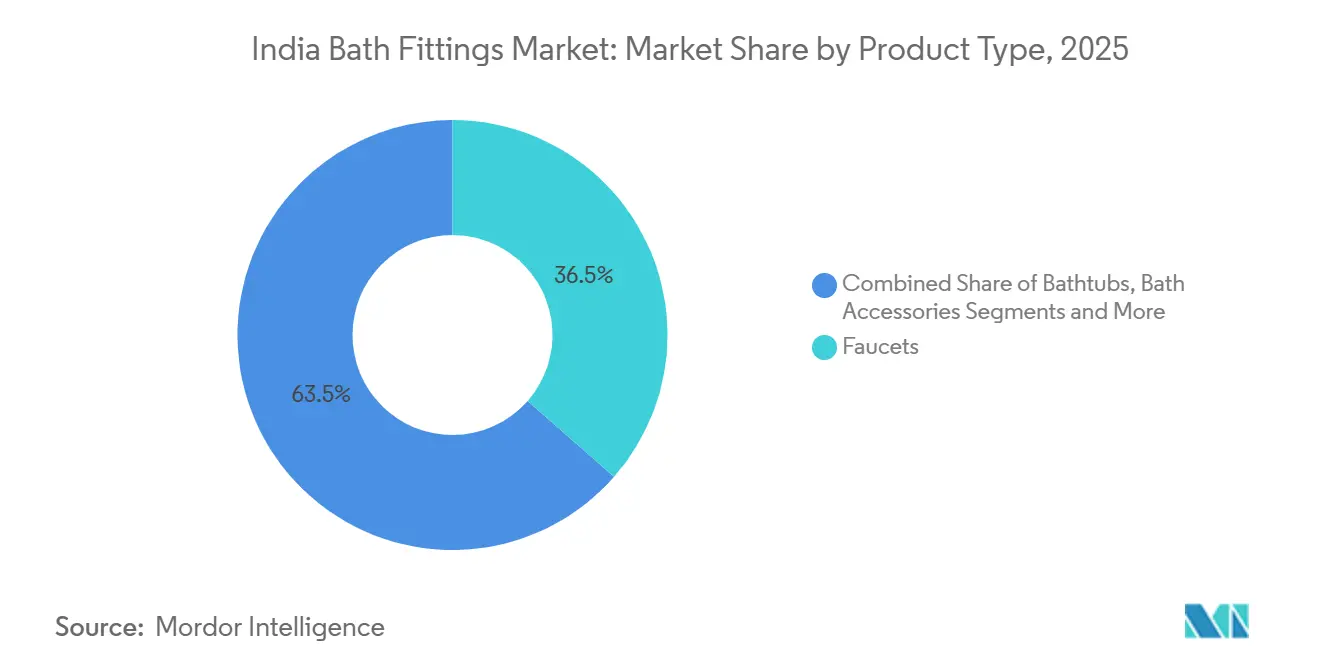

- By product category, faucets led with 36.45% of the India bath fittings market share in 2025, while bathtubs and spa fittings are projected to record the fastest 7.34% CAGR through 2031.

- By market type, the organized segment held 58% of the India bath fittings market share in 2025, while organized brands are projected to grow at an 8.58% CAGR through 2031.

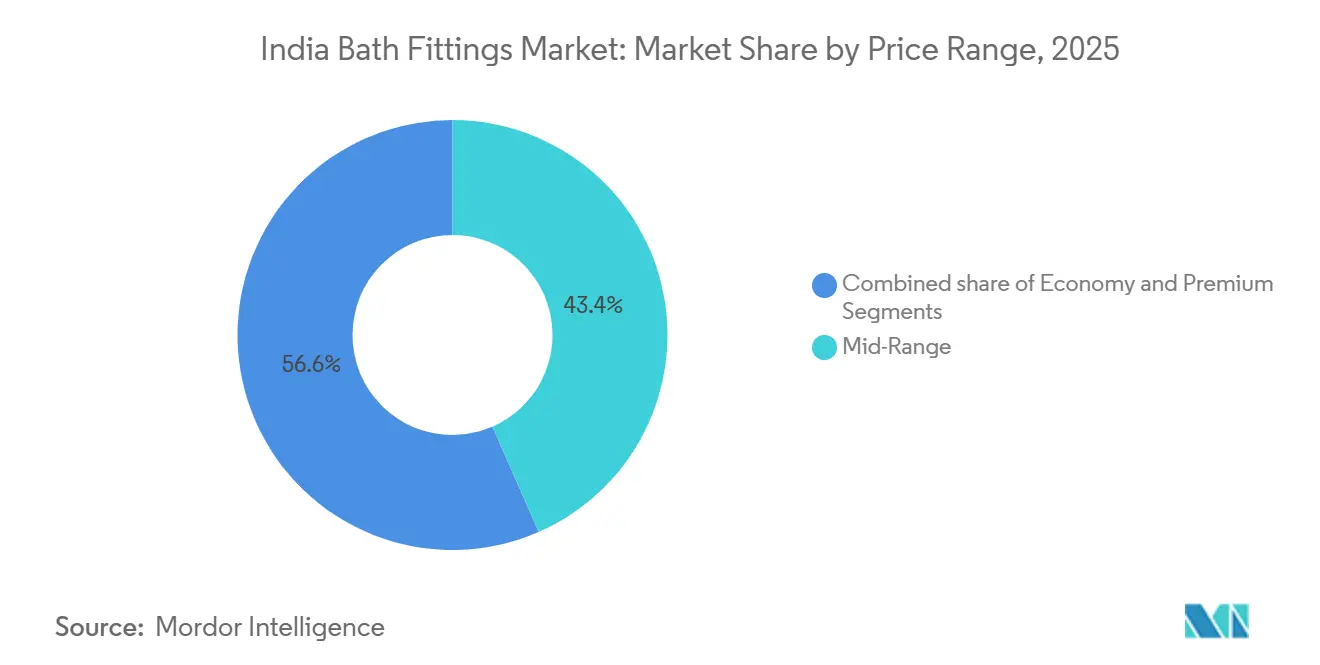

- By price range, the mid-range segment accounted for 43.44% of the India bath fittings market share in 2025, while the premium segment is projected to grow at the fastest 6.94% CAGR through 2031.

- By end user, the residential segment held 63.35% of the India bath fittings market share in 2025, whereas the commercial segment is projected to grow at an 8.34% CAGR through 2031.

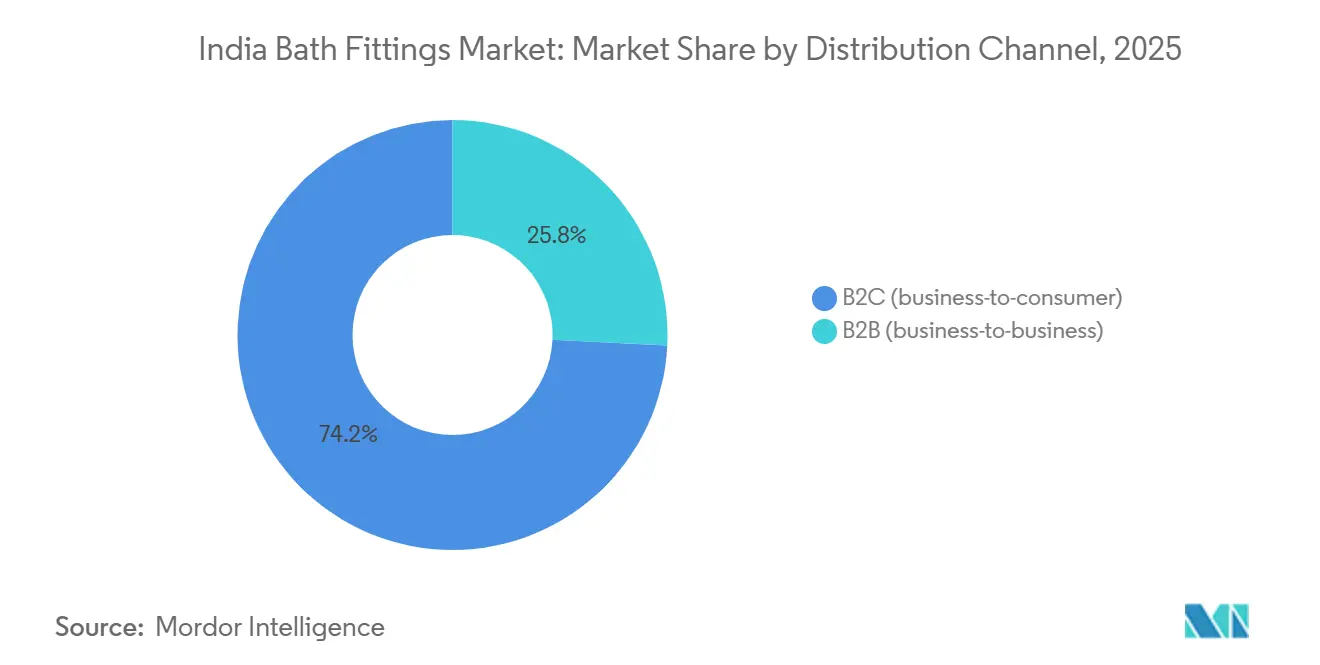

- By distribution channel, B2C channels retained 74.23% of the India bath fittings market share in 2025, while B2B project sales are projected to grow at an 8.72% CAGR through 2031.

- By geography, West India accounted for 30.23% of the India bath fittings market share in 2025, while South India is projected to lead growth at a 7.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Bath Fittings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PMAY-led urban housing completions sustain fixture demand | +1.2% | National, with the highest delivery concentration in Andhra Pradesh, Gujarat, and Chhattisgarh | Medium term (2-4 years) |

| Premiumization and aesthetic upgrades in bathrooms | +1.5% | Metros and tier-1 cities, spill-over to tier-2 hubs | Short term (≤ 2 years) |

| Hospitality and healthcare project pipeline | +1.1% | National, with early gains in Guwahati, Bengaluru, Mumbai, Hyderabad | Medium term (2-4 years) |

| Green building codes (IGBC/GRIHA/NBC) specifying low-flow fixtures | +0.9% | Primarily, metros and state capitals are mandatory for many public buildings. | Long term (≥ 4 years) |

| BIS star-rating (IS 17650) nudges low-flow faucets and showers | +0.7% | National phased rollout under AMRUT 2.0 | Long term (≥ 4 years) |

| Shift to organized players in tier-2 and tier-3 cities | +1.3% | Surat, Hyderabad, Kolkata, Bengaluru, Ahmedabad, Pune | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PMAY-Led Urban Housing Completions Sustain Fixture Demand

PMAY Urban crossed 96.65 lakh completed homes by February 2026, which set a structural floor for fixture demand as each eligible unit requires basic tap and sanitation infrastructure[2]The Times of India, “PMAY Urban scheme nears 1 crore completed homes; Andhra, Gujarat lead the drive,” The Times of India, timesofindia.indiatimes.com. The next leg of demand will track beneficiary occupancy and handover timelines, since final utility connections and essential services determine when installation orders convert at scale in individual projects. Andhra Pradesh has been among the highest delivery states, which supports sustained volumes of faucets, showers, cisterns, and accessories in local procurement pipelines across 2026. PMAY U 2.0 targets an additional one crore homes by 2029, with new sanctions already underway as of mid 2025, which extends visibility for the Indian bath fittings market into the late 2020s. The PMAY framework links closely with sanitation and water conservation reforms under AMRUT 2.0 and Bharat Tap, which together are nudging municipal procurements toward certified water-efficient fixtures over the medium term. As these programs scale, the Indian bath fittings market benefits from long cycle replacement demand due to maintenance intervals and upgrades in high-use public and affordable housing assets.

Premiumization and Aesthetic Upgrades in Bathrooms

Premium features are moving beyond metros as developers and homeowners in tier-2 cities adopt spa-style showers, concealed diverters, and coordinated finish suites that elevate perceived value in new projects and renovations across the Indian bath fittings market. Lixil’s plan to expand from 350 to 500 stores highlights how funnel depth is growing outside top metros, and large B2B orders often span thousands of bathrooms per high-rise development, which keeps premium lines visible and available in local markets[3]ETRetail, “Lixil bets on tier-2 demand and B2B push to scale in India market,” The Economic Times, retail.economictimes.indiatimes.com. Hindware’s focus on premiumization through Experience Centers and a three-tier brand architecture keeps price ladders clear for consumers and architects who want sensor taps, rain showers, and smart controls in curated combinations. Premium growth also reflects higher awareness of water-efficient and sustainable products as IGBC credits and BIS star ratings become part of design briefs in urban projects. As portfolios skew to touchless and low-flow products, users report better hygiene and lower water bills, which reinforces premium uptake through word of mouth and developer specifications in 2026. These dynamics continue to separate India’s path from commodity-led cycles as premiumized SKUs sustain value creation for the India bath fittings market through 2031.

Hospitality and Healthcare Project Pipeline

India’s hotel pipeline reached 906 projects and 118,334 rooms by Q4 2025, which signals steady project to procurement conversion for shower systems, mixers, and sensor taps through 2026 and beyond. Independent forecasts indicate India will continue to lead Asia-Pacific excluding China in new hotel openings through 2026, which keeps multi-year volume visibility high for organized suppliers that can standardize packages by chain scale and brand tier. Lemon Tree’s planned 300-room Premier property in Guwahati sits within a broader mixed-use hospitality and healthcare development, with a project cost of INR 800 crore (USD 96.4 million) and a fixture scope that spans guest rooms and public areas. Ambuja Neotia’s INR 700 crore (USD 84.3 million) integrated hospital and hotel project in Guwahati adds a healthcare demand layer in the same hub, where hospitals require touchless and antibacterial solutions alongside water saving targets that lower lifetime operating costs. A typical 200-room mid-upscale hotel installs several hundred fixtures, which translates into procurement packages that reward brands capable of on-time delivery, site support, and compliance documentation at scale. As more chains finalize brand standards for low flow performance and touchless operation, suppliers that cover full bathroom suites gain an advantage in repeat orders across the Indian bath fittings market.

Green Building Codes (IGBC/GRIHA/NBC) Specifying Low-Flow Fixtures

IGBC water-efficiency pathways reward projects that achieve 8% to 24% savings against baseline flow and flush rates, which directs architects to specify efficient faucets, showers, and dual-flush cisterns across commercial and high-end residential buildings. GRIHA’s water benchmarks add complementary thresholds that support pressure-independent regulators and coordinated fittings that stabilize flows across diverse building conditions. BIS SP 73 encourages standardized development and building regulations, which now guide many state and urban local bodies in adopting water-efficient plumbing and aligning tender specs with national standards. The Bharat Tap initiative under AMRUT 2.0 provides an implementation pathway for cities to prefer star-rated water-efficient fixtures in public buildings, which raises familiarity and trust among contractors and facility managers. As these codes spread, the Indian bath fittings market shifts from feature-led selling to compliance-led specifications that prioritize proven flow rates and lifecycle performance. The effect compounds in 2026 as corporate tenants and public agencies set minimum star-rating thresholds in new fitouts that then cascade into residential retrofit preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance costs for chrome and nickel plating, ETP, and permits | -0.8% | National, affecting small to mid-scale manufacturers without an integrated ETP. | Medium term (2-4 years) |

| Input cost volatility, brass and plating chemicals, and energy | -1.1% | National, with impact concentrated in Gujarat and Tamil Nadu manufacturing hubs | Short term (≤ 2 years) |

| Grey and unorganized price competition in value tiers | -0.6% | Primarily Gujarat, secondary effects in tier-3 markets with low organized retail penetration | Short term (≤ 2 years) |

| Emerging water-efficiency codes raising spec thresholds | -0.4% | Urban local bodies under AMRUT 2.0, faster adoption in metro regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compliance Costs for Chrome and Nickel Plating, ETP, and Permits

Compliance costs are rising for electroplating, including requirements for effluent treatment plants and adherence to discharge norms for chromium and nickel, which raises fixed and recurring costs for small and mid-scale units that lack integration[4]Netsol Water, “CPCB Guidelines for Electroplating Industry Effluent Treatment Plants,” Netsol Water, netsolwater.com. Environmental compliance places pressure on units that previously competed on price alone, which narrows the cost gap with organized players that amortize these systems across larger volumes. The effect is more acute for value-tier SKUs where price ceilings are strict, which reduces flexibility to pass through higher treatment and monitoring costs to channel partners. As state pollution control boards and urban local bodies step up oversight in 2026, frequent audits and documentation add administrative load to production schedules and delivery commitments. These requirements dampen the speed at which sub-scale manufacturers can respond to tender-led demand that prefers companies with proven compliance records.

Input Cost Volatility, Brass and Plating Chemicals, and Energy

Input cost volatility remains a headline risk as brass, nickel, and energy costs move with global and domestic conditions, which can squeeze margins in value tiers during upswings and unsettle inventory planning. Brass scrap prices fell 2.84% in mid-February 2026, yet history shows sharp quarterly swings that complicate pricing ladders for faucets and shower bodies when long-term contracts are limited. Nickel salts and plating chemicals follow their own cycles, which affects finishing costs at the same time that water and energy charges trend differently across states. Organized suppliers can cushion some volatility through procurement scale and design standardization, but sudden spikes still compress EBITDA if channel prices cannot adjust in time in competitive micro-markets. These challenges reinforce the value of project-based sales that lock volumes and pricing for longer periods, which helps stabilize throughput in the India Bath Fittings market during input-cost swings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wellness Pivot Lifts Bathtub Demand

Faucets accounted for 36.45% of the Indian bath fittings market size in 2025, and the product mix shows wellness-driven momentum as bathtubs and spa fittings are projected to grow at a 7.34% CAGR through 2031. Faucets remain volume anchors across new builds and renovations, and adoption rises when brands add touchless activation and durable finishes that align with both hygiene and aesthetic preferences in urban households. Shower systems are bifurcating between rain-shower formats in premium projects and efficient handheld units in mid-tier and public buildings that prioritize three-star performance under BIS standards. Low-flow compliance at 6.8 liters per minute for three-star shower heads and optimized aerators for basin taps are influencing the specification sheets on Grade-A offices and hotels, which then filter into residential preferences over time. Bathtubs and spa fittings, while having a smaller base, benefit from developers positioning master bathrooms as wellness spaces in premium apartments and luxury hotels, which pulls coordinated accessory sales along with core fixtures in the Indian bath fittings market.

Developers show homes and hospitality brand standards are normalizing premium shower columns, thermostatic mixers, and concealed diverters, which elevate buyer expectations during home selection and upgrade cycles. Efficient dual-flush cisterns and coordinated accessories are becoming baseline in green-focused projects, as IGBC and GRIHA credits translate into practical checklists for contractors and MEP consultants. Branded accessory sets bundled with faucets and showers are increasing average ticket sizes as homeowners prefer matched finishes, which reduces piecemeal purchases that often lead to fit and finish issues. The Indian bath fittings market is also seeing a steady shift to products tested for pressure and flow stability, which support reliable performance across variable municipal water conditions in 2026. Together, these forces keep product innovation tied to both wellness and compliance outcomes, which strengthens category resilience through the forecast period.

By Market Type: Organized Segment’s Margin Shield

The organized segment held 58% share in 2025 and is projected to grow at an 8.58% CAGR through 2031, which outpaces the unorganized segment and reflects consistent gains in brand-led distribution and project credentials. Exclusive stores now act as specification hubs for architects and developers, where brands demonstrate synchronized suites of faucets, showers, and accessories with documented flow and efficiency metrics under BIS and IGBC norms. Multiyear project frameworks for offices, hotels, and institutional buildings reinforce organized suppliers’ advantages in service, spare parts availability, and installation support across multiple cities. New brand entries confirm the market’s capacity to absorb premium tiers, as seen with Moen’s partnership-led entry and Experience Center in New Delhi that targets discerning buyers and project specifiers.

Production investments underline confidence in the India bath fittings industry’s demand runway, including Roca India’s INR 400 crore (USD 48.2 million) program in Tamil Nadu to enhance process automation and expand fittings capacity, and Hansgrohe’s plan to expand assembly capacity with a 2030 horizon for scale. As water-efficiency codes deepen, organized brands that maintain broad certification coverage and strong post-installation support are likely to attract more project-based orders than unorganized competitors that face rising compliance and documentation hurdles. These advantages compound in 2026 as public and private tenders incorporate star ratings and installation assurance requirements, which keep the organized trajectory ahead of the broader Indian bath fittings market.

By Price Range: Luxury Tier Splits Mid-Range Volume

The mid-range segment accounted for 43.44% share in 2025, reflecting stable replacement cycles and new-home installations in urban and fast-growing tier-2 markets that favor branded chrome finishes and reliable cartridge technologies, and the Luxury / Premium segment is projected to grow at an 6.94% CAGR through 2031. Premium adoption is the fastest-growing in value terms, supported by spa-like showers, concealed plumbing, and sensor-based controls that map to both wellness and hygiene priorities in high-end homes and hotels. Premium lines that also meet low-flow thresholds strengthen positioning in projects that pursue IGBC and GRIHA credits, which aligns aesthetics with measurable water savings. Brands continue to bridge the gap between mid-range and premium through curated bundles, which reduce friction in consumer decision-making and raise in-bathroom coordination across finishes and geometries.

Project procurement further accelerates premium presence because developers can standardize suites across 200 to 300 rooms in a single contract, which expands visibility of premium specifications among contractors and installers who then carry those preferences into residential retrofit work. As code compliance becomes a requirement rather than an option for many public and commercial buildings, premium faucets and showers that already meet BIS star ratings and IGBC thresholds integrate smoothly into tender-led frameworks. The premium path in 2026 also reflects the role of Experience Centers, where brands offer design consultations that help buyers envision full spaces and future-proof investments through warranty and service coverage. This approach anchors sustained value creation even as mid-range volumes carry the largest base of the India Bath Fittings market.

By End User: Commercial’s B2B Leverage

The residential segment held 63.35% share in 2025, while commercial is the faster-growing end user at an 8.34% projected CAGR through 2031 as Grade-A offices, hotels, and healthcare facilities emphasize standardized, low-flow, and touchless fixtures in new builds and upgrades. The India bath fittings market size for commercial end users is projected to expand at 8.34% CAGR between 2026 and 2031 as hotel openings and corporate expansion programs convert design intent into procurement packages that run over multiyear build cycles. A single office tower or 200- to 300-room hotel can aggregate volumes across faucets, showers, cisterns, and public-area sensor taps, which supports predictable throughput for brands with installation and warranty coverage across cities. Healthcare facilities add infection-control requirements that raise the share of touchless fittings and antibacterial surfaces in procurement, which lock in technology choices for subsequent maintenance cycles.

Residential demand remains broad-based due to housing completions and steady renovation cycles in older urban stock, and homeowners increasingly prefer star-rated fittings as installers become familiar with certified SKUs through public and commercial projects. As retrofit activity rises in 2026, demand for coordinated accessories grows alongside core fixtures because matched finishes and geometries support design cohesion without repeated store visits. In hotels, fixture budgets scale by chain scale, yet all segments are moving toward auditable performance standards and installation quality, which keeps branded suppliers central to high-occupancy properties. These patterns keep commercial growth ahead of residential in percentage terms, while residential sustains the largest base of the Indian bath fittings market in 2026.

By Distribution Channel: B2B’s Margin Paradox

B2C channels held 74.23% share in 2025, while B2B project sales are projected to grow at 8.72% CAGR through 2031 compared with 8.34% in retail, as developers procure bundled low-flow and touchless suites that meet code and brand standards in one award. Exclusive brand stores act as CX-led showrooms for B2C journeys and as specification venues for architects, supported by expanding footprints such as Hindware’s 540 stores and new Experience Centers that help drive category upgrades. Online channels raise discovery and consultation options for homeowners and small contractors, while complex installations still favor on-ground brand and service networks that ensure reliable after-sales outcomes. On the B2B side, large orders lock volumes and price terms for long stretches, which supports factory scheduling and inventory planning without frequent price resets.

CERA’s Style Studios in Kochi and other cities show how showrooms serve not just retail walk-ins but also professional communities that want to review full-room concepts and documentation in one place before finalizing specifications. New global entrants such as Moen are also opting for Experience Centers that complement existing multibrand networks, which indicates a maturing ecosystem where buyers expect immersive selection and robust service. The Indian bath fittings market benefits from these parallel tracks because both retail and projects build category literacy that then sustains replacement and upgrade cycles over years rather than quarters. In 2026, the balance of channels continues to tilt toward models that combine design guidance, code compliance, and assured installation quality.

Geography Analysis

West India accounted for 30.23% of the India bath fittings market size in 2025, supported by Mumbai’s high-rise redevelopment and Gujarat’s supply clusters that feed organized and unorganized production bases. South India is projected to lead the regional growth trajectory at a 7.82% CAGR through 2031, which reflects Bengaluru’s premium housing pipeline and robust commercial and hospitality activity in Chennai, Hyderabad, and Kochi. North India remains a large demand center across Delhi-NCR and Uttar Pradesh, where PMAY-Urban sanctions and completions underpin volume tiers in faucets and showers alongside upscale demand in Gurugram and Noida. East and Northeast India hold a smaller share but show rising hospitality-led demand, especially in Guwahati, which is anchoring integrated healthcare and hotel projects that require branded, low-flow fixtures across guest, patient, and public areas. These regional contrasts keep procurement patterns varied across the Indian bath fittings market in 2026 as capital flows into both residential and commercial assets.

In West India, developer consolidation and brand standards in commercial projects support steady demand for certified shower systems, concealed cisterns, and touchless public-area fittings, which favors organized brands with strong service coverage. South India’s lead in hotel pipelines and tech-driven office expansion creates scale for project-based procurement that can lock orders across multiple properties in the same city, which improves forecast reliability for suppliers. North India’s demand profile includes premium residential pockets that prefer coordinated finish suites, while PMAY-linked volumes continue to support value tiers in faucets and showers that focus on function and code alignment. East and Northeast India are leveraging connectivity improvements that attract hotel brands and healthcare projects, which together increase the share of touchless fixtures and low-flow installations in project specifications.

Developer and brand store footprints are expanding fastest in a subset of tier-2 cities, where Lixil and others are building points of presence that reduce selection friction and accelerate delivery cycles. The shift toward IGBC and BIS-aligned specifications begins in public and commercial buildings in key metros and then radiates into residential retrofits as installers gain confidence with certified SKUs in large projects. The Indian bath fittings market benefits as more municipalities and state agencies integrate low-flow requirements into tender documents, which creates uniformity in evaluation criteria and rewards suppliers with broad certification coverage. These trends point to continued regional asymmetry, yet the combined effect is a national move toward performance-led procurement in 2026.

Competitive Landscape

The Indian bath fittings market is moderately concentrated within the organized segment, where leading brands sustain premium positioning through exclusive stores, project references, and broad certification portfolios that meet BIS and IGBC criteria. Capacity additions and local assembly investments affirm long-term commitment, including Roca’s process automation and fittings expansion in Tamil Nadu at INR 400 crore (USD 48.2 million) and Hansgrohe’s plan to scale assembly lines through the end of the decade to support faster delivery and broader product coverage. New global entrants, such as Moen’s collaboration with Bathline Acquaviva and the opening of an Experience Center in New Delhi, underscore confidence that India can absorb premium and smart fixture supply with robust retail and installation support. These moves build on a rising hospitality pipeline and municipal water efficiency reforms that together uphold healthy demand visibility through 2031.

White space opportunities are most visible in retrofit cycles for Grade A commercial assets and public buildings, where pre-standard installations can be replaced with BIS star-rated and IGBC-aligned fixtures to achieve measurable water savings and compliance outcomes. Organized suppliers with full range suites and trained installer networks can execute high velocity change outs with predictable timelines and water saving documentation, which lowers operational risk for asset owners. On the hospitality side, multi-property pipelines help brands negotiate three year supply and service frameworks that standardize bathrooms across projects and accelerate post opening maintenance cycles. Suppliers that integrate IoT-ready components in faucets and showers position themselves for future retrofit mandates and analytics-led maintenance preferences, especially in high-occupancy commercial and hospitality buildings.

Strategy patterns show parallel plays at the top and middle of the price pyramid, where incumbents protect premium margins with design-forward collections and expand reach with curated mid-range bundles that emphasize code compliance and service assurance. Retail networks and Experience Centers double as design labs and training hubs for installers, which improves fit and finish outcomes and reduces post installation issues for end users. Parallel to bathroom fittings, adjacent kitchen fixtures and sinks are attracting capacity investments, as seen in Carysil’s INR 500 crore (USD 60.2 million) program to scale production, which supports integrated home solutions that share distribution and installation channels with bathroom categories. In 2026, these strategies will keep the India bath fittings market competitive and innovation-focused while strengthening compliance and service moats that matter in tender-led growth.

India Bath Fittings Industry Leaders

Jaquar Group

CERA Sanitaryware

Hindware

Roca Parryware

Grohe India

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: In Kochi, CERA Sanitaryware launched a company-owned CERA Style Studio display center showcasing luxury sanitaryware and bathroom solutions such as Senator and CERA Luxe.

- March 2026: Hansgrohe India announced plans to expand assembly line capacity sixfold by 2030, with capacity expected to nearly double in 2026 compared to the previous year. A new initiative for direct sourcing of raw materials, components, and finished goods globally is set to begin by April 2026, improving efficiency and market responsiveness. This investment reflects Hansgrohe's ambition to become one of the group's top five global subsidiaries.

India Bath Fittings Market Report Scope

The India bath fittings market comprises a wide range of sanitary and plumbing fixtures designed to enhance functionality, hygiene, and aesthetics in residential and commercial bathrooms.

The India bath fittings market is segmented by product type, market type, price range, end user, distribution channel, and geography. By product type, the market is segmented into faucets, showerheads & systems, bathtubs, and other bath accessories and fittings. By market type, the market is segmented into organized and unorganized segments. By price range, the market is segmented into economy, mid-range, and premium categories. By end user, the market is segmented into residential and commercial sectors. By distribution channel, the market is segmented into B2C and B2B (direct & project sales). The B2C segment is further divided into multibrand stores, exclusive stores, online, and other distribution channels. By geography (India), the market is segmented into North India, South India, West India, and East & Northeast India. The report offers the market size in value terms in USD for all the above-mentioned segments.

By Product Type

| Faucets |

| Showerheads & Systems |

| Bathtubs |

| Other Bath Accessories and Fittings |

By Market Type

| Organized |

| Unorganized |

By Price Range

| Economy |

| Mid-Range |

| Premium |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C | Multibrand Stores |

| Exclusive Stores | |

| Online | |

| Other Distribution Channels | |

| B2B (Direct & Project Sales) |

By Region (India)

| North India |

| South India |

| West India |

| East & Northeast India |

| By Product Type | Faucets | |

| Showerheads & Systems | ||

| Bathtubs | ||

| Other Bath Accessories and Fittings | ||

| By Market Type | Organized | |

| Unorganized | ||

| By Price Range | Economy | |

| Mid-Range | ||

| Premium | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C | Multibrand Stores |

| Exclusive Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (Direct & Project Sales) | ||

| By Region (India) | North India | |

| South India | ||

| West India | ||

| East & Northeast India | ||

Key Questions Answered in the Report

What is the current size and 2031 outlook for the India Bath Fittings market?

The India bath fittings market size is expected to increase from USD 11.49 billion in 2025 to USD 12.36 billion in 2026 and reach USD 17.97 billion by 2031, at a 7.8% CAGR over 2026–2031.

Which product categories are leading the growth in the India Bath Fittings market in 2026?

Faucets hold the largest share at 36.45% while bathtubs and spa fittings are projected to grow fastest at 7.34% through 2031 as wellness-focused renovations and hotel standards spread.

How are green building codes and BIS star ratings shaping specifications in India Bath Fittings?

IGBC and GRIHA credits reward measurable water savings, and BIS IS 17650 sets star-rated flow thresholds that push projects toward low-flow faucets and showers, which standardize specs in public and commercial buildings.

Which channels are growing faster in India Bath Fittings during 2026?

B2C retained the largest share at 74.23% in 2025, while B2B sales are projected to grow at 8.72% CAGR through 2031 as developers lock in bundled, code-compliant suites for hotels, offices, and public assets.

What regions show the strongest momentum in India Bath Fittings through 2031?

West India leads by share with 30.23% of 2025 revenues, while South India is projected to lead growth at a 7.82% CAGR through 2031, on the back of premium housing and hotel pipelines in Bengaluru, Chennai, Hyderabad, and Kochi.

What risks can impact margins in the India Bath Fittings market?

Brass and plating chemical volatility, along with compliance costs for electroplating and water-efficiency requirements, can compress margins in value tiers when price pass-through is constrained.

Page last updated on: