Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

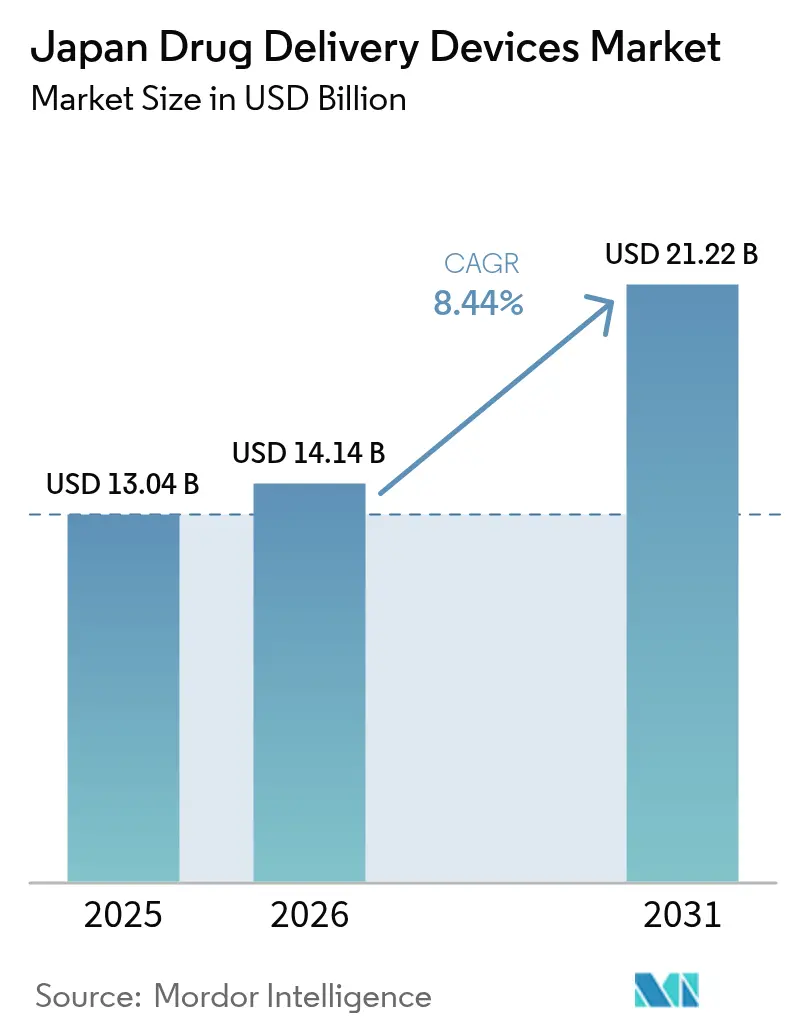

| Base Year Market Size (2025) | USD 13.04 Billion |

| Market Size (2026) | USD 14.14 Billion |

| Market Size (2031) | USD 21.22 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Drug Delivery Devices Market Analysis by Mordor Intelligence

The Japanese drug delivery devices market size was valued at USD 13.04 billion in 2025 and estimated to grow from USD 14.14 billion in 2026 to reach USD 21.22 billion by 2031, at a CAGR of 8.44% during the forecast period (2026-2031). The primary growth drivers are the country’s unprecedented aging population, the increasing prevalence of chronic diseases, and policy shifts that favor self-administration technologies. Injectable products currently dominate usage patterns; yet, rapid gains in implantables and smart-connected formats signal a broader pivot toward sustained-release and data-enabled care. The government’s fast-track pathway for Software as a Medical Device (SaMD) injectors, combined with Japan's National Health Insurance (NHI) reimbursement of wearables, is accelerating the time-to-market for next-generation devices. Supply-side innovation is also stimulated by a noticeable “drug-loss” gap, where more than 80 therapies remain unapproved in Japan, opening opportunities for firms that can navigate complex regulatory checkpoints. Heightened competition, however, collides with workforce shortages and regional care disparities, ensuring continued demand for automation and home-based solutions.

Key Report Takeaways

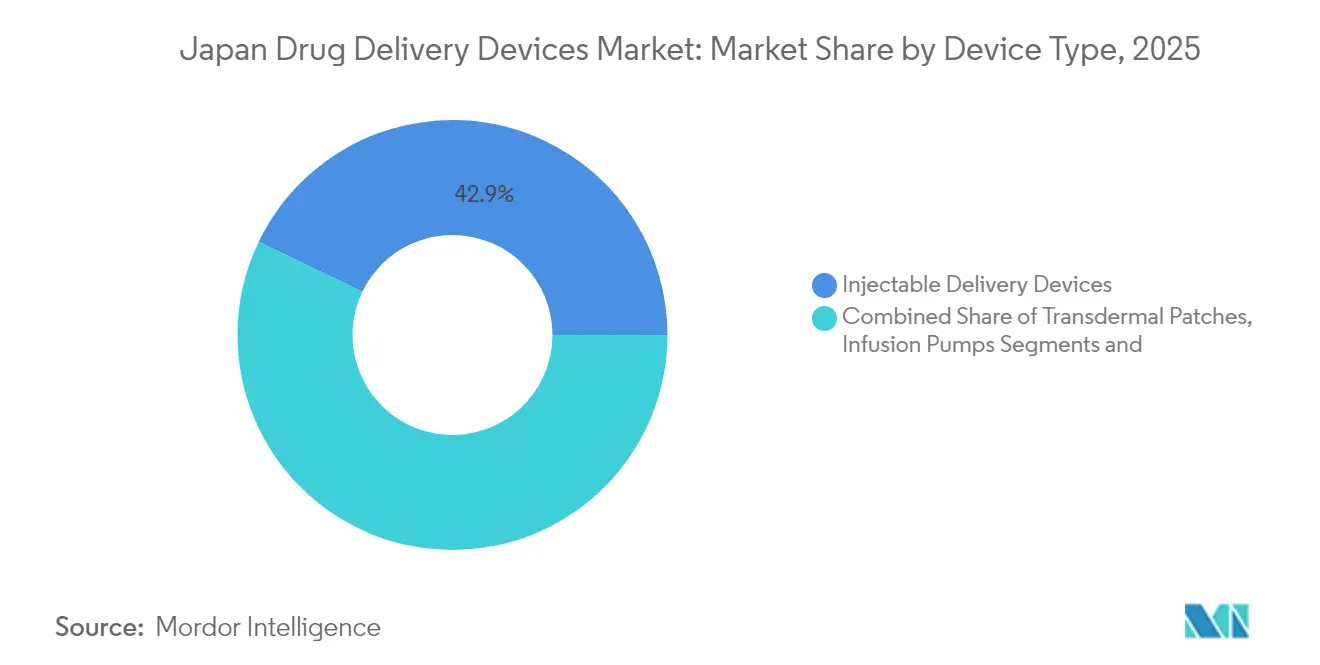

- By device type, injectable systems led with 42.87% of Japan's drug delivery device market share in 2025, while implantable devices are projected to grow at a 10.22% CAGR through 2031.

- By route of administration, injectable formats accounted for a 55.96% share of the Japan drug delivery devices market size in 2025; inhalation pathways are expected to advance at a 8.92% CAGR to 2031.

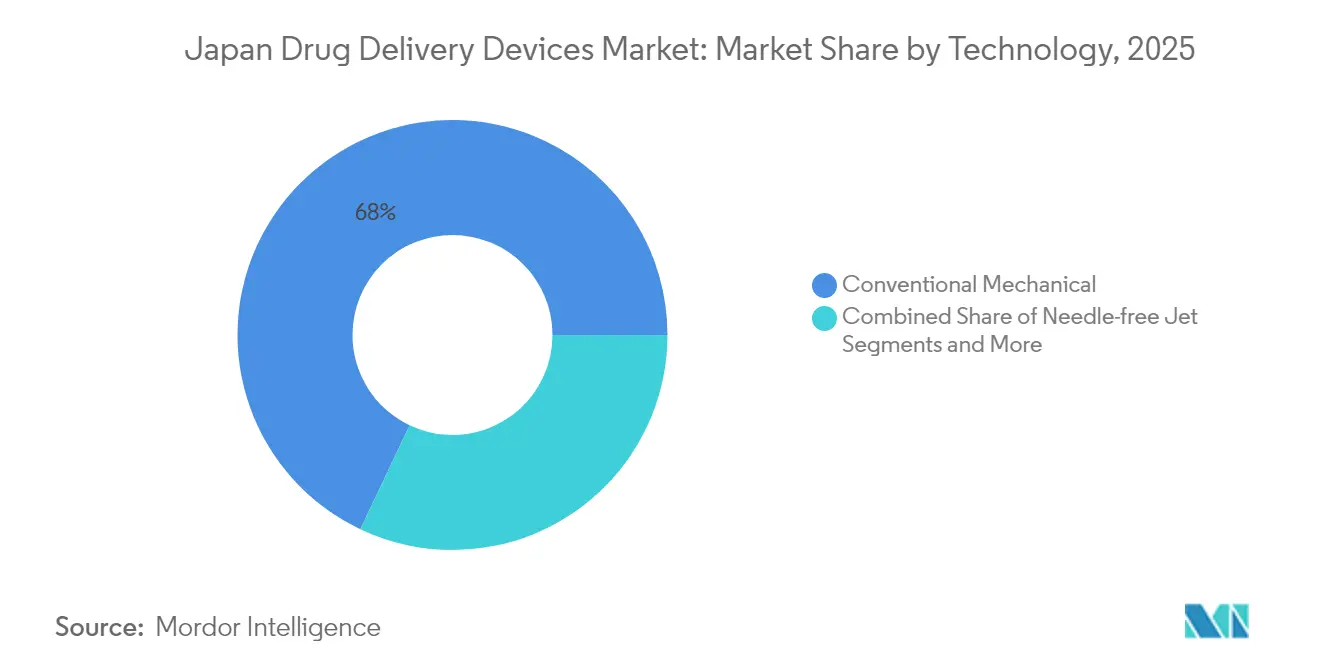

- By technology, conventional mechanical products held 67.95% revenue share in 2025, whereas electronic / smart devices are on track for 9.25% CAGR expansion to 2031.

- By application, diabetes accounted for a 28.35% share of the Japanese drug delivery devices market in 2025, but oncology is expected to post the fastest growth rate of 10.12% through 2031.

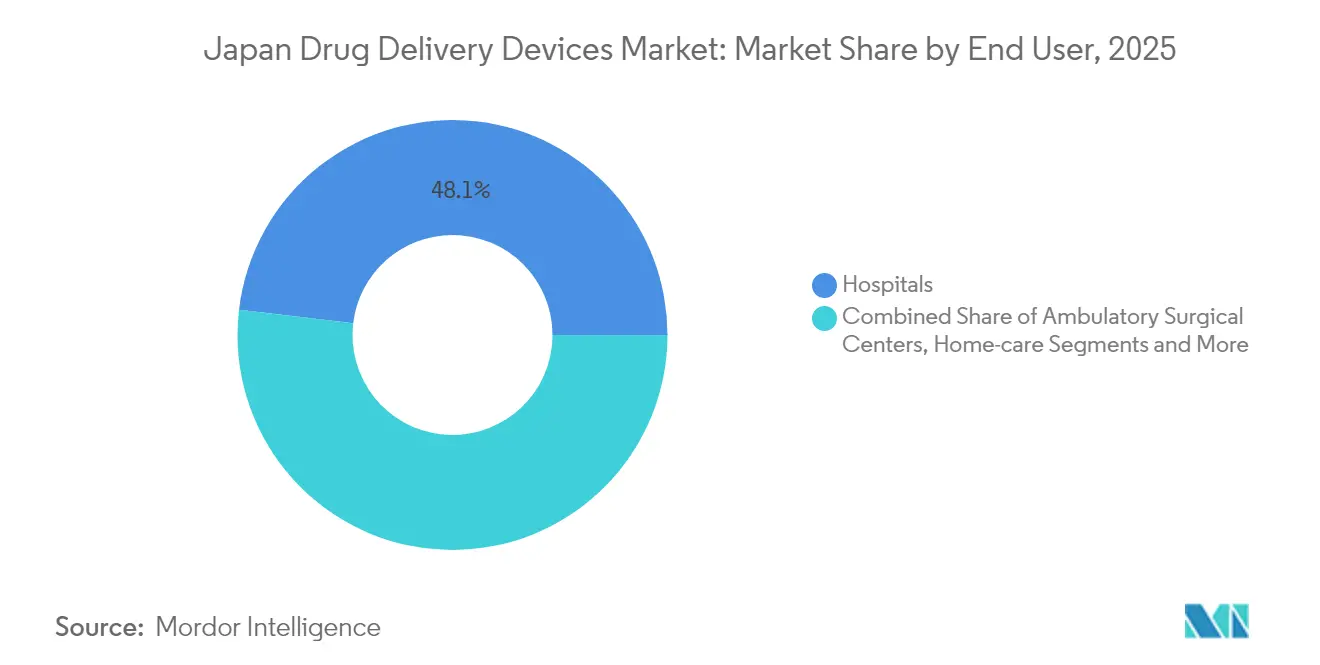

- By end user, hospitals retained 48.12% share in 2025, yet home-care settings are forecast to climb at a 11.55% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Drug Delivery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High burden of chronic diseases and aging population | +3.2% | National, stronger in urban hubs | Long term (≥ 4 years) |

| Government push for home-based care (NHI reimbursement for wearables) | +2.1% | National, early in Tokyo, Osaka, Nagoya | Medium term (2-4 years) |

| Fast-track approval pathway for SaMD-enabled smart injectors | +1.8% | National | Short term (≤ 2 years) |

| Technological advancements in drug delivery devices | +1.7% | Innovation centers | Medium term (2-4 years) |

| Shortage of medical professionals | +1.6% | National, strongest in rural prefectures | Medium term (2-4 years) |

| Rise of biosimilars needing novel formats | +1.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Burden of Chronic Diseases and Aging Population

Japan counts 24 million older adults managing multiple chronic conditions. Device designers therefore prioritise simplified interfaces, reduced dosing frequency, and safety locks that accommodate limited dexterity and cognitive changes. Controlled-release implants that exploit senescence biomarkers are gaining R&D attention, positioning local firms to capture export opportunities for geriatric-friendly solutions.[1]Yoshihara K. & Horiguchi M., “Drug Delivery Strategies for Age-Related Diseases,” International Journal of Pharmaceutics, sciencedirect.com The demographic pressure will remain structural, supporting steady demand well beyond the forecast window.

Government Push for Home-based Care (NHI Reimbursement for Wearables)

Insurance coverage for remote consultations and selected wearables fuels investment in self-administration platforms. Yet reimbursement for disease-specific digital rehab remains incomplete, creating a patchwork that innovators must navigate. Urban uptake is strong, while rural regions still lack robust home-care staffing and IT backbones, tempering near-term volume gains.[2]Sun X. et al., “Home Healthcare Resources and Regional Disparities,” Journal of General Internal Medicine, link.springer.com Even so, policy direction is clear: shift care from hospitals to homes to offset staff shortages.

Fast-track Approval Pathway for SaMD-Enabled Smart Injectors

Revisions to the PMD Act introduced priority reviews for digital combination products, cutting regulatory lead times for connected autoinjectors and pumps.[3]PMDA, “Regulatory Science Strategy and Fast-Track Guidelines,” Pharmaceuticals and Medical Devices Agency, pmda.go.jp Formal SaMD guidelines issued in 2023 clarify performance benchmarks, giving developers greater certainty on evidence packages. These measures aim to secure market access for novel devices that support real-time adherence monitoring and data feedback, reinforcing Japan as a test-bed for digital therapeutics.

Technological Advancements and Shortage of Medical Professionals

Artificial intelligence and robotics are entering routine care to counter workforce gaps, with policymakers framing technology as a productivity lever. Qualitative interviews during the COVID-19 period confirmed strong interest in wearables among both clinicians and seniors, suggesting high receptivity to automated drug administration add-ons. Autonomous delivery platforms lower nursing workloads and promise consistent dosing, making them pivotal in understaffed settings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent PMDA validation for combination products | –1.2% | National | Medium term (2-4 years) |

| High up-front cost of electronic pumps | –0.8% | National, heavier in rural clinics | Short term (≤ 2 years) |

| Domestic CDMO capacity constraints | –0.7% | Manufacturing clusters | Medium term (2-4 years) |

| Low patient awareness of nasal & pulmonary devices | –0.6% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent PMDA Validation for Combination Products Increases Time-to-Market

Half of the approved autoinjectors received clearance only after the parent drug’s initial approval, underscoring sequential review hurdles. Foreign companies frequently grapple with uncertainties surrounding human-factor studies for their device-drug combinations. Despite engaging in consultations with the PMDA office in Washington, DC, United States, foreign firms frequently grapple with heightened uncertainties in device-drug human-factor studies, leading to extended timelines. The resulting delay favors incumbent domestic players, who possess more profound regulatory expertise.

High Up-front Cost of Electronic Pumps Limits Smaller Clinics

Only 18.6% of local sponsors adopted decentralised clinical trial models in 2023, citing IT spending and staff workload as chief barriers. Capital-intensive smart pumps follow the same pattern, slowing diffusion to small or rural facilities. Financial constraints risk widening urban-rural treatment gaps even as policy pushes community-based care.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Implantable Disrupt Traditional Delivery Paradigms

Injectables accounted for 42.87% of Japan's drug delivery devices market share in 2025, driven by their broad applicability in diabetes and oncology. Autoinjector approvals climbed steadily as ergonomic designs improved safety and convenience. Meanwhile, implantables are forecast to post a 10.22% CAGR, supported by workforce shortages that favour long-acting solutions. Japan's drug delivery devices market size for implantables is projected to increase significantly as developers refine biodegradable matrices that minimize the need for replacement surgeries.

Inhalation devices are the next emerging category, driven by advancements in dry-powder technology. Transdermal patches continue to appeal to older patients who prefer painless, steady dosing. Ocular inserts and nasal pumps stay niche but attract R&D for targeted CNS or ophthalmic therapy. Competition is shifting as digital entrants challenge mechanical incumbents with sensor-equipped applicators. Investments in senescence-targeted release systems further differentiate domestic portfolios.

By Route of Administration: Inhalation Pathways Gain Therapeutic Momentum

Injectable routes controlled 55.96% of the Japan drug delivery devices market in 2025 owing to their entrenched role in biologics delivery. The inhalation route, however, is forecast to expand at 8.92% CAGR, driven by patient-friendly triple therapies such as AstraZeneca’s Breztri. Japan drug delivery devices market size for inhalation products is thus set for robust growth as formulators achieve higher lung deposition efficiency.

Transdermal pathways hold steady appeal, while oral mucosal routes gain visibility for rapid-acting pain or rescue medications. Nasal and ocular pathways remain small but could accelerate once awareness barriers drop. The route mix increasingly reflects patient autonomy goals and the search for non-invasive, home-compatible options.

By Technology: Electronic Solutions Transform Patient Experience

Mechanical formats retained 67.95% of revenue in 2025 but electronic-smart devices are expected to advance at 9.25% CAGR. Terumo’s GS26 strategy epitomises the pivot from single devices to digital ecosystems that track dosing and feed data to clinicians. The Japan drug delivery devices market size tied to connected products is likely to exceed USD 7.45 billion by 2031 if forecast adoption curves hold.

Needle-free jets attract niche demand among paediatric and needle-phobic groups. Controlled-release technologies benefit chronic disease management, especially where workforce gaps favour longer dosing intervals. Artificial intelligence modules that adapt dose timing to biomarker feedback are under active exploration.

By Application: Oncology Innovations Drive Precision Delivery

Diabetes held 28.35% share of the Japan drug delivery devices market size in 2025, reflecting mature insulin platforms. Oncology is on track for 10.12% CAGR as biomarker-guided regimens require precise, often targeted delivery.

Cardiovascular disorders leverage implantable and wearable pumps to enhance adherence. Respiratory diseases harness new DPIs and nebulisers, validated by recent COPD evidence on Breztri. Infectious and autoimmune segments round out the application map, each fostering specialised device tweaks.

By End User: Home-care Settings Reshape Delivery Paradigms

Hospitals still absorb 48.12% of national expenditure, anchoring complex infusion and peri-operative needs. Yet home settings will record 11.55% CAGR as NHI incentives encourage self-administration. Japan drug delivery devices market share shifts toward domiciliary channels as seniors seek convenience and institutions confront staffing caps.

Ambulatory surgical centres benefit from minimally invasive trends, while retail pharmacies emerge as counselling nodes for device initiation. Regional service gaps remain, underscoring demand for plug-and-play products that work with limited professional oversight.

Geography Analysis

Urban regions—such as Tokyo, Osaka, and Nagoya—account for a significant share of Japan's drug delivery devices market value, reflecting the presence of dense specialist networks and higher digital literacy. Tokyo alone accounts for nearly 30% of national consumption. The concentration is reinforced by the presence of enhanced home-care support clinics that streamline the deployment of wearable and implantable devices.

Government subsidies now target uptake in peripheral prefectures, where aging rates are highest yet provider density is lowest. Rural pilot programmes that combine telemedicine with innovative injectors show early success, hinting at future convergence of connectivity and drug delivery. Growth rates, therefore, outpace national averages, although absolute spend remains lower.

Manufacturing geography adds another layer—Shizuoka, Tochigi, and Saitama host sizeable device plants, including Nipro’s expanded Odate site. R&D clusters in Tsukuba Science City and Kansai foster university–industry collaborations, enabling advanced prototypes to progress without leaving the country. Regional interplay of demand, policy, and industrial capability thus shapes market rollout patterns.

Regulatory Landscape

Japan regulates drug delivery devices, including drug-device combination products and connected delivery systems, mainly under the Pharmaceuticals and Medical Devices Act (PMD Act) through the Ministry of Health, Labour and Welfare (MHLW) and the Pharmaceuticals and Medical Devices Agency (PMDA). Amendments enacted on May 14, 2025 are being implemented in phases through 2027, reinforcing pathways intended to reduce device lag while keeping strict evidence expectations for combination products. For connected injectors and other software-enabled delivery platforms, PMDA issued clearer Software as a Medical Device (SaMD) guidance in 2023 and introduced a more streamlined, two-step review approach in early 2024, which affects how sponsors structure clinical, performance, and cybersecurity documentation.

For combination products, classification depends on the Primary Mode of Action (PMOA), which determines whether the submission is treated principally as a drug (GMP) or a device (QMS), while still requiring integrated control over the non-primary constituent. Human factors and usability engineering remain central for self-administration products, with alignment to Japan Industrial Standards (for example, JIS T 62366-1 for usability engineering) commonly reflected in evidence packages. PMDA consultation channels, including its Washington, DC office opened in 2024, support earlier regulatory alignment for foreign and domestic developers addressing Japan-specific expectations for labeling, packaging, and validation of combination products.

Value Chain Analysis

The Japan drug delivery devices value chain covers drug and device design (including user-centered engineering for self-administration), component sourcing (polymers, elastomers, needles, microelectronics and sensors for connected devices), and manufacturing under either drug GMP or medical device QMS, depending on combination-product PMOA. Japan-based drug-device CDMOs and packaging specialists support scale-up, sterile assembly, device component production, and fill-finish coordination, while also helping sponsors manage integrated purchasing and supplier qualification for the non-primary constituent of the combination. A key constraint in advanced formats is capacity and lead-time friction in complex subcomponents, particularly microelectronics for electronic and smart platforms, which drives manufacturers to tighten supplier partnerships and use multi-sourcing strategies.

Downstream, wholesalers and logistics providers extend distribution into end-to-end service models that go beyond delivery into post-marketing support, reflecting the operational needs of home-based care and connected monitoring. Bundled platforms that combine manufacturing with regulatory application support and commercialization services are a common entry route for overseas companies seeking to reduce initial Japan set-up burden; one example is the J-ENTRY Consortium (Suzuken, Bushu Pharmaceuticals, EPS Holdings), positioned as a one-stop channel across approval support and distribution. As connected delivery systems expand, lifecycle cybersecurity risk management requirements embedded in Japan’s Essential Principles add another compliance layer that influences vendor selection, device maintenance planning, and post-market workflows.

Competitive Landscape

The field is moderately consolidated. Terumo Corporation leads domestically, posting FY 2025 revenue of JPY 1,036.2 billion (USD 6.9 billion). Partnerships are a defining tactic; Orchestra BioMed’s collaboration with Terumo on the Virtue SAB balloon underscores the move toward therapy-device bundles.

Whitespace persists in geriatric-friendly formats that simplify use for seniors with cognitive impairments. Regulatory attention to “drug loss” has spurred entrants to target combination product voids, primarily paediatric and rare-disease areas. Digital firms that pair dosing with analytics are gaining traction as healthcare payers seek demonstrable outcome improvements.

Competition also hinges on supply chain resilience. Domestic contract manufacturers face capacity bottlenecks in microelectronics, prompting them to form alliances with semiconductor suppliers. Multinationals continue diversifying into value-added services, bundling cloud dashboards with hardware to secure recurring revenue and lock in provider ecosystems.

Japan Drug Delivery Devices Industry Leaders

Tasei Kako Co. Ltd.

Novartis AG

Becton, Dickinson and Company

Johnson & Johnson

Nipro Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Home-based care expansion and PMDA support for digital review workflows are widening whitespace for self-administered, connected drug delivery devices that reduce clinician workload and enable adherence monitoring, particularly in high-burden chronic areas such as diabetes and oncology. There is also room for practical, geriatric-friendly product redesign, consistent with Japan’s large older-adult population managing chronic conditions, where simplified interfaces, safety locks, and longer dosing intervals directly address dexterity and caregiving constraints. PMDA Regulatory Science (RS) consultations offer an identifiable route for innovators to align R&D strategy and evidence generation for novel delivery approaches, which is especially relevant when combination-product packaging, naming, and validation expectations add complexity to market entry.

Manufacturing investments in Japan provide an execution platform for advanced injectables and device-drug combinations that depend on reliable sterile supply and flexible surge capacity. In April 2026, Nipro completed a new vial-based injectable drug manufacturing building at its Omi plant in Shiga Prefecture with emergency vaccine manufacturing switch capability, indicating continued domestic build-out for injectable formats used across multiple therapies. Large-scale expansions across biopharma and CDMO infrastructure, including Fujifilm’s completion of a major bio-CDMO facility at its Toyama Second Factory in December 2025, support a broader pipeline mix (including biologics and ADCs) that often pairs with higher-precision delivery devices and administration systems, reinforcing demand for compatible primary containers, injectors, and integrated delivery solutions.

Recent Industry Developments

- April 2026: Nipro completed a new vial-based injectable drug manufacturing building at its Omi plant in Shiga Prefecture, adding emergency vaccine manufacturing switch capability alongside routine prescription medicine output. The added domestic injectable capacity supports supply continuity for therapies that rely on vials and associated administration hardware, strengthening local readiness for both chronic-care demand and surge scenarios.

- May 2025: UCB received PMDA approval in Japan for at-home self-administration of Rystiggo using either an infusion pump or manual push syringe for patients with generalized myasthenia gravis (gMG). The approval expands the range of reimbursable administration options suited to home care, directly reinforcing demand for user-friendly infusion and syringe-based delivery configurations.

- November 2024: PMDA opened its first overseas office in Washington, DC to streamline guidance and engagement for foreign companies seeking access to the Japan market. Earlier, more direct consultation can shorten iteration cycles on combination-product and usability evidence packages, supporting a smoother pathway for imported drug-device platforms entering Japan.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of devices used in Japan to deliver a finished drug dose into the body, including devices that store, meter, or help administer medicines across major routes of administration.

Scope exclusions: We exclude software-only adherence apps and contract packaging or drug-filling services that do not represent device value.

Segmentation Overview

- By Device Type

- Injectable Delivery Devices

- Inhalation Delivery Devices

- Infusion Pumps

- Transdermal Patches

- Implantable Drug Delivery Systems

- Ocular Inserts & Delivery Implants

- Nasal & Buccal Delivery Devices

- By Route of Administration

- Injectable

- Inhalation

- Transdermal

- Oral Mucosal (Buccal & Sublingual)

- Ocular

- Nasal

- By Technology

- Conventional Mechanical

- Electronic / Smart / Connected

- Needle-free Jet

- Controlled / Sustained-release Systems

- By Application

- Diabetes Mellitus

- Oncology

- Cardiovascular Disorders

- Respiratory Diseases (Asthma, COPD)

- Infectious Diseases (e.g., RSV, Influenza)

- Auto-immune & Others

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Home-care Settings

- Retail Pharmacies & Clinics

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the device landscape and set the starting assumptions, which we later checked with interviews. We reviewed public sources such as Japan MHLW notifications and medical device policy updates, PMDA product and safety information, Statistics Bureau of Japan demographic series, OECD Health Statistics, and peer-reviewed clinical and health economics journals that discuss self-injection and adherence outcomes.

We also used company annual reports, investor presentations, and credible press releases to track product launches, recall events, and manufacturing footprints. For signals that are harder to observe in open sources, we selectively used paid subscriptions focused on company financials and intelligence, patent activity, and shipment-level import-export records to sanity-check device flows and the direction of pricing. These desk sources are illustrative and not exhaustive, and additional references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was conducted through expert interviews and structured surveys with manufacturers, distributors, hospital procurement stakeholders, clinicians, and home-care related channels. This input helped us verify adoption patterns and how pricing logic works in Japan, particularly across care settings and distribution pathways. Because this is a Japan-only market, we covered prefecture clusters and care contexts where device usage is commonly reported, so gaps from desk research could be closed and key assumptions triangulated before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | |

| Mid tier: 58% | Functional/Unit leaders: 31% | |

| Smaller Players: 14% | Managers: 56% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where Japan healthcare demand signals are translated into device spending pools, then split across delivery routes and care settings using observed usage patterns. The totals are subsequently corroborated through selective bottom-up checks, including supplier revenue sampling, channel feedback on unit movement, and sampled ASP-times-volume math for common device formats, so we can adjust any overstatement.

Inputs used in the model include Japan age structure and chronic disease burden, self-administration penetration by therapy area, procedure and infusion utilization trends, device replacement cycles for durable formats, and observed ASP movement after reimbursement or policy changes. Where a bottom-up proxy is incomplete, we apply conservative range assumptions and then trim them back using interview-led share bands so the final number remains explainable.

For forecasting, we use scenario analysis supported by variable-level expectations from primary experts. The key scenarios mainly differ on the uptake speed of self-injection formats, the shift into home-care, and the pricing progression. This approach keeps the forecast traceable to a few clear drivers rather than relying on hidden statistical complexity.

Data Validation & Update Cycle

Outputs are validated through triangulation across multiple signals, followed by variance checks at the route-of-administration level and against Japan macro healthcare spending direction. When a segment shows an unusual jump or an unexpected price move, we re-check the underlying assumptions, revisit source notes, and re-contact relevant interviewees if the gap cannot be explained.

Before sign-off, the model goes through multi-step analyst review where inputs, calculations, and unit conversions are checked again, so the final dataset stays consistent across years. Reports are refreshed annually, with interim updates triggered by material events such as major reimbursement revisions, safety actions, or step-changes in adoption. A final pre-delivery pass is then performed to ensure clients receive the latest view.

Mordor Intelligence's Japan Drug Delivery Devices Market Size Compared Against Other Published Estimates

Published market sizes for Japan drug delivery devices do not always match because firms often draw the scope lines differently, pick different base years, and apply their own pricing and adoption assumptions. The result is that two credible-looking numbers can still be measuring slightly different things.

The table highlights that the spread is mostly driven by what is counted as a device market versus an adjacent services or specialty subset, and by how fast pricing is allowed to change over time. Some estimates also extend the forecast horizon far out, which makes the outcome more sensitive to long-term penetration assumptions and currency timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.04 B (2025) | |

| Industry Publisher A | USD 13.20 B (2025) | Uses a broader downstream framing that can blend device value with wider application and facility splits, which can shift category mapping when comparing route-of-administration totals. |

| Global Databook B | USD 0.04 B (2024) | Measures a narrow subset labeled as drug and gene delivery devices and reports a much smaller pool, so it is not comparable to an all-device view across mainstream delivery routes. |

The table shows the largest gap comes from scope. In Mordor Intelligence's model, the total is built only from physical drug delivery devices sold into Japan, with software-only tools and contract packaging services left out, so the number stays tied to repeatable device demand indicators. Once that scope is held consistent, the remaining differences usually come down to pricing progression and the pace assumed for self-administration adoption over the forecast window.

Key Questions Answered in the Report

What is the current size of the Japan drug delivery devices market?

The market reached USD 14.14 billion in 2026 and is projected to climb to USD 21.22 billion by 2031.

Which device type holds the largest Japan drug delivery devices market share?

Injectable systems led with 42.87% share in 2025 because of their versatility in diabetes and oncology care.

Why are home-care settings important for future sales?

Home-care environments are projected to expand at a 11.55% CAGR to 2031 as policymakers shift care away from hospitals to manage workforce shortages.

How are government policies influencing adoption?

NHI reimbursement for wearables and PMDA fast-track reviews for SaMD injectors are speeding uptake of self-administration technologies.

What is the main restraint hindering faster growth?

Stringent PMDA validation processes for combination products can delay market entry, especially for foreign manufacturers unfamiliar with local requirements.

Page last updated on: