Italy Nuclear Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

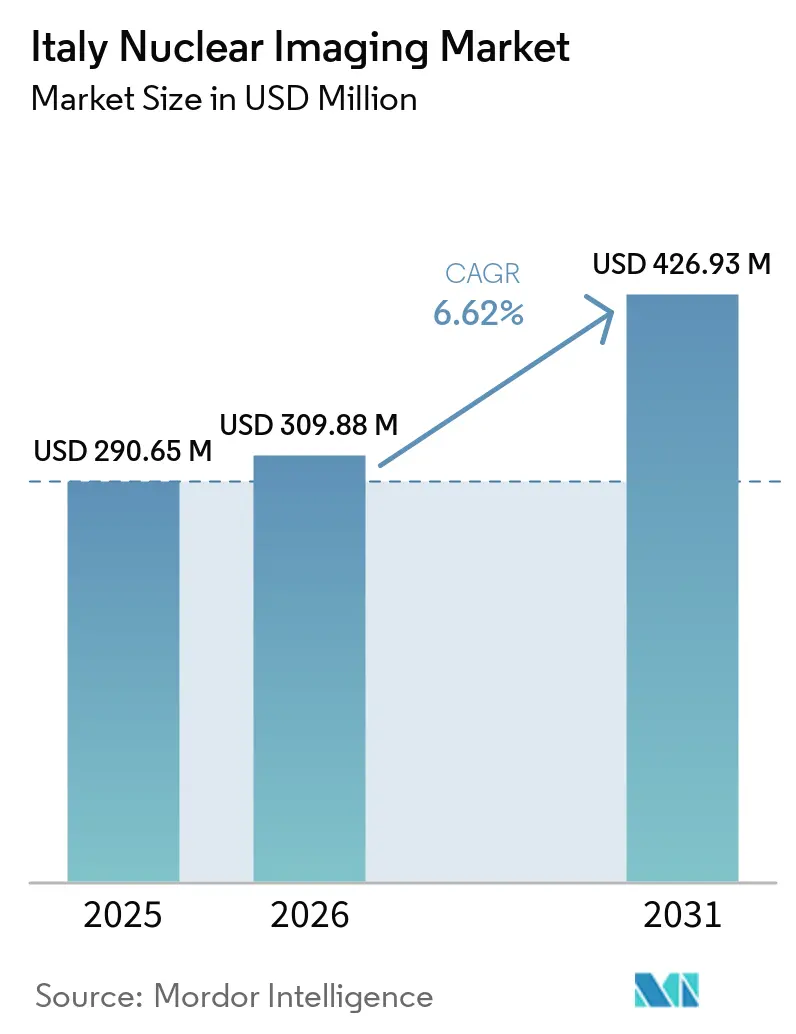

| Base Year Market Size (2025) | USD 290.65 Million |

| Market Size (2026) | USD 309.88 Million |

| Market Size (2031) | USD 426.93 Million |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Nuclear Imaging Market Analysis by Mordor Intelligence

The Italy Nuclear Imaging Market size is projected to expand from USD 290.65 million in 2025 and USD 309.88 million in 2026 to USD 426.93 million by 2031, registering a CAGR of 6.62% between 2026 to 2031.

Robust oncology demand, swift adoption of hybrid PET/CT and SPECT/CT platforms, and steady public-private spending on cyclotron-based radioisotope capacity anchor this upward trajectory. Northern regions capture a disproportionate share of new installations, leveraging denser hospital networks and favorable Servizio Sanitario Nazionale (SSN) tariffs to accelerate procedure volumes. Supply-chain stress linked to overseas Mo-99/Tc-99m reactors keeps domestic isotope innovation front-and-center, with ENEA’s SORGENTINA-RF and INFN’s LARAMED initiatives aiming to curb import reliance. Meanwhile, equipment vendors intensify competitive positioning through R&D-backed product launches and acquisitions that bundle hardware with theranostic tracers.

Key Report Takeaways

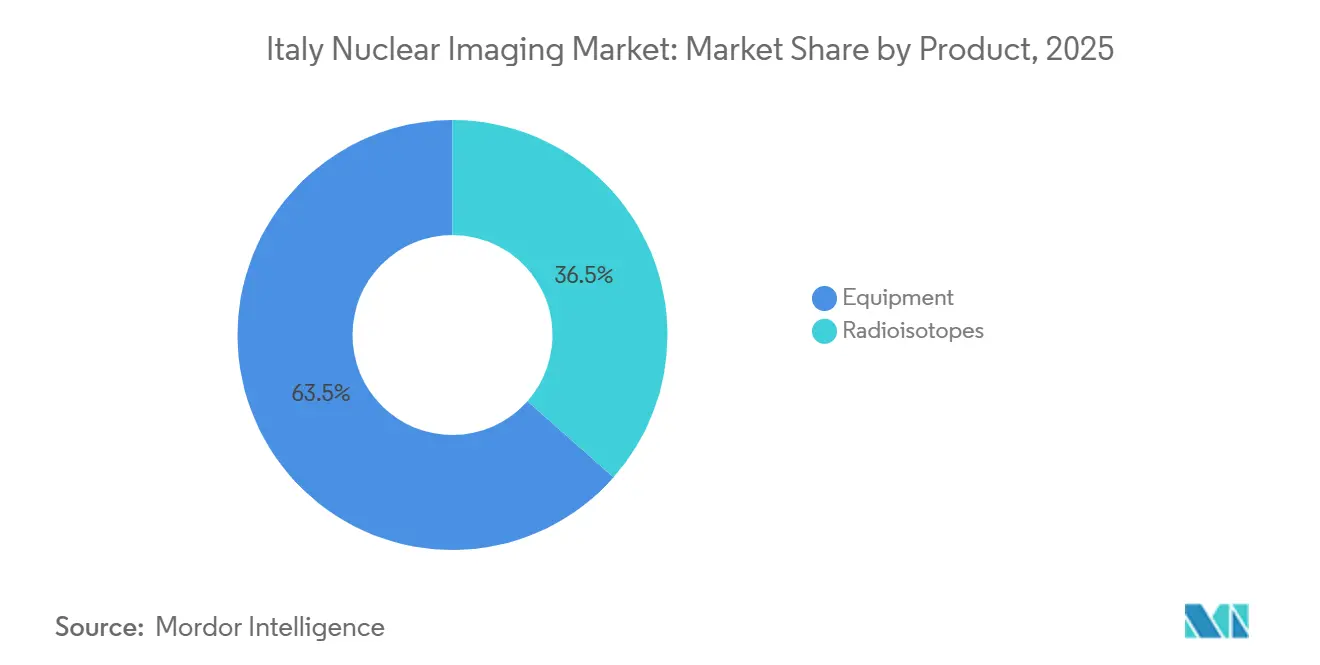

- By product category, equipment led with 63.55% of Italy nuclear imaging market share in 2025, radioisotopes are projected to post a 6.75% CAGR through 2031, the fastest among all categories.

- By application, oncology commanded 38.30% share of the Italy nuclear imaging market size in 2025, neurology is projected to expand at a 7.08% CAGR between 2026-2031.

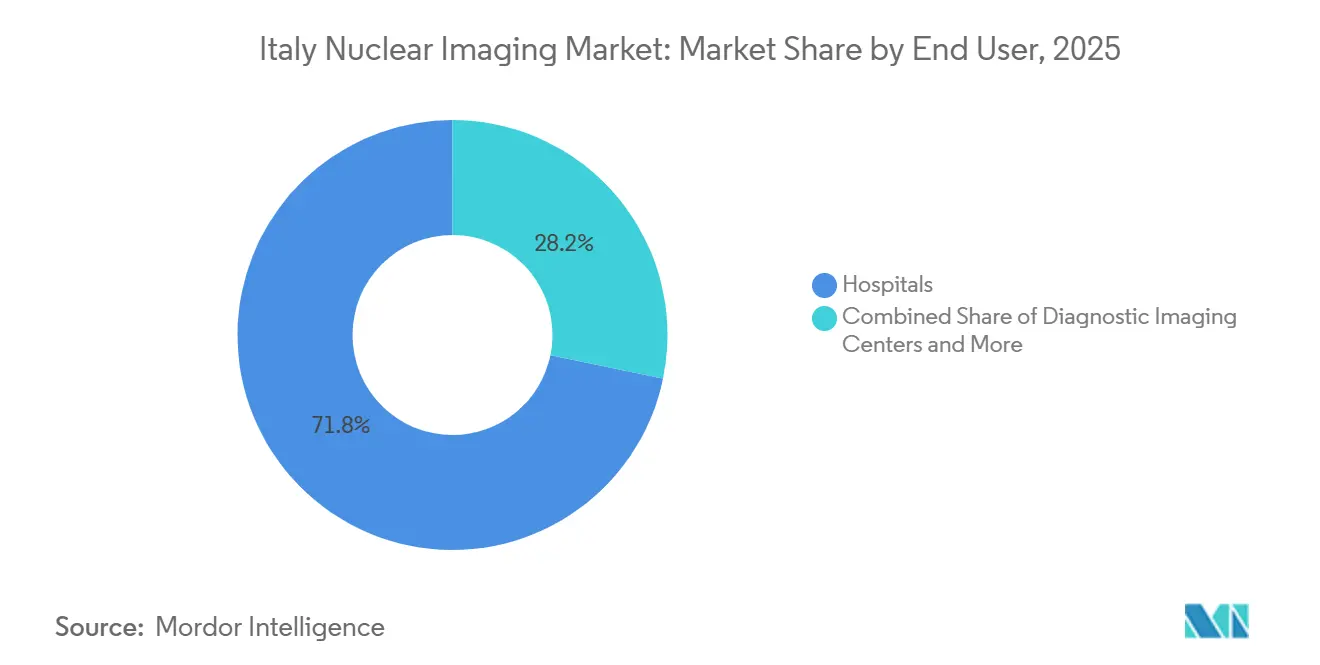

- By end user, hospitals accounted for 71.76% share of the Italy nuclear imaging market size in 2025, diagnostic imaging centers projected to expand at a 7.25% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Italy Nuclear Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of cancer & CVD | +1.80% | National, concentrated in Northern Italy | Medium term (2-4 years) |

| Growing adoption of hybrid PET/CT & SPECT/CT | +1.50% | Northern Italy, expanding to Central regions | Short term (≤ 2 years) |

| Favorable reimbursement framework (SSN tariffs) | +1.20% | National coverage with regional variations | Long term (≥ 4 years) |

| Increase in public-private investment for nuclear-medicine suites | +1.00% | Northern Italy, selective Southern expansion | Medium term (2-4 years) |

| Expansion of theranostic radioisotope production in Northern Italy | +0.80% | Northern Italy with national distribution | Long term (≥ 4 years) |

| Adoption of cyclotron-based Ga-68 generators in regional radiopharmacies | +0.60% | Northern Italy, gradual national rollout | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Cancer & CVD

New cancer diagnoses in Italy climbed to 390,700 in 2022, up 14,100 from 2020, with breast, colorectal, and lung cancers topping incidence charts. Mortality projections for 2025 signal a 3.5% national decline, yet aging cohorts continue to push demand for precise staging and therapy monitoring through PET/CT imaging. Hybrid modalities now influence treatment decisions in more than 42% of differentiated thyroid carcinoma cases, highlighting clinical reliance on molecular imaging. Cardiovascular disease persists as the primary mortality cause, and Tc-99m SPECT remains routine for perfusion assessment, reinforcing baseline procedure volumes.

Growing Adoption of Hybrid PET/CT & SPECT/CT

Italian participation in Europe-wide multimodality imaging surveys shows steady acceleration of PET/CT rollouts, with 18F-FDG dominating tracer use. University of Padua researchers recorded 100% sensitivity and 96% accuracy for [18F]FDG PET/MRI in hepatocellular carcinoma surveillance after liver transplantation, outperforming conventional protocols. A 502-patient multicenter trial demonstrated that segmental PET/CT lowers radiation dose without diagnostic compromise in solitary pulmonary nodules, supporting guideline updates. Northern centers advance niche tracers such as 64CuCl2 for bladder cancer staging, reinforcing regional leadership.

Favorable Reimbursement Framework

AIFA oversight ensures nuclear medicine procedures appear in national tariff lists, safeguarding predictable payback for hospitals across Italy. The EUR 15.62 billion (USD 18.27 billion) National Recovery and Resilience Plan earmarks digital infrastructure and primary-care upgrades from 2021-2026, indirectly smoothing patient pathways to molecular imaging. Decentralized SSN governance still causes tariff variation, but transparency lists narrow price dispersion and support capital planning for hybrid scanners. Complementary funds of EUR 2.387 billion (USD 2.79 billion) further finance hospital refurbishments, prompting energy-efficient equipment replacement cycles.

Increase in Public-Private Investment for Nuclear-Medicine Suites

Capital inflows intensify in Northern corridors, exemplified by Bracco Imaging’s EUR 80 million (USD 93.60 million) Hexagon manufacturing facility that triples ultrasound-contrast output. The government cleared Novartis’s EUR 80 million expansion in Torre Annunziata to scale pharmaceutical packaging by 2025, part of a South-oriented economic rejuvenation plan[1]Italian Government - Expansion of Novartis Pharmaceutical Plant in Torre Annunziata and Construction of a Resort in the Province of Taranto under a Unified SEZ for Southern Italy. GE HealthCare heads the EUR 25.3 million (USD 29.60 million) Thera4Care consortium, uniting 29 partners in isotope-production standardization. Parallel nuclear-energy joint ventures among Enel, Leonardo, and Ansaldo Energia may yield synergies for medical isotope supply.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment capital & maintenance costs | -1.40% | National, more pronounced in Southern Italy | Long term (≥ 4 years) |

| Mo-99 / Tc-99m supply bottlenecks | -1.10% | National impact with regional mitigation strategies | Short term (≤ 2 years) |

| Radiation-dose safety & regulatory scrutiny | -0.80% | National, with AIFA and ISS oversight | Medium term (2-4 years) |

| Emerging photon-counting CT substitution risk | -0.60% | Northern Italy early adoption, national expansion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Equipment Capital & Maintenance Costs

PET/CT platforms cost EUR 4 million (USD 4.68 million) and frequently require bunker upgrades, straining hospital budgets that already allocate nearly 77.45% of operational spending to facility management. Aging buildings, 70% surpassing their designed 50-year lifecycle, magnify retrofit expenses, especially in Southern provinces with fewer tertiary centers. Maintenance contracts with multinational OEMs add long-term overhead, prompting some regions to defer scanner refresh cycles and rely on referral flows to Northern hubs.

Mo-99/Tc-99m Supply Bottlenecks

Italy conducts more than 600,000 examinations annually with technetium-99m, yet depends on aging European reactors such as Petten’s High Flux Reactor, whose outages disrupt tracer availability. ENEA’s SORGENTINA-RF pilot dissolves molybdenum in hydrogen peroxide to yield domestic 99mTc batches, but economic parity with generator supply remains elusive. National contingency protocols include cyclotron-based back-ups and cross-regional patient redistribution, yet high isotope cost persists as a limiting factor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Equipment Dominance Drives Infrastructure Modernization

Equipment retained 63.55% Italy nuclear imaging market share in 2025 as hospitals prioritized PET/CT and SPECT/CT replacements to meet hybrid-imaging demand. Lombardy, Veneto, and Emilia-Romagna collectively host the densest scanner fleets, benefiting from consistent SSN reimbursements and regional budget surpluses. The radioisotope segment advances at a 6.75% CAGR, buoyed by expanding Ga-68 and Lu-177 pipelines that support theranostic protocols. Cyclotron-based production shortens supply chains and elevates the Italy nuclear imaging market size for isotopes, particularly as LARAMED scales multi-curie outputs. Northern laboratories integrate artificial-intelligence-driven QC systems to optimize batch scheduling and reduce waste, a practice expected to cascade nationwide.

Adoption of energy-efficient digital scanners tempers hospital utility overhead and aligns with EU Green Deal directives, strengthening capital-expenditure cases. Vendor service-as-a-subscription models further mitigate upfront cost, encouraging smaller Southern facilities to enter the modality mix, albeit at slower cadence. Continuous performance upgrades, such as extended axial field-of-view detectors, are forecast to keep equipment leading Italy nuclear imaging market revenues through 2031.

By Application: Oncology Leadership Amid Neurological Growth

Oncology anchored 38.30% of 2025 procedure revenue, reflecting wide guideline inclusion for PET/CT in staging breast, lung, colorectal, and prostate malignancies. Neurology shows the sharpest climb at 7.08% CAGR as dementia prevalence in Italy’s aging population lifts F-18 amyloid and tau tracer demand. Cardiology sustains baseline volumes via Tc-99m SPECT perfusion, while thyroid applications benefit from standardized PRRT protocols released by the Italian Association of Nuclear Medicine. The oncology segment leverages PSMA and FAPI tracer innovation, broadening theranostic grids and reinforcing its dominance in Italy nuclear imaging market revenues.

Clinical trials such as the ITALIAN study validate radiation-sparring imaging workflows, bolstering payer confidence and supporting wider reimbursement for newer tracers. Emerging fibrotic-activity tracers expand the “other applications” bucket, hinting at diversified future revenue streams but not yet shifting share lines materially.

By End User: Hospital Consolidation Versus Private Expansion

Hospitals controlled 71.76% of procedures and tracer purchases in 2025, cementing their role as the backbone buyer in the Italy nuclear imaging market size. Diagnostic imaging centers, however, race ahead with a 7.25% CAGR as private chains exploit gaps in Southern service coverage and capture outbound patient flows. Academic and research institutes underpin innovation pipelines, often partnering with OEMs for first-in-human tracer trials and next-generation detector evaluations.

Hospital mergers and regional hub-and-spoke models aim to rationalize high-complexity workloads, yet operational costs still exceed sustainable thresholds, nudging administrators toward outsourcing non-core nuclear medicine services to accredited private centers. The government’s “super hospitals” blueprint could rebalance geography but faces scrutiny over capital efficiency and timelines.

Geography Analysis

Northern Italy captures the lion’s share of equipment installations and isotopic manufacturing, aided by a cluster of institutions, including INFN Legnaro, CNAO Pavia, and the Trento Proton Center-that collectively shape the technical frontier. Bracco Imaging’s Milan headquarters and Siemens Healthineers’ PETNET facility in Ivrea round out a vertically integrated ecosystem stretching from drug substance to finished dose. Regional healthcare budgets support higher scanner density, Lombardy alone runs 97 acute hospitals, translating into broader access and lower wait times.

Central Italy taps strengths in academic research and regulatory stewardship from Rome, yet market penetration trails the North. AIFA’s presence fosters faster price-listing for innovative tracers, but capital investments remain lopsided. Southern Italy struggles with a 21.3% escape index for complex imaging, reflecting patient migration northward for advanced care. Government-approved pharmaceutical plant expansions in Torre Annunziata and SEZ fiscal incentives aim to seed a nucleus for future nuclear medicine growth, but scanner deployment still lags.

Proton therapy exemplifies geographic imbalance: all three operational centers are Northern, leaving head-and-neck patients in the South reliant on cross-regional referrals, a gap current capacities fail to bridge. Although new “super hospital” proposals could mitigate disparities, financing and staffing hurdles temper near-term forecasts. Overall, regional divergence remains a structural feature shaping procurement cycles, utilization rates, and ultimately the Italy nuclear imaging market.

Competitive Landscape

The Italy nuclear imaging market features moderate consolidation as capital intensity and regulatory barriers curb entrant numbers. Multinationals such as Siemens Healthineers, GE HealthCare, and Bracco Imaging dominate equipment and tracer supply, sustained by global manufacturing scale and deep IP portfolios. Siemens’ USD 223 million acquisition of Novartis’s Advanced Accelerator Applications Molecular Imaging in December 2024 expanded its European radiopharmacy network to 13 sites, bolstering PET tracer reach across Italy[2]Press Release: Siemens Healthineers Acquires Advanced Accelerator Applications Molecular Imaging. GE HealthCare’s full takeover of Nihon Medi-Physics in March 2025 underscores plans to integrate tracer production with scanner analytics and cloud platforms.

Domestic incumbent Bracco Imaging continues to allocate more than 10% of revenue to R&D and now controls over 1,500 patents, positioning itself as a global force in contrast media and precision diagnostics. White-space opportunity persists in local cyclotron networks and Southern infrastructure upgrades, arenas where regional players and public-private consortia could carve share. Artificial-intelligence-enabled workflow tools, spanning dose optimization to lesion detection, add another layer of differentiation, invigorating competition beyond hardware specs.

Start-ups and midsize firms gain footing through theranostic niches; Curium’s March 2025 purchase of Monrol amplifies Lu-177 capacity, an isotope pivotal to prostate and neuroendocrine tumor therapy. Meanwhile, Blue Earth Therapeutics secured USD 77 million to advance PSMA-targeted candidates, enriching the innovation pipeline. Overall, supplier strategies converge on end-to-end service models that fuse scanners, tracers, and analytics, intensifying rivalry and raising switching costs for Italian providers.

Italy Nuclear Imaging Industry Leaders

GE Healthcare

Koninklijke Philips N.V.

Siemens Healthineers AG

Fujifilm Holdings Corporation

Canon Medical Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Bracco Imaging, an Italian company entered into a strategic partnership with NYU Langone Health to drive innovation in medical imaging through a multi-year Master Research Agreement (MRA).

- May 2025: The IAEA Director General announced a collaboration targeting energy, cancer care, agriculture, and environmental initiatives, aligning with the country's efforts to adopt nuclear energy as a sustainable power source.

Italy Nuclear Imaging Market Report Scope

As per the scope of the report, nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers.

The Italy nuclear imaging market is segmented by product, application, and end user. By product, the market is divided into equipment and radioisotopes, with the radioisotopes segment further categorized into SPECT radioisotopes, including technetium-99m (Tc-99m), thallium-201 (Tl-201), gallium-67 (Ga-67), iodine-123 (I-123), and other SPECT isotopes, and PET radioisotopes, including fluorine-18 (F-18), rubidium-82 (Rb-82), and other PET isotopes. By application, the market is segmented into cardiology, neurology, thyroid, oncology, and other applications. By end user, the market is categorized into hospitals, diagnostic imaging centers, and academic and research institutes. The report offers the value (in USD) for the above segments.

| Equipment | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) |

| Thallium-201 (Tl-201) | ||

| Gallium-67 (Ga-67) | ||

| Iodine-123 (I-123) | ||

| Other SPECT Isotopes | ||

| PET Radioisotopes | Fluorine-18 (F-18) | |

| Rubidium-82 (Rb-82) | ||

| Other PET Isotopes | ||

| Cardiology |

| Neurology |

| Thyroid |

| Oncology |

| Other Applications |

| Hospitals |

| Diagnostic Imaging Centres |

| Academic & Research Institutes |

| By Product | Equipment | ||

| Radioisotopes | SPECT Radioisotopes | Technetium-99m (Tc-99m) | |

| Thallium-201 (Tl-201) | |||

| Gallium-67 (Ga-67) | |||

| Iodine-123 (I-123) | |||

| Other SPECT Isotopes | |||

| PET Radioisotopes | Fluorine-18 (F-18) | ||

| Rubidium-82 (Rb-82) | |||

| Other PET Isotopes | |||

| By Application | Cardiology | ||

| Neurology | |||

| Thyroid | |||

| Oncology | |||

| Other Applications | |||

| By End User | Hospitals | ||

| Diagnostic Imaging Centres | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

How big is the Italy Nuclear Imaging Market?

Italy nuclear imaging market, valued at USD 290.65 million in 2025 and USD 309.88 million in 2026, is set to reach USD 426.93 million by 2031, marking a CAGR of 6.62% from 2026 to 2031.

What is the current Italy Nuclear Imaging Market size?

In 2026, Italy Nuclear Imaging Market size is expected to reach USD 309.88 million.

Who are the key players in Italy Nuclear Imaging Market?

GE Healthcare, Koninklijke Philips N.V., Siemens Healthineers AG, Fujifilm Holdings Corporation, Canon Medical Systems Corporation are the major companies operating in the Italy Nuclear Imaging Market.

Which product is growing the fastest?

Radioisotopes are forecast to post an 6.75% CAGR between 2026-2031.

Page last updated on: