Jackfruit Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 375.31 Million |

| Market Size (2031) | USD 483.93 Million |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

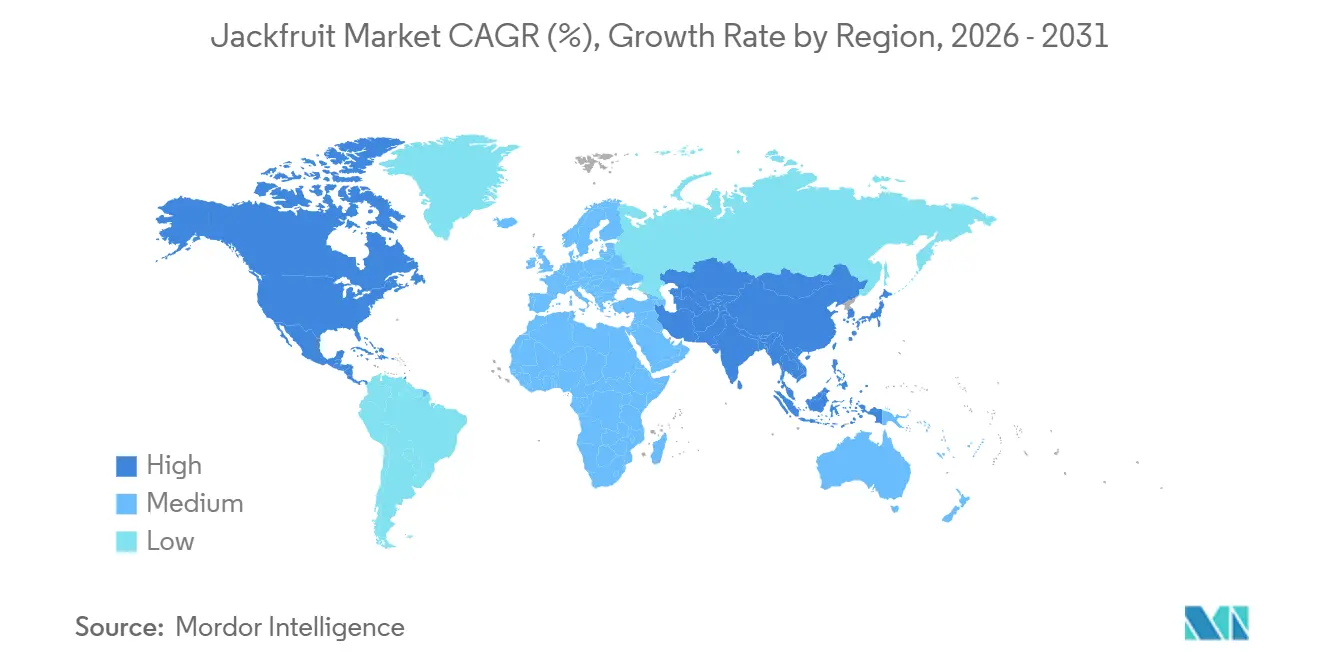

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

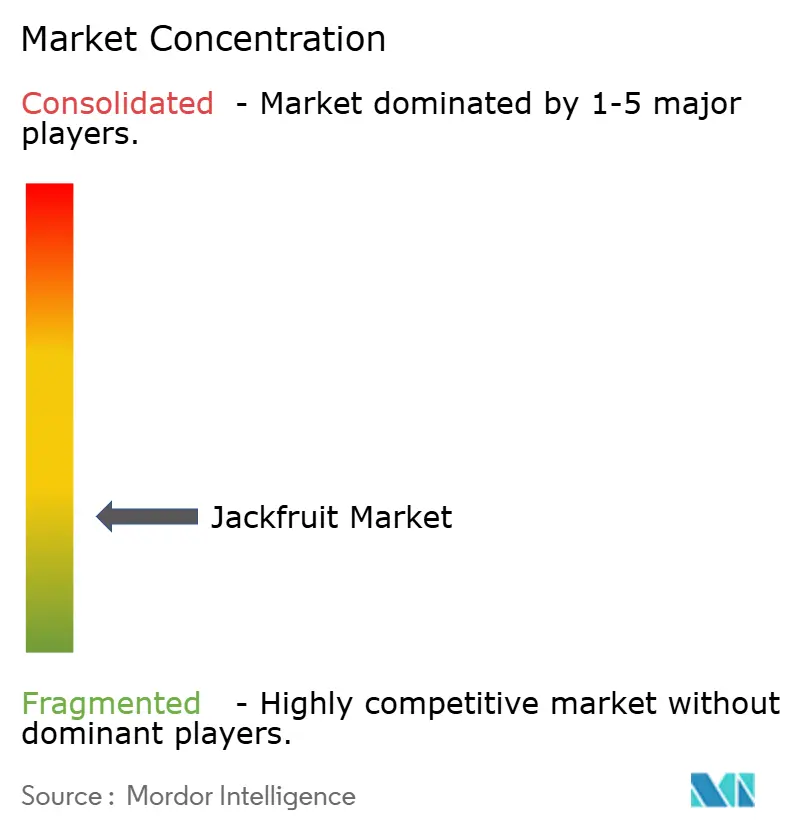

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jackfruit Market Analysis by Mordor Intelligence

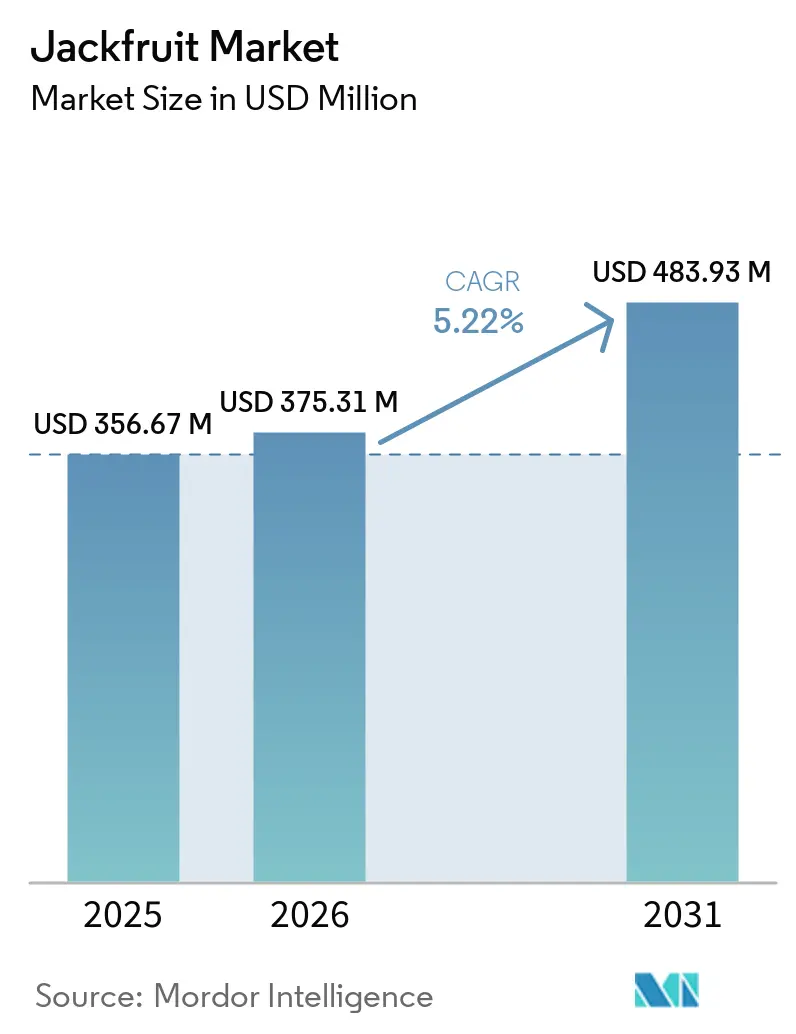

The jackfruit market size is anticipated to increase from USD 356.67 million in 2025 to USD 375.31 million in 2026 and reach USD 483.93 million by 2031, growing at a CAGR of 5.22% over 2026-2031. The jackfruit market is moving beyond its older dependence on fresh tropical consumption and ethnic grocery demand, as plant-based positioning, shelf-stable processing, and by-product monetization become more central to commercial growth. The category is also seeing a shift in value toward processed uses, indicating that revenue growth in the jackfruit market is being shaped more by format innovation than by raw fruit trade alone. Asia-Pacific remains the production and consumption base for the jackfruit market, while developed markets are creating new demand through mainstream retail and foodservice adoption of plant-based jackfruit formats. Regulatory controls in the European Union and China show that the jackfruit market now faces a more formal trade environment, where traceability, orchard registration, and phytosanitary compliance matter more than before. That shift creates clearer opportunities for companies that can combine processing scale, quality consistency, and compliant export systems across the jackfruit market.

Key Report Takeaways

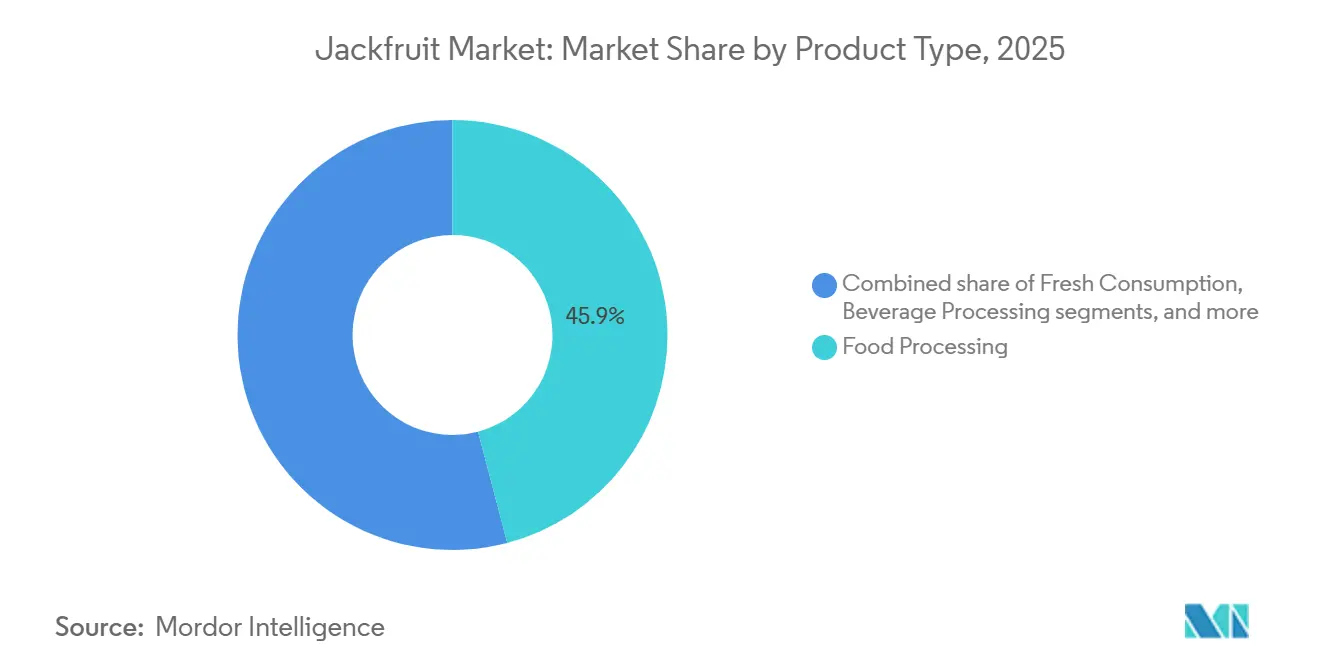

- By product type, food processing was the largest segment, accounting for 45.9% of the jackfruit market size in 2025, while plant-based meat products are the fastest-growing segment and are projected to expand at a 6.7% CAGR during 2026-2031.

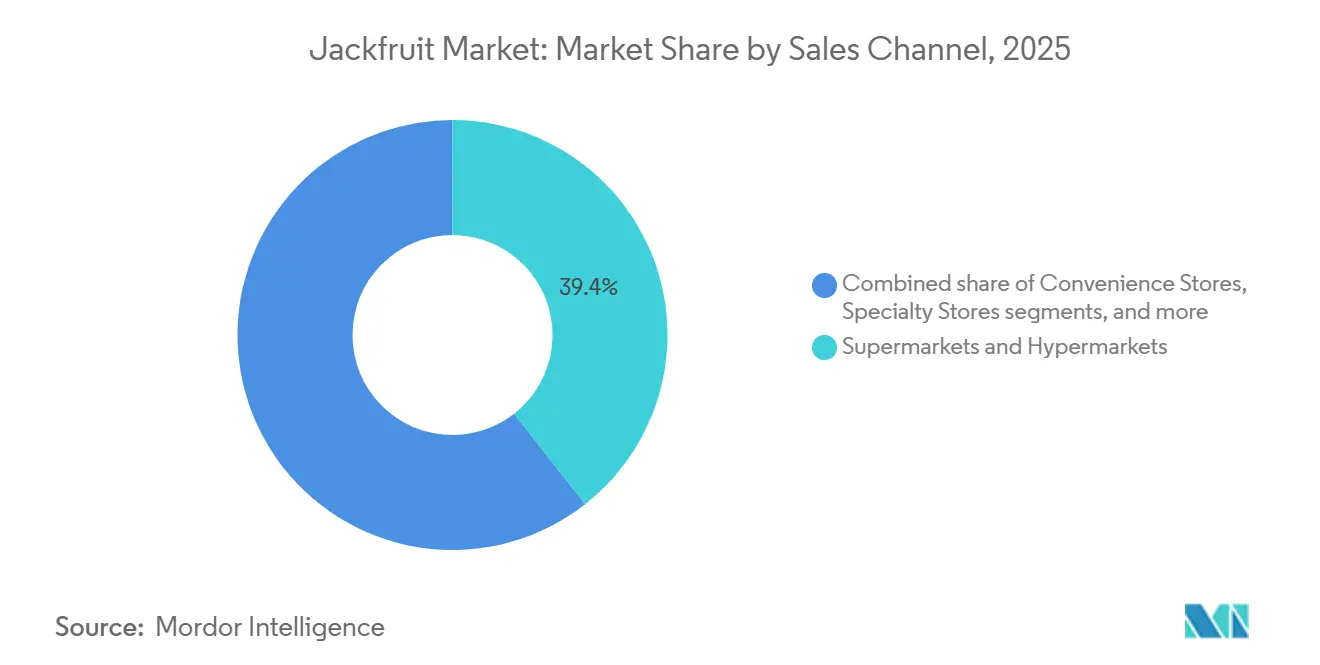

- By sales channel, supermarkets and hypermarkets were the largest segment, accounting for 39.4% of the jackfruit market share in 2025, while online retail is the fastest-growing segment, with a projected 7.2% CAGR during 2026-2031.

- By geography, Asia-Pacific was the largest regional segment with 70.3% share in 2025, while North America will be the fastest-growing regional segment with a 6.5% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Jackfruit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Plant-based meat alternative adoption | +1.20% | Strongest in North America and Europe, expanding in urban Asia-Pacific | Medium term (2–4 years) |

| Health and fiber-led consumer positioning | +0.90% | Global relevance, especially North America and Asia-Pacific | Medium term (2–4 years) |

| Processed format expansion across retail and foodservice | +0.80% | Important in North America, Europe, and Asia-Pacific export markets | Short term (≤ 2 years) |

| Product innovation in snacks, ready meals, and beverages | +0.70% | Most visible in North America and Europe, expanding into Asia-Pacific | Medium term (2–4 years) |

| By-product valorization into flour, pectin, and biomaterials | +0.60% | Led by Asia-Pacific, with growing interest in Europe and the Middle East | Long term (≥ 4 years) |

| Shelf-life extension through high-pressure processing (HPP), modified atmosphere packaging (MAP), and advanced drying | +0.40% | Relevant in Asia-Pacific and emerging export hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Plant-Based Meat Alternative Adoption

Young jackfruit has a fibrous structure that allows it to mimic pulled meat applications without relying on extrusion or isolated proteins, giving the jackfruit market a distinct place in the wider plant-based foods space. The Good Food Institute reported that shreds, chunks, and strips, the core commercial form that includes jackfruit products, posted 8% unit sales growth in 2025 and 14% unit growth in the natural channel, even as the broader United States retail plant-based meat and seafood category declined 10% in dollar sales [1]Source: The Good Food Institute, “Analyzing Plant-Based Meat and Seafood Sales,” gfi.org. That pattern suggests that buyers are still willing to purchase products that feel less engineered and more recognizable, which supports a longer runway for plant-based jackfruit within the jackfruit market. Performance Food Group reinforced that commercial case in November 2024 when it launched the FarmSmart Beef and Jackfruit Burger with the Jackfruit Company, a product distributed through its foodservice network and positioned with 40% less saturated fat and 40% lower cholesterol than a 100% beef burger. As foodservice buyers test blended formats with familiar eating quality, the jackfruit market gains access to a broader operator base that may not have adopted fully plant-based menu items at scale.

Health and Fiber-Led Consumer Positioning

Health messaging is becoming increasingly important in the jackfruit market because jackfruit aligns with consumer demand for recognizable ingredients, fiber, and simpler product labels. Companies such as The Jackfruit Company have positioned jackfruit as a whole-food meat alternative with a naturally fibrous texture and clean-label appeal, supporting broader consumer interest in minimally processed plant-based meal options. The Good Food Institute found that consumers who view plant-based meat as healthier, including for higher fiber and lower saturated fat, tend to spend more in the category, which matters for premium plant-based jackfruit products. This is helping the jackfruit market appeal to flexitarian households that are not necessarily seeking a perfect meat replica, but do want a whole-food option that feels easier to trust. In practical terms, health-led positioning is expanding the jackfruit market's consumer base beyond tropical familiarity into broader clean-label meal occasions.

Processed Format Expansion Across Retail and Foodservice

Processed formats are expanding the jackfruit market because they remove the handling difficulty associated with whole fruit, which can weigh up to 45 kg and deliver only 30% to 35% edible content[2]Source: Taylor & Francis, “Insights into Phytonutrient Profile and Postharvest Quality Management of Jackfruit, A Review,” Critical Reviews in Food Science and Nutrition, tandfonline.com. Canned, pouch, frozen, and ready-to-cook formats allow retailers, food manufacturers, and foodservice buyers to source jackfruit in standardized forms rather than manage sticky latex, rind disposal, and labor-intensive cutting. Kiril Mischeff’s January 2025 promotion of 2.5 kg prepared jackfruit pouches as ready-stock products available for immediate dispatch highlighted the increasing commercialization of processed jackfruit formats within foodservice and ingredient supply channels. That matters because a processed procurement model supports repeat buying, broader menu use, and easier category planning across the jackfruit market. The companies that control processing assets are therefore in a stronger position to capture value in the jackfruit market than firms that remain limited to fresh fruit aggregation.

Product Innovation in Snacks, Ready Meals, and Beverages

Product innovation is expanding the jackfruit market's use cases beyond canned young fruit and simple meat substitutes. In 2024, the postharvest review in Critical Reviews in Food Science and Nutrition described several value-added product pathways, including ready-to-serve beverages, seed-based chocolate, cookies, and other processed formats developed from different parts of the fruit. Commercial activity is growing within mainstream food manufacturing channels. In early 2025, Fiber Foods secured orders from leading Dutch meat producers to develop hybrid sausages, burgers, and croquettes using its PrimeJack dehydrated jackfruit ingredient. These blended products incorporate up to 40% jackfruit into traditional meat formulations, aiming to reduce carbon footprints and lower saturated fat content. This broadening product map gives the jackfruit market more pricing tiers, more consumer entry points, and more routes into private-label and business-to-business development. It also reduces the risk that the jackfruit market will remain tied to a single product story or a single retail shelf location.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High perishability and post-harvest losses | -0.70% | Global issue, especially in Asia-Pacific and parts of Africa | Short term (≤ 2 years) |

| Seasonal supply swings and cold-chain gaps | -0.50% | Most acute in Asia-Pacific production and export markets | Medium term (2–4 years) |

| Export compliance bottlenecks in origin markets | -0.40% | Concentrated in Asian exporters serving Europe and China | Medium term (2–4 years) |

| Limited harvest standardization and orchard commercialization | -0.30% | Most relevant in India, Bangladesh, and similar producer markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Perishability and Post-Harvest Losses

High perishability remains a significant restraint in the jackfruit market, as it reduces the usable supply before processors or exporters can generate revenue from the fruit. A 2025 assessment published in the International Journal of Environmental & Agriculture Research (IJOEAR) reported that postharvest fruit and vegetable losses in Sri Lanka had previously reached 30–40%, underscoring the broader spoilage risks affecting tropical fruits such as jackfruit in markets with limited cold-chain infrastructure and inadequate handling systems. Supporting this issue, a 2025 study published in the Journal of Current Science and Technology found that untreated jackfruit deteriorated rapidly during storage, whereas treatments with hydrogen peroxide and 1-MCP were necessary to significantly reduce disease incidence and weight loss. This challenge creates a difficult commercial cycle in the jackfruit market, where farmers often encounter price declines during peak seasons, while processors face shortages of usable quality outside limited procurement periods. Without increased adoption of cold storage and value-added processing, the jackfruit market will continue to experience avoidable waste and unstable supply dynamics.

Seasonal Supply Swings and Cold-Chain Gaps

Seasonal supply swings and cold-chain gaps create uneven raw material availability across the jackfruit market, even in countries with strong production bases. The fruit’s size, ripening pattern, and handling sensitivity make it difficult to move large harvests efficiently without chilled logistics and standardized pre-processing systems. A 2025 study published in Food and Nutrition Sciences on intelligent packaging for processed jackfruit found that advanced storage and packaging systems could significantly extend product shelf life and maintain quality, highlighting how inadequate cold-chain and packaging infrastructure directly accelerates spoilage and reduces commercial usability in conventional supply chains. These swings matter because processing plants need consistent intake to run economically, and retailers need a dependable supply to keep the category visible year-round. As a result, the jackfruit market often sees a mismatch between abundant fruit availability at harvest and limited commercial availability in more distant consumer markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food Processing Anchors the Market as Plant-Based Formats Accelerate

Food processing accounted for 45.9% of the jackfruit market size in 2025 and remained the largest product type, as it already has the strongest trade and processing infrastructure. The largest segment benefits from established demand for canned, pouch, frozen, and ready-to-cook formats that are easier to export and easier for foodservice buyers to use. Fresh consumption still holds an important place in producing countries, but it plays a smaller commercial role in the global jackfruit market because of perishability, preparation difficulty, and uneven cold-chain access, which limit wider trade. Beverage Processing is still emerging, yet the scientific literature already points to juice and ready-to-serve beverage pathways that could widen commercial use in the jackfruit industry over time. Functional and health products remain at an early stage, though seed- and flour-based product types suggest the jackfruit market can move into more specialized food and ingredient formats as commercialization improves.

Plant-based meat products are the fastest-growing product type segment, projected to grow at a 6.7% CAGR during 2026-2031, keeping it ahead of the broader jackfruit market. A 2025 study by the ICAR-Indian Institute of Horticultural Research, which evaluated 94 jackfruit accessions in southern Karnataka, reported flake recovery rates ranging from 15.8% to 49.7%. This indicates significant variability in edible yield and processing suitability among the cultivars [3]Source: Nature, “Characterization of Jackfruit Artocarpus heterophyllus Lam. for Economic Traits in Dry Zones of Karnataka, India,” Scientific Reports, nature.com. The study further observed that accessions with thicker, crunchier flakes and lower rind weight demonstrated greater potential for commercial use and value-added processing. Fiber foods also received commercial orders in early 2025 from major Dutch meat producers for liver sausage, burgers, and croquettes using its PrimeJack ingredient, which confirms that adoption is moving into business-to-business manufacturing channels. As a result, the fastest-growing segment is built on repeat industrial use rather than short-lived novelty, giving the jackfruit market a firmer growth base through 2031.

By Sales Channel: Supermarkets and Hypermarkets Lead While Online Retail Expands Reach

Supermarkets and hypermarkets accounted for 39.4% of revenue in 2025 and were the largest sales channel in the jackfruit market. The largest channel reflects the category’s shift from specialist retail into mainstream grocery, where processed formats are easier to merchandise and easier for consumers to understand. This channel also benefits from the growing role of prepared products, which fit routine store operations much better than whole fresh fruit, which is high in handling complexity. Specialty stores and convenience stores remain relevant for premium, natural, or impulse-led purchases, while foodservice and wholesale support institutional volume and menu development across the jackfruit market.

Online retail is the fastest-growing sales channel and is forecast to advance at a 7.2% CAGR during 2026-2031, making it an important growth lever for the jackfruit market. Digital channels help brands reach vegan, vegetarian, and flexitarian households that may not find a full range of plant-based jackfruit products in physical stores. Online listings also work well for shelf-stable, frozen, premium, and trial-oriented formats because product education, recipes, and ingredient details can be displayed more effectively than on a crowded shelf. That dynamic supports higher-value positioning in the jackfruit market, especially for products that rely on health, convenience, or clean-label messaging rather than on price alone. Over time, the fastest channel is likely to reward companies that can balance direct consumer communication with dependable fulfillment and repeat purchase conversion.

Geography Analysis

Asia-Pacific accounted for 70.3% of the jackfruit market share in 2025 and remained the largest regional base for production, consumption, and primary processing. India, Bangladesh, Thailand, and Indonesia continue to anchor the jackfruit market in the region because they combine large agricultural output with established familiarity in local diets. The Food and Agriculture Organization identified jackfruit as Bangladesh’s priority product under the One Country One Priority Product initiative, indicating that value-added export development is becoming a policy focus rather than solely a private-sector effort. Even so, the region still carries major postharvest losses and commercialization gaps, which hold back the full revenue potential of the jackfruit market despite abundant fruit supply. Growth in Asia-Pacific is therefore supported more by improved processing, storage, and export formalization than by basic supply growth alone.

North America is the fastest regional segment in the jackfruit market and is projected to grow at a 6.5% CAGR during 2026-2031. Mainstream plant-based eating occasions, whole-food product positioning, and wider retail and foodservice penetration beyond specialty vegan channels are supporting demand in this region. Walmart and Target are offering shelf placement for plant-based snacks and meat alternatives that include jackfruit jerky, ready-to-cook pulled jackfruit, and frozen meal kits, signaling stronger acceptance of jackfruit products in mass retail rather than only natural food stores. Whole Foods Market and Sprouts Farmers Market also increased visibility of clean-label tropical fruit snacks and minimally processed meat alternatives, supporting premium positioning for jackfruit-based products across North America. At the same time, brands such as Upton’s Naturals and Big Mountain Foods are offering barbecue-style and spicy jackfruit snack offerings targeted at flexitarian consumers seeking recognizable ingredients and lower-processed alternatives to soy-based meat substitutes. These developments indicate that North American demand growth is increasingly tied to mainstream retail accessibility, convenience-driven plant-based meals, and clean-label snacking trends rather than niche vegan consumption alone.

Europe is the next important growth market for jackfruit, as retailers, ingredient suppliers, and meat processors are testing more processed and blended formats. Kiril Mischeff’s 2025 push for ready-to-use jackfruit pouches and Fiber Foods’ 2025 orders from Dutch meat producers show that Europe is building both retail-facing and manufacturing-facing demand. South America is earlier in formal commercialization, yet it has long-term potential for local production to support low-cost processing and regional product development. The Middle East and Africa are still smaller in terms of current demand, but they are gaining relevance as import markets and as potential future supply locations for value-added ingredients. Over the longer term, the jackfruit market could see a broader production map if African processors scale near-source dehydration and other shelf-life-enhancing formats for export.

Competitive Landscape

The jackfruit market remains fragmented because fresh fruit trade is still spread across many local and regional suppliers, while the branded processed segment is only partially consolidated. This means competitive strength in the jackfruit market often depends less on brand size alone and more on sourcing reach, processing control, and channel fit. The Jackfruit Company, Kiril Mischeff Limited, LOTAO GmbH, Mother Dairy Fruit and Vegetable Private Limited, and Samroiyod Corporation Ltd. were the key players in 2025 and are positioned around different strengths, including business-to-business supply, packaged retail formats, domestic distribution, and jackfruit-focused processing. In practice, the companies with clearer processing capabilities are better placed to shape value capture in the jackfruit market than firms that stay concentrated in the fresh fruit movement. The competitive picture also remains open because no single global business model has yet defined how scale will be built across all regions of the jackfruit market.

Strategic moves since 2024 show that commercial momentum is coming from partnerships, product development, and processing innovation rather than from large-scale consolidation. In February 2025, Fiber Foods secured funding from VP Capital, the Blossom Ventures Syndicate, and the Brabant Development Agency and received early 2025 orders from large Dutch meat producers for hybrid products based on its dried jackfruit ingredient technology. In January 2025, Institut Pertanian Bogor University installed a Hiperbaric 55 system to support research on jackfruit and other tropical fruits, a move that could later influence how processors handle preservation and compliance in Southeast Asia. These actions show that the competitive direction of the jackfruit market is being set by companies and institutions that can address texture, shelf life, and channel adoption simultaneously.

Another important shift is the rise of ingredient-led competition, which may become more influential than consumer branding in several parts of the jackfruit market. Fiber Foods’ model of processing dried jackfruit ingredients for hybrid meat applications is one example of how companies can sell into existing protein systems rather than build standalone retail categories first. Companies that monetize seeds, peel, and other fractions could also improve their cost structures and sustainability claims, making them more resilient in the jackfruit market. At the same time, exporters with stronger traceability and orchard registration systems are likely to gain an edge as border checks and import rules become more demanding. The businesses that combine raw material discipline, processing flexibility, and compliant export execution are therefore best placed to strengthen their standing in the jackfruit market through 2031.

Jackfruit Industry Leaders

The Jackfruit Company

Mother Dairy Fruit and Vegetable Private Limited

Kiril Mischeff Limited

Samroiyod Corporation Ltd.

LOTAO GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: India-based jackfruit producer network Jackfruitking Agro Producers Company Pvt. Ltd., expanded its integrated jackfruit farming and processing operations in Maharashtra, managing more than 88 jackfruit varieties and supplying approximately 30,000-35,000 grafted plants annually.

- February 2025: Fiber Foods secured investment from VP Capital, Blossom Ventures Syndicate, and the Brabant Development Agency to scale production of its dried jackfruit ingredient PrimeJack. The company simultaneously received commercial orders from major Dutch meat producers for hybrid liver sausage, burgers, and croquettes, targeting retail distribution in the Netherlands.

- January 2025: Institut Pertanian Bogor University in Indonesia installed a Hiperbaric 55 High-Pressure Processing machine to advance food science research on tropical fruits, including jackfruit. The university is committed to collaborating with Indonesia’s Food and Drug Administration to establish High-Pressure Processing regulatory frameworks in Southeast Asia, signaling an early-stage policy pathway for High-Pressure Processing tropical ingredients in the region.

Global Jackfruit Market Report Scope

The jackfruit market covers fresh jackfruit and processed jackfruit products sold for food, beverage, functional, and plant-based meat uses through retail, wholesale, and foodservice channels. The Jackfruit Market is Segmented by Product Type (Fresh Consumption, Food Processing, Beverage Processing, Functional and Health Products, and Plant-Based Meat Products), by Sales Channel (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, and Foodservice and Wholesale), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). Market Forecasts are in Value (USD).

| Fresh Consumption |

| Food Processing |

| Beverage Processing |

| Functional and Health Products |

| Plant-Based Meat Products |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail |

| Foodservice and Wholesale |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Product Type | Fresh Consumption | |

| Food Processing | ||

| Beverage Processing | ||

| Functional and Health Products | ||

| Plant-Based Meat Products | ||

| By Sales Channel | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Foodservice and Wholesale | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the jackfruit market by 2031?

The jackfruit market is projected to reach USD 483.93 million by 2031, up from USD 375.31 million in 2026, with a 5.22% CAGR during 2026-2031.

Why is Asia-Pacific so important for global supply?

Asia-Pacific held 70.3% of revenue in 2025 and remains the main production base, with India, Bangladesh, Thailand, and Indonesia shaping farm supply, early processing, and export activity.

What is the biggest operational challenge for suppliers and exporters?

High perishability remains the biggest challenge because post-harvest losses are significant, cold-chain coverage is uneven, and export markets are applying stricter traceability and phytosanitary requirements.

How are companies building competitive advantage in this category?

Companies are improving their position through processing control, product innovation, shelf-life technologies, hybrid meat partnerships, and stronger compliance systems for export markets.

Page last updated on: