Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 84.55 Billion |

| Market Size (2026) | USD 89.33 Billion |

| Market Size (2031) | USD 117.57 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

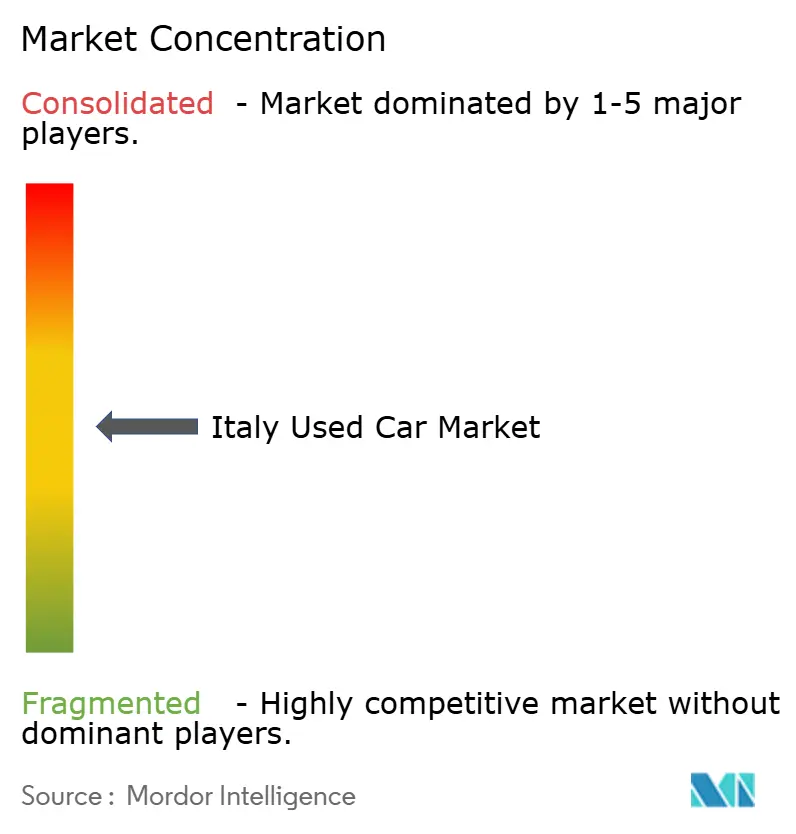

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Used Car Market Analysis by Mordor Intelligence

Italy used car market size in 2026 is estimated at USD 89.33 billion, growing from 2025 value of USD 84.55 billion with 2031 projections showing USD 117.57 billion, growing at 5.65% CAGR over 2026-2031. Consumer migration from rising new-car prices, the country’s 12.8-year average fleet age, and the availability of off-lease inventory set the tone for sustained growth. Strong online engagement, led by platforms that generate more than 2 billion annual searches, is widening geographic reach and easing price discovery. Regulatory pressure on older diesel vehicles, coupled with Stellantis' production shifts toward premium segments, is tightening supply in certain categories and underpinning residual values. Increasing adoption of certified-pre-owned programs and telematics-based scoring mechanisms is elevating buyer confidence and stimulating repeat purchases across the Italy used car market coming years.

Key Report Takeaways

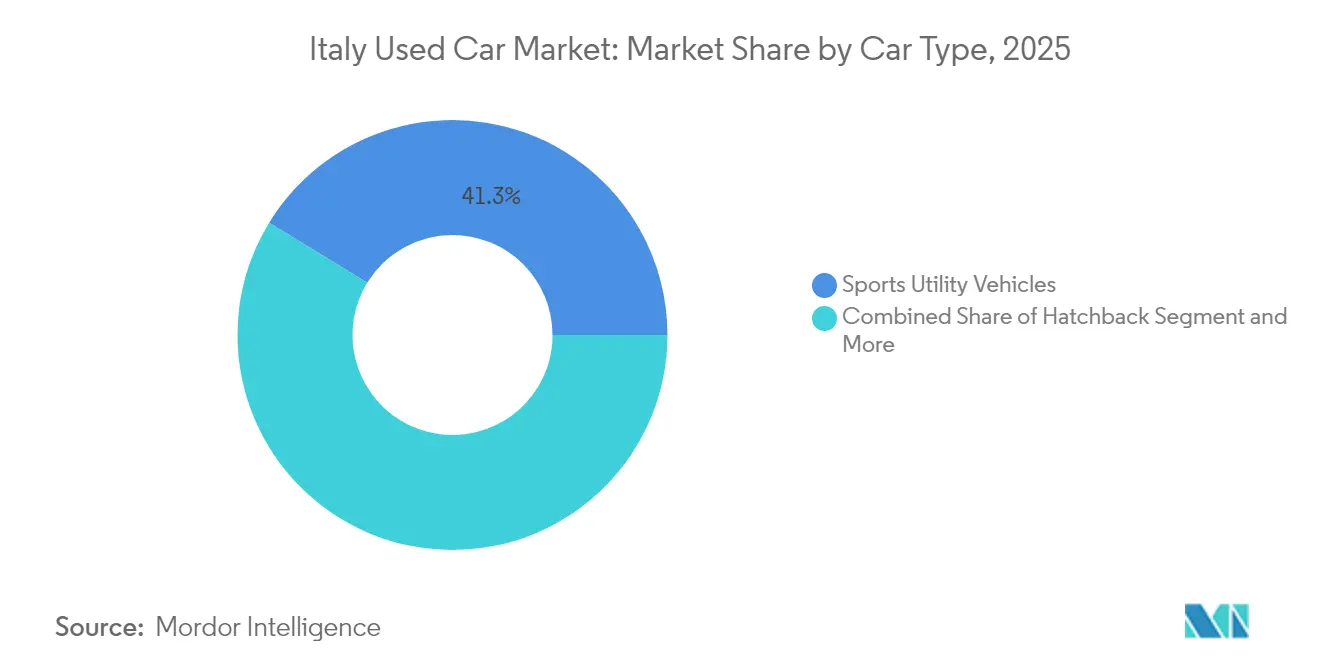

- By car type, SUVs led with 41.25% revenue share in 2025; SUVs are forecast to grow at a 7.12% CAGR to 2031.

- By propulsion, ICE vehicles held 84.10% of the Italy used car market share in 2025, while BEVs are projected to expand at a 17.54% CAGR through 2031.

- By vendor type, unorganized dealers accounted for 62.30% share of the Italy used car market size in 2025; organized dealers record the highest projected CAGR at 7.20% through 2031.

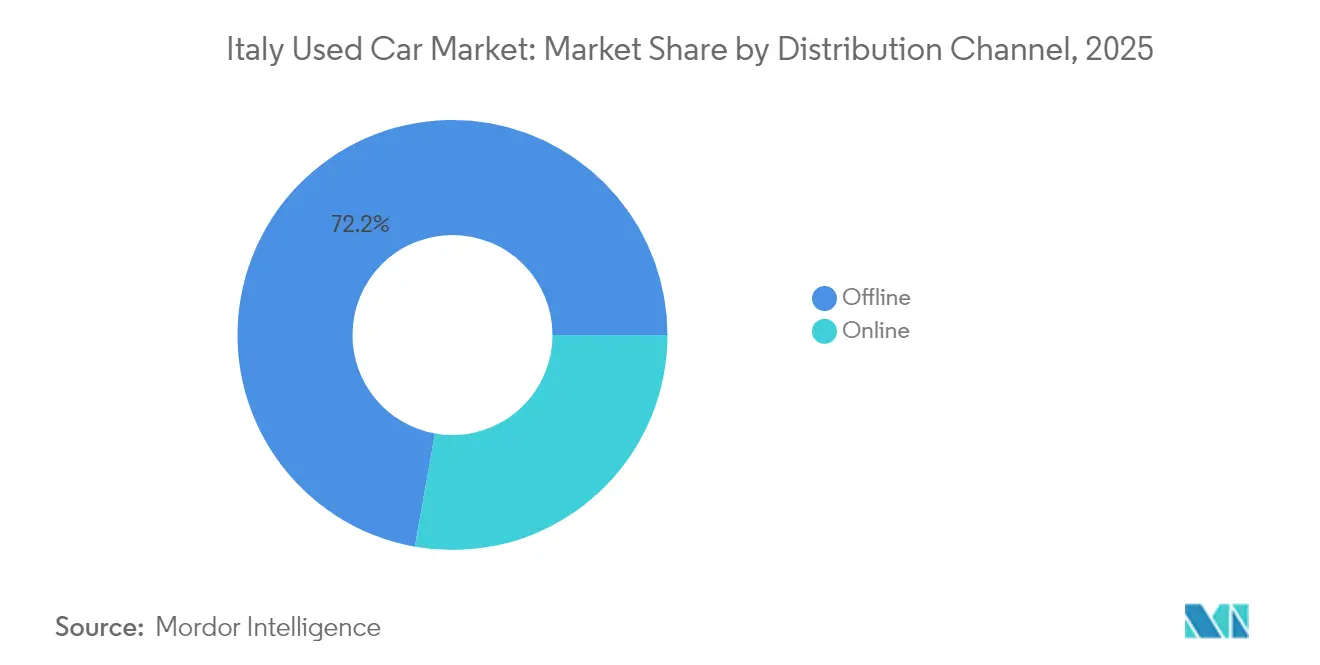

- By distribution channel, offline outlets captured 72.20% of the Italy used car market size in 2025; online channels grow fastest at 14.45% CAGR to 2031.

- By vehicle age, the 4-6 years bracket held 30.60% share of the Italy used car market size in 2025, while the 0-3 years bracket grows fastest at 4.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| New-Car Price Inflation Shifts Demand | +1.2% | National, with stronger impact in northern industrial regions | Short term (≤ 2 years) |

| Online Used-Car Platforms Proliferate | +0.8% | National, with higher penetration in urban centers | Medium term (2-4 years) |

| OEM CPO Programs Expand | +0.6% | National, concentrated in major metropolitan areas | Medium term (2-4 years) |

| Off-Lease Returns Boost Supply | +0.9% | Northern Italy, particularly Lombardy and Veneto | Short term (≤ 2 years) |

| Eco Trade-Ins Add ICE Stock | +0.4% | National, with regional variations based on local policies | Long term (≥ 4 years) |

| Telematics Scores Build Buyer Trust | +0.3% | Urban centers initially, expanding to national coverage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising New-Car Prices Shift Demand to Used

The ratio of used-to-new registrations climbed in early 2025 as OEMs prioritized higher-margin models, pricing many households out of factory-fresh vehicles [1]Redazione Quattroruote, “ACI: in Italia le auto sono sempre più vecchie,” Quattroruote, quattroruote.it . This redirected demand favors Euro 6 petrol and mild-hybrid cars listed between EUR 9,000 and EUR 15,000, a price corridor where inventory remains fluid. The shift has been strongest in Lombardy and Piedmont, regions hit hardest by 2025 diesel restrictions, and is expected to sustain headline growth in the Italy used car market into 2026.

Proliferation of Online Used-Car Platforms

Digital marketplaces deliver national exposure previously unavailable to local dealers, with one leading portal counting of million users in 2024. Click-to-lead conversion tools, embedded financing calculators, and verified seller ratings compress transaction times while raising transparency. Urban millennials, the cohort most comfortable with digital buying, are extending the Italy used car market beyond regional boundaries, hastening price convergence among northern and southern provinces[2]BeBeez Staff, “Hellman & Friedman compra AutoScout24,” BeBeez, bebEEz.it .

Expansion of OEM Certified-Pre-Owned Programs

Programs such as SPOTICAR and Toyota Plus combine 100-point inspections with 12-month warranties to ease reliability concerns around hybrids and BEVs. Factory-grade diagnostic equipment and software updates give OEM stores an edge in marketing late-model electrified vehicles, and the certification badge commands a premium that organized dealers readily capture. The trend supports value retention and repeats purchases, particularly in metropolitan areas where warranty coverage mitigates commuter range anxiety[3]Giulio Piovaccari & Valentina Za, “Stellantis Italy output falls 37% in 2024, car production hits 68-year low,” Reuters, reuters.com.

Surging Off-Lease Returns Fuel Supply

Corporate fleets returning 36- to 48-month-old vehicles are replenishing dealer lots with documented service histories. Leasing companies concentrated in Lombardy and Veneto are feeding a steady stream of sub-50,000-km units, balancing the supply shortfall caused by the 37% production decline at Italian factories in 2024. This supply is especially relevant for the Italy used car market because it maintains quality standards while satisfying demand for near-new inventory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sparse Vehicle-History Databases | -0.5% | National, with greater impact in fragmented dealer networks | Medium term (2-4 years) |

| Low-Emission Zones Deter Old Diesels | -0.8% | Northern Italy, particularly Milan, Turin, and major urban centers | Short term (≤ 2 years) |

| Quality Stock Exports Eastward | -0.4% | National, with concentration in border regions | Medium term (2-4 years) |

| Reconditioning Costs Rise on Labor Gaps | -0.6% | National, with acute impact in industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Standardized Vehicle-History Databases

Italy relies on piecemeal service records instead of a unified national title registry, leaving gaps that erode buyer confidence during purely online transactions. Insurtech tools using AI image recognition to validate exterior damage are emerging, yet mass adoption hinges on regulatory harmonization and dealer cooperation mdpi.com. Until that occurs, cautious shoppers may restrict budgets or select certified stock only, modestly capping expansion in the Italy used car market.

Low-Emission Zones Discourage Older Diesel Purchases

From October 2025, Euro 5 diesels face weekday bans across four northern regions, affecting more than 1 million vehicles. Dealers must reposition restricted stock to less-regulated territories or accept steeper markdowns, a logistical shuffle that elevates holding costs and limits segment turnover. The same policy, however, stimulates demand for compliant Euro 6 units and BEVs, reinforcing the age and powertrain tilt already underway in the Italy used car market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Car Type: Sport Utility Vehicles Dominates The Market

SUVs Drive Premium Positioning SUVs generated 41.25% of total 2025 sales and are forecast to advance at a 7.12% CAGR, retaining the top perch in the Italy used car market. Compact crossovers such as the Jeep Avenger benefit from urban practicality while matching lifestyle aspirations for ground clearance and perceived safety.

Hatchbacks, represented by the Fiat Panda’s remain crucial for budget-oriented shoppers yet cede share to SUVs that narrow the efficiency gap. On the premium end, Maserati and Alfa Romeo vehicles fall victim to volatile production flows but uphold Italy’s performance heritage, supporting a small high-margin niche. Meanwhile, MPVs cater to larger families but confront SUV cannibalization, reinforcing the two-tier demand curve that defines car-type preferences across the Italy used car market.

By Propulsion: Electric Surge Challenges ICE Dominance

Electric Surge Challenges ICE Dominance ICE units delivered 84.10% of 2025 transactions, yet BEVs post a 17.54% forecast CAGR that outpaces every other powertrain. Hybrids leverage Stellantis leadership, adding electric operating capability without range concerns and winning urban commuters constrained by low-emission zones.Residual-value stabilization, expanded charging infrastructure, and extended battery warranties reduce ownership risk. LPG and CNG stay relevant among cost-conscious rural drivers but face infrastructure erosion, gradually compressing their footprint within the broader Italy used car market.

By Vendor Type: Unorganized Vendor Dominates The Market

Unorganized operators captured 62.30% revenue in 2025, yet organized chains are scaling at 7.20% CAGR by rolling out omnichannel interfaces, captive financing, and reconditioning hubs that small dealers struggle to match. Formal groups negotiate bulk sourcing from auctions and off-lease feeders, creating inventory velocity and consistency. Independents still flourish where personal rapport overrides brand uniformity, particularly in small towns where cultural familiarity matters.Regulatory compliance on consumer protection, digital invoicing, and emissions disclosure nudges the landscape toward professionalization. As organized entities digest smaller rivals, the Italy used car market experiences a gradual but noticeable shift to franchised showrooms and data-driven pricing engines that optimize turnover.

By Distribution Channel: Offline Channel Surges

Digital Acceleration Continues Physical dealerships held 72.20% revenue in 2025, revealing the lasting need for tactile evaluation before purchase. However, online channels are compounding at 14.45% per year, and their influence on buyer research exceeds their share of final transactions. Virtual walk-around videos, instantaneous valuation tools, and end-to-end financing modules redefine consumer expectations. Click-and-collect models that blend internet discovery with brick-and-mortar delivery are emerging as the default pathway.Seasoned buyers who previously dismissed digital listings now rely on them for price benchmarking, while first-time millennial purchasers are confident in completing deals remotely. This dual behavior compresses pricing spreads and improves liquidity, reinforcing transparency across the Italy used car market.

By Vehicle Age: 4-6 Years Vehicles Dominated The Market

Newer Models Command Premium Vehicles aged 4-6 years accounted for 30.60% of 2025 turnover, balancing affordability and contemporary features. Meanwhile, the 0-3 year slice is expanding at 4.78% CAGR as price inflation in the new-car arena steers affluent shoppers to near-new stock that offers factory warranty remnants. Units older than 10 years face rising operational limitations in metropolitan low-emission zones, forcing dealers to pivot inventories toward compliant regions or adopt cross-border sales strategies.Italy’s 12.8-year average fleet age leaves latent replacement demand, yet regulatory frameworks accelerate churn at the younger end of the spectrum. Dealers that stock Euro 6 petrol and mild-hybrid vehicles in the 25,000-to-60,000-km range enjoy the fastest turnover and the most resilient margins within the Italy used car market.

Geography Analysis

Northern regions command the highest transaction values because industrial wages enable buyers to absorb near-new prices. Lombardy, Piedmont, Veneto, and Emilia-Romagna jointly face Euro 5 diesel bans that displace more than 1 million vehicles, forcing accelerated trade-ins or migrations to rural provinces. Higher BEV penetration in these regions drives a budding secondary battery-electric segment that aligns with local charging density.Central Italy balances performance and practicality.

Rome’s metropolitan zone, lacking the most stringent low-emission rules, supports brisk demand for both Euro 6 diesels and hybrids, creating a diversified inventory mix. Dealers here benefit from tourist-driven seasonality that prompts short leasing cycles and early fleet disposals, enriching late-model stock flows into the Italy used car market.Southern regions prioritize durability and fuel economy over advanced tech and thus gravitate to LPG, CNG, and older petrol vehicles.

Lower average income extends replacement intervals, but the availability of de-registered northern diesels at discounted prices keeps volumes steady. Limited charging infrastructure tempers BEV adoption for now, yet falling battery prices could unlock incremental demand and progressively level regional disparities.

Competitive Landscape

Italy’s used-vehicle arena remains moderately fragmented even as organized chains grow. SPOTICAR, backed by Stellantis, anchors the branded OEM segment through warranties and manufacturer-grade reconditioning. AutoScout24 complements OEM websites by offering cross-border listings, while Arval and LeasePlan remarket off-lease stock via wholesaling platforms that interface directly with dealer management systems.

Independent sellers harness personal networks and word-of-mouth credibility, a hallmark of Italian retail culture that larger entities find hard to replicate. Technology adoption is the fault line: AI-assisted damage recognition and automated pricing algorithms reside mostly with the top 20 organizers. Partnerships between mid-tier dealers and financial institutions embed insurance and maintenance bundles, raising barriers to entry. As consolidation gains pace, the Italy used car market inches toward a structure where five to seven national groups will likely dominate urban centers, with regional independents occupying value niches.

First-mover investments in vehicle-history integration could determine future competitive advantage. Firms that mesh telematics scores with certified-pre-owned warranties will differentiate readiness for online-only transactions, particularly important as digital natives swell the buyer base. International capital may accelerate this convergence, yet cultural nuances and complex zoning laws favor incumbents who already master local regulation.

Italy Used Car Industry Leaders

AUTO1 Group

Arval Service Lease Italia SpA

Ayvens Group (ALD Automotive Italia)

brumbrum SpA

BCA Italia srl

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Stellantis NV partnered with Ayvens in a pioneering effort to reshape the used car rental market. This collaboration supports the principles of the circular economy by revitalizing pre-owned vehicles. By prioritizing sustainable practices, they aim to reduce waste and optimize the use of existing resources, delivering benefits to both the environment and consumers.

- February 2025: Dealcar, a SaaS platform based in Barcelona, has raised Euro 3 million in a Seed funding round. The platform streamlines and digitizes the buying and selling process of used cars for dealerships of all sizes. The funding will be used to enhance their payment solution and drive the company's expansion in Italy.

Italy Used Car Market Report Scope

A used Car is a pre-owned vehicle that has previously had one or more retail owners. These cars are sold through a variety of outlets through independent dealers, online sales channels, and others.

Italy Used Car Market is segmented by car type, by propulsion, and by vendor type. Based on the car type, the market is segmented into Hatchback, Sedan, and SUV. Based on the Propulsion, the market is segmented into Internal Combustion engines and Electric.

Based on the Vendor type, the market is segmented into Organized and Unorganized. For each segment, the market sizing and forecast have been done on the basis of value (USD Billion).

By Car Type

| Hatchback |

| Sedan |

| SUV |

| MPV |

| Luxury & Sports |

By Propulsion

| Internal Combustion Engine (Petrol/Diesel) |

| Hybrid |

| Electric |

| LPG/CNG |

By Vendor Type

| Organized |

| Unorganized |

By Distribution Channel

| Online |

| Offline |

By Vehicle Age

| 0-3 Years |

| 4-6 Years |

| 7-10 Years |

| More than 10 Years |

| By Car Type | Hatchback |

| Sedan | |

| SUV | |

| MPV | |

| Luxury & Sports | |

| By Propulsion | Internal Combustion Engine (Petrol/Diesel) |

| Hybrid | |

| Electric | |

| LPG/CNG | |

| By Vendor Type | Organized |

| Unorganized | |

| By Distribution Channel | Online |

| Offline | |

| By Vehicle Age | 0-3 Years |

| 4-6 Years | |

| 7-10 Years | |

| More than 10 Years |

Key Questions Answered in the Report

What is the current value of the Italy used car market?

The Italy used car market stood at USD 89.33 billion in 2026 and is projected to reach USD 117.57 billion by 2031.

Which vehicle type dominates sales?

SUVs led 2025 turnover with 41.25% share and are forecast to grow at 7.12% CAGR during 2026-2031 period.

How fast are online channels growing?

Online platforms are set to expand at a 14.45% CAGR through 2031, outpacing offline growth but still relying on hybrid fulfillment.

Which propulsion segment is growing fastest?

Battery-electric vehicles show a 17.54% forecast CAGR, the highest among all powertrains, driven by affordable new-model launches and maturing charging networks.

Page last updated on: