Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

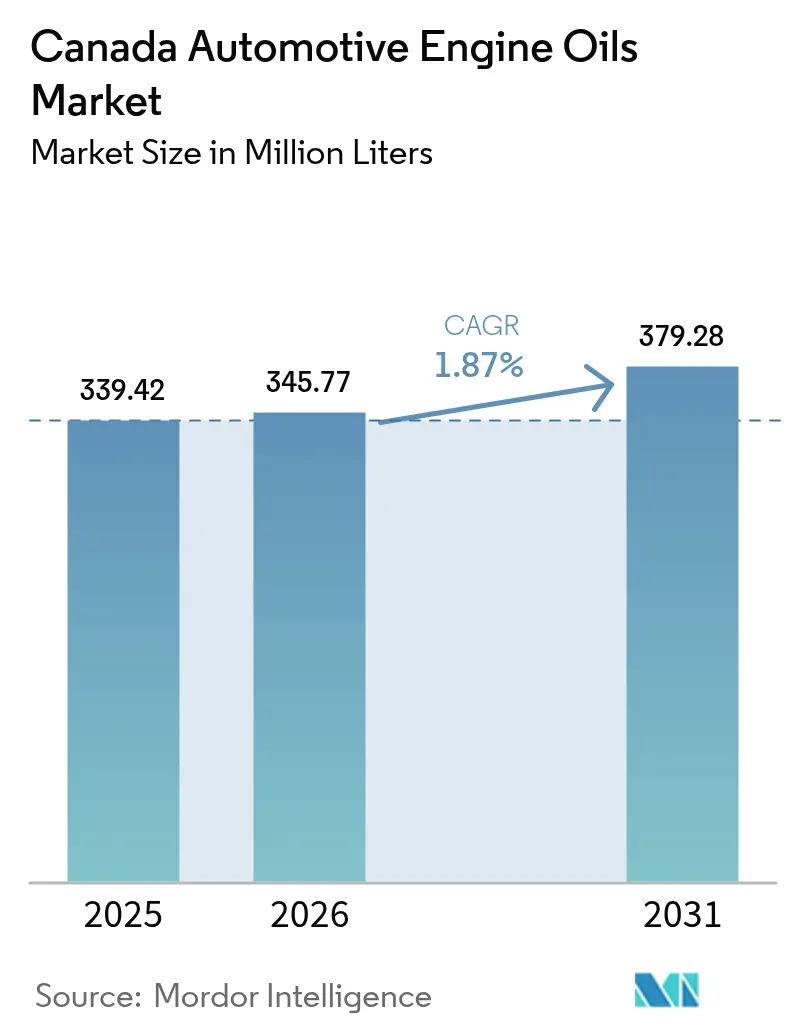

| Base Year Market Size (2025) | 339.42 Million Liters |

| Market Volume (2026) | 345.77 Million Liters |

| Market Volume (2031) | 379.28 Million Liters |

| Growth Rate (2026 - 2031) | 1.87% CAGR |

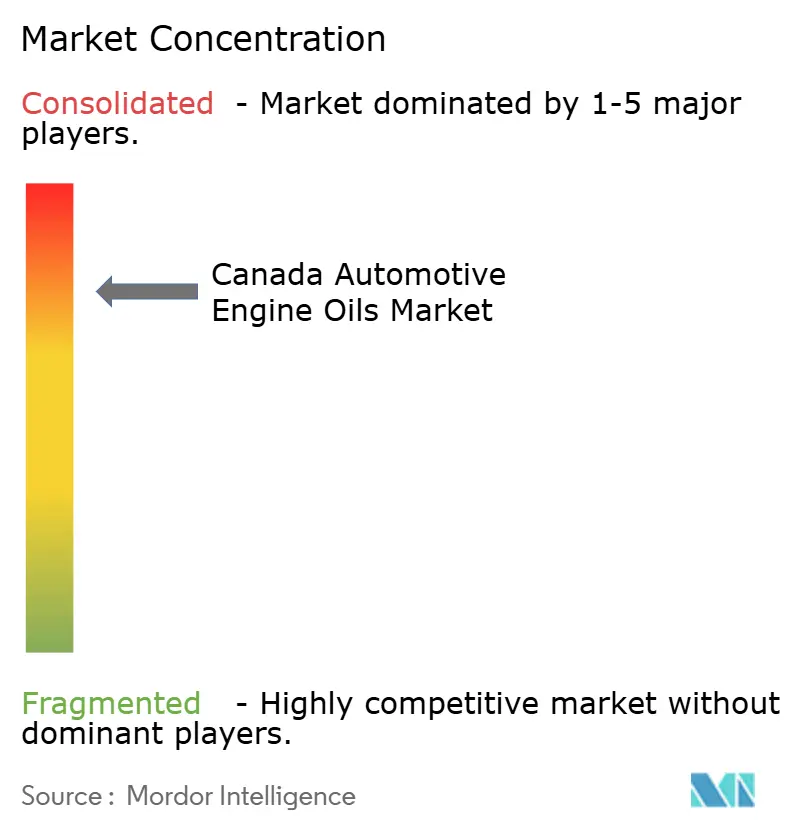

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Automotive Engine Oils Market Analysis by Mordor Intelligence

The Canada Automotive Engine Oils Market size is expected to grow from 339.42 million liters in 2025 to 345.77 million liters in 2026 and is forecast to reach 379.28 million liters by 2031 at 1.87% CAGR over 2026-2031. Growing demand for low-viscosity synthetic grades, the resilience of heavy-duty vehicle activity, and climate-driven viscosity requirements underpin the measured expansion of the Canada automotive engine oils market. While electrification is beginning to erode lubricant consumption in the United States and Mexico, Canada’s colder climate, longer average vehicle age, and extensive resource-extraction corridors slow the substitution effect. Multinational suppliers are scaling synthetic production capacity to meet Clean Fuel Regulations that favor 0W-20 and 5W-20 formulations. At the same time, e-commerce growth pushes light commercial fleets to operate in start-stop urban cycles that elevate oil stress levels and accelerate fill frequency, partially offsetting volume lost to passenger EV adoption. Competitive dynamics remain shaped by vertically integrated majors that leverage upstream access to Alberta crude, refinery presence in Ontario and Quebec, and nationwide retail footprints, sustaining high brand visibility and scale efficiencies.

Key Report Takeaways

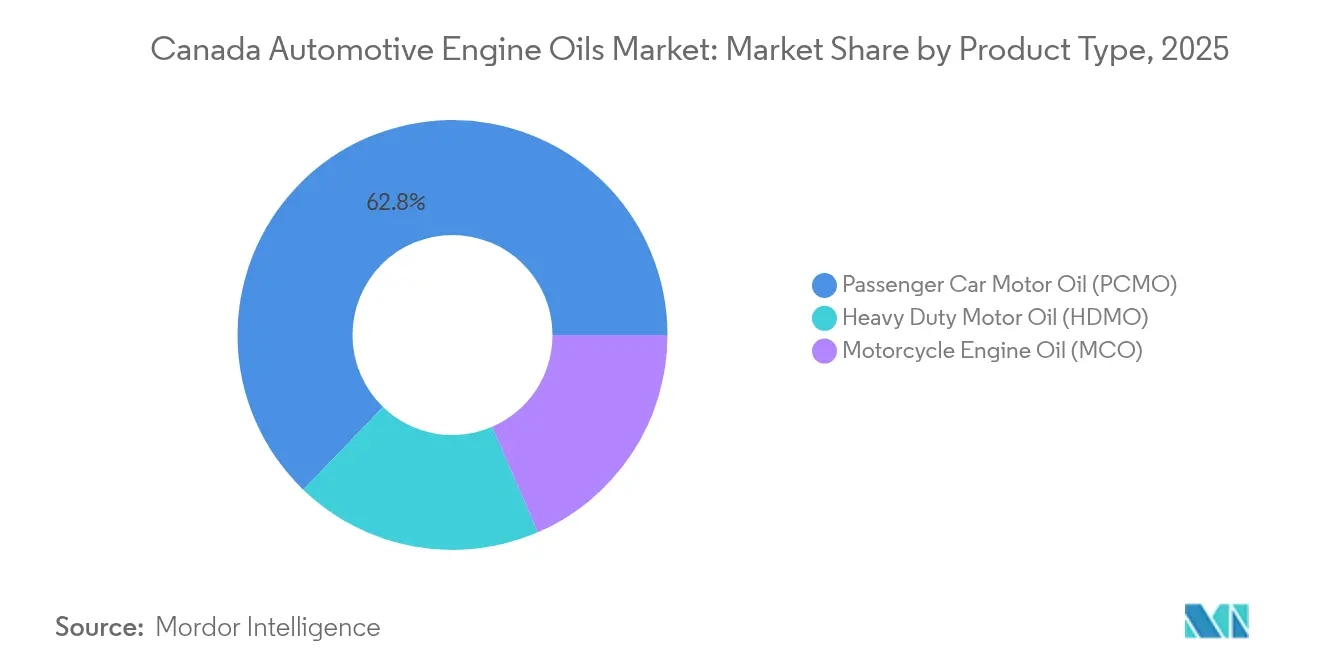

- By product type, passenger car motor oil accounted for a 62.78% share of the Canada automotive engine oils market size in 2025, whereas heavy duty motor oil is forecast to advance at a 2.02% CAGR through 2031.

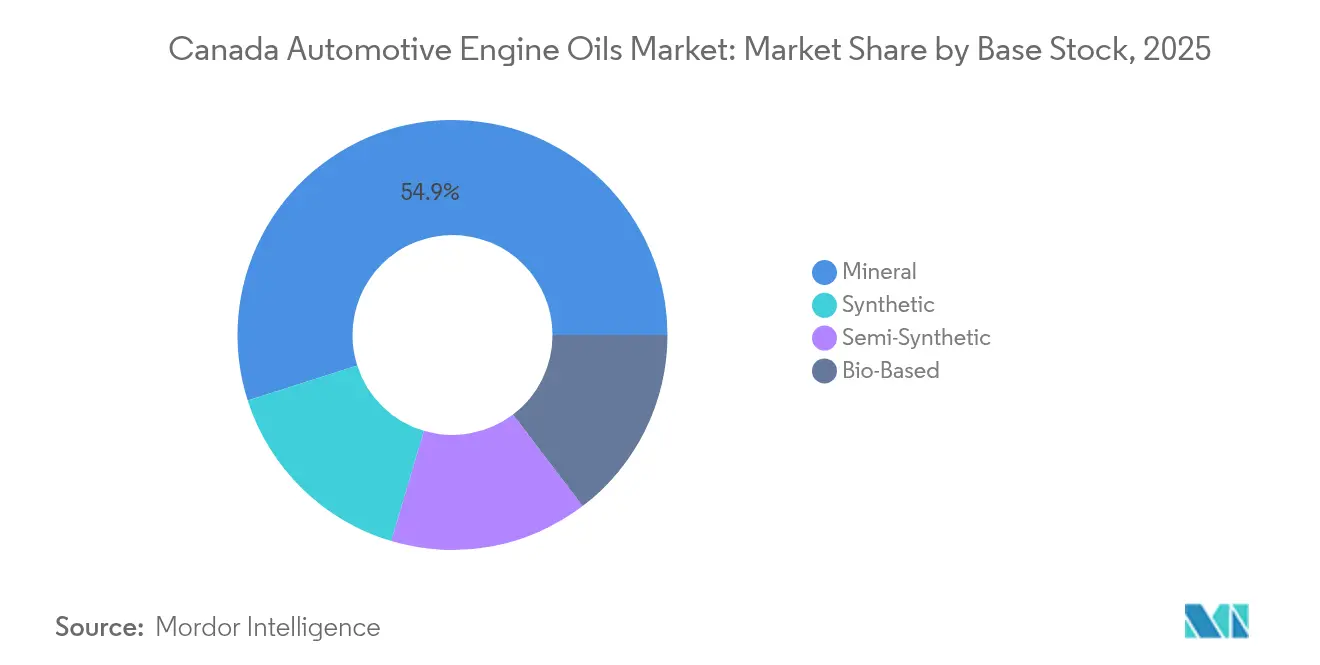

- By base stock, mineral oils held 54.92% of the Canada automotive engine oils market share in 2025, while synthetic grades are projected to expand at a 2.14% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of last-mile delivery fleets | +0.40% | National, concentrated in Toronto, Vancouver, Montreal metropolitan areas | Medium term (2-4 years) |

| Surge in ride-hailing platform vehicles and bulk-service tie-ups | +0.30% | Urban centers, expanding to mid-tier cities | Short term (≤ 2 years) |

| Tightening CO₂ / Euro 6-equivalent emission norms driving premium synthetics | +0.20% | National, with early adoption in British Columbia, Ontario | Long term (≥ 4 years) |

| OEM-mandated extended-drain intervals raising per-fill value | +0.10% | National, led by premium vehicle segments | Medium term (2-4 years) |

| Motorcycle enthusiast culture boosting high-performance oils | +0.10% | Regional, strongest in Alberta, British Columbia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Last-Mile Delivery Fleets

Commercial vehicle registrations rose 8.3% in 2024, and a large share of that gain came from light vans servicing e-commerce fulfillment[1]Statistics Canada, “Motor Vehicle Registrations,” statcan.gc.ca . Every vehicle in this cohort experiences frequent cold starts, prolonged idling, and dense stop-and-go operation that degrade conventional oils quickly. Fleet managers now specify semi-synthetic or full-synthetic formulations to maintain viscosity at elevated sump temperatures and to secure warranty compliance across mixed-make fleets. Concentrated activity in Toronto, Vancouver, and Montreal produces localized spikes in lubricant demand that wholesalers must meet with flexible inventory programs. The Canada automotive engine oils market benefits because these fleets favor 10,000 km or shorter drains despite OEM guidance, opting for preventive maintenance to cut downtime. Suppliers that bundle telematics-based oil monitoring with bulk delivery contracts are strengthening long-term customer stickiness in this fast-growing niche.

Surge in Ride-Hailing Platform Vehicles and Bulk-Service Tie-ups

Uber and other mobility platforms formalized fleet-maintenance agreements in 2024 that allow operators to buy premium synthetics at negotiated rates. Typical ride-hailing vehicles accumulate over 200,000 km annually, driving synthetic oil penetration as platforms enforce strict vehicle uptime metrics. These B2B channels now capture a sizeable portion of urban PCMO volume that previously moved through quick-lube outlets. Concentration of demand in large metropolitan areas lets suppliers schedule milk-run deliveries and reduce last-mile logistics costs. The Canada automotive engine oils market, therefore, records higher average selling prices even as overall passenger-car kilometres plateau. New entrants that lack B2B relationships face a steeper climb because brand switching costs have fallen for fleet owners who buy on total cost of ownership rather than ticket price alone.

Tightening CO₂ / Euro 6-Equivalent Emission Norms Driving Premium Synthetics

Clean Fuel Regulations mandate stepwise carbon-intensity reductions that push automakers toward engines calibrated for thinner oils. OEM service manuals increasingly prescribe 0W-20 and 5W-20 synthetics with high VI base oils that minimize hydrodynamic drag. Mineral oils often fail cold-crank simulations at -30 °C, common in prairie provinces, forcing a migration to Group III or Group IV stocks. Provinces that attach provincial carbon levies to tailpipe emissions have accelerated adoption, with British Columbia leading due to its aggressive ZEV credits. As engine downsizing and turbocharging proliferate, formulation specialists incorporate shear-stable viscosity modifiers and low-SAPs additive packs to protect after-treatment devices. The regulation led shift toward synthetics sustains volume even as drain intervals elongate, maintaining revenue resilience for the Canada automotive engine oils market.

OEM-Mandated Extended-Drain Intervals Raising Per-Fill Value

Ford’s 2024 bulletin moved scheduled drains for select models from 8,000 km to 16,000 km, contingent on certified synthetic usage. This tactic transfers routine maintenance cost to consumers, yet it also lifts per-fill value, because full synthetics command 40-60% price premiums over mineral alternatives. Fleets gain productivity through fewer service stops, but lubricant marketers offset shrinking litres with richer margins. Additive houses invest in boron and molybdenum chemistries that deliver TBN retention over longer cycles. The Canada automotive engine oils market therefore tilts toward high-value SKUs, cushioning suppliers from electrification-driven volume attrition. Extended drains are also spurring digital fleet dashboards that predict optimal oil-change timing, creating data-centric revenue opportunities for service providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shared-mobility consolidation reducing private-car kilometres | -0.20% | Urban centers, particularly Toronto, Vancouver, Montreal | Medium term (2-4 years) |

| Grey-import lubricants eroding branded volumes | -0.10% | Border regions, online retail channels | Short term (≤ 2 years) |

| Rising drain-intervals lowering service frequency | -0.10% | National, accelerated by OEM mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shared-Mobility Consolidation Reducing Private-Car Kilometres

Household vehicle ownership plateaued at 1.4 vehicles in 2024 as urban households opted for car-sharing subscriptions[2]OECD, “Household Transport Choices and Climate Policy,” oecd.org. Each shared unit records higher annual mileage, but the aggregate national VKT shrinks as redundant private vehicles leave the road. The Canada automotive engine oils market loses conventional retail transactions because professional fleet depots service these shared cars and often adopt extended-drain synthetics. Municipal investments in multimodal transport and zero-emission zones will deepen this trend by 2027. Suppliers respond by shifting promotional budgets from consumer channels to fleet account management, yet brand recognition among individual motorists declines, making future retention harder if ownership rebounds.

Grey-Import Lubricants Eroding Branded Volumes

Parallel imports through e-commerce sites surged during 2024, as currency swings widened the price gaps between U.S. and Canadian retail shelves. Unofficial channels offer branded packs at 20-30% discounts, undercutting authorized distributors. Warranty clauses rarely block these oils because they meet API and ILSAC labels, so price-sensitive do-it-yourself consumers embrace them. The Canada automotive engine oils market thus faces downward price pressure even within premium categories. Regulators are reviewing label-compliance enforcement, yet policing thousands of small parcels is challenging. Authorized suppliers counter with QR code authentication and loyalty programs, but the competitive moat continues to narrow in regions close to the U.S. border.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Commercial Fleets Push HDMO Momentum

Heavy Duty Motor Oil accounted for a smaller base but is forecast to grow at a 2.02% CAGR to 2031 within the Canada automotive engine oils market. Resource extraction in Alberta, Saskatchewan, and British Columbia exposes engines to abrasive particulates and 40 °C temperature swings, compelling operators to specify high-TBN synthetics. OEMs endorse 10W-30 CK-4 formulations that promise 3% fuel-economy gains, an advantage that resonates when diesel costs spike. Fleet trials show 20,000 km drains are feasible under oil-analysis programs, reducing service pit stops in remote mining sites. Among on-road freight haulers, border congestion and long idling times raise soot levels, making premium detergency essential. Suppliers offering field-lab sample kits improve value perception and secure contract renewals.

Passenger Car Motor Oil retained a commanding 62.78% share of the Canada automotive engine oils market size in 2025. However, growth moderates as electric cars chip away at internal-combustion share in urban centers. Remaining ICE vehicles age, with a median of 10.6 years, which sustains demand for high-mileage 5W-30 formulations that swell seals and counter blow-by. Yet OEM push for 0W-20 synthetics in new models is shifting mix, lifting revenue per litre. Quick-lube chains adapt by promoting synthetic upgrades bundled with cabin filters and tire rotations to hold ticket values steady. Recreational off-roaders and performance enthusiasts preserve demand for 5W-50 and 10W-60 niche grades that carry premium margins.

Motorcycle Engine Oil remains a niche yet high-value pocket within the Canada automotive engine oils market. Seasonal riders in Alberta and British Columbia favor ester-rich synthetics that resist shear in shared-sump transmissions, and demand spikes between April and July. Powersports dealerships stock small-pack SKUs with attractive dollar-per-litre yields, although total litres are modest. LIQUI MOLY’s Parts Canada tie-up expands shelf presence at 1,200 locations and exemplifies the opportunity for specialty blenders to carve profitable micro-segments.

By Base Stock: Synthetic Leadership Strengthens

Synthetic formulations are projected to post a 2.14% CAGR through 2031, outpacing all other base-stock categories in the Canada automotive engine oils market. Group III and Group IV stocks deliver pour points below -40 °C, a critical attribute for reliable starts in prairie winters. Price premiums narrow as multinationals add capacity—Shell’s CAD 15 million expansion in Sarnia being a prime example—compressing unit economics for conventional mineral blends. Fleet TCO calculations favor synthetics once drain intervals exceed 12,000 km, tipping procurement policies even among cost-conscious small operators.

Mineral oils still held 54.92% of the Canada automotive engine oils market share in 2025, reflecting entrenched habits among owners of legacy vehicles built before 2015. DIY consumers buying 4-litre jug specials at big-box retailers remain loyal to SN-grade 5W-30 conventional oil that meets minimum warranty coverage at the lowest upfront cost. However, tightened volatility and cold-crank benchmarks under ILSAC GF-6 make it harder for mineral formulations to remain compliant without costly additive boosts. Semi-synthetic blends emerge as a compromise solution, capturing drivers moving up the quality curve while trimming sticker shock.

Bio-based lubricants stay nascent, limited to pilot deployments in municipal fleets that chase Scope 3 emission reductions. Earth Alive’s acquisition of Interlube positions it to scale biodegradable hydraulic fluids, yet automotive crankcase volumes will remain small until ASTM oxidation stability hurdles are cleared. Nonetheless, Clean Fuel Regulations assign carbon value to life-cycle emissions, so early adopters could gain subsidy support and secure future upside if policy incentives strengthen.

Geography Analysis

Ontario and Quebec together represent over half of the national lubricant demand by volume, aided by 18.2 million registered vehicles and dense dealership networks that ensure product availability. Ontario’s auto-assembly corridor drives OEM factory-fill requirements for export-bound vehicles, supporting steady offtake for 0W-20 synthetics. Quebec’s winter climate pushes retailers to stock higher VI grades that flow at -35 °C, driving an above-average synthetic mix. Urban electrification strategies in Toronto and Montreal will curb growth, yet last-mile van fleets clustered around suburban distribution hubs maintain baseline consumption.

Western Canada delivers the fastest incremental litres to the Canada automotive engine oils market. Alberta’s oil-sands haul trucks use 5-W 40 HDMO with advanced dispersant packages that maintain viscosity under severe soot load. British Columbia’s forestry and mining sectors rely on hydraulic fracturing and logging equipment that demand extreme-pressure additives. Recreational vehicle culture supports robust sales of motorcycle and ATV oils, especially during spring thaw when off-road trail access opens. Suppliers face logistical hurdles moving stock into remote northern towns, so bulk rail shipments to Edmonton and Calgary terminals are followed by road tanker redistribution.

Atlantic Canada records modest but stable demand. Its older vehicle parc leans toward mineral oils, and harsh salt-spray winters shorten vehicle life, keeping average engine technology dated. Distribution costs across dispersed coastal communities lift shelf prices, nudging some consumers toward online cross-border purchases that feed the grey-import channel. Nonetheless, commercial fishing fleets increasingly trial biodegradable gear oils under federal grant schemes, pointing to a potential early adopter role for bio-based crankcase liquids should technical barriers fall.

Competitive Landscape

The Canada automotive engine oils market exhibits consolidated concentration. Scale advantages secure stable feedstock, letting majors amortize additive R&D over larger volumes and sustain aggressive price promotions. Private-label store brands source base oils on the spot market and outsource blending, limiting their ability to match OEM-specific formulations or to secure factory-fill agreements.

Digital transformation is reshaping channel power. Quick-lube chains deploy subscription apps that recommend service windows based on telematics data, locking customers into brand ecosystems. B2B platforms negotiate multi-year supply contracts with ride-hailing or parcel-delivery fleets, bundling lubricant, filter, and diagnostic services. Majors that can guarantee just-in-time delivery to urban depots at competitive rates win share, while smaller regional blenders pivot toward niche products such as vintage-car zinc-rich formulas or biodegradable hydraulic oils.

Innovation focus centers on lower-viscosity synthetics capable of meeting GF-7 and API SP+ standards that will roll out before 2030. Companies invest in molybdenum-based anti-wear and calcium-rich detergents to protect turbocharged gasoline particulate filters. Petro-Canada’s digital handbook platform simplifies viscosity selection for fleet managers suffering winter gelling issues, boosting customer retention. Castrol, Valvoline, and Mobil leverage retail partnerships to push 0W-20 packs into big-box stores, reinforcing brand equity even as overall passenger-car litres edge downward.

Canada Automotive Engine Oils Industry Leaders

BP p.l.c.

HF Sinclair Corporation (Petro-Canada lubricants)

Imperial Oil Limited

Shell Plc

Saudi Arabian Oil Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: In a move to align with the latest ILSAC GF-7 and API SQ performance benchmarks for passenger car engine oils, Petro-Canada Lubricants launched its revamped SUPREME product line. This debut showcases reformulated lubricants and a fresh nomenclature, and eye-catching packaging.

- April 2025: TotalEnergies Marketing Canada Inc., a player in Canadian automotive lubrication technology, announced its transition to moving from mineral-based to synthetic engine oils.

Canada Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

How large is the Canada automotive engine oils market in 2026?

The Canada automotive engine oils market size reached 345.77 million liters in 2026.

What CAGR is expected for engine oils in Canada through 2031?

Demand is forecast to grow at a 1.87% CAGR, taking volume to 379.28 million liters by 2031.

Which segment is growing fastest in Canadian engine oils?

Heavy Duty Motor Oil leads growth with a 2.02% CAGR, fueled by resource and freight activity.

Why are synthetic oils gaining share in Canada?

Clean Fuel Regulations, cold weather performance, and OEM extended-drain mandates are pushing adoption of low-viscosity synthetics.

Which provinces consume the most engine oils?

Ontario and Quebec together account for more than half of national demand due to their large vehicle fleets and industrial bases.

How are ride-hailing fleets affecting lubricant sales?

Bulk-purchase agreements with mobility platforms shift volume to B2B channels and raise synthetic mix, increasing per-litre value despite fewer retail transactions.

Page last updated on: