Japan Dietary Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 13.60 Billion |

| Market Size (2026) | USD 14.04 Billion |

| Market Size (2031) | USD 16.48 Billion |

| Growth Rate (2026 - 2031) | 3.26% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Dietary Supplements Market Analysis by Mordor Intelligence

The Japanese dietary supplements market size was valued at USD 13.60 billion in 2025 and estimated to grow from USD 14.04 billion in 2026 to reach USD 16.48 billion by 2031, at a CAGR of 3.26% during the forecast period (2026-2031). This moderate growth rate masks significant underlying shifts in consumer preferences and product innovation, particularly in response to Japan's super-aging society, where supplements are increasingly viewed as essential health maintenance tools rather than optional wellness products. The aging population is driving demand for condition-specific nutrients, supported by the shift of a robust retail ecosystem toward online channels and advancements in probiotics, gummies, and plant-based formats. Government initiatives that position supplements as complements to food rather than pharmaceuticals continue to strengthen consumer trust. Additionally, premiumization trends are contributing to higher average selling prices. Market leaders are enhancing scientific validation, establishing cross-industry partnerships with biotech and digital health firms, and expanding their presence across broader Asian markets. Although cost-of-living challenges and stricter labeling regulations are moderating demand, they have not disrupted the positive revenue growth trajectory.

Key Report Takeaways

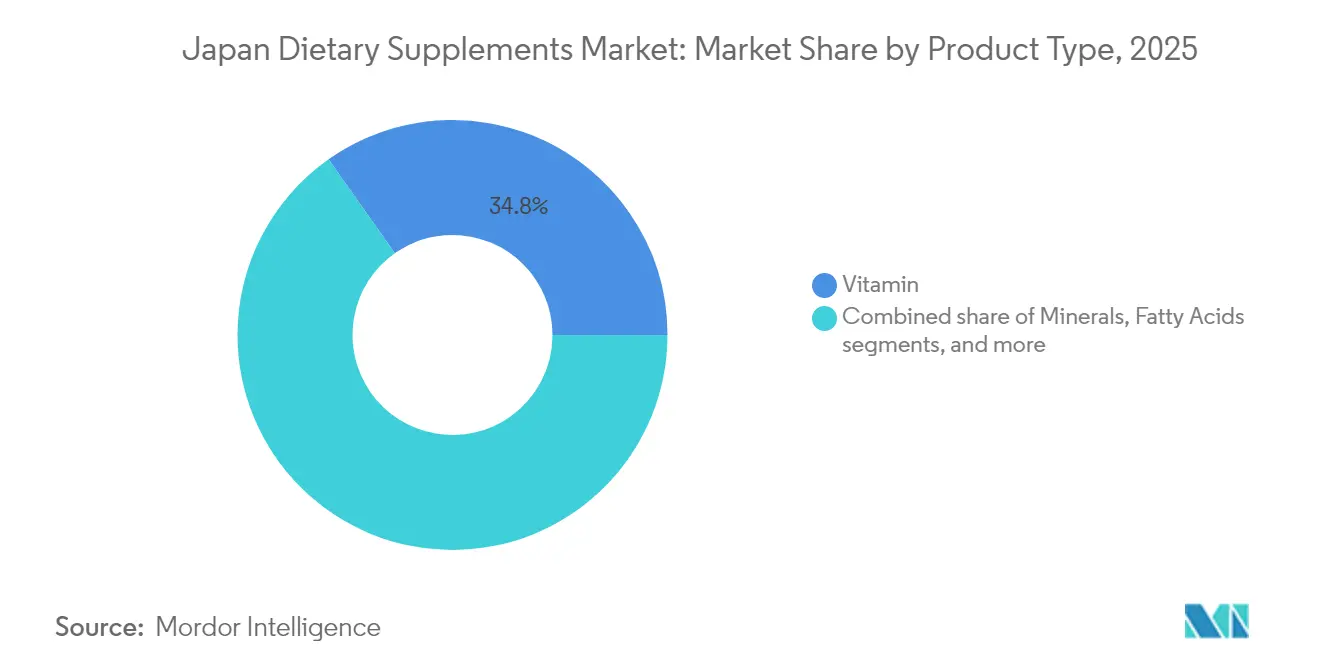

- By product type, vitamins led with a 34.78% share of the Japan dietary supplements market in 2025, while probiotics are set to grow at a 5.63% CAGR through 2031.

- By form, capsules secured 37.64% of the 2025 Japan dietary supplements market share, whereas gummies are forecasted to register a 4.14% CAGR from 2026-2031.

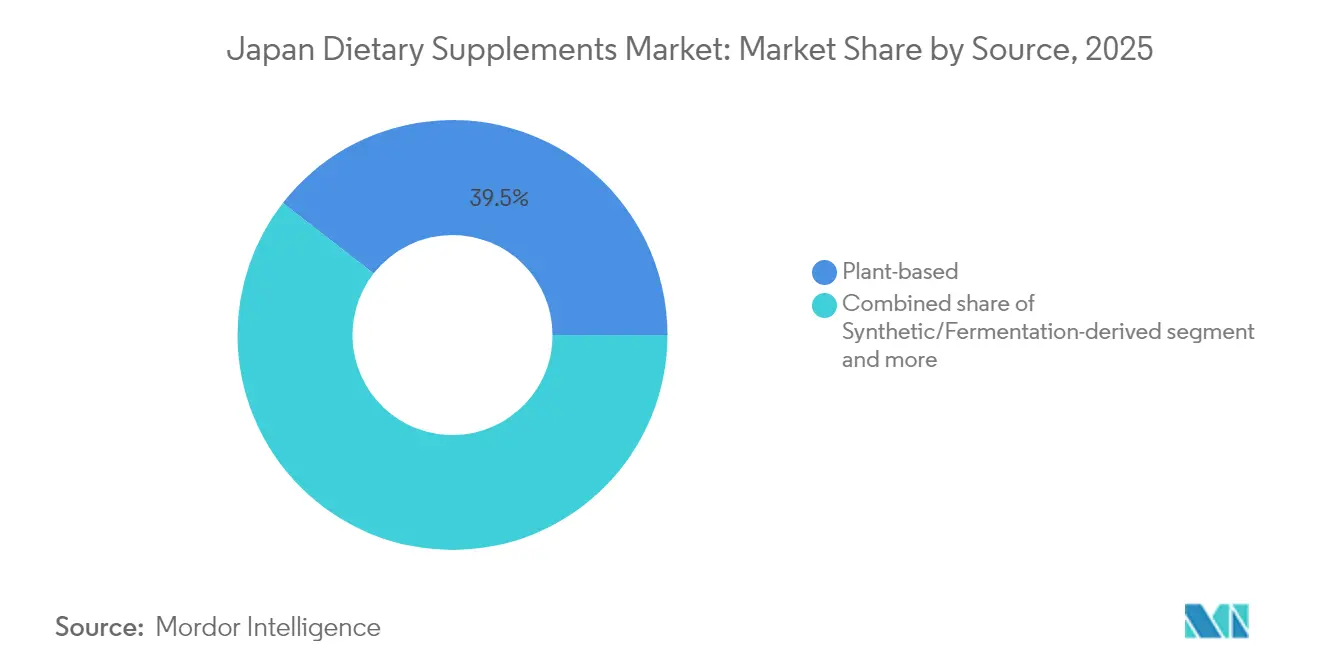

- By source, plant-based supplements held a 39.48% revenue share in 2025, while synthetic/fermentation-derived supplements are forecasted to grow at a 4.22% CAGR over the next five years.

- By consumer group, women captured 50.61% of 2025 revenue, while the kids/children segment is expected to advance at a 5.52% CAGR over 2026-2031.

- By health application, immunity enhancement products accounted for 27.62% of sales in 2025, with skin, hair, and nail care offerings projected to post a 4.05% CAGR during 2026-2031.

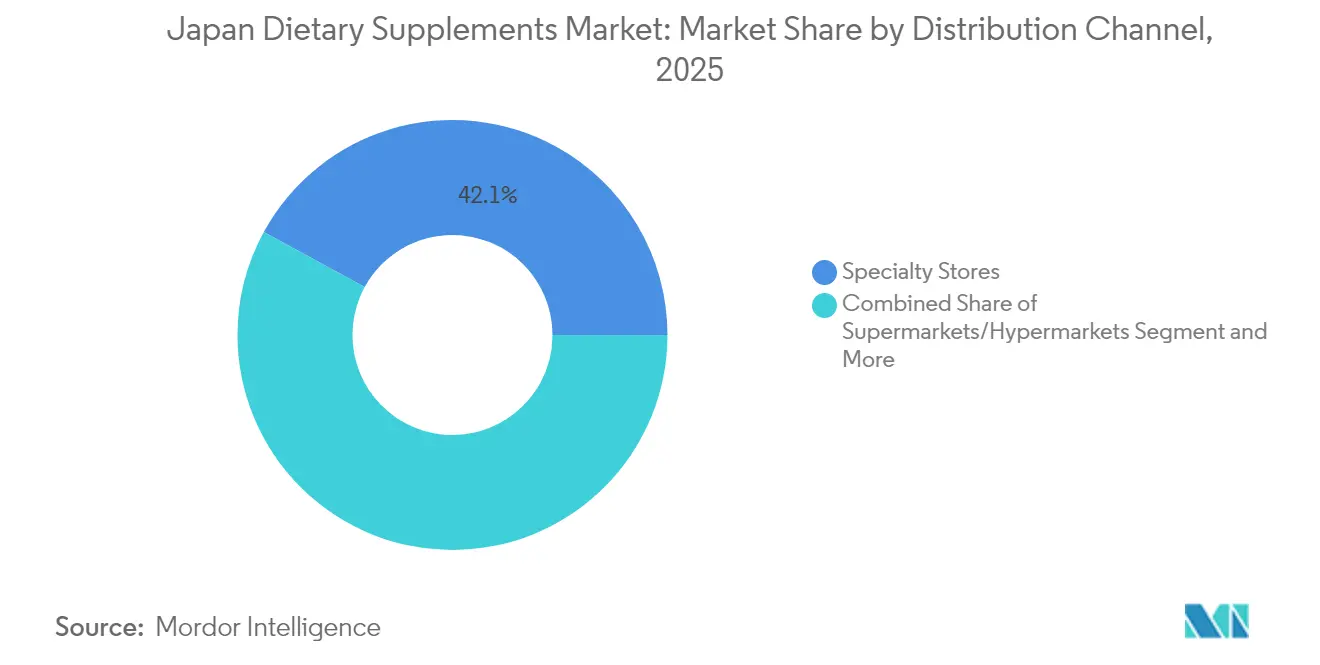

- By distribution channel, specialty stores claimed 42.05% of 2025 revenue, while online retail is positioned for the fastest expansion at a 3.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Dietary Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising emphasis on preventive healthcare | +1.2% | Nationwide (Japan) | Medium term (2–4 years) |

| Emergence of personalized nutrition platforms leveraging gut-microbiome testing | +0.8% | Nationwide (Japan) | Medium term (1–3 years) |

| Corporate wellness programs expanding workplace supplement purchases | +0.3% | Nationwide (Japan) | Long term (≥ 4 years) |

| Aging population driving condition-specific supplement uptake | +0.5% | Nationwide (Japan) | Short term (1–2 years) |

| Increasing awareness of nutritional deficiencies driving supplement adoption | +0.3% | Nationwide (Japan) | Medium term (2–4 years) |

| Rising e-commerce penetration enhancing accessibility to dietary supplements | +0.3% | Nationwide (Japan) | Medium term (3–5 years) |

| Source: Mordor Intelligence | |||

Rising Emphasis on Preventive Healthcare

Japan's healthcare system is transitioning from a treatment-focused model to a prevention-oriented framework. To mitigate rising healthcare costs, consumers are increasingly adopting preventive health measures. According to the Organisation for Economic Co-operation and Development (OECD), the per capita health expenditure in Japan was USD 5,639.62 in 2023[1]Source: Organisation for Economic Co-operation and Development, "Health Expenditure and Financing", www.oecd.org. This shift is driving substantial growth opportunities in the dietary supplements market, as these products are being positioned as essential components of proactive health management strategies. A key example of this transition is the Specific Health Checkup initiative, which has demonstrated a measurable reduction in the prevalence of chronic conditions such as diabetes and hypertension among participants compared to non-participants. The adoption of preventive healthcare practices is particularly strong among younger demographics, including millennials and Gen Z, who are increasingly incorporating dietary supplements into their daily routines. These consumer segments exhibit a strong preference for products that provide immune-boosting and energy-enhancing benefits, aligning with their active lifestyles and long-term health objectives.

Emergence of Personalized Nutrition Platforms Leveraging Gut-Microbiome Testing

Japan's supplement market is undergoing a significant transformation, driven by advancements in gut microbiome research and the integration of digital health technologies. These innovations are enabling the development of highly personalized solutions tailored to the unique biological profiles of individual consumers, marking a shift toward precision nutrition. For instance, Meiji Seika Pharma launched its meiQua supplement brand. This brand is strategically positioned to address specific nutrient deficiencies identified through comprehensive medical consultations and diagnostic testing. By leveraging a science-based approach, the brand aligns with the evolving preferences of Japan's well-informed and health-conscious consumer base, which increasingly prioritizes products supported by credible scientific evidence. This shift in consumer behavior is reflected in the personalized nutrition segment, which is projected to grow at nearly twice the rate of the overall supplements market. This growth underscores a clear trend as consumers move away from generic offerings and gravitate toward tailored solutions designed to meet their distinct biological and nutritional needs.

Corporate Wellness Programs Expanding Workplace Supplement Purchases

Japanese corporations are increasingly incorporating dietary supplements into their employee wellness programs, establishing an innovative distribution channel while encouraging consistent supplement consumption among employees. This strategic initiative in corporate wellness is gaining significant traction as organizations seek to reduce healthcare-related expenses, minimize absenteeism, and enhance overall workforce productivity, particularly within Japan's demanding and high-pressure professional environment. As per the Ministry of Internal Affairs and Communications, Japan's employment rate among individuals aged 25 to 34 years reached 87.6% in 2024. For the population aged 65 years and above, the employment rate increased to 25.7%. In response to this trend, dietary supplement manufacturers are designing customized corporate wellness solutions that include subscription-based models and educational programs. These initiatives not only provide manufacturers with reliable and recurring revenue streams but also address critical workplace health challenges, such as stress management and immune system support, aligning seamlessly with the broader objectives of fostering organizational health, efficiency, and employee well-being.

Aging Population Driving Condition-Specific Supplement Uptake

Older adults increasingly adopt proactive measures to manage their health. In 2024, Japan's population aged 65 and above reached 36.24 million, accounting for 29.3% of the total population, according to the Statistics Bureau of Japan[2]Source: Statistics Bureau of Japan, "Current Population Estimates", www.stat.go.jp. This demographic shift highlights the growing prevalence of chronic conditions such as osteoporosis, cardiovascular diseases, arthritis, and cognitive decline. As a result, the health supplements market is experiencing significant growth, driven by rising demand for products specifically designed to address age-related health challenges. The expanding elderly population has fostered innovation, particularly in the development of formulations targeting bone health, cognitive function, and mobility. In Japan, seniors are increasingly integrating health supplements into their daily routines, considering them essential to their overall healthcare management. This evolving consumer behavior, supported by evidence-based research, is reshaping product development pipelines and marketing strategies. Companies are leveraging these insights to align their offerings with the specific and growing needs of this demographic segment, thereby securing a competitive advantage in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit products stifling growth | -0.7% | Nationwide (Japan) | Medium term (2–4 years) |

| Growing consumer doubts on synthetic additives | -0.4% | Nationwide (Japan) | Short term (1–3 years) |

| Stringent advertising rules limiting health-benefit claims | -0.3% | Nationwide (Japan) | Short term (≤ 2 years) |

| High production costs challenge market expansion | -0.3% | Nationwide (Japan) | Medium term (2–5 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products Stifling Growth

The prevalence of counterfeit dietary supplements is undermining consumer trust and disrupting various markets, particularly within e-commerce, where ensuring product authenticity remains a persistent challenge. This issue is especially significant in Japan, as counterfeit products often enter the market through cross-border e-commerce platforms. High-value segments, such as beauty supplements, are disproportionately impacted due to their premium pricing, which incentivizes counterfeit activities. To address this concern, leading manufacturers are increasingly implementing advanced authentication technologies, including blockchain-based traceability systems and QR code verification mechanisms, to protect product integrity. However, the adoption of these advanced technologies leads to higher operational costs, which are ultimately transferred to consumers, influencing overall market dynamics.

Growing Consumer Doubts on Synthetic Additives

Japanese consumers are increasingly evaluating supplement formulations with heightened scrutiny, showing growing skepticism toward synthetic additives and high-dose products. This shift was exemplified by the "red yeast rice issue," which adversely affected consumer trust in dietary supplements, particularly tablets and capsules. Regulatory changes are further influencing this trend. In March 2024, Japan's Ministry of Health, Labour and Welfare classified 'Polyvinyl Alcohol' as a 'Designated Additive,' restricting its use to non-standard food forms such as capsules and tablets. These developments are driving demand for "clean label" products with minimal additives and scientifically supported dosages. While this creates challenges for manufacturers reliant on legacy formulations, it also presents opportunities for brands prioritizing purity and evidence-based efficacy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Probiotics Disrupt Traditional Vitamin Dominance

The vitamins segment holds a significant 34.78% share of the market, highlighting its critical role in Japan's dietary supplementation industry. Recognized as essential for daily health support, vitamins are particularly valued by seniors seeking to maintain independence and prevent frailty. In comparison, the probiotics segment is anticipated to grow at a strong CAGR of 5.63% during the forecast period of 2026-2031. This growth is driven by increasing scientific research linking gut health to overall wellness and immunity, alongside advancements in delivery systems and strain-specific formulations that address a wider range of health concerns beyond digestion.

Yakult Honsha, leveraging its established cultural association with fermented products, has expanded its probiotic offerings. Its latest product, the Yakult BL Firstone capsule, incorporates the proprietary Lactobacillus casei strain Shirota, providing a convenient option for daily consumption. The protein and amino acids segment is diversifying its market focus, moving beyond traditional sports nutrition to target the aging population with claims centered on sarcopenia prevention. Simultaneously, herbal supplements are witnessing growth, driven by increasing consumer interest in traditional Japanese and Asian botanicals, supported by modern scientific research.

By Form: Gummies Revolutionize Consumption Experience

While capsules and softgels currently dominate the market with a 37.64% share in 2025, the gummies segment is experiencing explosive growth at 4.14% CAGR (2026-2031), revolutionizing supplement consumption patterns across demographic groups. This growth is significantly altering supplement consumption patterns across various demographic groups. The trend underscores a growing emphasis on improving the consumption experience and ensuring compliance, particularly among younger consumers and seniors who often encounter difficulties with traditional pill formats. Technological advancements in gummy formulations have addressed previous challenges related to ingredient stability and dosage precision, enabling the efficient delivery of active ingredients in consumer-preferred formats.

The tablet segment remains a significant market player but is gradually losing share to more consumer-focused formats. Powders continue to be relevant, especially in protein supplements and drink mixes. The liquid segment is gaining momentum in beauty-from-within products and energy formulations, leveraging its rapid absorption properties. Recent innovations include collagen gummies with enhanced bioavailability and probiotic gummies utilizing patented microencapsulation technology to maintain product efficacy. This diversification in delivery formats enables manufacturers to target specific demographic groups with tailored solutions, thereby broadening the consumer base beyond traditional supplement users.

By Source: Plant-Based Leads While Synthetic Gains Momentum

Plant-based supplements currently lead the market with a 39.48% share in 2025, aligning with Japanese cultural preferences for natural ingredients and traditional botanical remedies. Ingredients like ginseng, turmeric, green tea extract, dokudami, barley grass, and shiso are commonly consumed for their believed health effects. However, the synthetic/fermentation-derived segment is experiencing the fastest growth at 4.22% CAGR (2026-2031), driven by advances in precision fermentation and bioengineering that enable the production of nature-identical compounds with enhanced stability, potency, and sustainability profiles.

Animal-based supplements, particularly collagen products, continue to play a significant role, with marine sources dominating this category. Shiseido's The Collagen Powder, featuring 5000mg of fish collagen, royal jelly, and vitamin C, highlights the premium positioning of this segment and its strong association with beauty benefits. The synthetic segment's expansion is supported by innovations in bioavailability and targeted delivery systems. Companies such as Kirin Holdings are leveraging their expertise in fermentation to develop advanced ingredients with enhanced functional properties. These technological advancements are facilitating the creation of supplements with precisely engineered molecular structures tailored for specific health applications, increasingly bridging the gap between supplements and pharmaceuticals.

By Consumer Group: Women Lead While Children's Segment Accelerates

In 2025, women hold a 50.61% share of the market, highlighting their significant engagement with health and wellness products and their critical role as primary health decision-makers within households. Conversely, the children's segment is anticipated to grow at a strong 5.52% CAGR during the forecast period of 2026-2031. This growth is driven by an increased parental focus on developmental support, strengthening immune systems, and addressing nutritional deficiencies in modern diets. These priorities are influenced by greater access to online health information, recommendations from pediatricians, input from schools, and a growing emphasis on early development, immunity, and cognitive focus.

The women's segment is evolving from general wellness solutions to targeted products designed to meet specific life-stage needs. For example, Otsuka Pharmaceutical's EQUELLE focuses on managing menopausal symptoms, reflecting this shift. Similarly, the men's segment is expanding, with gender-specific formulations addressing concerns such as prostate health, stress management, and physical performance. This segmentation of consumer groups is driving more precise marketing strategies and product development, with formulations increasingly tailored to the unique physiological requirements and health priorities of distinct demographic categories.

By Health Application: Immunity Leads While Beauty Supplements Surge

Immunity enhancement currently leads the market with a 27.62% share in 2025, reflecting heightened health consciousness following the global pandemic. The skin, hair, and nail care segment is the fastest-growing, with a projected 4.05% CAGR from 2026 to 2031. This growth is driven by the rising popularity of the "beauty from within" concept and heightened awareness of the relationship between nutrition and physical appearance. Younger generations, particularly Gen Z and Millennials, increasingly associate nutrition with beauty, leading to their rapid adoption of SHN supplements.

The general health and wellness segment remains a key market component but is gradually losing share to more specialized applications as consumers shift their focus to targeted benefits over generalized solutions. The bone and joint health segment is gaining traction, supported by the aging population. Gastrointestinal and gut health applications are expanding their scope, moving beyond traditional digestive support to address the gut-brain axis and immune system modulation. Additionally, cognitive and mental health applications are emerging as a significant growth area. Products designed to reduce stress, improve sleep quality, and enhance cognitive performance are gaining popularity, particularly among professionals in high-pressure environments.

By Distribution Channel: Specialty Stores Dominate While Online Accelerates

Specialty stores hold a dominant 42.05% market share, capitalizing on curated product selections, knowledgeable staff, and personalized recommendations to build consumer trust. However, online retail channels are experiencing the fastest growth, with a projected CAGR of 3.55% from 2026 to 2031. This growth is driven by the convenience of online shopping, a broader product range, and the integration of digital health platforms that provide supplement recommendations. Online platforms offer seamless access to a wide variety of supplements, eliminating the need for visits to multiple physical stores. This is particularly advantageous for individuals in rural or remote areas, time-constrained consumers, and repeat buyers who prefer subscription-based purchases.

Supermarkets and hypermarkets maintain a significant market presence by offering mainstream brands at competitive prices. According to the Statistics Bureau of Japan, there were 5,962 supermarkets in Japan in 2023. Simultaneously, direct selling continues to thrive, supported by established network marketing leaders such as Amway Japan G.K. and Herbalife Japan K.K. The rise of e-commerce is driving increased price transparency and providing consumers with detailed product information and reviews. In response, traditional retailers are enhancing their in-store experiences and expertise to remain competitive. Meanwhile, online platforms are optimizing advanced recommendation algorithms and subscription models to strengthen customer loyalty and maximize lifetime value.

Geography Analysis

In Japan, prominent urban centers such as Tokyo, Osaka, and Nagoya dominate the dietary supplements market, reflecting higher penetration rates and a strong consumer preference for innovative product formats and advanced ingredient formulations. Concurrently, the aging population in rural areas serves as a significant growth driver, with increasing demand for condition-specific supplements designed to address mobility challenges, cardiovascular health concerns, and cognitive function support.

Regional variations play a critical role in shaping product demand across the country. Western Japan demonstrates a marked preference for traditional herbal formulations, while eastern regions exhibit greater receptivity to cutting-edge ingredients and modern product formats. The Kansai region, which includes key cities like Osaka, Kyoto, and Kobe, showcases robust demand for beauty supplements, particularly collagen-based products, which consistently achieve penetration rates exceeding the national average.

In northern regions, seasonal consumption patterns are evident, with vitamin D usage peaking during winter months to mitigate the effects of reduced sun exposure. This geographic diversity highlights the strategic importance of adopting region-specific marketing and distribution approaches. Brands that successfully align their messaging and product portfolios with localized health priorities and cultural preferences are better positioned to capture market share and drive sustained growth.

Competitive Landscape

The Japanese dietary supplements market is moderately fragmented, comprising established domestic companies with strong cultural expertise and multinational corporations offering advanced research capabilities and large-scale manufacturing. The market is moderately concentrated, with prominent players including Otsuka Pharmaceutical Co. Ltd., DHC Corporation, Suntory Holdings, Kirin Holdings Company, Limited (FANCL Corp.), and Yakult Honsha Co. Ltd.

In Japan's dietary supplement market, companies are increasingly turning to strategic partnerships as a key competitive strategy. These partnerships enable firms to leverage shared resources, access advanced research and development capabilities, co-develop innovative products, and expand their reach through collaborative distribution channels, thereby strengthening their market position. Companies in the market are implementing strategic initiatives such as product innovation, rapid market expansion, mergers and acquisitions, and partnerships to enhance market share, expand their customer base, and achieve a competitive advantage. In May 2024, Kirin Holdings announced plans to launch a tender offer for the complete acquisition of FANCL Corporation, converting FANCL from a public company to a wholly owned subsidiary. This acquisition aligns with Kirin's transformation strategy to expand its Health Science segment and enhance its market position in preservative-free beauty products and health supplements.

Opportunities exist in personalized nutrition platforms that integrate diagnostic testing with customized supplement solutions. Emerging disruptors include niche direct-to-consumer brands utilizing social media marketing and subscription-based models to establish loyal customer bases outside traditional retail frameworks. Technology adoption is becoming a key differentiator, with leading companies leveraging blockchain for supply chain traceability, AI-driven formulation development, and digital platforms offering personalized recommendations based on individual health data and consumption patterns.

Japan Dietary Supplements Industry Leaders

-

Otsuka Pharmaceutical Co. Ltd.

-

DHC Corporation

-

Yakult Honsha Co. Ltd.

-

Kirin Holdings Company, Limited (FANCL Corp.)

-

Suntory Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Suntory Wellness, the health and wellness division of Japan's Suntory Group, has launched VISTRA Sesamin Night Time in Thailand, marking its first collaborative product development with NBD Healthcare Co., Ltd. The supplement, which contains sleep-enhancing sesamin compounds, is now available through select e-commerce platforms, pharmacies, and drugstores.

- October 2024: South Korean firm Clio has launched its ingestible beauty brand, TRUE RX, in drugstores throughout Japan, marking a significant step in its expansion efforts beyond the cosmetics sector.

- June 2024: Shiseido Company launched its new Ultimune ingestible probiotic powder across Japan. The product is filled with probiotic strain Bifidobacterium animalis, amla fruit, and blueberry ingredients. The product claims to improve the intestinal environment and support the immune system and oral health.

- April 2024: CURE, a New York-based brand, announced the launch of a range of CBD-infused functional beverages and supplements in the form of gummies in Japan, catering specifically to the sports nutrition segment.

Japan Dietary Supplements Market Report Scope

Dietary supplements are products that are intended to add to or supplement the diet and are different from conventional food. Dietary supplements help improve and maintain overall health and meet daily requirements for nutrients.

The Japanese dietary supplements market is segmented by type, form, consumer group, health applications, and distribution channel. Based on type, the market is segmented into vitamins, minerals, fatty acids, protein and amino acids, prebiotic & probiotic supplements, herbal supplements, enzymes, blended supplements, and others. Based on form, the market is segmented into tablets, capsules & softgels, powders, gummies, liquids, and others. Based on the source, the market is segmented into plant-based, animal-based, and synthetic / fermentation-derived. Based on consumer group, the market is segmented into men's, women's, and kids'/children's. Based on health applications, the market is segmented into general health & wellness, bone & joint health, energy & weight management, gastrointestinal & gut health, immunity enhancement, cardiovascular health, diabetes management, cognitive & mental health, skin, hair & nail care, eye health, and other health applications. Based on distribution channels, the market is segmented into supermarkets & hypermarkets, specialty stores, online retail channels, direct selling, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Vitamins |

| Minerals |

| Fatty Acids |

| Protein and Amino Acids |

| Prebiotic and Probiotic Supplements |

| Herbal Supplements |

| Enzymes |

| Blended Supplements |

| Other Types |

| Tablets |

| Capsules and Softgels |

| Powders |

| Gummies |

| Liquids |

| Other Forms |

| Plant-Based |

| Animal-Based |

| Synthetic/Fermentation-Derived |

| Men |

| Women |

| Kids/Children |

| General Health and Wellness |

| Bone and Joint Health |

| Energy and Weight Management |

| Gastrointestinal and Gut Health |

| Immunity Enhancement |

| Cardiovascular Health |

| Diabetes Management |

| Cognitive and Mental Health |

| Skin, Hair, and Nail Care |

| Eye Health |

| Other Health Applications |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Direct Selling |

| Other Distribution Channels |

| By Product Type | Vitamins |

| Minerals | |

| Fatty Acids | |

| Protein and Amino Acids | |

| Prebiotic and Probiotic Supplements | |

| Herbal Supplements | |

| Enzymes | |

| Blended Supplements | |

| Other Types | |

| By Form | Tablets |

| Capsules and Softgels | |

| Powders | |

| Gummies | |

| Liquids | |

| Other Forms | |

| By Source | Plant-Based |

| Animal-Based | |

| Synthetic/Fermentation-Derived | |

| By Consumer Group | Men |

| Women | |

| Kids/Children | |

| By Health Application | General Health and Wellness |

| Bone and Joint Health | |

| Energy and Weight Management | |

| Gastrointestinal and Gut Health | |

| Immunity Enhancement | |

| Cardiovascular Health | |

| Diabetes Management | |

| Cognitive and Mental Health | |

| Skin, Hair, and Nail Care | |

| Eye Health | |

| Other Health Applications | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Direct Selling | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current size of the Japanese dietary supplements market?

The Japanese dietary supplements market stands at USD 14.04 billion in 2026.

How fast will the market grow over the next five years?

Revenue is projected to increase at a 3.26% CAGR, reaching USD 16.48 billion by 2031.

Which supplement category holds the largest share today?

Vitamins account for 34.78% of 2025 sales, making them the single-largest type segment.

Which distribution channel is expanding the faster?

Online retail is forecast to register a 3.55% CAGR between 2026 and 2031.

Page last updated on: