Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

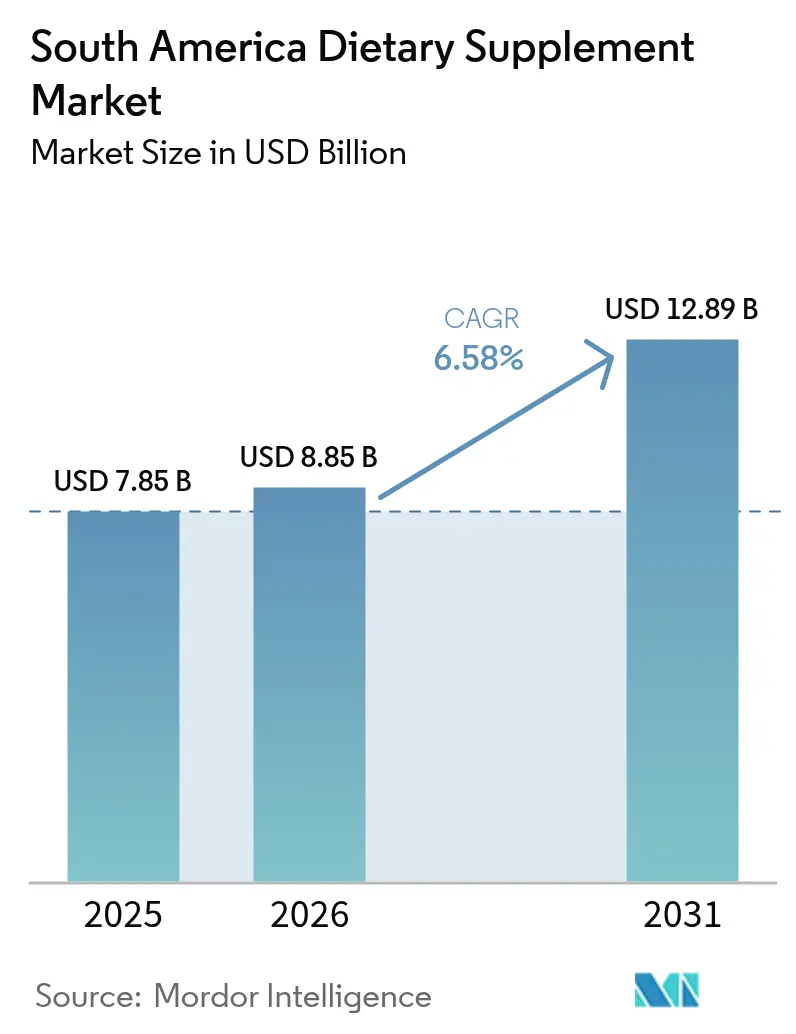

| Base Year Market Size (2025) | USD 7.85 Billion |

| Market Size (2026) | USD 8.85 Billion |

| Market Size (2031) | USD 12.89 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Dietary Supplement Market Analysis by Mordor Intelligence

The South America dietary supplements market size is expected to increase from USD 8.85 billion in 2026 to reach USD 12.89 billion by 2031, growing at a CAGR of 6.58% over 2026-2031. Consumers across Brazil, Argentina, Colombia, Chile, and Peru are shifting from reactive sick-care to proactive nutrient optimization, partly because non-communicable diseases cause 77% of regional deaths while households still pay 32.4% of total health costs out-of-pocket. Pandemic-related declines in life expectancy of 2.9 years heightened interest in immune resilience. Regulatory tightening under ANVISA, INVIMA, and ANMAT improves product quality, while e-commerce platforms expand reach even as real incomes fall. Multinational research ad development commitments and clean-label innovation support premiumization, yet local price wars squeeze margins, creating a dual-speed competitive field within the South America dietary supplements market.

Key Report Takeaways

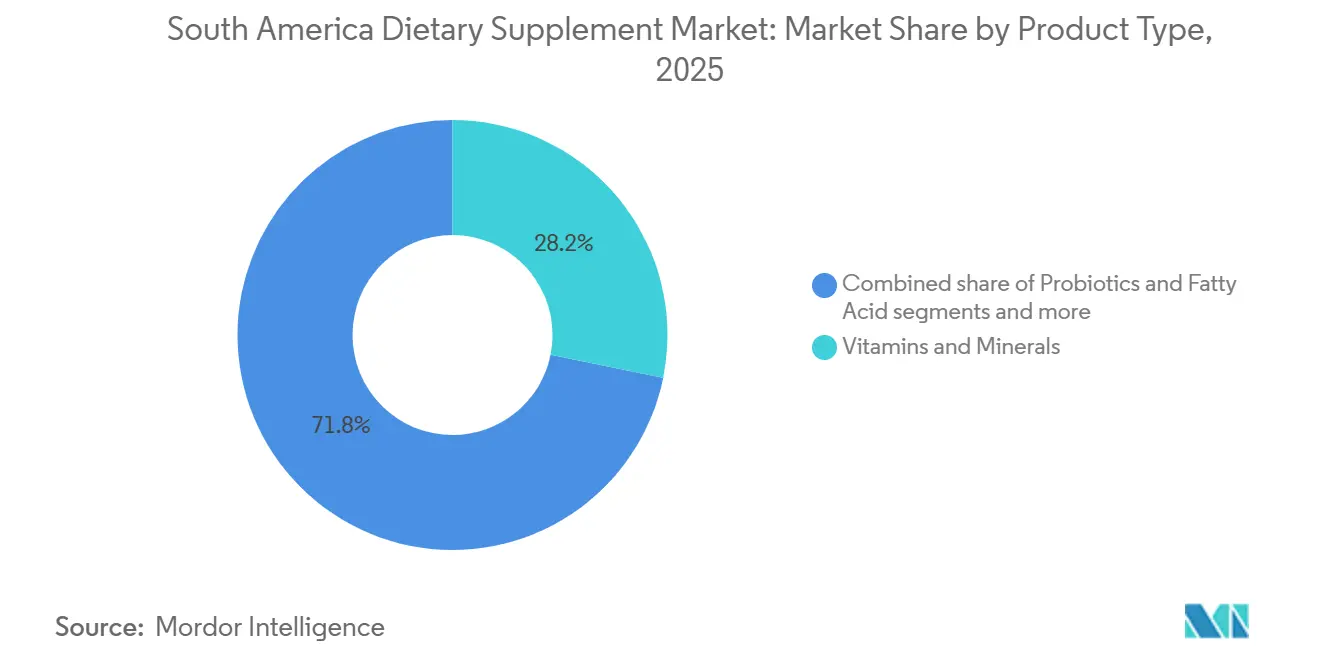

- By product type, vitamins and minerals led with 28.18% revenue share of the South America dietary supplements market in 2025, while probiotics are projected to advance at a 7.62% CAGR through 2031.

- By form, capsules and softgels captured 39.28% of the South American dietary supplements market share in 2025, whereas gummies are forecast to register the fastest 8.02% CAGR to 2031.

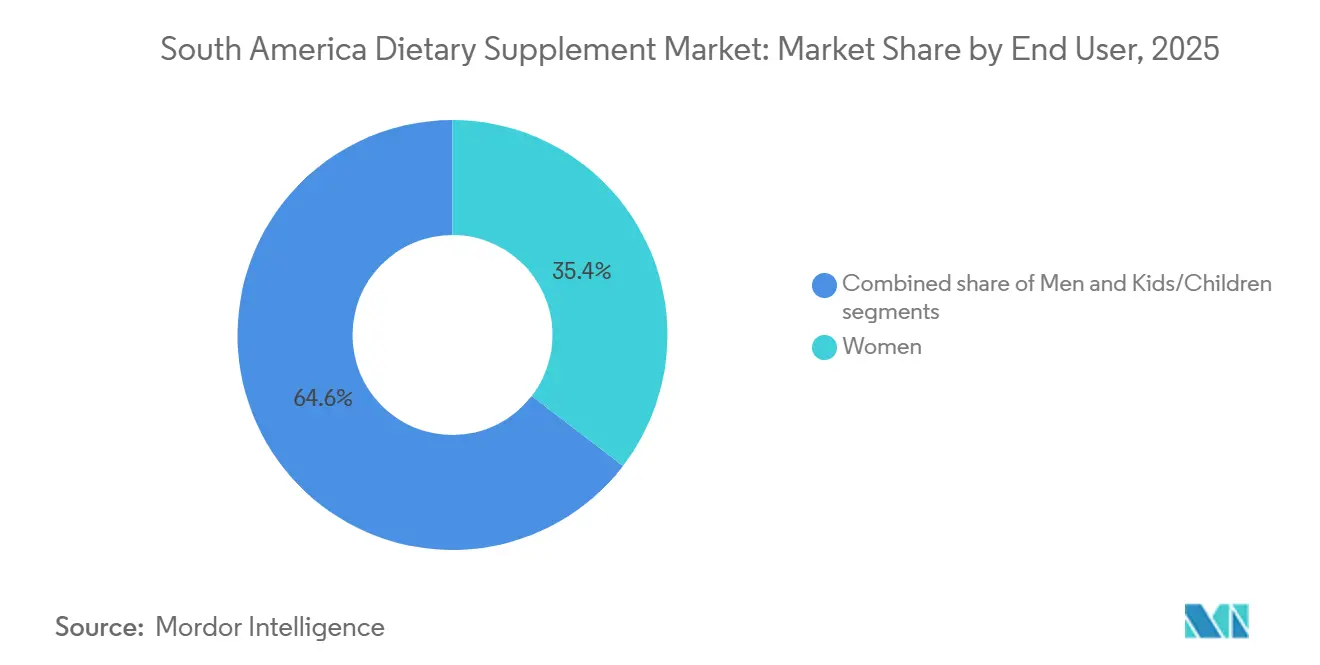

- By end user, women accounted for 35.42% sales in 2025, but the kids and children segment is poised for a 9.11% CAGR between 2026 and 2031.

- By geography, Brazil commanded 60.28% revenue in 2025, while Colombia is expected to post the highest 7.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Dietary Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Focus On Preventive Healthcare | +1.2% | Global, with highest intensity in Brazil, Chile, Argentina | Medium term (2-4 years) |

| Supplements Targeting Women Consumers Fueling Growth | +0.9% | Brazil, Colombia, Argentina, urban centers across region | Medium term (2-4 years) |

| Growing Preference For Clean-Label, Plant-Based And Vegan Formulas | +0.8% | Brazil, Chile, Argentina, metropolitan areas | Long term (≥ 4 years) |

| Healthy-Ageing Focus Accelerating Multivitamin Uptake Among Consumers | +1.0% | Brazil, Argentina, Chile, with spillover to Colombia, Peru | Long term (≥ 4 years) |

| E-Commerce Growth Enhances Supplement Accessibility And Market Reach | +0.7% | Brazil, Argentina, Colombia, Chile | Short term (≤ 2 years) |

| Research And Development Investments Drive Innovative Product Development And Targeted Solutions | +0.6% | Global, led by multinational R&D hubs serving South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increased Focus on Preventive Healthcare

In South America, out-of-pocket health expenditures accounted for 32.4% of total health spending, ranking among the highest globally, according to the World Health Organization[1]Source: World Health Organization, “Global Health Expenditure Database,” who.int. This significant financial burden forces households to independently fund wellness interventions, often as a preventive measure to avoid the high costs associated with advanced medical care, as reported by the World Health Organization. Non-communicable diseases, such as diabetes, hypertension, and cardiovascular disorders, contributed to 77% of deaths in the region, highlighting an urgent demographic need for nutrient-based strategies to mitigate health risks. Additionally, the lack of adequate primary care services in rural and peri-urban areas has further fueled the demand for self-care solutions. Consumers increasingly rely on over-the-counter supplements as a substitute for physician consultations, driven by accessibility challenges and cost considerations. This shift has transformed the role of dietary supplements, positioning them as essential tools for proactive health management rather than optional wellness products. Consequently, this change has significantly influenced both the frequency of purchases and the composition of consumer baskets.

Supplements Targeting Women Consumers Fueling Growth

In 2025, women constituted 35.42% of end-user demand, driven by the growing availability of life-stage-specific formulations tailored to address key health concerns such as prenatal nutrition, menopause management, and bone health. Iron deficiency continues to be a significant issue among women of reproductive age across South America, while calcium and vitamin D supplementation remain critical for preventing osteoporosis in post-menopausal women. Brazil's Rede Cegonha maternal health initiative, supported by the Brazilian Ministry of Health, played a pivotal role in raising awareness about the importance of folic acid and DHA supplementation during pregnancy[2]Source: Brazilian Ministry of Health, “Rede Cegonha,” saude.gov.br. This initiative laid a strong clinical foundation for the growth of commercial prenatal brands. In 2024 and 2025, leading companies such as Nestlé, Bayer, and Abbott expanded their prenatal product portfolios. These companies leveraged endorsements from gynecologists and implemented pharmacy-based educational campaigns to strengthen their market presence. The segment benefits from a higher willingness-to-pay among female consumers, who prioritize products with transparent ingredient lists and clinical validation. This consumer preference enables brands to command premium pricing compared to mass-market multivitamins.

Growing Preference for Clean-Label, Plant-Based and Vegan Formulas

Recent surveys indicate a growing acceptance of plant-based alternatives among consumers, with younger demographics leading this shift due to their focus on sustainability and animal welfare. Millennials and Generation Z, in particular, are highly attentive to product transparency, often examining supplement labels in detail and using mobile apps to cross-check ingredients. These groups are especially attracted to clean-label formulations that exclude synthetic colors, artificial preservatives, and genetically modified ingredients. A significant trend among vegan consumers is the preference for pectin-based gummy vitamins, which have replaced traditional gelatin-based options. Furthermore, botanical extracts such as turmeric, ginger, and echinacea are gaining popularity as natural substitutes for synthetic active ingredients. Despite this growing interest, affordability remains a key challenge. Plant-based supplements are typically priced 15% to 25% higher than conventional alternatives, which limits their accessibility primarily to upper-middle-income households and above.

Healthy-Ageing Focus Accelerating Multivitamin Uptake Among Consumers

In 2024, 15.1% of Brazil's population consisted of individuals aged 60 and above, with this proportion expected to nearly double, reaching 29.4% by 2050. Similarly, Colombia's senior population accounted for 13.9% in 2024 and is projected to rise significantly to 28.6% by 2050. In Argentina, 16.2% of the population fell into this age group in 2024, with forecasts indicating an increase to 24.5% by 2050. This demographic transformation is driving a growing demand for specialized health formulations tailored to the needs of aging populations. Bone-health products that combine calcium, vitamin D, and magnesium are becoming increasingly popular. Joint-support supplements containing glucosamine and chondroitin are also witnessing rising demand, alongside cognitive-health products formulated with omega-3 fatty acids and B-vitamins. Furthermore, multivitamins specifically designed for seniors are addressing challenges related to age-related nutrient malabsorption by incorporating higher concentrations of vitamin B12, folate, and antioxidants. Physician recommendations during routine geriatric consultations play a pivotal role in promoting these products. Such endorsements not only encourage initial trials but also foster repeat purchases, even among older adults who were previously reluctant to adopt supplement use.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence Of Counterfeit Products Hampering Growth | -0.4% | Brazil, Argentina, Peru, informal retail channels | Short term (≤ 2 years) |

| Rising Consumer Scepticism Toward Synthetic Additives And Mega-Dose Safety Concerns | -0.3% | Brazil, Chile, Argentina, urban educated consumers | Medium term (2-4 years) |

| Tighter Regulations On Dietary Supplements And Borderline Products | -0.5% | Brazil, Colombia, Argentina, formal retail channels | Medium term (2-4 years) |

| Price Wars From Local Producers Reduce Profit Margins | -0.6% | Brazil, Argentina, Colombia, mass-market segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Presence of Counterfeit Products Hampering Growth

In January 2026, ANVISA banned four supplement brands for failing to meet safety and quality standards[3]Source: ANVISA, “RDC 843/2024,” anvisa.gov.br. Meanwhile, in October 2025, INVIMA issued Alert 131-2025, cautioning consumers about illegal supplements in Colombia. Counterfeit products not only erode consumer trust in legitimate brands but also amplify the damage when negative media highlights adverse events tied to these substandard formulations. In Brazil, Argentina, and Peru, informal retail channels remain susceptible to unregistered products that lack proper labeling, traceability, or verification of active ingredients. Despite tightening regulations, enforcement gaps endure. Resource-limited agencies find it challenging to inspect cross-border e-commerce shipments and keep tabs on small-scale distributors. When counterfeit versions of their products inflict harm, legitimate manufacturers risk reputational damage. This has led them to invest in anti-counterfeiting technologies, including holographic labels, QR-code authentication, and blockchain-based supply-chain tracking.

Rising Consumer Skepticism Toward Synthetic Additives and Mega-Dose Safety Concerns

Millennials and Generation Z increasingly prefer clean-label products, showing skepticism toward synthetic colors, artificial preservatives, and high-potency formulations perceived as exceeding physiological needs. Reflecting regulatory caution, ANVISA has restricted melatonin supplementation to 0.21 milligrams per day for adults, contrasting with the mega-dose trends prevalent in North American markets. Public health authorities are promoting balanced diets over supplementation through consumer education campaigns, creating challenges for brands marketing products as meal replacements rather than nutritional complements. Safety concerns have grown due to adverse events linked to excessive intake of vitamin A, vitamin D, and iron, leading consumers to seek physician advice before starting supplementation. This trend benefits brands that emphasize clinical validation, transparent ingredient sourcing, and dosage formulations aligned with recommended dietary allowances, while disadvantaging mass-market products that rely on high-potency claims to differentiate themselves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Probiotics Outpace Traditional Categories

In 2025, vitamins and minerals accounted for 28.18% of the market, reflecting strong consumer trust in multivitamins, vitamin C, and calcium supplements. Probiotics, however, are projected to grow at a 7.62% CAGR through 2031 as gut-health science moves from research to mainstream wellness. Bayer's September 2025 launch of Iberoflora probiotics in Latin America, featuring strains like Lactobacillus rhamnosus GG and Bifidobacterium lactis BB-12, underscores the focus on strain-specific formulations backed by clinical trials. In Brazil and Argentina, where traditional medicine remains significant, herbal supplements with botanicals like chamomile, ginger, and turmeric are gaining traction as natural alternatives to synthetic products. Omega-3 fatty acids, derived from fish oil and algae, support cardiovascular and cognitive health, but consumption in South America remains below WHO recommendations due to limited cold-water fish availability and high costs.

Digestive enzymes such as lactase, amylase, and protease address gastrointestinal sensitivities, while collagen peptides, amino acids, and specialized formulations target athletic performance and beauty-from-within needs. Regulatory clarity from ANVISA's Normative Instruction 28/2018, updated multiple times in 2024, has encouraged innovation by defining permissible ingredients, dosages, and health claims while ensuring consumer safety. Probiotics' rapid growth is driven by clinical validation, physician endorsements, and rising awareness of the gut-brain connection, making them a strategic focus for manufacturers aiming to differentiate beyond standard multivitamins.

By Form: Gummies Disrupt Traditional Delivery Formats

In 2025, capsules and softgels accounted for 39.28% of the market share, driven by established manufacturing, precise dosing, and broad consumer acceptance. Gummies, however, are expected to grow at an 8.02% CAGR through 2031, fueled by taste-masking technology and non-pill formats appealing to millennials and pediatric consumers. Gummy production requires specialized equipment and expertise to maintain ingredient stability in humid climates like Brazil and Colombia, creating barriers to entry that benefit established players such as Church & Dwight, Bayer, and Nature's Bounty. Pectin-based gummies have replaced gelatin among vegan consumers, while sugar-free options address concerns about added sugar. However, their premium pricing, 15% to 25% higher than tablets, limits adoption to upper-middle-income households. Tablets remain the most affordable option, attracting price-sensitive consumers and supporting high-potency formulations for larger doses.

Powders serve sports nutrition and meal-replacement needs with dosing flexibility and flavor customization, while liquids cater to pediatric and geriatric populations with swallowing difficulties. Niche formats like effervescent tablets, sublingual strips, and transdermal patches offer convenience or bioavailability benefits, justifying higher prices. Under RDC 843/2024, ANVISA enforces uniform notification requirements across all formats, ensuring gummy manufacturers meet the same standards as capsule producers. The rapid growth of gummies reflects a consumer shift toward wellness products combining efficacy with sensory appeal. This trend pressures established brands to reformulate portfolios or risk losing market share to digitally native brands prioritizing user experience over traditional delivery systems.

By End User: Kids and Children Segment Accelerates

In 2025, women accounted for 35.42% of end-user demand, driven by prenatal, postnatal, menopause, and bone health formulations. Meanwhile, the kids and children segment is expected to grow at a 9.11% CAGR through 2031, as parents increasingly focus on pediatric immunity, cognitive development, and growth support post-pandemic. Despite government fortification efforts, Vitamin A, D, iron, and zinc deficiencies persist among South American children, with stunting remaining a concern in lower-income areas. Picky eating and limited dietary diversity are pushing parents toward multivitamin gummies and chewable tablets, which improve compliance by masking nutrient taste. Regulatory challenges, including age-specific dosing and safety standards, are significant, with ANVISA and INVIMA enforcing strict labeling and marketing rules to prevent overconsumption.

Men represent the other end-user segment, focusing on sports nutrition, testosterone support, and cardiovascular health. However, growth in this segment lags behind women and children due to lower supplement adoption rates and cultural norms discouraging preventive health behaviors. Rising female workforce participation, linked to higher disposable income and health awareness, supports this segment, while intergenerational wealth transfers drive pediatric supplement demand, with grandparents often funding purchases. Brands targeting women and children differentiate themselves through clinical endorsements, pediatrician recommendations, and pharmacy education campaigns, enabling premium pricing and higher margins compared to mass-market multivitamins.

By Distribution Channel: Online Retail Gains Momentum

In 2025, health and wellness stores accounted for 28.62% of the market share, benefiting from specialized products, trained staff, and consumer trust. However, online retail channels are expected to grow at a 7.25% CAGR through 2031, driven by convenience, competitive pricing, and direct-to-consumer fulfillment. Brazil's health and wellness e-commerce reached USD 5.2 billion in 2025, growing 18% year-over-year, led by Mercado Livre, Amazon, Drogasil, and Raia. Supermarkets and hypermarkets offer mass-market access and encourage impulse purchases, while other channels include pharmacies, direct-selling networks like Grupo Omnilife's multi-level marketing, and institutional channels for hospitals and clinics. By 2024, modern retail channels surpassed 50% of total sales, with e-commerce growing 44% in the first half of the year despite macroeconomic challenges.

Online platforms leverage subscription models to boost customer lifetime value and improve inventory predictability. Features like detailed product information, customer reviews, and ingredient transparency align with millennial and Generation Z preferences. Regulatory compliance remains a challenge, as ANVISA's notification requirement under RDC 843/2024 applies to both online and offline channels, necessitating robust quality assurance and traceability systems. Health stores face slower growth due to urban market saturation and competition from pharmacy chains expanding supplement offerings to capture higher-margin categories. Meanwhile, the rapid growth of online retail highlights a structural shift toward digital commerce, set to reshape distribution economics and competition by 2031.

Geography Analysis

In 2025, Brazil accounted for 60.28% of the market share, reaffirming its position as South America's largest economy and most populous nation. The population aged 60 and above, at 15.1% in 2024, is expected to reach 29.4% by 2050, driving demand for bone-health, joint-support, and cognitive-health products. ANVISA's mandatory notification under RDC 843/2024, effective September 1, 2024, increased compliance costs but enhanced product quality and consumer trust by eliminating irregular supplements. Nestlé's USD 224 million investment over three years, announced in October 2025, aims to establish Brazil as a regional innovation hub, with Puravida receiving USD 45 million for product development and export expansion into Mexico and Argentina.

E-commerce platforms like Mercado Livre, Amazon, Drogasil, and Raia drove health and wellness sales to USD 5.2 billion in 2025, an 18% year-over-year increase, supported by expanded supplement assortments and subscription-based deliveries. Vitamedic's USD 17 million factory in Anápolis, inaugurated in December 2025, plans to triple capacity by 2027, reflecting domestic manufacturing growth to meet rising demand. Colombia is the fastest-growing region, with a 7.36% CAGR through 2031, driven by INVIMA's automatic-registration framework and a growing middle class. The population aged 60 and above, at 13.9% in 2024, is projected to reach 28.6% by 2050, boosting demand for healthy-aging products. INVIMA's Alert 131-2025, issued in October 2025, warned against illegal supplements, reinforcing enforcement to protect legitimate manufacturers. Bayer's September 2025 launch of Iberoflora probiotics in Colombia, following rollouts in Mexico, Guatemala, Costa Rica, and Ecuador, highlights confidence in the market's potential. Argentina, Chile, and Peru hold smaller shares but show unique trends.

Argentina's population aged 60 and above, at 16.2% in 2024, is expected to reach 24.5% by 2050, driving demand for bone-health and cardiovascular supplements. ANMAT's Disposition 11362/2024 exempted dietary supplements from front-of-pack warning labels, easing regulatory requirements compared to processed foods and beverages. Smaller markets like Paraguay, Uruguay, and Bolivia benefit from cross-border distribution and free-trade agreements but face growth challenges due to limited purchasing power and reliance on informal retail channels.

Regulatory Landscape

Dietary supplements across South America operate under country-specific food and health surveillance regimes, making market entry and portfolio standardization dependent on local sanitary pathways. In Brazil, ANVISA governs supplements under RDC 243/2018, with the region also seeing tighter enforcement via the mandatory notification framework under RDC 843/2024 (effective September 1, 2024), raising the bar for ingredient compliance, labeling, and permitted claims across formats.

Colombia requires sanitary registration for manufacture, import, and commercialization under INVIMA, anchored in Decree 3249 of 2006, while Argentina frames suplementos dietarios within the Argentine Food Code (CAA) under Article 1381 and oversight by ANMAT and CONAL. Ecuador runs a sanitary notification process for supplements via ARCSA, reinforcing the need for multi-country regulatory mapping, local representation, and disciplined claim substantiation to avoid borderline food-drug classifications and enforcement actions.

Competitive Landscape

In South America, dietary supplement manufacturers establish niches through targeted marketing and specialized offerings, resulting in a moderately consolidated market. EMS’s acquisition of Vitamine-se provided the company with access to an extensive distribution network, enabling advertising across 86,000 points of sale. This strategy positioned personalized vitamins and mineral supplements as premium products. Collaborations with influencers and celebrities, such as footballer Neymar Jr.’s launch of the Next10 brand, enhance brand visibility and appeal to tech-savvy consumers. Companies are focusing on niche segments, including women’s health and children’s supplements, by developing tailored formulations and packaging that highlight efficacy, quality, and lifestyle alignment.

Leading players utilize technology to gain a competitive edge and boost product appeal. Funtrition, leveraging its proprietary gummy technologies, GummyGels and Layer-G, is scaling up production for both domestic and export markets. Additionally, e-commerce consolidations, such as Merama's, enable multiple brands to operate on unified platforms, improving consumer targeting through digital analytics. Tools like AI-driven questionnaires and customized formulations not only enhance engagement and loyalty but also differentiate brands in a competitive market.

In South America's supplements market, competitive dynamics are shaped by strategic partnerships, acquisitions, and regulatory compliance. Key developments, such as EMS’s acquisition of Vitamine-se and Merama’s takeover of Growth Supplements, highlight a trend of consolidation, expanded distribution, and streamlined marketing. Collaborations with local manufacturers help international players comply with ANVISA standards. These strategies benefit established companies with strong quality and regulatory frameworks, creating barriers for smaller competitors and reinforcing the market's moderate concentration while fostering sustained growth.

South America Dietary Supplement Industry Leaders

Abbott Laboratories

Bayer AG

Herbalife Nutrition Ltd.

Amway Corp.

Glanbia PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Local manufacturing scale-up in Brazil is opening whitespace for faster lead times, private label production, and localized formulations that fit country-specific notification and labeling requirements. Concrete capacity signals include Pronutrition announcing an R$ 11 million investment to build a new 8,500 square meter industrial plant in Valinhos, Brazil, targeting a ramp in output capacity up to 18.6 million units per month. The expansion strengthens regional B2B and white-label manufacturing capability, improving supply reliability for brands selling through pharmacies and online platforms.

Opportunity is also forming around clinically positioned and strain- or ingredient-specific products that navigate tighter claim scrutiny while differentiating beyond commodity multivitamins. Probiotics and targeted actives gain distribution leverage through partnerships and regulated launches, illustrated by NVP Healthcare signing an exclusive supply agreement with Brazil's Marjan Farma for a probiotic ingredient and Kyowa Hakko's Setria glutathione entering Chile via a finished product launched by Nutrapharm following SEREMI-related approval steps. With e-commerce already a major route to market in Brazil and enforcement focusing on irregular products, brands that pair compliant dossiers with traceability tools (for example, QR authentication) and pharmacy education can compete more effectively against counterfeit-heavy informal channels.

Recent Industry Developments

- July 2026: NVP Healthcare expanded its probiotic collaboration with Marjan Farma by extending the scope to additional Latin American markets, enabling broader access to the NVP-1702 line in the region and strengthening distribution alongside ongoing regulatory coordination.

- June 2026: Pronutrition announced an R$ 11 million investment to build a new 8,500 square meter industrial plant in Valinhos, Brazil, targeting a ramp in output capacity up to 18.6 million units per month. The expansion enhances regional B2B and white-label manufacturing capability and improves supply reliability for pharmacy and online channels.

- July 2024: NXT USA introduced Digexin under its Motility brand in Brazil, combining okra pod and winter-cherry root extracts for digestive and stress-related positioning. The launch added to the botanical and functional digestive pipeline and highlighted growing demand for non-traditional actives in mainstream supplement retail.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the sales value of dietary supplements consumed in South America, counted at the point they are sold through retail and professional channels. It includes products taken to add nutrients or support wellness goals, in formats such as tablets, capsules, powders, liquids, and gummies.

Scope exclusions: This sizing does not include prescription drug therapies, conventional packaged foods and beverages, or personal care items even if they carry wellness claims.

Segmentation Overview

- By Type

- Vitamins And Minerals

- Herbal Supplements

- Fatty Acids

- Probiotics

- Enzymes

- Other Product Types

- By Form

- Tablets

- Capsules And Softgels

- Powders

- Gummies

- Liquids

- Others

- By End User

- Men

- Women

- Kids/Children

- By Distribution Channel

- Supermarkets/Hypermarkets

- Health And Wellness Stores

- Online Retail Channels

- Other Distribution Channels

- By Country

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest Of South America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the demand pool and supply landscape, so assumptions do not drift without measurable anchors. We typically review public health and nutrition indicators, consumer expenditure context, and trade movement for supplement-type products before building the model. For South America, sources include national health surveillance and statistics offices, customs and foreign trade portals, central bank inflation and FX series, and regional bodies that publish nutrition and wellness indicators.

We also review company filings, investor decks, retailer disclosures, and reputable press to understand how products are priced and pushed through retail and pharmacy channels, and to cross-check any abrupt movements. Patent databases are used to flag ingredient and formulation activity, and an import/export shipment-level database is applied selectively to sanity-check cross-border flows where local disclosures are less consistent. The desk sources listed here are illustrative only, and additional public references were used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs were collected through expert interviews and structured surveys across manufacturers, ingredient suppliers, distributors, and retail and pharmacy channel participants in South America. We also spoke with functional leaders who manage pricing, regulatory affairs, and category growth, so assumptions on formats, claims, and channel mix could be adjusted using on-ground feedback. When a country-level data point differed, the checks were repeated across major economies and other countries in the region to keep the model consistent.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | APAC: 42% |

| Mid tier: 46% | Functional/Unit leaders: 27% | EMEA: 37% |

| Smaller Players: 18% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach once, where South America supplement demand is reconstructed from category consumption signals, channel-level sales patterns, and macro indicators, then filtered through pricing and mix assumptions. To keep outputs grounded, we corroborated totals using selective bottom-up checkpoints such as sampled average selling price by format, checkout basket values from key channels, and supplier and distributor sense checks on annual volumes.

Key inputs used in the model include population by age bands, prevalence of lifestyle-related conditions that drive supplementation intent, household spending and consumer confidence direction, inflation and FX movement for USD normalization, and shifts in channel mix toward e-commerce and modern trade. Because pricing can move faster than volume in this category, ASP progression was tracked using inflation-adjusted price steps and validated through interview feedback on promotions and pack-size changes. Forecasts were developed using scenario analysis supported by shortlists of demand drivers agreed by local experts, followed by an ARIMA-style time series check on the historical trend to avoid overreaction to one-off years. Where bottom-up checkpoints were incomplete for smaller countries, gaps were handled with per-capita demand proxies and then reviewed against trade and retail signals.

Data Validation & Update Cycle

Outputs were cross-checked against independent signals such as import trends, reported category growth in public updates, and macro constraints that typically limit discretionary spending. Outliers were flagged, and assumptions were reworked when implied per-capita spend or price levels looked inconsistent with known channel realities.

A multi-step internal review was followed, where model logic, year-over-year movements, and country rollups were checked before sign-off. If interviews indicated a major change, such as a regulatory shift, a new tax, or a sudden channel disruption, the team re-contacted sources to confirm direction and timing. The report is refreshed annually, and material events trigger interim updates, with a final pre-delivery check so the numbers align with the latest available signals.

Mordor Intelligence's South America Dietary Supplement Market Size Compared Against Other Published Estimates

Published market numbers for dietary supplements in South America can vary widely, even when the titles sound similar. The gaps usually come from what gets counted as a supplement, how multi-country coverage is handled, and how price inflation and currency conversion are applied year to year.

Some published figures blend Central America with South America, and some also treat broad nutraceutical foods as part of supplements, which expands the value pool. In Mordor Intelligence, the count is limited to dietary supplement products sold in South America, and the USD series is kept consistent by controlling for FX timing and checking channel mix so that price-led spikes are not mistaken for pure demand growth.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.85 B (2025) | |

| Global Consultancy A | USD 8.12 B (2024) | Uses a Central and South America scope and a different base year, which can lift totals by adding countries and by applying a separate price and channel structure for 2024. |

| Industry Publisher B | USD 11.33 B (2021) | Uses an older base year and reports in nominal terms for that period, and the reported level can be inflated if adjacent health products are grouped into supplements or if currency conversion timing is not aligned across countries. |

Overall, the spread is mainly explained by geography coverage, base-year choice, and how the supplement basket is defined. By keeping the product scope tight, aligning FX and inflation handling, and rechecking channel pricing logic with primary inputs, our estimate stays traceable to clear demand and price variables that can be repeated each update.

Key Questions Answered in the Report

How large will supplement sales become in South America by 2031?

Sales are forecast to reach USD 12.89 billion by 2031, expanding at a 6.58% CAGR.

Which country is projected to grow fastest through 2031?

Colombia is expected to register the highest 7.36% CAGR, driven by regulatory streamlining and a rising middle class.

Why are probiotics gaining share?

Clinically validated strains and growing awareness of gut-health benefits push probiotics to a 7.62% CAGR, outpacing traditional vitamins.

What format is expanding quickest?

Gummies lead with an 8.02% CAGR because taste-masking and vegan formulations attract millennials and children.

Page last updated on: