Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.82 Billion |

| Market Size (2026) | USD 3.99 Billion |

| Market Size (2031) | USD 4.91 Billion |

| Growth Rate (2026 - 2031) | 4.25% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Battery Market Analysis by Mordor Intelligence

The Japan Battery Market size is expected to increase from USD 3.82 billion in 2025 to USD 3.99 billion in 2026 and reach USD 4.91 billion by 2031, growing at a CAGR of 4.25% over 2026-2031.

The measured expansion mirrors manufacturers shifting from commodity lithium-ion output toward premium solid-state formats and stationary storage solutions, supported by the Ministry of Economy, Trade and Industry’s multiyear subsidy program. Panasonic’s cost-compression roadmap for 4680 cylindrical cells, Toyota-backed joint ventures that anchor domestic plug-in hybrid demand, and GS Yuasa’s solid-state pilot line form the technological spine behind short-term revenue growth. Export-oriented electric-vehicle strategies by Toyota, Nissan, and Honda keep factory utilization high while the U.S. Inflation Reduction Act rules steer cathode sourcing away from China. Ongoing investments by JOGMEC in Chilean lithium and Australian nickel deposits signal a concerted effort to reduce raw-material risk, although graphite and nickel sulfate dependencies linger.

Key Report Takeaways

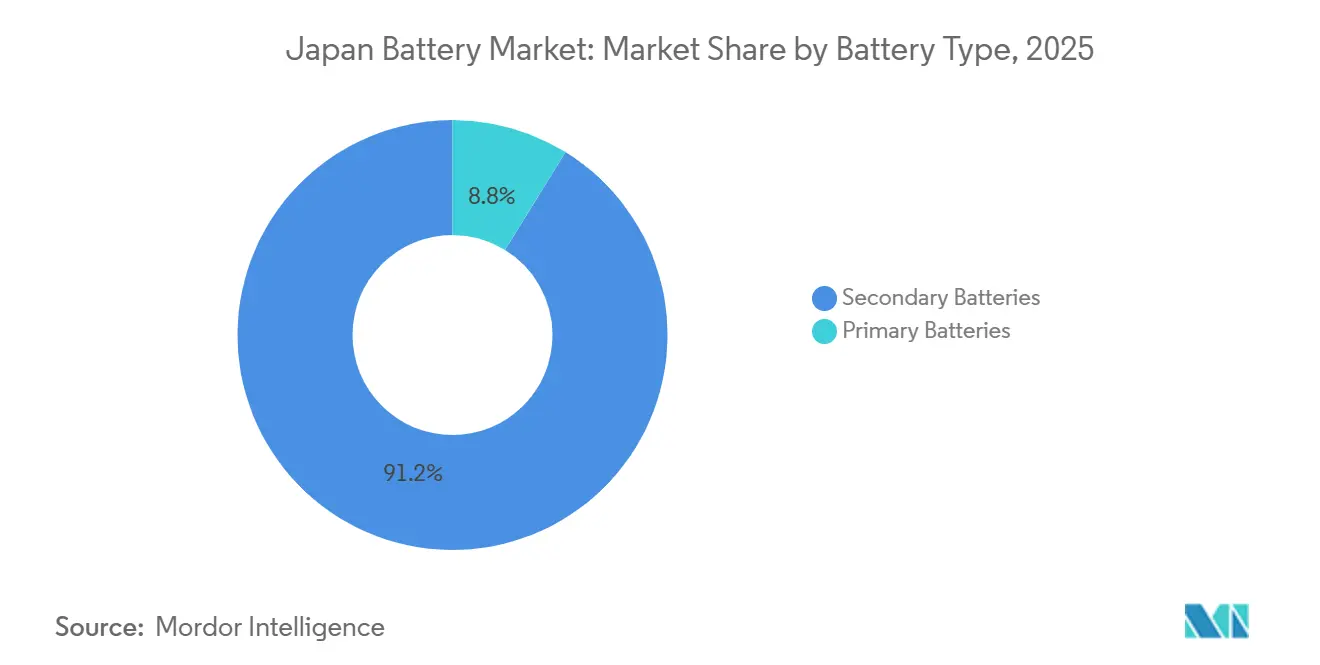

- By battery type, secondary batteries led with 91.2% Japan battery market share in 2025, while the segment is set to expand at a 4.6% CAGR through 2031.

- By technology, lithium-ion retained 51.5% share of the Japan battery market size in 2025, whereas solid-state chemistries are poised for the fastest growth at a 19.8% CAGR to 2031.

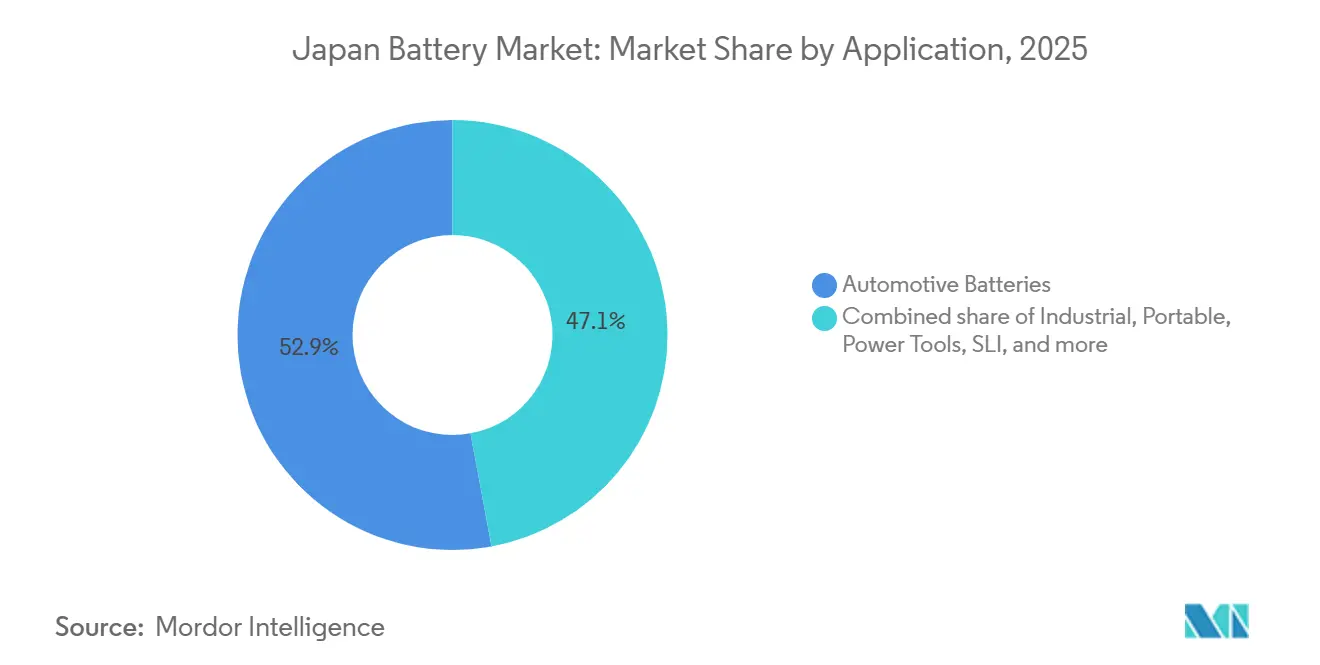

- By application, the automotive segment accounted for 52.9% of the Japan battery market size in 2025 and is forecast to advance at a 5.5% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining domestic lithium-ion cell production costs | +0.8% | National, concentrated in Osaka, Hyogo, and Shiga prefectures | Medium term (2-4 years) |

| Government subsidies for energy storage system adoption | +0.6% | National, with accelerated uptake in Tokyo, Osaka, and Hokkaido | Short term (≤ 2 years) |

| Growing electric vehicle exports from Japan-based OEMs | +1.0% | National, export corridors via Yokohama and Nagoya ports | Medium term (2-4 years) |

| Recycling mandates boosting circular supply chains | +0.4% | National, pilot programs in Kansai and Kanto regions | Long term (≥ 4 years) |

| Semiconductor fabrication facilities' power-backup demand | +0.3% | Regional, Kyushu and Tohoku semiconductor clusters | Medium term (2-4 years) |

| Solar power purchase agreement roll-outs in rural prefectures | +0.2% | Regional, Tohoku, Hokuriku, and Shikoku prefectures | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Domestic Lithium-Ion Cell Production Costs

Panasonic activated a 32-gigawatt-hour Kansas line in July 2025 that applies dry-electrode coating and nickel-rich cathodes to cut cost per kilowatt-hour by half during the early 2030s.[1]Maki Shiraki, “Panasonic Targets Cost Cuts for Tesla Batteries in Profitability Push,” Bloomberg, bloomberg.com Prime Planet Energy Solutions relies on those process gains while commissioning a Himeji prismatic-cell line in 2026, positioning the venture to displace South Korean imports in plug-in hybrids. GS Yuasa is scaling a Kyoto facility to 1 gigawatt-hour and parallel-piloting solid-state output, demonstrating that unit economics remain the gating factor for market share.[2]Tim Kelly, “Japan to Provide $2.4 Billion in Subsidies for 12 Battery-Related Projects,” Reuters, reuters.com Domestic manufacturers thus wager that automation and yield gains will outrun raw-material cost pressure and close the price gap with Chinese lithium iron phosphate cells priced near USD 60 per kilowatt-hour. Success would keep the Japan battery market on its current growth trajectory and preserve high-value manufacturing jobs.

Government Subsidies for Energy Storage System Adoption

Tokyo earmarked USD 2.4 billion across 12 battery projects in September 2024, underscoring that energy storage is treated as national infrastructure rather than discretionary hardware. The Long-term Decarbonization Auction awarded JPY 9 billion in 10-year capacity payments during 2024, removing revenue uncertainty for aggregators deploying behind-the-meter batteries. A Tokyo subsidy of up to JPY 150,000 per residential unit lifted the city’s 2024 installation count above 50,000 systems, triple the national average. These stacked incentives anchor demand for stationary batteries and enable suppliers such as NGK Insulators to secure multiyear offtake contracts with Tokyo Electric Power Company. Mandatory interoperability and cybersecurity standards issued by METI guide product roadmaps, ensuring that subsidy recipients invest in upgradeable, grid-ready platforms.

Growing Electric Vehicle Exports from Japan-Based OEMs

Toyota declared plans in October 2025 to triple battery-electric exports to North America and Southeast Asia by 2028, leveraging domestic cell supply to avoid tariff headwinds. Nissan scaled Ariya shipments via Yokohama port, sustaining utilization at Envision AESC’s Ibaraki plant and neutralizing capacity cuts elsewhere. Honda’s Tochigi demonstration line launched in January 2025 to validate solid-state batteries intended for export models from 2027. These outbound flows ensure that the Japan battery market remains coupled to foreign demand dynamics and justify continued domestic cell investment. Sourcing compliance shapes strategy; Toyota Tsusho’s 25% stake in LG Chem’s Gumi cathode plant guarantees Inflation Reduction Act alignment while diversifying away from China.

Recycling Mandates Boosting Circular Supply Chains

Japan’s Act for Promotion of Effective Utilization of Resources sets a 30% recycling target, yet lithium-ion recovery stood at only 6% in 2024 due to limited collection points. The Japan Portable Rechargeable Battery Recycling Centre piloted hydrometallurgical processes that capture 95% of cobalt and nickel, a vital step toward reducing import dependence. Toyota signed a 2024 agreement with Sumitomo Metal Mining to close the cathode loop, anticipating EU regulations that compel recycled-content thresholds on batteries sold in Europe. When successful, such programs will unlock domestic secondary supply streams and lift the Japan battery market toward circularity while lowering exposure to geopolitical supply shocks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material import dependency on China | -0.7% | National, affecting all cell production hubs | Short term (≤ 2 years) |

| Safety recalls affecting consumer trust | -0.5% | National, with concentrated impact in consumer electronics segment | Short term (≤ 2 years) |

| Prefectural grid-fee disparities | -0.2% | Regional, rural prefectures with higher connection charges | Medium term (2-4 years) |

| Aging workforce in cell manufacturing | -0.3% | National, acute in Kansai and Chubu industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Import Dependency on China

China supplied about 90% of Japan’s natural graphite imports in 2024, and October 2023 export controls caused a 35% price spike that persisted through early 2024. Nickel sulfate exposure has risen as cobalt content falls, yet 60% of refined nickel still arrives from Chinese smelters. JOGMEC’s 2024 equity stakes in Chilean lithium and Australian nickel projects hedge supply risk but offer little relief to near-term pricing. Until diversified offtake agreements mature, raw-material shocks could curb profitability and slow capacity expansions inside the Japan battery market.

Safety Recalls Affecting Consumer Trust

Panasonic recalled 2.9 million laptop batteries in October 2024 due to overheating faults, followed a month later by Toshiba’s withdrawal of 76,000 Dynabook units. In response, METI ordered extra thermal-runaway tests for portable packs over 100 watt-hours, adding up to 12 weeks to certification timelines and raising compliance costs by around 4%. The incidents diluted the historical safety premium associated with Japanese brands and steered some buyers toward lower-priced Chinese alternatives. Solid-state batteries promise inherent safety benefits, yet they must still pass the same tests, meaning reputation recovery will take time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: Rechargeable Cells Dominate Amid Primary Segment Decline

Secondary batteries captured 91.2% of the Japan battery market share in 2025, and the segment is set to grow at 4.6% through 2031 as high-cycle lithium titanate and fast-charge lithium-ion solutions align with industrial and automotive duty cycles.[3]Toshiba, “SCiB Battery Technology,” global.toshiba Primary cells remain useful where five-year replacement intervals or extreme temperature tolerance matter, but revenue contribution keeps sliding. Regulatory frameworks favor rechargeables because extended producer responsibility applies to those chemistries. Maxell’s transfer of its micro primary line to Murata in June 2025 signals a broader exit from low-margin niches. The Japan battery market size tied to primary formats will therefore keep contracting.

Primary batteries do retain footholds in sub-zero utility metering and offshore sensing, where lithium thionyl chloride outperforms lithium-ion electrolyte stability. Even so, no Japanese player announced new capacity beyond maintenance capital in 2025, suggesting replacement demand alone sustains output. Rechargeable suppliers enjoy design-in advantages across automotive, energy storage, and power-tool applications, locking customers into multi-year contracts that underpin volume visibility.

By Technology: Lithium-Ion Leads, Solid-State Disrupts, Legacy Chemistries Persist

Lithium-ion technologies held 51.5% of the Japan battery market size in 2025, supported by Panasonic’s 4680 programs and Prime Planet Energy Solutions’ prismatic packs. Solid-state chemistries, however, are expanding at 19.8% a year toward 2031, targeting densities near 400 watt-hours per kilogram that could trigger a share shift once economies of scale kick in. Murata’s joint development pact with QuantumScape illustrates how tier-two suppliers are chasing safer, higher-margin oxide designs.[4]QuantumScape, “QuantumScape and Murata Manufacturing Enter Joint Development Agreement,” quantumscape.com

Lead-acid and nickel-metal hydride hold niche positions in starting-lighting-ignition and earlier hybrid models. NGK Insulators’ sodium-sulfur systems answer six-hour grid-balancing needs, while Sumitomo Electric’s flow batteries appeal where ultra-long cycle life outweighs size penalties. The technology bifurcation means lithium-ion continues to dominate on cost, solid-state on safety and density, and legacy chemistries on application specificity.

By Application: Automotive Leads, Industrial Storage Accelerates, Portable Electronics Mature

Automotive packs accounted for 52.9% of the Japan battery market size in 2025 and are estimated to grow at 5.5% through 2031 as Toyota triples battery-electric exports and Nissan scales Ariya volumes.[5]Peter Landers, “Toyota Leads Global Race for Solid-State Battery Patents,” Nikkei Asia, nikkei.com Industrial stationary storage benefits from METI auctions that guarantee revenue streams, pushing commercial deployments into positive cash flow territory. Portable electronics growth aligns with replacement cycles around 3% annually, so suppliers regard the category as stable rather than expansive.

High selling prices of automotive packs support specialized production lines like Prime Planet’s Himeji plant, which opens in 2026. In contrast, telecom tower backup and data-center storage drive diversification into sodium-sulfur and flow batteries that tolerate long discharge windows. Power-tool platforms from Makita and Hikoki standardize on 18-volt and 36-volt lithium-ion cartridges that bind consumers into brand ecosystems.

Geography Analysis

The Kansai corridor, spanning Osaka, Hyogo, and Shiga, anchors lithium-ion and solid-state capacity. Panasonic’s Osaka headquarters governs global battery strategy, GS Yuasa pilots solid-state in Shiga, and Prime Planet’s Himeji line sits in Hyogo. Export logistics funnel through Yokohama and Nagoya ports, sustaining throughput for Toyota and Nissan vehicle shipments. Kyushu’s semiconductor cluster creates a secondary hub by demanding reliable backup power.

Prefectural policy divergence shapes stationary storage uptake. Tokyo’s subsidy produced more than 50,000 home-battery systems in 2024, triple the national average. Hokkaido, facing colder climates and higher tariffs, adopted NGK sodium-sulfur units for renewable firming. Rural regions in Tohoku and Shikoku pilot paired solar and battery power purchase agreements, though scale remains modest.

Export competitiveness determines future siting decisions. Higher Japanese port fees and labor costs challenge producers as South Korean and Chinese rivals add capacity. Nissan’s canceled Sunderland plant highlights the risk of duplicative facilities when foreign exchange or spot-price swings erode margins. Whether upcoming solid-state lines disperse to lower-cost prefectures will depend on automation lowering labor sensitivity.

Competitive Landscape

Panasonic, Prime Planet Energy Solutions, and GS Yuasa supply most domestic automotive packs, giving the market moderate concentration. Panasonic pursues dry-electrode coating and high-nickel cathodes to halve costs by the early 2030s. Simultaneously, pilot-scale solid-state lines hedge against lithium-ion commoditization. Toyota Tsusho’s stake in LG Chem’s cathode plant locks compliant supply chains for U.S. markets. NGK Insulators leads utility storage with sodium-sulfur, while Toshiba leverages lithium titanate oxide for industrial motive applications where 20,000-cycle durability offsets a 30% price premium.

Murata Manufacturing’s October 2025 agreement with QuantumScape propels the electronics component leader into automotive-grade solid-state cells. Patent activity reinforces competitive positioning; Toyota filed more than 1,300 solid-state battery patents between 2014 and 2024, signaling intent to defend premium margins. Compliance obligations under the EU Battery Regulation and domestic recycling laws spur joint ventures with smelters to retain cathode materials inside Japan’s borders.

Japan Battery Industry Leaders

Panasonic Corporation

GS Yuasa International Ltd

NGK Insulators Ltd.,

Toshiba Corporation

Maxell, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Murata Manufacturing and QuantumScape entered a joint development agreement to produce ceramic separators for oxide solid-state cells.

- October 2025: Toyota and Sumitomo Chemical announced a collaboration to develop high-energy cathode materials for solid-state batteries.

- September 2025: Toyota Tsusho acquired a 25% stake in LG Chem’s Gumi cathode plant to secure an Inflation Reduction Act–compliant supply.

- July 2025: Panasonic began 32 gigawatt-hour annual production of 4680 cells in Kansas, targeting a 50% cost reduction by the early 2030s.

- June 2025: Murata transferred its micro primary battery business to Maxell to focus on rechargeable technologies.

Japan Battery Market Report Scope

A battery can be defined as an electrochemical device (consisting of one or more electrochemical cells) that can be charged with an electric current and discharged whenever required. Batteries are usually devices that are made up of multiple electrochemical cells that are connected to external inputs and outputs.

The Japan battery market is segmented by battery type, technology, and application. By battery type, the market is segmented into primary batteries and secondary batteries. By application, the market is segmented into automotive batteries, industrial batteries, portable batteries, SLI batteries, and others. By technology, the market is segmented into lithium-ion batteries, lead-acid batteries, and others. For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

By Battery Type

| Primary Batteries |

| Secondary Batteries |

By Technology

| Lead-acid |

| Li-ion |

| Nickel-metal hydride |

| Nickel-cadmium |

| Sodium-sulfur |

| Solid-state |

| Flow Battery |

| Emerging chemistries |

By Application

| Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) |

| Portable (Consumer Electronics, etc.) |

| Power Tools |

| SLI |

| Other Applications |

| By Battery Type | Primary Batteries |

| Secondary Batteries | |

| By Technology | Lead-acid |

| Li-ion | |

| Nickel-metal hydride | |

| Nickel-cadmium | |

| Sodium-sulfur | |

| Solid-state | |

| Flow Battery | |

| Emerging chemistries | |

| By Application | Automotive (HEV, PHEV, and EV) |

| Industrial (Motive, Stationary (Telecom, UPS, ESS), etc.) | |

| Portable (Consumer Electronics, etc.) | |

| Power Tools | |

| SLI | |

| Other Applications |

Key Questions Answered in the Report

What is the current value of the Japan battery market?

The Japan battery market size reached USD 3.99 billion in 2026.

How fast is the market expected to grow toward 2031?

Revenue is projected to rise to USD 4.91 billion by 2031, representing a 4.25% CAGR.

Which battery technology is expanding quickest?

Solid-state chemistries are advancing at a 19.8% CAGR as manufacturers seek higher energy density and safety.

Why are secondary batteries dominant in Japan?

Rechargeable formats deliver total-cost-of-ownership benefits once applications exceed 50 cycles, driving a 91.2% market share in 2025.

What risks could slow market expansion?

Heavy reliance on Chinese raw-material imports and consumer trust issues following safety recalls pose the greatest headwinds.

Which segment delivers the highest revenue contribution?

Automotive batteries accounted for 52.9% of 2025 revenue due to large pack sizes and rising export volumes.

Page last updated on: