Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

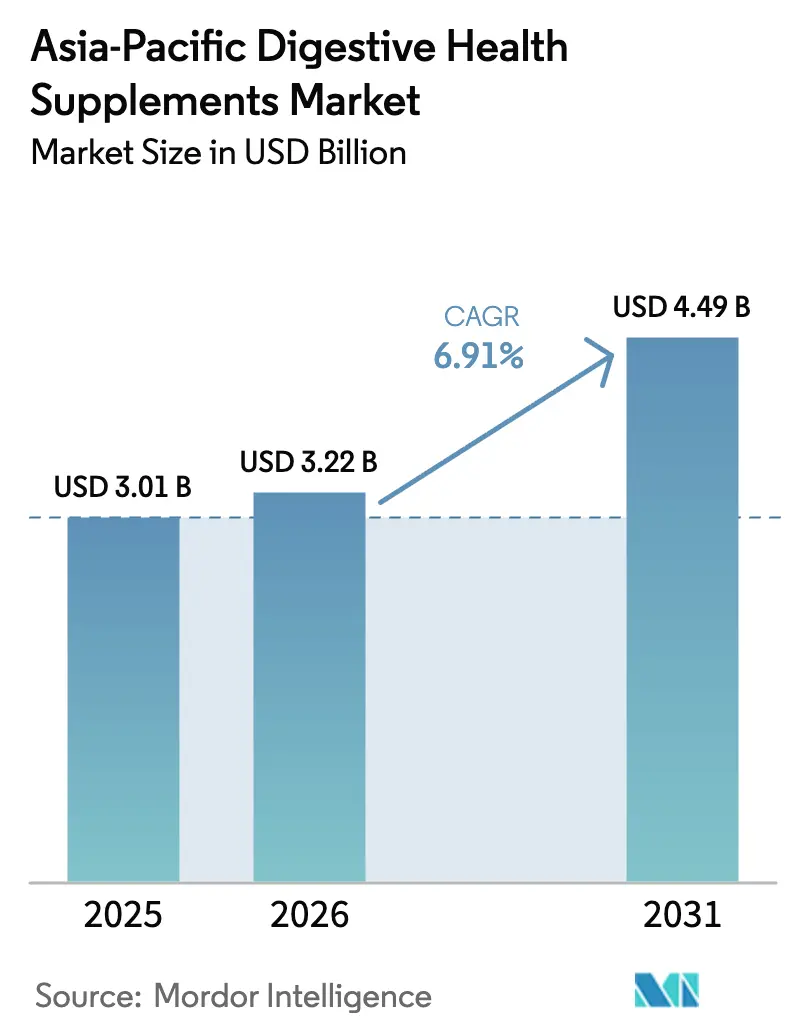

| Base Year Market Size (2025) | USD 3.01 Billion |

| Market Size (2026) | USD 3.22 Billion |

| Market Size (2031) | USD 4.49 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Digestive Health Supplements Market Analysis by Mordor Intelligence

The Asia-Pacific digestive health supplements market size was valued at USD 3.01 billion in 2025 and estimated to grow from USD 3.22 billion in 2026 to reach USD 4.49 billion by 2031, at a CAGR of 6.91% during the forecast period (2026-2031). The market growth is primarily influenced by the region's increasing emphasis on preventive healthcare measures, as consumers become more health-conscious and proactive about their well-being. The rising incidence of digestive disorders, coupled with a deeper understanding among consumers about how gut health influences immunity, mental well-being, and metabolic functions, has created substantial market opportunities. This trend is particularly evident in urban populations, where modern lifestyle factors have contributed to an increase in digestive health issues, resulting in sustained consumer demand for traditional probiotic supplements and innovative microbiome-modulating products. The market's expansion is further supported by improved healthcare infrastructure, rising disposable incomes, and greater accessibility to health information through digital platforms.

Key Report Takeaways

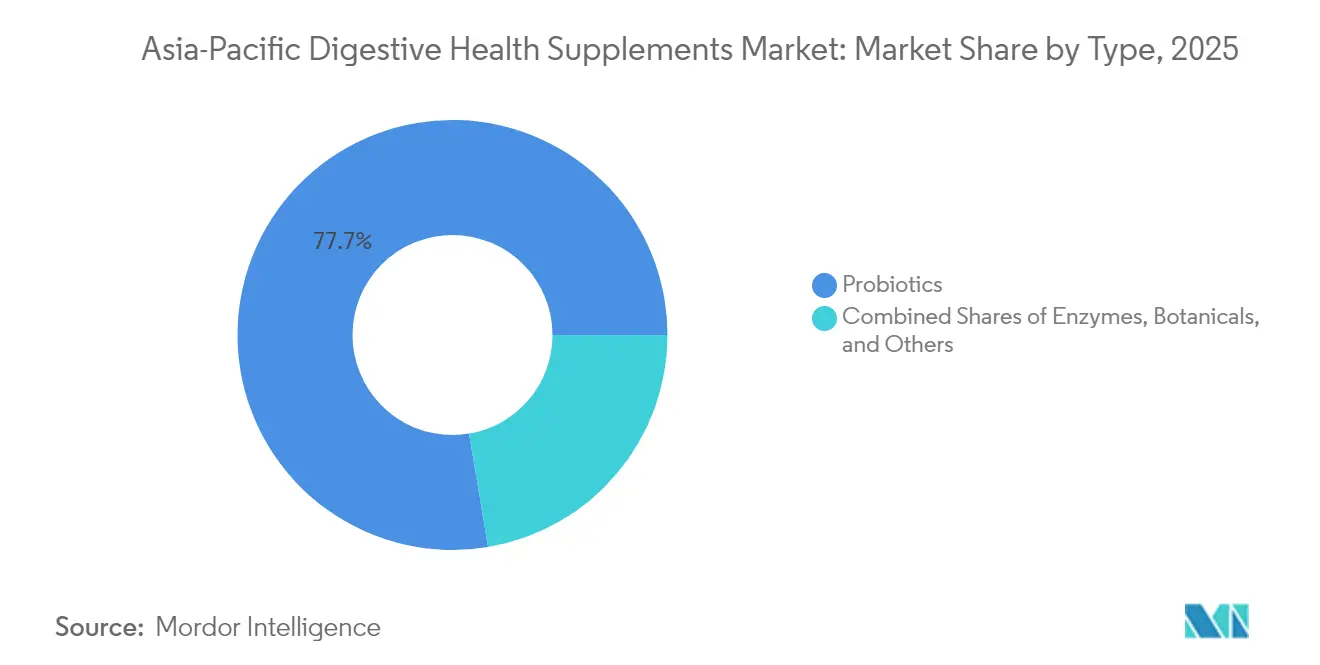

- By type, probiotics accounted for 77.65% of the Asia-Pacific digestive health supplements market share in 2025, prebiotics are projected to expand at an 8.04% CAGR to 2031.

- By form, capsules and softgels held 46.58% revenue share in 2025, gummies and chewables are advancing at a 7.74% CAGR through 2031.

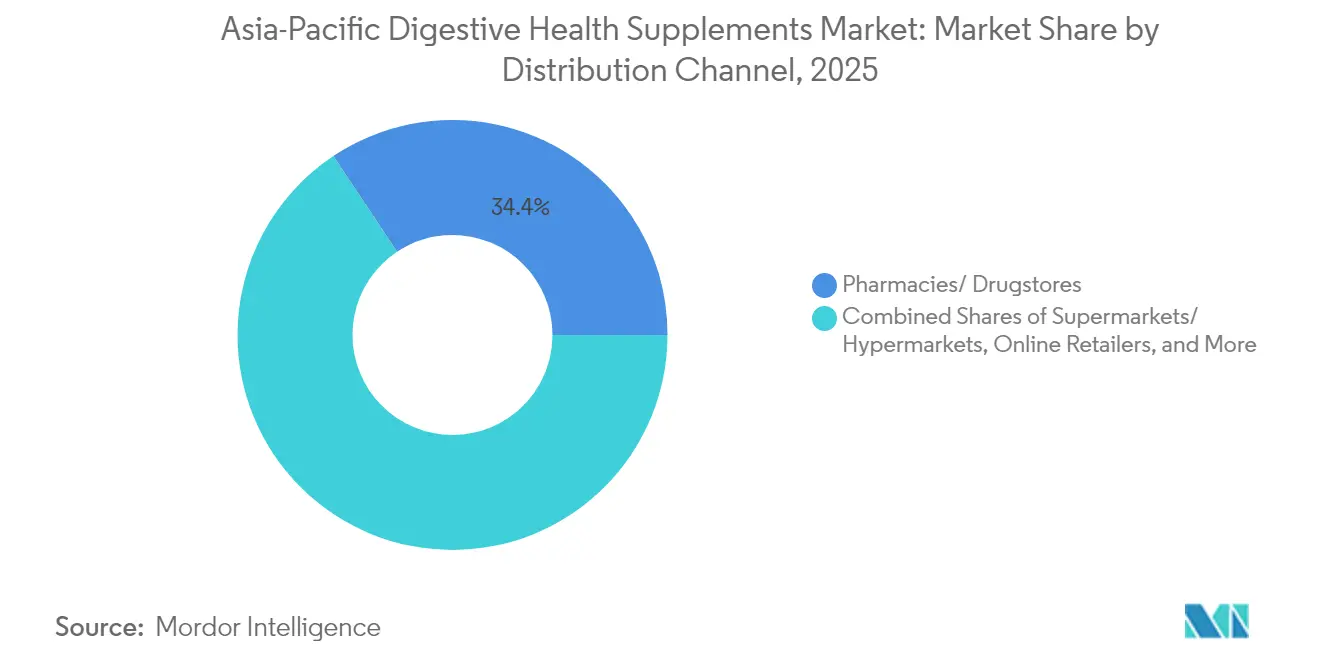

- By distribution channel, pharmacies and drugstores led with 34.35% revenue share in 2025; online retailers are forecast to record an 7.88% CAGR to 2031.

- By geography, Japan commanded 26.92% share of the Asia-Pacific digestive health supplements market size in 2025, while India is registering the highest projected CAGR at 8.11% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Digestive Health Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of digestive disorders prompting demand for supplements | +1.2% | APAC core, with highest impact in China, India, Japan | Medium term (2-4 years) |

| Increasing focus on preventive healthcare and natural health solutions | +1.0% | Global, with early adoption in Japan, Australia, Singapore | Long term (≥ 4 years) |

| Fueling fitness and sports nutrition trends promoting digestive health | +0.8% | Urban centers across APAC, particularly South Korea, Taiwan | Short term (≤ 2 years) |

| Growing demand for organic and plant-based digestive supplements | +0.7% | Japan, Australia, urban China and India | Medium term (2-4 years) |

| Expansion of dairy-free and allergen-free supplement options | +0.5% | Japan, South Korea, Australia with spillover to Southeast Asia | Medium term (2-4 years) |

| Greater penetration of e-commerce and online distribution channels | +0.9% | China, India, Southeast Asia with rapid digital adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Digestive Disorders Prompting Demand for Supplements

The rising prevalence of digestive diseases across Asia has generated sustained demand for therapeutic supplements, with the region experiencing a substantial burden from digestive conditions. This health trend stems from urbanization-related dietary changes, increased stress levels affecting gut function, and growing cases of inflammatory bowel conditions that traditional medications do not fully address. The aging populations in Japan, South Korea, and Singapore have increased the need for therapies that support digestive enzyme production and maintain microbiome balance. Research validating the effectiveness of specific probiotic strains like Bifidobacterium longum ES1 in treating irritable bowel syndrome has encouraged both medical professionals to recommend and patients to use these supplements. Healthcare systems, particularly in markets with developed infrastructure, are increasingly incorporating digestive health supplements into standard treatment protocols, shifting from treating symptoms to preventing digestive issues.

Increasing Focus on Preventive Healthcare and Natural Health Solutions

The increasing health consciousness among consumers has fundamentally shifted their preferences toward preventive supplementation, as evidenced by the substantial growth in online health supplement sales across China. This transformation extends beyond immediate immune support, with consumers adopting holistic wellness approaches and recognizing gut health as a cornerstone of overall well-being. In response to this trend, governments in China and India have implemented programs that effectively bridge traditional medicine with modern nutraceuticals while maintaining stringent safety regulations. The market has evolved to meet these changing consumer needs by introducing personalized nutrition offerings, as demonstrated by Calbee's innovative approach of providing microbiota-based granola recommendations. This shift in consumer behavior reflects a growing willingness to invest in preventive healthcare products, particularly when companies can validate health improvements through concrete measures such as biomarker measurements and systematic symptom tracking.

Fueling Fitness and Sports Nutrition Trends Promoting Digestive Health

The convergence of athletic performance optimization and gut health research has created premium market segments with higher profit margins and customer retention. In June 2025, Wecare Probiotics' Weizmannia coagulans BC99 received the Ingredient of the Year award in Sports Nutrition for enhancing protein absorption. Research shows that athletes with diverse gut microbiota exhibit better endurance and recovery times, increasing adoption among professional athletes and fitness enthusiasts. Sports nutrition provides an entry point for digestive health supplements to reach younger consumers, who typically focus on gut health only after experiencing digestive problems. In South Korea, partnerships between supplement manufacturers and fitness influencers are expanding market penetration beyond traditional health-conscious consumers. The premium pricing in sports nutrition enables companies to invest in advanced delivery systems and clinically validated formulations, creating product differentiation in the competitive market.

Growing Demand for Organic and Plant-Based Digestive Supplements

The plant-based supplement market continues to undergo significant transformation through innovative product formulations, exemplified by Nomura Dairy Products' strategic introduction of plant-based probiotic carrot juice in Japan's traditionally dairy-centric probiotic market. This evolution is further driven by increasing consumer awareness regarding the impact of agricultural chemicals on gut microbiome diversity and overall health outcomes, resulting in a stronger preference for organic formulations. The market's expansion is supported by regulatory bodies approving plant-based probiotic strains, particularly those derived from traditional fermented foods like Chinese sauerkraut, which maintains cultural connections while broadening ingredient options. Environmental consciousness, especially prevalent among younger consumer demographics, has created a notable shift toward supplements with minimal ecological footprints, providing competitive advantages to companies that implement and showcase sustainable sourcing and manufacturing practices. The premium pricing structure associated with organic certification not only presents opportunities for enhanced profit margins but also aligns with consumer values regarding personal health and environmental responsibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexities and inconsistent policies | -0.8% | APAC-wide, particularly affecting cross-border trade | Long term (≥ 4 years) |

| Stability and shelf-life issues affecting probiotic product viability | -0.6% | Tropical climates in Southeast Asia, India | Medium term (2-4 years) |

| Taste and palatability challenges affecting consumer adherence | -0.4% | Consumer-sensitive markets like Japan, South Korea | Short term (≤ 2 years) |

| Storage and refrigeration requirements limiting distribution | -0.5% | Infrastructure-limited regions in Southeast Asia, rural India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexities and Inconsistent Policies

The regulatory landscape across Asia-Pacific presents significant barriers to market expansion, as each jurisdiction maintains distinct approval processes, health claim requirements, and quality standards. These variations increase compliance costs and cause market entry delays. For example, Indonesia's registration requirements demand detailed scientific evidence for each probiotic strain, creating challenges for smaller companies while established multinationals benefit from their regulatory expertise. The absence of mutual recognition agreements between major markets requires companies to duplicate clinical studies and regulatory submissions, which increases development costs and constrains innovation investment. Regulatory updates in 2025 across multiple APAC jurisdictions have introduced additional compliance requirements that existing market participants must address while maintaining product availability. This regulatory environment particularly affects novel probiotic strains and innovative delivery formats without established precedents, creating market entry challenges for new products.

Stability and Shelf-Life Issues Affecting Probiotic Product Viability

The probiotic industry encounters significant technical challenges in tropical climates that affect product viability and consumer trust. Manufacturers must maintain specific viable cell counts to ensure optimal health benefits, but moisture exposure during production and storage creates substantial risks. In Southeast Asia and rural India, limited cold chain infrastructure restricts the distribution of temperature-sensitive formulations. While solutions such as desiccant-lined bottles and advanced packaging technologies can preserve stability without refrigeration, these increase production costs and reduce product accessibility in price-sensitive markets. Companies developing heat-stable probiotic strains, particularly spore-forming Bacillus strains, gain competitive advantages in challenging distribution environments. The industry faces ongoing quality control issues in maintaining viable cell counts throughout the supply chain, which can result in regulatory compliance problems and liability risks affecting brand reputation and market position. These challenges require manufacturers to balance product stability with market accessibility while maintaining stringent quality standards to ensure consumer safety and satisfaction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Probiotics Dominate While Prebiotics Accelerate

The microbiome supplement market demonstrates clear consumer preferences, with probiotics maintaining a substantial 77.65% market share in 2025. This dominance reflects years of consumer familiarity and robust scientific validation. In contrast, prebiotics have emerged as the market's growth driver, achieving an 8.04% CAGR through 2031, as consumers develop a more sophisticated understanding of microbiome optimization strategies.

The probiotic segment's market leadership builds on decades of research that validates strain-specific benefits for digestive health, immunity, and metabolic function. Major industry players, such as Morinaga Milk, are capitalizing on this trend by developing proprietary strains like Bifidobacterium longum subsp. infantis M-63 for specialized infant nutrition products in China. Within the broader market, enzymes maintain consistent demand for targeted digestive support applications, while botanicals benefit from increasing integration with traditional medicine practices. The "Others" category encompasses innovative postbiotic formulations and synbiotic combinations, representing the latest developments in microbiome science and product development.

By Form: Traditional Formats Lead Innovation Wave

The probiotic supplement market demonstrates a significant consumer inclination toward capsules and softgels, which currently maintain a substantial 46.58% market share in 2025. This strong market position reflects consumers' trust in these traditional delivery formats, primarily due to their reliability in providing precise, measured doses for daily supplementation. The market landscape is experiencing a notable transformation as gummies and chewables gain increasing acceptance among consumers, with projections indicating a robust growth rate of 7.74% CAGR through 2031. This shift in consumer preferences underscores a broader market trend where supplement users actively seek more enjoyable and convenient ways to incorporate probiotics into their daily routines, effectively addressing historical challenges with supplement compliance.

In the current market environment, capsules maintain their leadership position by offering superior protective qualities for sensitive probiotic strains against environmental degradation, while simultaneously providing controlled release mechanisms that enhance survival rates in the gastrointestinal tract. The World Health Organization's data highlighting over 1.7 billion annual cases of enteric diseases, coupled with an increasing prevalence of inflammatory conditions in developed regions, emphasizes the importance of effective probiotic delivery systems . While traditional tablets continue to offer manufacturers considerable production cost advantages, market dynamics indicate a clear shift toward more user-friendly alternatives. The market has evolved to accommodate diverse consumer needs through specialized delivery formats, with powders and granules serving specific segments such as infant nutrition and individualized dosing requirements. Additionally, the introduction of innovative delivery systems through functional foods and beverages represents an expanding market category that directly responds to modern consumers' lifestyle preferences and nutritional requirements.

By Distribution Channel: Digital Transformation Accelerates

Pharmacies and drugstores hold a dominant 34.35% market share in the distribution landscape in 2025. Their market leadership is attributed to established relationships with healthcare professionals who recommend products to patients, and consumer trust in medical retail environments. The online retail segment is experiencing the fastest growth, with a projected CAGR of 7.88% through 2031. This growth is driven by consumer preference for home delivery, competitive pricing, and wide product selections on digital platforms. India's expanding e-commerce market, supported by increased digital payment adoption, growing internet penetration, and rising online shopping preferences, provides favorable conditions for dietary supplement sales, including digestive health products .

Traditional pharmacy channels continue to maintain their strong position through consistent healthcare provider endorsements and consumer confidence in product quality, particularly crucial for digestive health supplements. Supermarkets and hypermarkets serve the mass market effectively but face increasing pressure on profit margins due to fierce online competition. Specialty and health stores have carved out their niche by offering premium products supported by expert consultation and carefully curated selections. The "Other Distribution Channels" category encompasses various sales approaches, including direct-to-consumer models and institutional sales channels, providing additional market penetration opportunities.

Geography Analysis

The Japanese market commands a significant 26.92% share of the Asia-Pacific digestive health supplements market in 2025, establishing itself as the regional leader. The country's well-structured FOSHU system provides companies with a clear pathway to make scientifically validated health claims. Japanese consumers have developed a sophisticated understanding of functional foods and probiotic benefits, supported by extensive clinical research and government-led preventive healthcare initiatives. The market's quality standards have been further enhanced by recent government regulations that mandate additional documentation for probiotic functional foods. This leadership position is exemplified by the strategic partnership between Kirin Holdings and Blackmores in March 2025, which introduced LC-Plasma powder to the Taiwan market.

India has emerged as the most dynamic market in the region, projecting an impressive 8.11% CAGR through 2031. This rapid growth stems from increasing middle-class purchasing power and supportive government policies for nutraceutical manufacturing under the FSSAI framework. The market's potential is underscored by the April 2024 joint venture between Nestlé India and Dr. Reddy's Laboratories, combining global expertise with local market knowledge. The FSSAI's comprehensive framework, which establishes clear standards for composition and labeling of health supplements, has created a robust foundation for market growth while ensuring consumer protection.

Other regional markets, including Australia, South Korea, Indonesia, Thailand, and Singapore, continue to develop with their distinct characteristics and opportunities. The ASEAN region's progress in regulatory harmonization for dietary supplements is creating more accessible market entry pathways while maintaining quality standards. China presents a particularly interesting market dynamic, with its post-1990 generation driving demand for innovative product formats and digital purchasing channels. Additionally, China's aging demographic, with 22% of the population aged 60 and above in 2024, represents a substantial consumer base for targeted nutritional products .

Competitive Landscape

The Asia-Pacific digestive health supplements market demonstrates moderate fragmentation, which has opened doors for both established multinational corporations and specialized regional players. These companies are actively pursuing market share through distinct market positioning and forming strategic partnerships within the industry. Established companies maintain their competitive edge by leveraging their extensive regulatory expertise, robust clinical validation processes, and well-developed distribution infrastructure. In contrast, newer market entrants are carving their niche by introducing innovative delivery systems, implementing personalized nutrition approaches, and developing direct-to-consumer business models.

Companies like Cell Biotech exemplify successful market leadership through their impressive 12-year dominance in Korean probiotic exports and systematic global expansion initiatives. Industry participants are making substantial investments in advanced packaging solutions, comprehensive microbiome analysis capabilities, and innovative product formats. These investments serve as key differentiators, enabling companies to establish unique market positions and command premium pricing in increasingly competitive market environments.

The market presents significant opportunities in previously underserved segments, particularly in pediatric applications, sports nutrition crossover products, and specialized formulations targeting metabolic health and cognitive function enhancement. Strategic acquisitions in the biotechnology sector, illustrated by Danone's strategic purchase of The Akkermansia Company for its specialized pasteurized Akkermansia muciniphila MucT strain, demonstrate the industry's commitment to advancing probiotic development. Regulatory frameworks established by FSSAI, MFDS, and other APAC regulatory bodies create substantial entry barriers, naturally favoring companies with established regulatory affairs capabilities and robust clinical research infrastructure. The market also offers unique opportunities for companies that can successfully bridge traditional medicine practices with modern biotechnology, particularly in regions where traditional medicine holds cultural significance. This integration of traditional and modern approaches enables companies to develop scientifically validated formulations while respecting established cultural health practices.

Asia-Pacific Digestive Health Supplements Industry Leaders

Abbott Laboratories

Amway

Herbalife Nutrition Ltd.

Bayer AG

GNC Holdings LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Daewoong Pharmaceutical launched Haapssen, a seven-in-one supplement containing omega-3, magnesium, vitamins B, C, D, lactic acid bacteria, and astaxanthin, targeting the growing demand for convenient multi-nutrient products in South Korea's health functional food market

- July 2025: Cell Biotech announced expansion into Thailand and Philippines markets with its DUOLAC premium probiotic brand, leveraging 12 years of Korean probiotic export leadership and strong Southeast Asian partnerships to capture growing health supplement demand

- June 2025: Danone acquired The Akkermansia Company, a Belgian biotics firm specializing in Akkermansia muciniphila MucT strain, to accelerate global growth of this EFSA-approved pasteurized strain for gut barrier function and metabolic health applications

Asia-Pacific Digestive Health Supplements Market Report Scope

Digestive supplements are health supplements that are generally consumed to enhance the digestive process.

The Asia-Pacific digestive health supplements market is segmented by type, distribution channel, and geography. By type, the market is segmented into prebiotics, probiotics, enzymes, and other types. By distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies and drugstores, online retailers, and other distribution channels. It provides an analysis of emerging and established countries across the Asia-Pacific, including China, Japan, India, Australia, and the Rest of Asia-Pacific. For each segment, the market sizes and forecasts are provided in terms of value in USD million.

By Type

| Prebiotics |

| Probiotics |

| Enzymes |

| Botanicals |

| Others |

By Form

| Capsules and Softgels |

| Tablets |

| Gummies and Chewables |

| Powders and Granules |

| Others |

By Distribution Channel

| Supermarkets/ Hypermarkets |

| Pharmacies/ Drugstores |

| Online Retailers |

| Other Distribution Channels |

By Geography

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| Rest of Asia-Pacific |

| By Type | Prebiotics |

| Probiotics | |

| Enzymes | |

| Botanicals | |

| Others | |

| By Form | Capsules and Softgels |

| Tablets | |

| Gummies and Chewables | |

| Powders and Granules | |

| Others | |

| By Distribution Channel | Supermarkets/ Hypermarkets |

| Pharmacies/ Drugstores | |

| Online Retailers | |

| Other Distribution Channels | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific digestive health supplements market in 2026?

The Asia-Pacific digestive health supplements market size reached USD 3.22 billion in 2026 and is projected to grow at a 6.91% CAGR to 2031.

Which country currently leads sales?

Japan holds the largest share at 26.92% in 2025, supported by FOSHU-backed health claims and an aging population.

What is the fastest-growing product type?

Prebiotics are expanding at an 8.04% CAGR as consumers seek ingredients that nourish existing gut microbes.

Why are gummies gaining popularity?

Gummies deliver pleasant taste, maintain viable probiotic counts without refrigeration, and therefore improve adherence, helping them post a 7.74% CAGR through 2031.

Which sales channel is rising the quickest?

Online retailers are projected to register an 7.88% CAGR owing to convenience, broader assortment, and personalized purchasing experiences.

Page last updated on: