Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Japan Data Center Processor Market Report Segments the Industry Into Processor Type (GPU, CPU, FPGA, AI Accelerator), Application (Advanced Data Analytics, AI/ML Training and Inferences, and More), Architecture (x86, Non-X86 (ARM, Power and Other Processors)), Data Center Type (Enterprise, Colocation, Cloud Service Providers). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

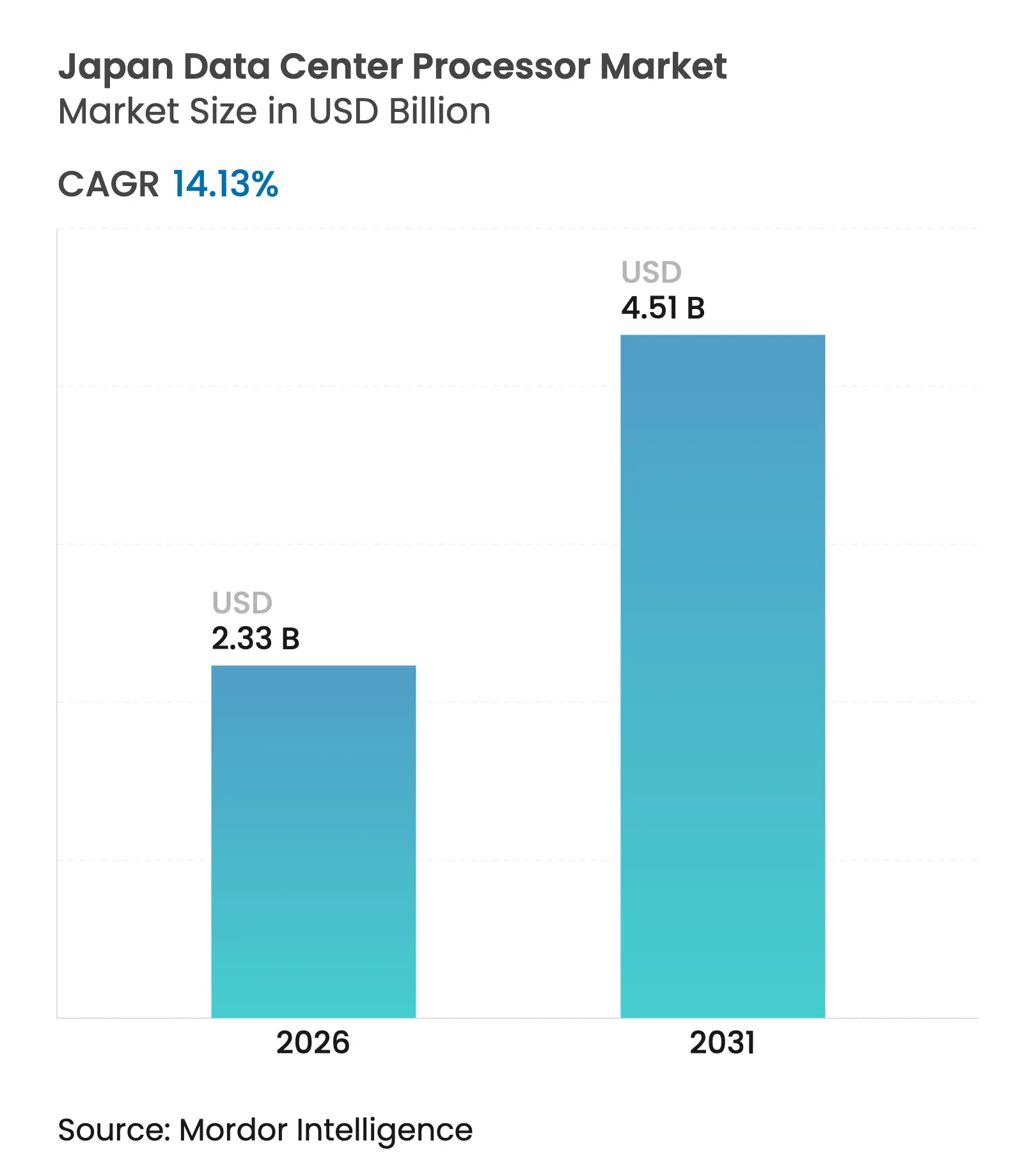

| Market Size (2026) | USD 2.33 Billion |

| Market Size (2031) | USD 4.51 Billion |

| Growth Rate (2026 - 2031) | 14.13 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Japan data center processor market size was valued at USD 2.04 billion in 2025 and estimated to grow from USD 2.33 billion in 2026 to reach USD 4.51 billion by 2031, at a CAGR of 14.13% during the forecast period (2026-2031). The growth reflects Tokyo’s rise as a regional AI hub, the USD 67 billion national semiconductor revival program, and hyperscaler investments that localize capacity for generative-AI workloads. Fiber-optic penetration among the top three OECD countries, combined with strong edge-computing demand for autonomous mobility, sustains high bandwidth and low-latency requirements. Liquid-cooling uptake improves energy efficiency for high-TDP chips, aligning with national net-zero targets. Traditional CPUs remain prominent, yet AI accelerators and ARM-based designs gain momentum as enterprises emphasize inference efficiency and power savings.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surge

in AI, IoT and 5G-led compute demand

Surge

in AI, IoT and 5G-led compute demand

| +3.2% | Japan nationwide, with concentration in Tokyo and Osaka metropolitan areas | Medium term (2-4 years) | (~) %

Impact on CAGR Forecast:

+3.2%

|

Geographic

Relevance

:

Japan

nationwide, with concentration in Tokyo and Osaka metropolitan areas

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Government

digital-transformation and green-IT incentives

Government

digital-transformation and green-IT incentives

| +2.8% | National, with early gains in government cloud adoption and smart city initiatives | Long term (≥ 4 years) | |||

Enterprise

cloud-migration boom

Enterprise

cloud-migration boom

| +2.1% | Global with Japan-specific data sovereignty requirements | Short term (≤ 2 years) | |||

Expansion

of edge-computing for autonomous mobility

Expansion

of edge-computing for autonomous mobility

| +1.9% | Japan automotive corridors, particularly Toyota and Honda manufacturing regions | Medium term (2-4 years) | |||

On-shore

advanced packaging enabling near-memory compute

On-shore

advanced packaging enabling near-memory compute

| +1.7% | Kumamoto, Hokkaido semiconductor clusters | Long term (≥ 4 years) | |||

Net-zero

targets accelerating liquid-cooled high-TDP chips

Net-zero

targets accelerating liquid-cooled high-TDP chips

| +1.5% | Japan data center hubs in Tokyo, Osaka, and emerging regional facilities | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in AI, IoT and 5G-led compute demand

SAKURA Internet’s early installation of 2,000 NVIDIA H100 GPUs delivers 2 EFLOPS capacity and signals a broader acceleration of AI infrastructure.[1]SAKURA Internet, “Ishikari Data Center Adds NVIDIA H100 GPUs to Reach 2 EFLOPS,” sakura.ad.jp Nearly 74% of Japanese enterprises pursue digital-transformation programs that shift analytics workloads toward LLMs, deepening demand for specialized accelerators. The Generative AI Accelerator Challenge eases hardware shortages for startups, while connected-car platforms stream data from more than 1 million vehicles, reinforcing the need for distributed edge processing. NTT’s real-time 4K inference chip further highlights the move beyond general-purpose CPUs to domain-specific silicon suited to 5G use cases.

Government digital-transformation and green-IT incentives

Japan earmarked JPY 10 trillion for AI and semiconductors and set a 40% energy-efficiency mandate for data-center assets.[2]Japan External Trade Organization, “Japan’s Digital Transformation Strategy and Semiconductor Incentives,” jetro.go.jp The Digital Agency promotes domestic cloud platforms that keep sensitive data on-shore, prompting demand for processors meeting strict security and performance thresholds. Immersion-cooling pilots show 94% cuts in cooling energy, and edge-AI start-up EdgeCortix won JPY 4 billion to develop chiplets with five-times efficiency gains. Semiconductor subsidies under the Economic Security Promotion Law encourage local manufacturing, fostering component resilience and speeding adoption of energy-efficient architectures.

Enterprise cloud-migration boom

Oracle’s USD 8 billion decade-long expansion and similar hyperscaler moves demonstrate corporate preference for compliant, low-latency clouds.[3]Nikkei Asia, “Oracle pledges USD 8 billion for Japan data centers,” asia.nikkei.com Hybrid strategies ask processors to balance legacy compatibility with next-generation AI inference, forcing suppliers to optimize memory bandwidth and energy draw. Financial services and manufacturing firms spearhead migrations that demand zero-downtime and hardened security, sharpening focus on processors with hardware encryption and telemetry-driven power scaling. The shift redirects budgets from on-premises refreshes to subscription-based performance, accelerating refresh cycles inside cloud data halls.

Expansion of edge-computing for autonomous mobility

Renesas’ R-Car V4H SoC offers 34 TOPS at 16 TOPS/W, supporting Level 2+ autonomy under ASIL-D safety. Aisin’s edge AI chip co-developed with Tohoku improves power efficiency tenfold, while Denso’s Data Flow Processor introduces a distinct category tailored to latency-critical control loops. Manufacturing facilities adopt compact, rugged processors for predictive maintenance as labor shortages climb. The convergence of 5G and real-time visualization across smart factories pushes designs that excel at streaming inference with minimal cooling overhead.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

GPU

supply-chain shocks and geopolitical tension

GPU

supply-chain shocks and geopolitical tension

| -2.4% | Global with specific impact on Japan-China-US technology corridors | Short term (≤ 2 years) | (~) %

Impact on CAGR Forecast:

-2.4%

|

Geographic

Relevance

:

Global

with specific impact on Japan-China-US technology corridors

|

Impact

Timeline

:

Short

term (≤ 2 years)

|

High

CAPEX and power-tariff burden

High

CAPEX and power-tariff burden

| -1.8% | Japan nationwide, particularly affecting smaller data center operators | Medium term (2-4 years) | |||

Scarcity

of sub-5 nm domestic foundry capacity

Scarcity

of sub-5 nm domestic foundry capacity

| -1.3% | Japan domestic market with spillover to regional supply chains | Long term (≥ 4 years) | |||

Strict

data-sovereignty rules limit custom foreign CPUs

Strict

data-sovereignty rules limit custom foreign CPUs

| -0.9% | Japan domestic market with implications for multinational operations | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

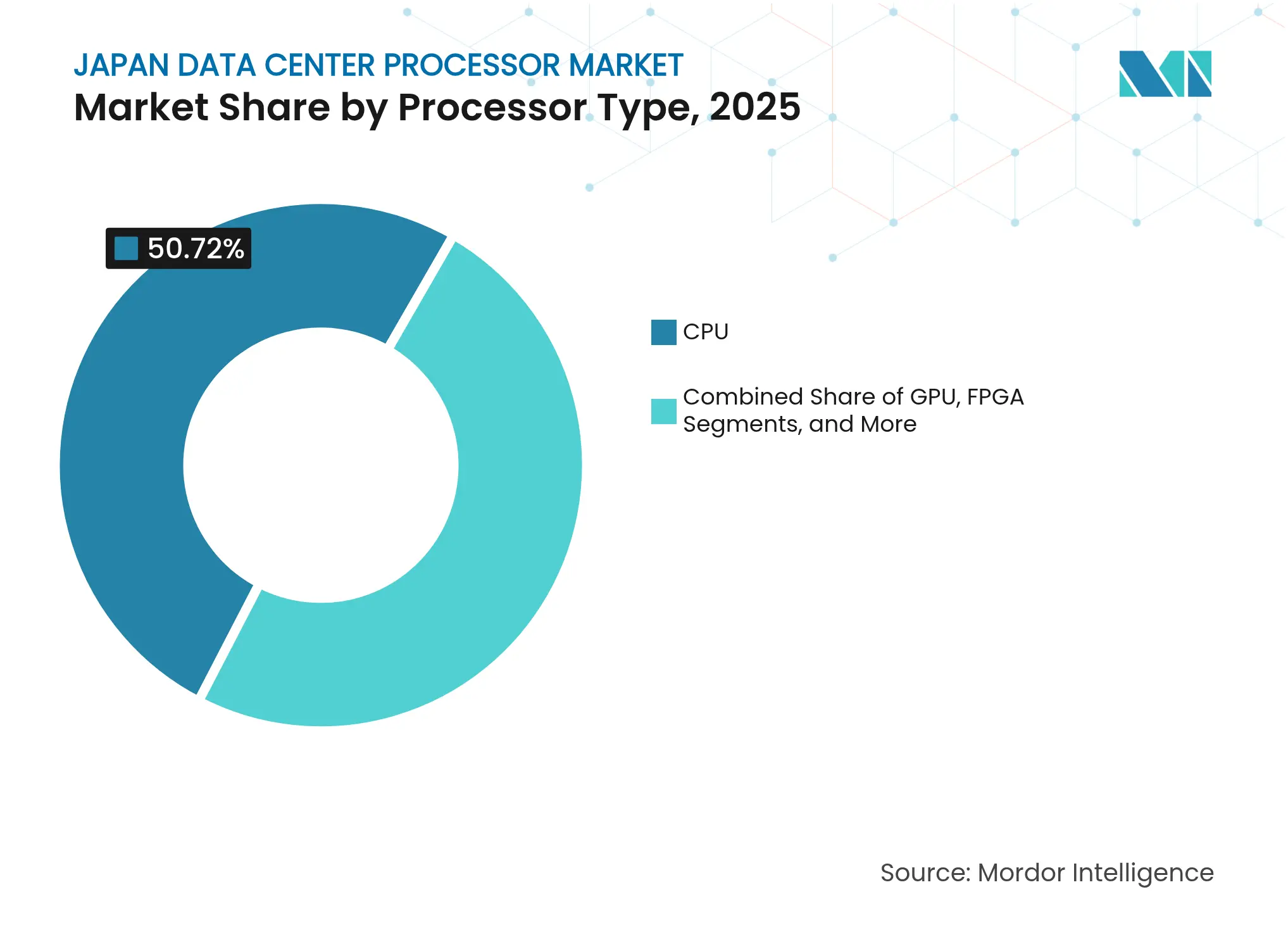

By Processor Type: AI accelerators challenge CPU dominance

CPU devices still held 50.72% of Japan data center processor market share in 2025. Revenue stability derives from their compatibility layer for legacy workloads and general-purpose orchestration. However, hyperscalers now qualify AI accelerators on parity pricing, reducing total CPU slots per rack. AI chips post a 17.02% CAGR to 2031 as model-training clusters dominate new build-outs. Sustained demand for inference nodes across language translation, video analytics, and fraud detection keeps accelerator utilization high, intensifying attention on power density and memory bandwidth.

The Japan data center processor market benefits from innovations such as EdgeCortix’s SAKURA-II platform, which offers 60 TOPS inside a sub-75-W envelope. Fujitsu’s ARM-based MONAKA, scheduled for 2027, targets 40% energy savings by applying many-core 3D stacking. Korean entrant Rebellions positions its ATOM chip at data-center inference with claimed 5× efficiency versus legacy GPUs. Together, these contenders erode monolithic CPU influence by offering specialized architectures that better align with green-IT financing criteria.

Note: Segment shares of all individual segments available upon report purchase

By Application: Advanced analytics drives fastest growth

AI/ML training and inference workloads controlled 33.42% of Japan data center processor market size in 2025. Enterprise adoption of ChatOps and automated customer engagement sustains large multi-GPU clusters. Yet the advanced-analytics segment grows quickest at 16.12% CAGR. Streaming data pipelines for digital twins and predictive maintenance demand processors optimized for high I/O throughput rather than peak floating-point rates. NEC’s generative-AI framework, which reaches GPT-4-level output at 10× speed, underscores this pivot toward application-specific tuning.

Insurance, logistics, and retail firms implement real-time fraud detection and inventory optimization, requiring tight coupling of CPUs, GPUs, and FPGA appliances. Security workloads gain momentum under data-sovereignty laws, pushing adoption of processors with embedded secure enclaves. Telecommunication operators virtualize network functions on accelerators that cut latency for 5G slicing. The Japan data center processor industry thus sees heterogeneous deployment models where each application dictates a distinct silicon footprint.

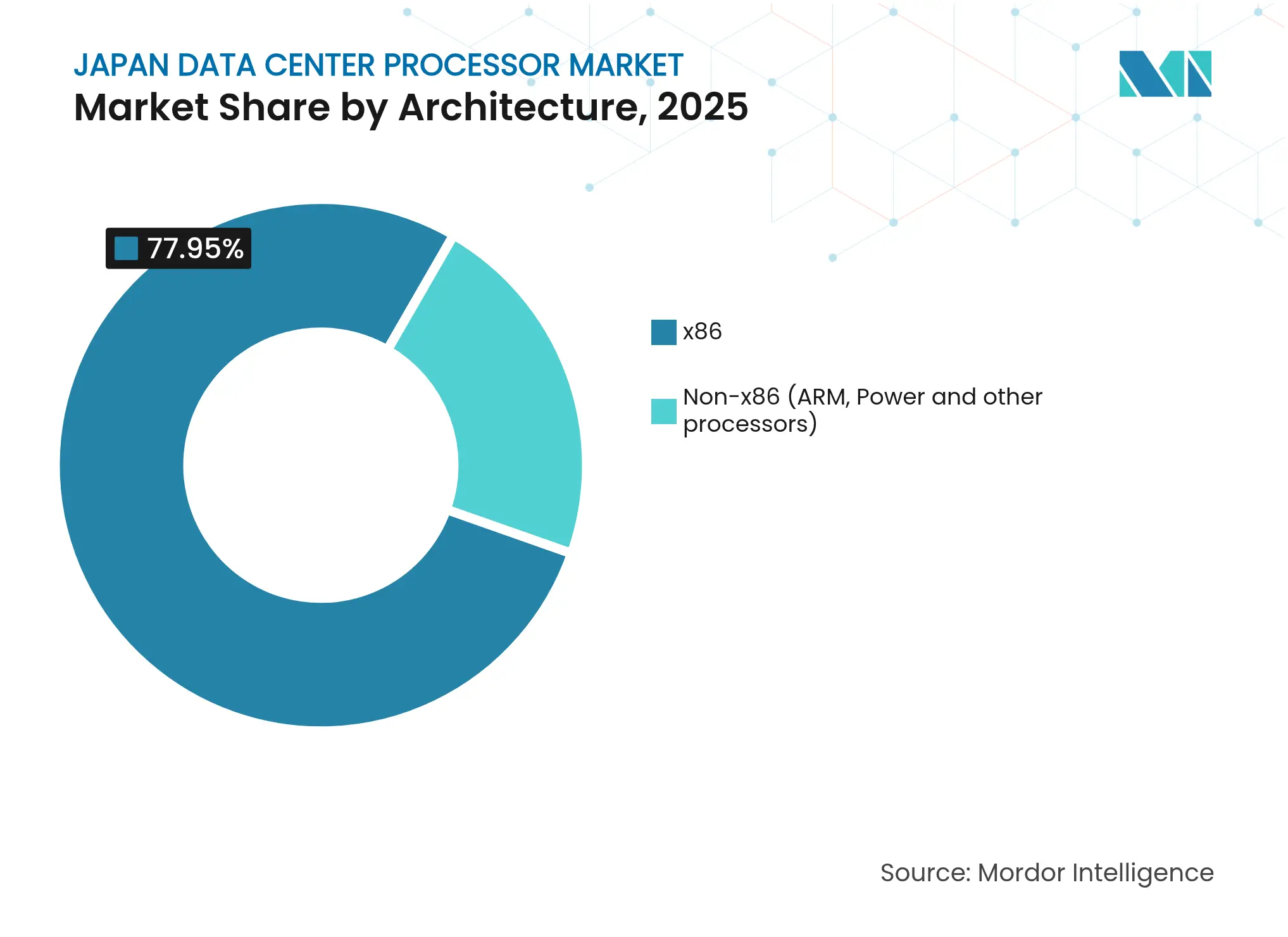

By Architecture: Non-x86 solutions gain momentum

x86 platforms retained 77.95% share in 2025, but non-x86 devices expand at 17.65% CAGR. ARM servers appeal to cloud providers seeking license flexibility and lower thermals. The Japan data center processor market sees open-source RISC-V cores entering pilot deployments for AI inference appliances. Fujitsu partners with Supermicro to integrate MONAKA boards into liquid-cooled racks, demonstrating how architectural choice interlinks with mechanical design.

As energy-use disclosure rules tighten, procurement teams compare total watts per inference rather than SPECint scores. AMD’s record 45% GPU retail share in Japan illustrates a readiness to diversify suppliers when value-added metrics align. Tenstorrent collaborates with Japan Advanced Semiconductor Technology Center on 2 nm RISC-V accelerators that promise open tool-chains, lowering software porting overhead. Consequently, the Japan data center processor market evolves toward architecture-agnostic orchestration layers that optimize for workload intent.

Note: Segment shares of all individual segments available upon report purchase

By Data-Center Type: Cloud providers lead infrastructure evolution

Cloud operators controlled 46.05% revenue in 2025 and advance at 18.72% CAGR, signaling a decisive shift to off-premises compute. Oracle, Microsoft Azure, and AWS deepen local regions to meet data-sovereignty requirements, embedding AI training clusters near metro hubs. Colocation providers still attract enterprises unwilling to relinquish hardware control, creating mixed-tenant halls equipped with reseller-friendly accelerators. The Japan data center processor market size for edge micro-sites is expanding as smart-factory rollouts necessitate ultra-low latency.

SoftBank’s Osaka campus converts an LCD plant to a 150 MW AI facility with 240 MW expansion headroom, illustrating how brownfield assets shorten ramp-up schedules. Equinix aligns with SAKURA Internet to pool GPU capacity across global exchange points, demonstrating multi-cloud synergy. NTT’s USD 16.4 billion consolidation of NTT Data harmonizes processor procurement across managed services, wholesale, and retail lines of business, reinforcing purchase volumes that influence supplier roadmaps.

Tokyo stands as Asia’s second-largest data-center hub after Singapore and closes on Beijing in total capacity expansion. The concentration supports latency-sensitive finance and government workloads and anchors new AI clusters that demand proximity to large language corpora. Osaka gains prominence through SoftBank’s 150 MW transformation of a Sharp plant, and Equinix’s fourth IBX facility, forming a twin-hub topology that improves disaster-recovery options without cross-border traffic.

Hokkaido and Kumamoto emerge as semiconductor and data-center clusters benefitting the Japan data center processor market. Cooler climates in Hokkaido reduce compressor loads and enable free-air-cooling for GPU farms, cutting energy costs and aligning with net-zero pledges. Kumamoto’s proximity to TSMC’s fabrication lines fosters an ecosystem of advanced packaging, promoting near-memory compute for AI accelerators.

Southern coastal regions integrate LNG power with compute loads, as shown by SAKURA Internet’s collaboration with JERA in Tokyo Bay. Proximity to submarine cables offers international bandwidth, important for cross-Pacific training datasets. Government incentives channel investment into regional cities to de-risk overconcentration in Kanto and Kansai, creating distributed micro-hubs that rely on ARM-based micro-servers for edge inference.

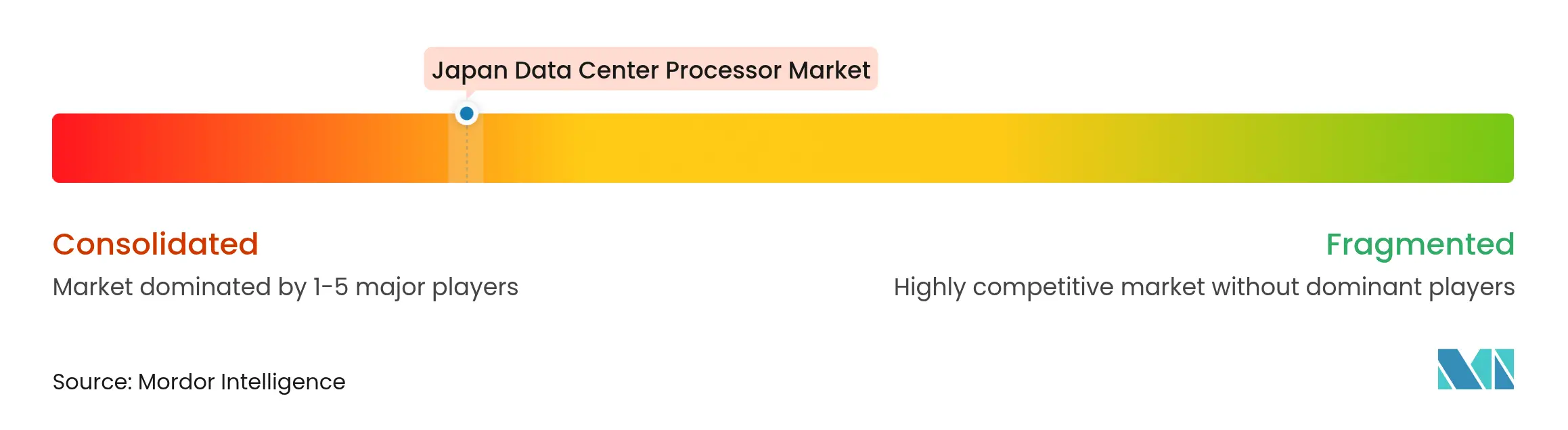

Market Concentration

The Japan data center processor market features moderate concentration. Intel, AMD, and NVIDIA hold sizeable bases, yet rapid shifts to AI accelerators allow domestic firms to capture niche share. Intel’s Q4 2024 revenue slipped 7% year-over-year, while AMD’s data-center segment surged 57%, illustrating divergent positioning as workloads pivot to energy-efficient inference. NVIDIA maintains leadership in training, but challengers exploit gaps in cost-per-query metrics.

Japanese innovators expand. Fujitsu’s MONAKA targets 40% lower power, Patents around 3D many-core implementation anticipate liquid-cooling integration. EdgeCortix’s SAKURA-II and Denso’s Data Flow Processor address specific verticals, from telecom edge to automotive. Korean entrant Rebellions opens a Tokyo office for direct sales of ATOM accelerators, reflecting regional supplier diversification.

Ecosystem partnerships intensify. Fujitsu works with Supermicro and Nidec on rack-level power efficiency, while NTT and Intel explore silicon photonics for optical I/O. Preferred Networks shifts from AI software to custom chip design through a Mitsubishi joint venture, aligning algorithmic stacks with hardware. The Japan data center processor industry therefore rewards firms that combine silicon advances with verticalized software tooling.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SEGMENTATION

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Data centers house and manage critical applications and data, using computing and storage networks for efficient delivery. Processors—GPUs, CPUs, and TPUs—are central to their operation. GPUs handle multitasking, excelling in graphics rendering and AI tasks. CPUs, with multi-core architecture, support parallel processing. TPUs, designed for machine learning, stand out from GPUs, which have transitioned from graphics to AI applications.

The Japan Data Center Processor Market is Segmented by Processor Type (CPU, GPU, FPGA, AI Accelerators), by Application (Advanced Data Analytics, AI/ML Training and Inferences, High Performance Computing, Security and Encryption, Network Functions, and Others), by Architecture (x86 and Non-x86 (ARM, Power and other processors), and by Data Center Type (Enterprise, Colocation and Cloud Service Providers). The Report Offers the Market Size and Forecasts for all the Above Segments in Terms of Value (USD).

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.