Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

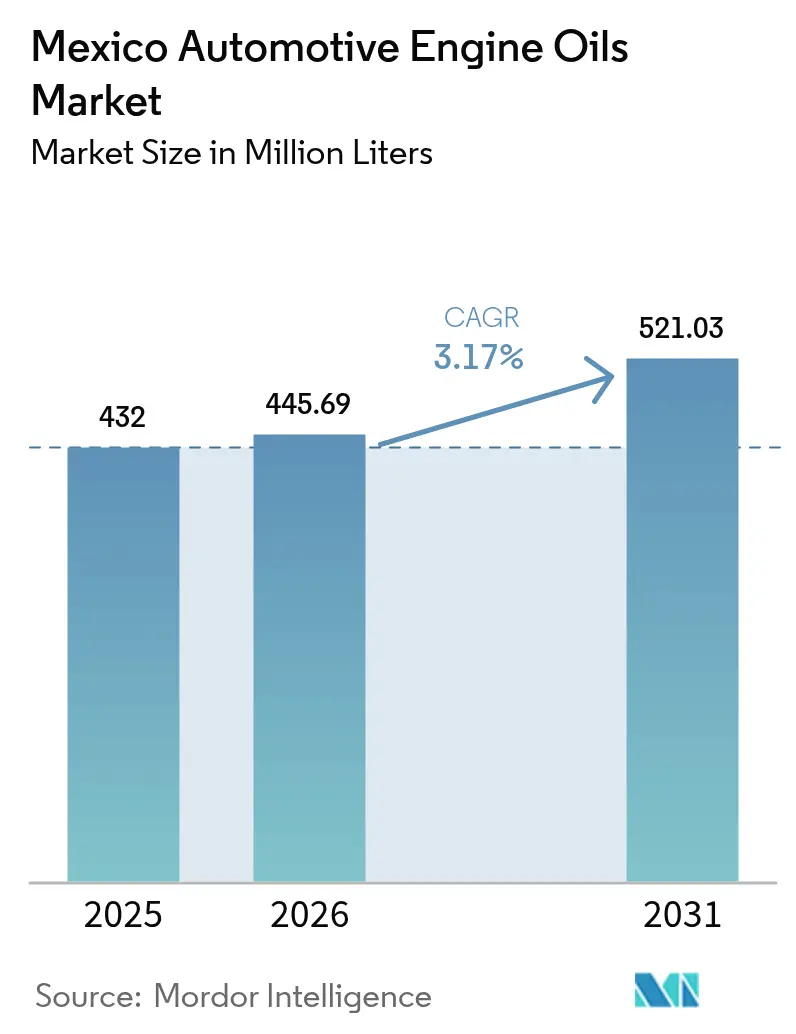

| Base Year Market Size (2025) | 432 Million Liters |

| Market Volume (2026) | 445.69 Million Liters |

| Market Volume (2031) | 521.03 Million Liters |

| Growth Rate (2026 - 2031) | 3.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Automotive Engine Oils Market Analysis by Mordor Intelligence

The Mexico Automotive Engine Oils Market size was valued at 432 Million Liters in 2025 and estimated to grow from 445.69 Million Liters in 2026 to reach 521.03 Million Liters by 2031, at a CAGR of 3.17% during the forecast period (2026-2031). Mexico’s position as Latin America’s second-largest vehicle producer, its expanding passenger-car fleet, and the upcoming alignment of NOM-116 specifications with ILSAC GF-7 collectively underpin steady demand for advanced lubricants. Low-viscosity synthetics are gaining traction as OEM mandates expand, while freight growth related to nearshoring drives sustained demand for heavy-duty applications. The Mexico automotive engine oils market is also benefiting from stricter enforcement against illicit trade, increasing the formal sales base, and from investments in domestic additive and blending capacity that mitigate recent base-oil import restrictions.

Key Report Takeaways

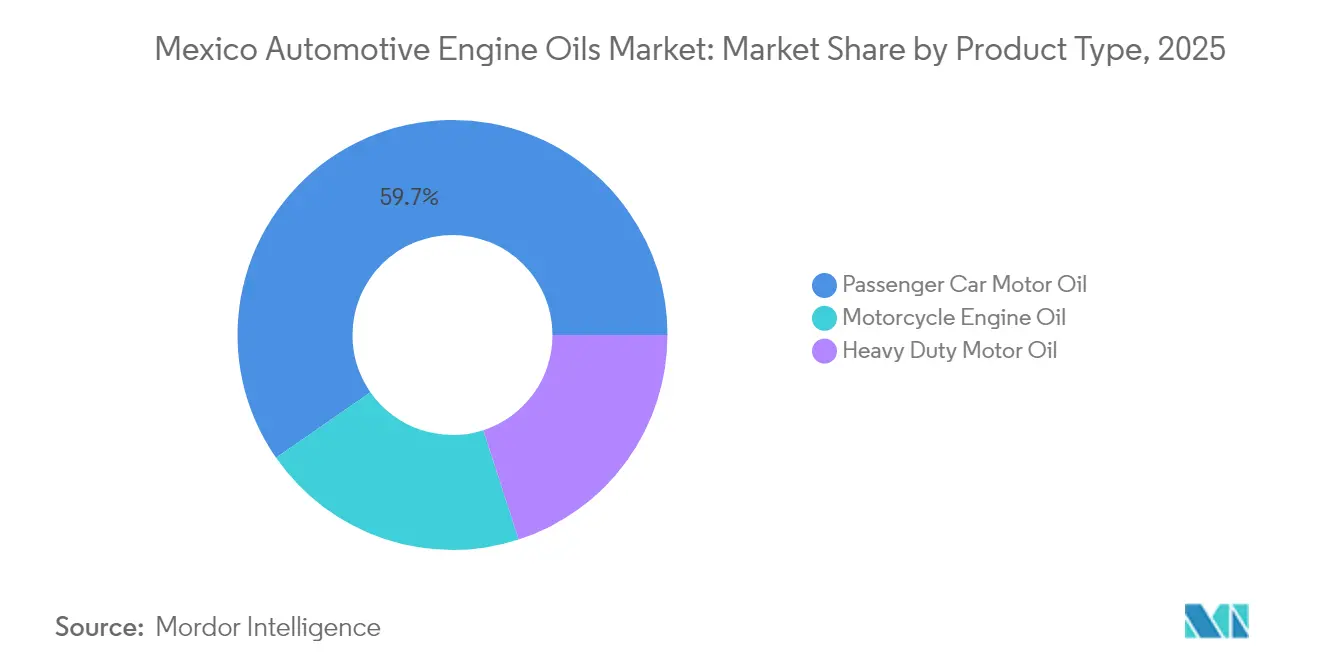

- By product type, passenger car motor oil (PCMO) accounted for 59.68% market share in 2025. However, the market share of motorcycle engine oil (MCO) is expected to increase with the fastest CAGR of 3.42% during the forecast period (2026-2031).

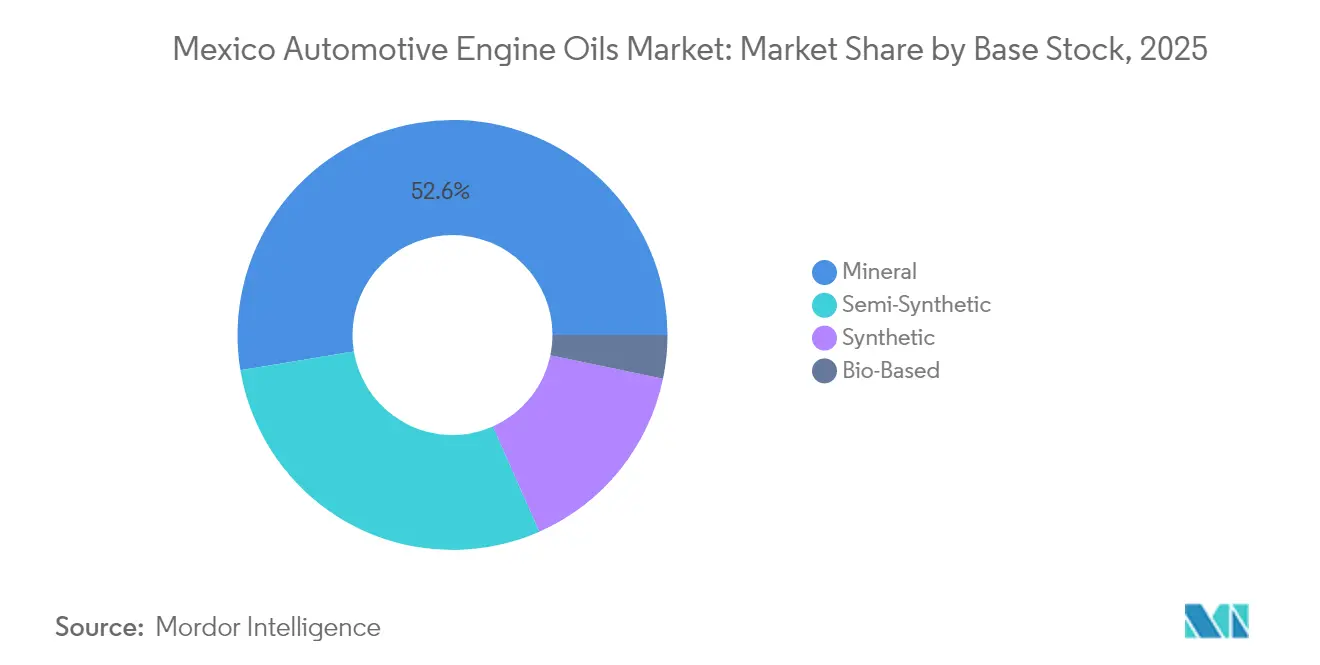

- By base stock, mineral held a share of 52.62% in 2025, and the synthetic base stock's share is expected to grow at a CAGR of 3.54% during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising passenger-car parc and frequent oil changes | +1.2% | Mexico City, Guadalajara, Monterrey metro areas | Medium term (2-4 years) |

| E-commerce freight boom lifting heavy-duty demand | +0.8% | Border states and national logistics corridors | Short term (≤ 2 years) |

| OEM-mandated low-viscosity synthetics under NOM-116 | +0.6% | Nation-wide OEM service networks | Medium term (2-4 years) |

| Anti-smuggling crackdown expanding formal volumes | +0.4% | Tijuana–San Diego and Juárez–El Paso corridors | Short term (≤ 2 years) |

| Rail-served base-oil terminals improving supply | +0.3% | Central industrial belt and Pacific coast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Passenger-Car Parc and High Oil-Change Frequency

Mexico added more than 850,000 passenger vehicles to its national fleet in 2024, and ownership patterns favor two annual oil changes —a rate well above that of the United States[1]Editorial, “La flota vehicular mexicana sigue creciendo,” expansion.mx. The Mexico automotive engine oils market, therefore, enjoys a compounding effect: more vehicles simultaneously require more frequent service. Retail infrastructure is adapting quickly as chains such as OXXO Gas expand from 570 to 1,000 stations, placing branded lubricant kiosks alongside forecourts. Urban air-quality programs also motivate owners to keep engines in peak condition, reinforcing demand for premium PCMO grades that support emission system durability. Taken together, these factors add 1.2 percentage points to the forecast CAGR of the Mexico automotive engine oils market.

E-commerce Freight Boom Lifting Heavy-Duty Demand

Online retail penetration reached 25% of auto-parts sales in 2025 and continues to rise, driving parcel volumes through fulfillment centers located in Monterrey, Tijuana, and Toluca. Each additional van or Class 8 truck in these networks multiplies lubricant consumption because routes combine harsh city stop-and-go traffic with long cross-border hauls. Heavy-duty truck output grew 12.1% year-over-year in 2024, and fleets increasingly specify premium 10W-30 synthetic formulations to gain fuel-economy savings over mineral 15W-40 blends. This logistics-led uptrend contributes 0.8 percentage points to the growth of the Mexico automotive engine oils market.

OEM-Mandated Low-Viscosity Synthetics (NOM-116)

Mexico will publish the revised NOM-116-SCFI standard in 2025 in tandem with ILSAC GF-7, effectively harmonizing labelling, performance tests, and viscosity-grade charts with U.S. and Japanese norms. Hyundai dealers, for example, converted entirely to Shell Helix 0W-20 and 5W-30 under a three-year exclusive signed in February 2024. Field trials demonstrate a 3.5% fuel-economy gain when fleets switch from 5W-40 to 0W-20, yielding significant cost benefits, given that domestic gasoline averages USD 1.22 per liter. These gains, combined with stricter OEM warranty language, increase synthetic penetration and add 0.6 points to the market's CAGR.

Anti-Smuggling Crackdown Expanding Formal Volumes

Customs authorities installed non-intrusive scanners at six major border crossings in 2024, slashing the flow of undeclared lubricant drums. Legitimate suppliers now see higher channel throughput, and consumers report greater confidence in product authenticity. The expanded taxable base enhances public revenue and raises compliance costs for grey-market operators, prompting them to adopt formality or exit. The resulting volume shift supports a 0.4-point increase in the growth rate of the Mexico automotive engine oils market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility squeezing blender margins | -0.9% | Nation-wide, strongest for independent blenders | Short term (≤ 2 years) |

| Gradual EV penetration eroding ICE oil demand | -0.5% | Mexico City and Guadalajara early-adopter zones | Long term (≥ 4 years) |

| Counterfeit lubricants hurting premium adoption | -0.3% | Border regions and open-air markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility Squeezing Blender Margins

Independent blenders import more than 65% of their base-oil requirements, exposing them to Brent swings and peso–dollar fluctuations, which ranged between MXN 18.6 and MXN 19.4 per USD in 2024. In October 2023, administrative barriers lengthened customs clearance to 15 days, increasing working capital needs and warehousing fees[2]Informe trimestral, “Refinación y logística,” pemex.com. Integrated majors offset these shocks with upstream cash flow, yet smaller firms struggle to pass through spot cost spikes, compressing gross margins by up to 3 percentage points and shaving 0.9 points off market CAGR.

Gradual EV Penetration Eroding ICE Oil Demand

Electric-vehicle sales in Mexico reached 2.1% of light-duty vehicle registrations in 2025, a modest base yet growing at a rate of 38% annually as battery-assembly projects in Chihuahua and Coahuila come online. Each new EV eliminates the 3.8 liters of engine oil a typical ICE car consumes per service, curbing future volume growth. While EVs require e-drive fluids, early real-world drain intervals exceed 100,000 km, which limits the near-term offset. The net effect is a 0.5-point CAGR drag on the Mexico automotive engine oils market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominance Driven by Fleet Modernization

Passenger Car Motor Oil (PCMO) held a 59.68% market share of the Mexican automotive engine oils market in 2025, reflecting an installed base of more than 35 million light vehicles. Motorcycle Engine Oil is the fastest-growing sub-segment, with a 3.42% CAGR, driven by two-wheeler registrations for cost-effective commuting. Heavy-Duty Motor Oil ranks second in volume terms, buttressed by the 12.1% jump in class-8 truck output that accompanies nearshoring.

Brands are now orienting their marketing toward durability warranties measured in mileage, with LIQUI MOLY’s Italika tie-up extending drain intervals to 6,000 km on entry-level bikes. PCMO buyers are migrating to 0W-20 and 5W-30 synthetics to secure warranty compliance and fuel savings, a dynamic that nudges average per-liter revenue higher, even if the absolute number of liters remains constant. In heavy-duty fleets, operators are embracing mid-SAPs 10W-30 blends to adhere to emissions limits without the oil-consumption penalties associated with earlier low-ash formulations. These trends collectively reinforce the primacy of PCMO within the Mexico automotive engine oils market.

By Base Stock: Synthetic Transition Accelerates Performance Migration

Mineral oils retained a 52.62% share of the Mexico automotive engine oils market in 2025, primarily driven by cost-sensitive taxi and light truck fleets. Yet, synthetic grades exhibit the strongest momentum, expanding at a 3.54% CAGR as NOM-116 and ILSAC GF-7 mandate tighter control over volatility, shear, and LSPI. Semi-synthetics offer a bridge solution, capturing 29% of the Mexican automotive engine oil industry volume by blending Group II base stocks with performance additives that meet most OEM requirements without the full cost premium.

BASF’s USD investment in Puebla to increase aminic antioxidant output will strengthen the domestic supply of key synthetic additives and reduce lead times for blenders. The parallel development of renewable feedstock blends, such as the BMBcert series, lowers carbon footprints by up to 95%, appealing to ESG-minded corporate fleets. Looking ahead to 2030, the Mexico automotive engine oils market size for synthetic formulations could approach parity with mineral volumes as price gaps narrow and warranty clauses become more stringent.

Geography Analysis

Central Mexico, encompassing Ciudad de México, Estado de México, Puebla, and Querétaro, accounts for approximately 45.60% of Mexico's automotive engine oils market size, thanks to its dense vehicle parc and concentration of assembly plants. This corridor hosts OEMs such as Volkswagen, Toyota, and KIA, ensuring both factory fill and aftermarket throughput. The Bajío region, particularly Guanajuato and Aguascalientes, has seen double-digit annual growth, stimulated by parts suppliers that have relocated from Asia under USMCA rules.

Northern border states—including Nuevo León, Chihuahua, and Coahuila—account for roughly 28.70% of the total volume, driven by cross-border freight and maquila activity. Heavy-duty motor oil demand in the Laredo–Monterrey logistics lanes exceeds national averages by 17%, reflecting the round-the-clock utilization of trucks. Border crackdowns on undeclared lubricant imports have begun to formalize this regional market, resulting in a 4% increase in per-liter realized prices since late 2023. Pacific coast ports, aided by new rail-served tank terminals, now experience faster containerized lube inflows, which trim delivery lead times to states such as Jalisco and Colima.

Southern Mexico presently accounts for less than 7.80% of national volume, limited by lower vehicle density and disposable income. Nonetheless, federal infrastructure spend on the Trans-Isthmus Corridor and near-term refinery upgrades at Salina Cruz aim to catalyze industrial growth that will raise lubricant demand. Blenders view Oaxaca and Chiapas as frontier territories for small-pack mineral oils, banking on rising motorcycle ownership to seed future market expansion.

Competitive Landscape

The Mexico Automotive Engine Oils Market is moderately consolidated. International majors—Shell, ExxonMobil, and BP Castrol—dominate premium synthetics through dealership tie-ins and nationwide quick-lube chains. Domestic champions such as Akron and Roshfrans leverage flexible batch sizes, widespread truck delivery, and trusted neighborhood branding to defend mineral and semi-synthetic niches. Independent blenders respond by co-batching mineral and synthetic lines to share processing costs, preserving margins despite volatile crude inputs.

Mexico Automotive Engine Oils Industry Leaders

Bardahl

BP PLC (Castrol)

ExxonMobil Corporation

Roshfrans

Royal Dutch Shell Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF announced to invest in its manufacturing site in Puebla, Mexico, to increase the capacity of aminic antioxidants for lubricants, including automotive engine oils. This expansion addresses the growing demand for antioxidant additives, driven by increasing stability requirements in lubricating oils.

- December 2024: The Carrera Panamericana, held in Mexico, concluded its 2024 edition, marking a collaboration with LIQUI MOLY as the official automotive engine oil partner of the event. The manufacturer conducted a range of promotional activities, including events at automotive workshops, retail stores, and car dealerships across the nation.

Mexico Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

What is the current size of the Mexico automotive engine oils market?

The market reached 445.69 million liters in 2026.

How fast is demand expected to grow by 2031?

Volume is forecast to climb to 521.03 million liters, reflecting a 3.17% CAGR during the forecast period (2026-2031).

Which product type holds the largest share?

Passenger Car Motor Oil leads with 59.68% of 2025 volume.

Why are synthetics gaining ground?

Revised NOM-116 rules, OEM warranties, and demonstrated 3.5% fuel-economy gains are shifting buyers toward low-viscosity synthetic grades.

Which region consumes the most engine oil?

Central Mexico, including Mexico City and the Bajío corridor, accounts for nearly half of national volume.

Page last updated on: