Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

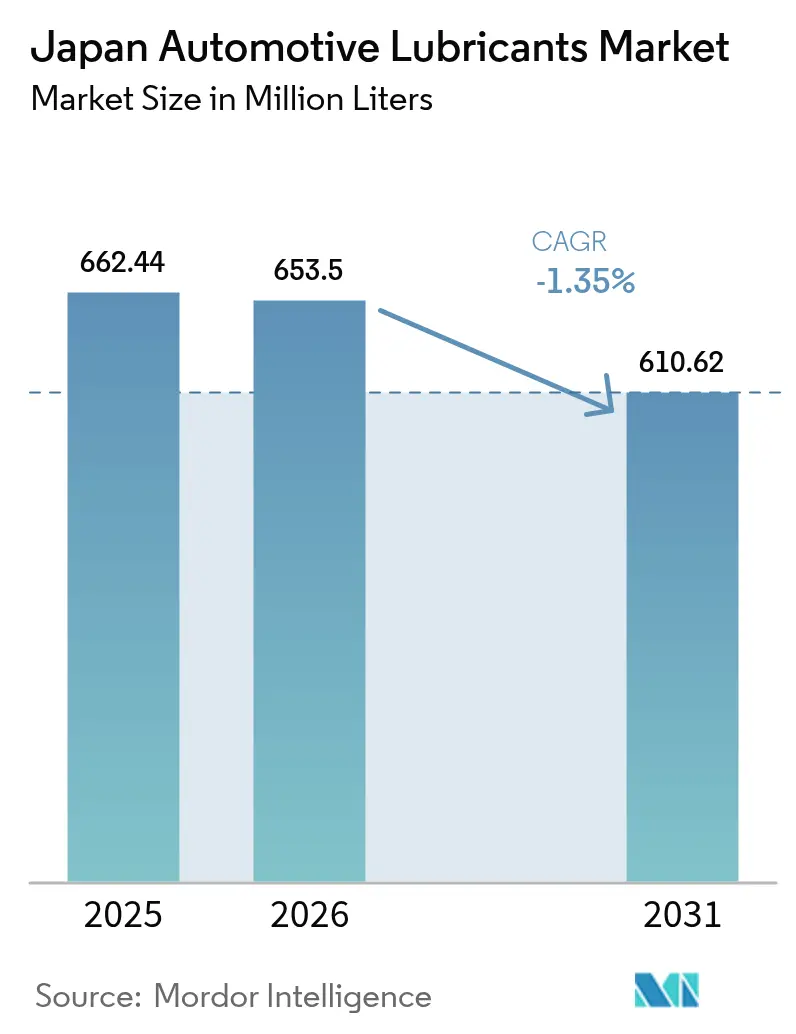

| Base Year Market Size (2025) | 662.44 Million liters |

| Market Volume (2026) | 653.5 Million liters |

| Market Volume (2031) | 610.62 Million liters |

| Growth Rate (2026 - 2031) | -1.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Automotive Lubricants Market Analysis by Mordor Intelligence

Japan Automotive Lubricants Market size in 2026 is estimated at 653.5 million liters, growing from 2025 value of 662.44 million liters with 2031 projections showing 610.62 million liters, growing at -1.35% CAGR over 2026-2031. The contraction reflects rapid electrification, stringent Corporate Average Fuel Economy targets, and the industry-leading OEM-genuine oil penetration that concentrates demand in premium but thinner viscosity grades. Low-viscosity formulations, such as 0W-8 and 0W-12, continue to gain market share because they deliver fuel efficiency gains, creating a technology moat for domestic refiners that control integrated base-oil production. Commercial fleets, on the other hand, deploy remote oil-condition monitoring to stretch drain intervals, partially offsetting volume loss while reinforcing the value proposition of higher-margin synthetics.

Key Report Takeaways

- By product type, automotive engine oil led with a 61.62% share of Japan's automotive lubricants market in 2025; automatic transmission fluids recorded the highest projected CAGR of -1.23% through 2031.

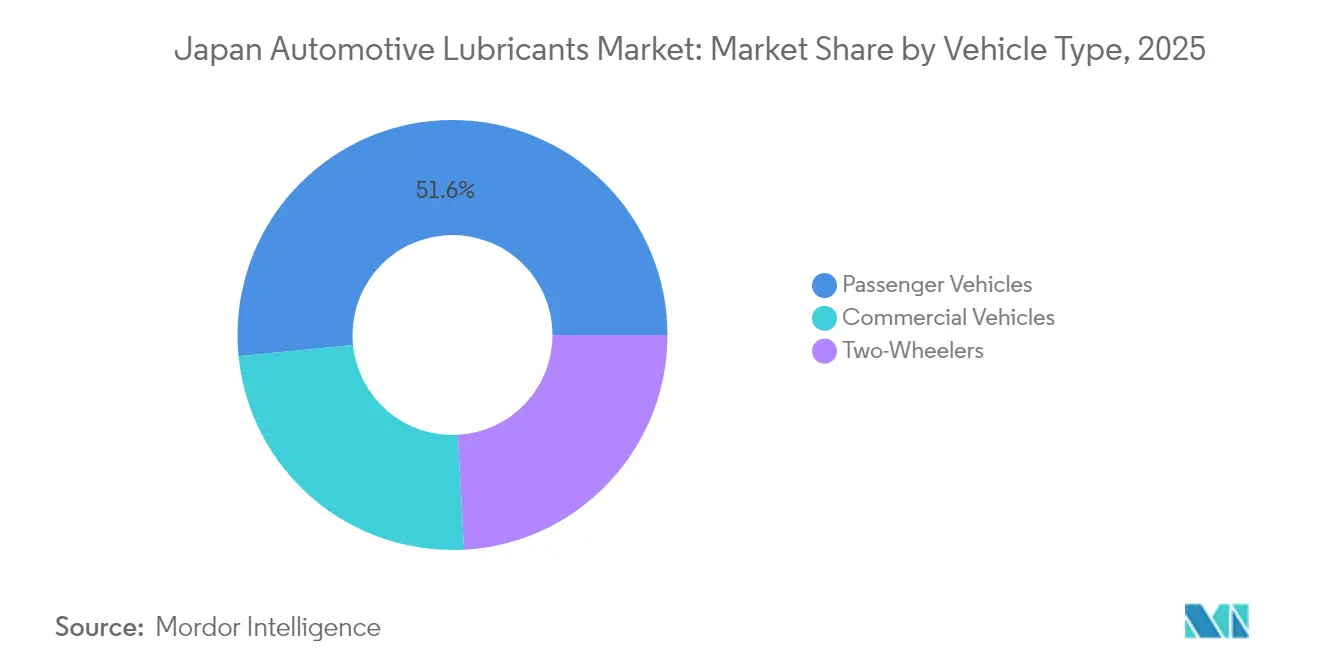

- By vehicle type, passenger vehicles accounted for a 51.58% share of the Japanese automotive lubricants market size in 2025, while commercial vehicles were projected to have the highest CAGR at -1.08% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High OEM-genuine oil penetration | +0.8% | Nationwide, strongest in urban centers | Medium term (2-4 years) |

| Regulatory shift to low-viscosity, fuel-efficient oils | +0.5% | Nationwide | Long term (≥ 4 years) |

| Mature but aging vehicle parc | +0.4% | Nationwide, rural skew | Medium term (2-4 years) |

| Growth of synthetic and bio-based blends | +0.3% | Nationwide | Long term (≥ 4 years) |

| Remote oil-condition monitoring adoption | +0.2% | Commercial-vehicle clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High OEM-Genuine Oil Penetration Sustains Premium-Grade Demand

OEM-genuine oil penetration surpasses the global average of 45%, enabling automakers and refiners to maintain premium pricing power despite the shrinking base of internal-combustion vehicles. Dealer-controlled maintenance schedules ensure routine lubricant replacement and keep genuine labels embedded in consumer habits. Toyota, Honda, and Nissan exploit this captive channel to mandate advanced synthetics that command higher margins than mineral oils. The legally mandated Shaken inspection obliges drivers to use certified workshops, reinforcing OEM channel dominance. As a result, premium-grade demand softens more slowly than total volume, helping the Japanese automotive lubricants market maintain a stable profit pool even as liters decline. Independent workshops respond by stocking value-branded synthetics to retain customers migrating out of warranty.

Regulatory Shift to Low-Viscosity, Fuel-Efficient Oils

Japan’s 2030 CAFE target of 25.4 km/L pushes refiners to deliver oils as thin as 0W-8, a grade that lowers hydrodynamic drag compared with 5W-30. Domestic players leverage integrated supply chains to customize Group III+ and Group IV base-oil blends that meet JASO GLV-1 and GLV-2 benchmarks at scale, whereas importers incur costs associated with formula redesign. Production expenses increase, yet OEMs willingly pass these premiums on to consumers because validated fuel-efficiency gains help them meet their fleet-average targets. The Japan automotive lubricants market, therefore, skews toward synthetics and ultra-low viscosities, widening the technology gap between incumbents and late-entry suppliers. Over the forecast horizon, viscosity downgrading is expected to reduce aggregate demand but simultaneously raise average selling prices, thereby tempering revenue erosion.

Mature but Aging Vehicle Parc Maintains Aftermarket Volumes

The average vehicle age reached 13.2 years in 2024, the highest among developed economies, creating a sizable pool of high-mileage engines that require more frequent oil changes[1]Japan Automobile Standards Organization, “JASO Engine Oil Standards,” JASO.OR.JP . Economic stagnation and demographic shifts delay replacement purchases, extending maintenance cycles for legacy ICE models. Service intervals for older engines remain at 10,000–12,000 kilometers, which is well below the 15,000–25,000-kilometer thresholds typical in North America, thereby preserving aftermarket throughput. Independent workshops cater to this segment with conventional and high-mileage mineral formulations, whereas OEM service centers focus on synthetics for newer fleets. The coexistence of old and new platforms enables suppliers to maintain a broad range of SKUs, thereby buffering revenue as total volumes decline. Regulatory checks on tailpipe emissions for older vehicles further anchor lubricant demand by mandating compliant formulations that maintain catalytic converter efficiency.

Growth of Synthetic and Bio-Based Blends for Carbon Reduction

Japan’s carbon-neutrality pledge for 2050 accelerates the adoption of synthetics that extend drain intervals and cut lifecycle emissions by up to 30%. ENEOS and Idemitsu have earmarked funds for bio-refinery upgrades to produce ester-based stocks derived from vegetable oils, targeting fleets that report sustainability metrics to shippers and investors. Incentives in the Green Growth Strategy—including tax credits and accelerated depreciation—encourage fleets to trial bio-lubes, opening a premium niche within the shrinking volume base. These dynamics help the Japan automotive lubricants market pivot toward lower-carbon value propositions, partially substituting margin for scale.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV/hybrid uptake curbs ICE-oil volumes | -2.1% | Metropolitan clusters | Short term (≤ 2 years) |

| Volatile base-oil feedstock costs | -0.8% | Import-dependent regions | Medium term (2-4 years) |

| Counterfeit lubricants on e-commerce | -0.3% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid EV/Hybrid Uptake Curbs ICE-Oil Volumes

Electrified vehicles captured a significant share of new sales in 2024, cutting engine running time and lubricant consumption per unit. Battery electric platforms eliminate the need for engine oil. The government’s 2035 ban on new ICE-only passenger cars accelerates the downward trajectory. ENEOS projects gasoline demand to fall by 50% by 2040, implying a direct correlation with engine oil erosion. While hybrid transmissions still require specialized fluids, the overall decline in liters is faster than the contraction of the vehicle stock. Suppliers respond by reallocating capital toward industrial and marine lubricants to hedge exposure. For the Japan automotive lubricants market, electrification remains the single largest headwind, outweighing all incremental drivers combined.

Volatile Base-Oil Feedstock Costs Pressure Margins

Domestic refinery closures, including ENEOS’s Wakayama shutdown, push import dependency for base oils, exposing manufacturers to swings in Group I price benchmarks. Smaller blenders without term contracts face cash-flow strain when prices spike, narrowing gross margins. Currency fluctuations compound volatility because purchases are dollar-denominated while sales accrue in yen. To manage risk, large refiners extend supply agreements with South Korean and Singaporean producers, whereas independents increasingly rely on spot volumes. Despite price pressures, the Japan automotive lubricants market sustains a premium positioning, but margin compression incentivizes further consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine-Oil Dominance Amid Viscosity Evolution

Automotive engine oil retained 61.62% of Japan's automotive lubricants market share in 2025, underscoring its centrality to ICE maintenance. Yet the segment’s negative CAGR mirrors the systemic shift toward electrified drivetrains. Within the category, 0W-8 and 0W-12 account for the fastest growth as OEM manuals specify these grades to satisfy fuel-economy tests. Japan's automotive lubricants market size for automatic transmission fluids is forecast to decline at a modest -1.23% CAGR, as hybrid powertrains and continuously variable transmissions require specialized ATFs for electric-motor lubrication and thermal management. Manual transmission fluids and power-steering fluids shrink more quickly due to the rise of CVTs and electric steering systems. Brake fluids remain steady because EVs still employ hydraulic braking circuits.

Elevated technical barriers in ultra-low viscosity formulations favor refiners with Group III+ upgrading units, enabling ENEOS and Idemitsu to supply OEM-approved 0W-8 at volume. As drain intervals extend, suppliers embed value by bundling oil-analysis services and warranty extensions. Greases hold niche relevance in wheel bearings and chassis components for both ICE and EV platforms, moderating the overall decline. The shaken inspection protocol enforces replacement cycles, ensuring that the Japanese automotive lubricants market maintains calibrated demand for every fluid family, even under pressure from electrification.

By Vehicle Type: Commercial Resilience Offsets Passenger Declines

Passenger vehicles comprised 51.58% of Japan's automotive lubricants market size in 2025; however, their lubricant consumption is projected to contract at the fastest rate, as urban EV uptake outpaces that in rural regions. BEV and PHEV penetration increased in new registrations, slashing engine oil liters per car. Conversely, commercial vehicles post the mildest decline at -1.08% CAGR as fleet electrification lags due to payload penalties and charging constraints. Heavy trucks, buses, and construction machinery retain large crankcase volumes, partially offsetting the decline in passenger car sales. Two-wheelers add stability; motorcycles require high-shear-stability oils, which are changed every 3,000-5,000 kilometers, and electrification remains nascent outside food-delivery fleets.

Remote oil-condition monitoring is gaining traction among trucking and heavy-equipment operators, enabling them to defer changes, yet the high base volumes keep the segment attractive. Stricter NOx and particulate matter rules for diesel engines mandate low-ash formulations to protect after-treatment systems, thereby boosting the adoption of synthetic fuels. This resilience provides a buffer for the Japan automotive lubricants market, giving suppliers a platform to transition toward next-generation fluids while managing volume attrition.

Geography Analysis

Japan's automotive lubricants market demand is concentrated along the Pacific industrial corridor, which stretches from Fukuoka through Osaka and Nagoya to the Tokyo-Yokohama cluster, where automotive manufacturing density is highest. These metro regions also exhibit the fastest electrification rates, which suppress engine oil volumes but catalyze demand for hybrid-specific transmission fluids. Rural prefectures, such as Hokkaido and Tohoku, maintain higher ICE dependency because sparse charging infrastructure extends the adoption timelines. Consequently, the Japan automotive lubricants market size for conventional 10W-30 grades persists in these areas, supporting independent distributors.

Petroleum product demand nationwide has declined since 1999 and is forecast to continue declining by 2030, prompting refiners to rationalize their coastal plants and consolidate distribution depots. ENEOS leverages its refineries in Chiba and Mizushima, linked to a nationwide network of over 10,000 service stations, to maintain its dominance despite shrinking volumes. Imports account for a major portion of the base-oil supply, mostly arriving at Yokohama and Kobe, then being transported inland by tank truck or coastal tanker. Geopolitical disruptions or refinery turnarounds in Singapore or South Korea, therefore, ripple quickly across Japanese inventories, prompting refiners to maintain safety stocks equivalent to 45 days of demand.

Demographic patterns further shape regional lubricant consumption. Aging populations in rural prefectures delay vehicle replacement, extending the service life of high-mileage ICE cars that require shorter drain intervals. In contrast, urban households tend to adopt newer hybrid or BEV models, which reduces engine oil consumption but increases demand for coolant and e-axle fluids. These geographic asymmetries compel suppliers to tailor their channel strategies-premium synthetics and dealer bundling in cities, and conventional oils and retail packs in rural markets-ensuring the Japanese automotive lubricants market remains segment-diverse even as aggregate volume softens.

Competitive Landscape

The market is moderately concentrated. Global majors carve out premium niches through Japan-specific synthetic lines and factory-fill agreements with luxury OEMs. Market consolidation has accelerated; ENEOS shuttered its Wakayama refinery in 2024 and plans to phase out Yokohama lubricant production by 2028, optimizing remaining sites to run higher-value Group III+ streams. Strategic differentiation centers on technology and sustainability. Domestic champions invest in research and development for GLV-grade formulations and bio-based esters, positioning themselves as indispensable partners for OEMs in achieving CAFE compliance. Global players respond with co-engineered e-transmission fluids and battery-thermal-management solutions. Niche specialists FUCHS and Motul target motorsport and high-performance segments, where price sensitivity is minimal. Digital services, including cloud-based oil analytics and QR-code authentication, emerge as table stakes for brand protection and fleet engagement. Competitive rivalry is intense but disciplined; capacity rationalization aligns supply with shrinking demand, averting price wars. However, the proliferation of counterfeit goods on e-commerce platforms pressures brand equity and necessitates joint enforcement initiatives. Overall, the Japan automotive lubricants market balances volume contraction against value-creation levers such as synthetics, services, and sustainability, sustaining profitability for players that pivot quickly.

Japan Automotive Lubricants Industry Leaders

ENEOS Corporation

Idemitsu Kosan Co. Ltd

Exxon Mobil Corporation

Shell plc

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP p.l.c. initiated the sale of its Castrol business, valued at up to USD 10 billion, aiming to meet a USD 20 billion divestment target by 2027. The move could realign Castrol’s strategy in Japan’s premium segment.

- March 2025: ENEOS Corporation announced the phased closure of lubricant production at its Yokohama plant by March 2028. The site currently produces 126,000 kiloliters of lubricants and 3,900 metric tons of grease annually.

Japan Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

What is the projected volume of automotive lubricants consumed in Japan by 2031?

Consumption is forecast to decline to 610.62 million liters by 2031, reflecting a negative CAGR of -1.35% from 2026 levels.

Which product category is shrinking the slowest?

Automatic transmission fluids are declining at only -1.23% CAGR because hybrid powertrains still require specialized ATF formulations.

Why are low-viscosity grades like 0W-8 growing in Japan?

Stringent fuel-economy rules and JASO GLV standards push automakers to specify ultra-low viscosities that trim engine friction by up to 3%.

What technology trend helps fleets reduce lubricant use?

Remote oil-condition monitoring extends drain intervals by 30–50% while cutting unplanned maintenance, especially in heavy-duty trucks and construction equipment.

Page last updated on: