Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

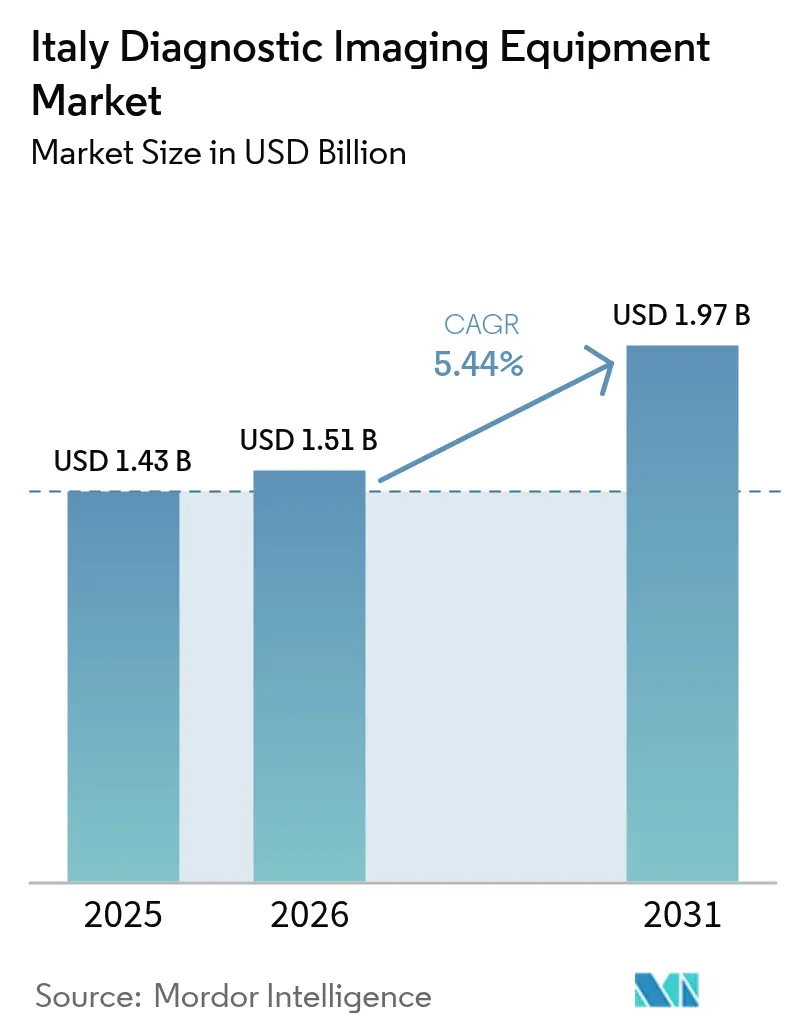

| Base Year Market Size (2025) | USD 1.43 Billion |

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 1.97 Billion |

| Growth Rate (2026 - 2031) | 5.44% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The Italy diagnostic imaging equipment market size was valued at USD 1.43 billion in 2025 and estimated to grow from USD 1.51 billion in 2026 to reach USD 1.97 billion by 2031, at a CAGR of 5.44% during the forecast period (2026-2031). Capacity upgrades financed by the National Recovery and Resilience Plan (PNRR) and private-sector investments are accelerating equipment replacement cycles and digital connectivity. Demand is reinforced by population aging, the high burden of oncological and cardiovascular diseases, and progressive adoption of artificial intelligence (AI) for image interpretation. Vendors respond with photon-counting CT, open-architecture MRI, and mobile X-ray systems that shorten exam times and fit emerging point-of-care workflows. Regional convergence policies and uniform national tariffs introduced in 2025 are expected to lift procedure volumes in historically underserved Southern provinces, while the hospitality of Italy’s sprawling private diagnostics network continues to attract self-pay and cross-border patients.

Key Report Takeaways

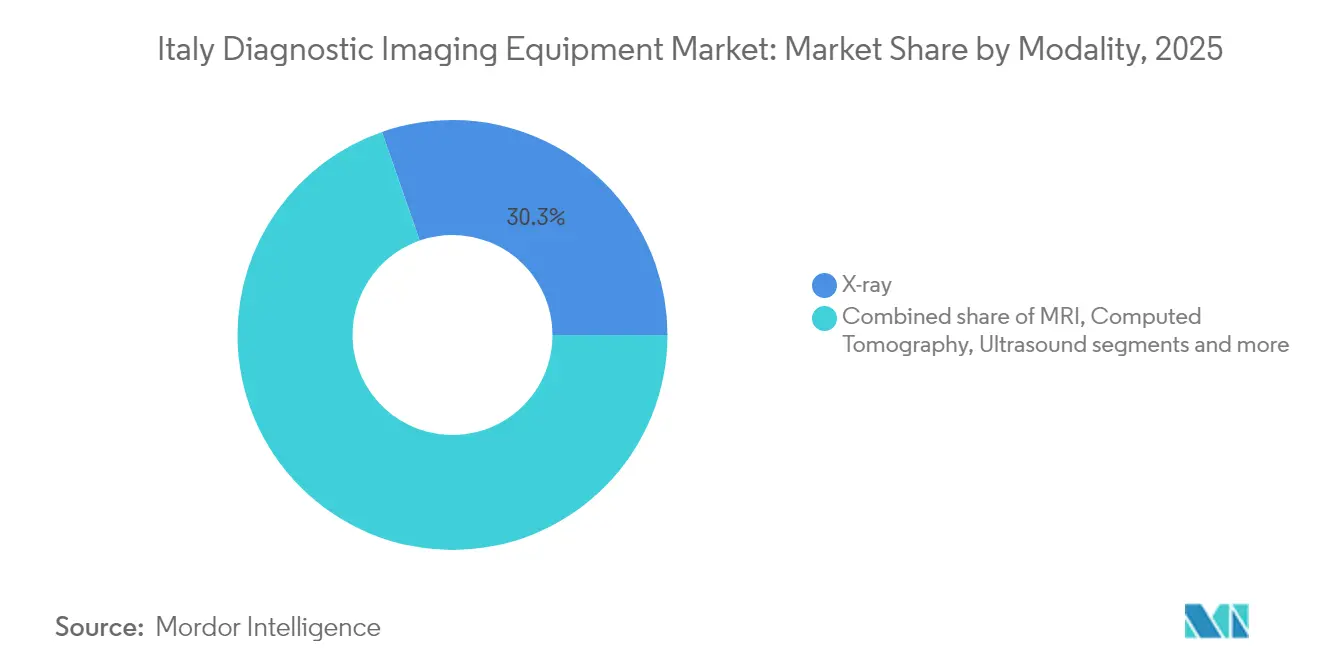

- By modality, X-ray led with 30.32% revenue share in 2025, whereas MRI is positioned to expand at a 7.17% CAGR to 2031.

- By portability, fixed systems held 81.12% of the Italy diagnostic imaging equipment market share in 2025; mobile and handheld systems are rising fastest at 6.79% CAGR.

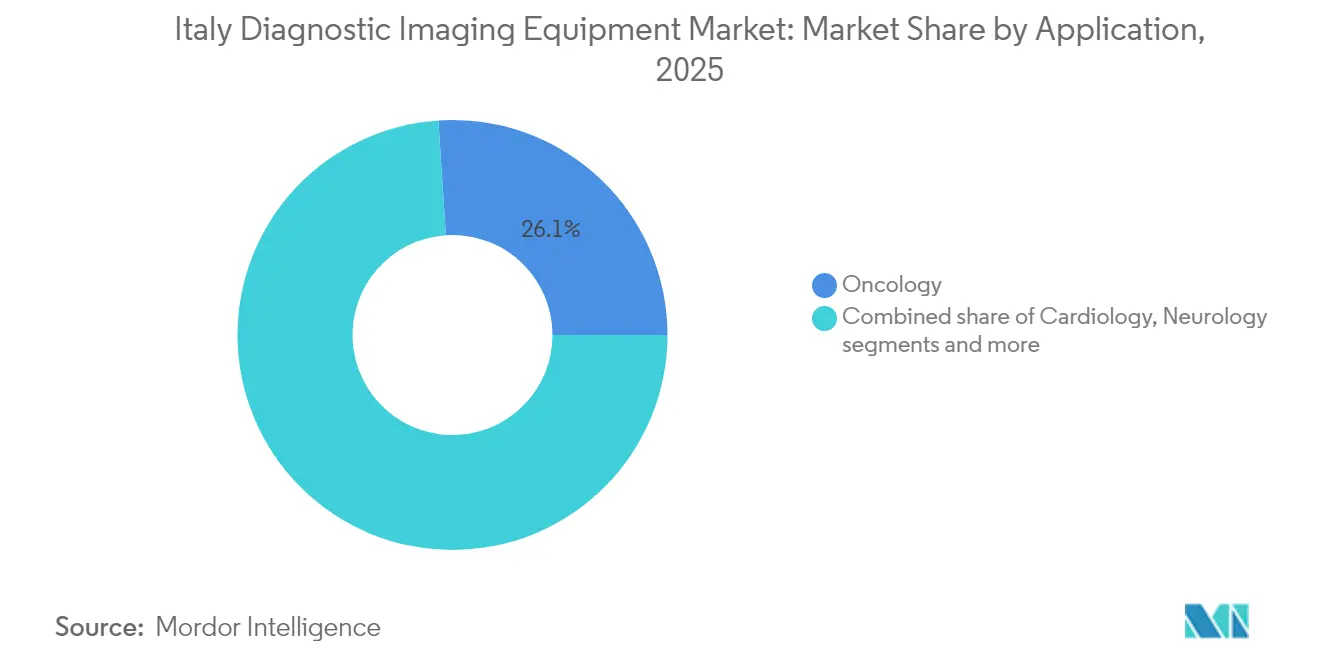

- By application, oncology accounted for 26.05% of the Italy diagnostic imaging equipment market size in 2025; cardiology is projected to grow at 7.15% CAGR through 2031.

- By end user, hospitals generated 68.92% of 2025 revenues, while diagnostic imaging centers exhibit the highest projected CAGR of 6.78%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic aging and escalating chronic-disease incidence | +1.8% | National, higher in Northern regions | Long term (≥ 4 years) |

| Large-scale government & EU recovery funding for healthcare modernization | +1.2% | National, priority to Southern regions | Medium term (2-4 years) |

| Rapid technological breakthroughs in multimodal imaging | +0.9% | Global, early adoption in major Italian medical centers | Medium term (2-4 years) |

| Rising uptake of point-of-care, portable and mobile imaging platforms | +0.7% | National, accelerated in emergency and ICU settings | Short term (≤ 2 years) |

| Growing emphasis on precision, preventive and value-based care models | +0.6% | National, led by academic medical centers | Long term (≥ 4 years) |

| Expansion of private diagnostics and outpatient imaging networks | +0.4% | National, concentrated in Northern and Central Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demographic Aging and Escalating Chronic-Disease Incidence

Citizens aged ≥65 are expected to climb from 24% to 34% by 2050, driving multi-modality follow-up for cancers, heart disease, and musculoskeletal conditions.[1]Source: Italia Domani, “Home – Italia Domani,” italiadomani.gov.it Hospital radiology departments report increasing examination complexity that favors higher-throughput CT scanners, wide-bore MRI, and iterative reconstruction software. Workflow automation and patient-comfort features gain priority as frail patients require longer positioning times. Vendors that combine low-dose protocols with rapid image reconstruction gain a competitive edge in the Italy diagnostic imaging equipment market.

Large-Scale Government & EU Recovery Funding for Healthcare Modernization

The PNRR sets aside funds to replace 3,100 legacy systems and digitalize 280 emergency departments, triggering a concentrated equipment buying cycle that benefits premium vendors able to guarantee cyber-secure interoperability. Southern hospitals receive above-average budget shares, narrowing the historic North–South technology gap. Public tenders favor systems offering AI-ready architectures, remote service diagnostics, and energy-saving standby modes, reinforcing high-spec replacements across the Italy diagnostic imaging equipment market.

Rapid Technological Breakthroughs in Multimodal Imaging

Academic hubs such as San Raffaele Hospital operate photon-counting CT and 3 T whole-body MRI to improve soft-tissue contrast and reduce radiation dose.[2]Source: Gruppo San Donato, “Photon Counting CT…San Raffaele,” gsdinternational.com Multimodal fusion of PET with MRI is gaining traction in neuro-oncology and cardiac sarcoidosis. Early adopters cite lower repeat-scan rates and greater clinician confidence, pushing the Italy diagnostic imaging equipment market toward integrated hardware-software ecosystems.

Rising Uptake of Point-of-Care, Portable and Mobile Imaging Platforms

Bedside ultrasound, mobile DR X-ray carts, and battery-powered CT are now embedded in emergency protocols forged during the COVID-19 pandemic. Hospitals report shorter patient transfer times and reduced cross-infection risk, justifying capital outlays for compact consoles and wireless probes. Handheld ultrasound is spreading from emergency medicine into cardiology and obstetrics, adding incremental volumes to the Italy diagnostic imaging equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of imaging equipment & procedures | -0.8% | National, more pronounced in Southern regions | Long term (≥ 4 years) |

| Lengthy regulatory, reimbursement and public-tender procedures | -0.6% | National, bureaucratic delays in public sector | Medium term (2-4 years) |

| Persistent shortage of qualified radiologists and technologists | -0.5% | National, critical shortage in rural areas | Long term (≥ 4 years) |

| Regional disparities in imaging infrastructure utilization and access | -0.3% | North–South divide, rural–urban disparities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Imaging Equipment & Procedures

Out-of-pocket healthcare spending rose 10.3% in 2023, and 4.5 million citizens skipped care due to cost. Capital budgets in smaller hospitals lag behind recommended five-to-seven-year replacement cycles, suppressing demand for high-end MRI and hybrid scanners. Service contracts, software upgrades, and energy costs compound financial strain, limiting purchasing power in parts of the Italy diagnostic imaging equipment market.

Lengthy Regulatory, Reimbursement and Public-Tender Procedures

Italian public tenders can stretch beyond 18 months, delaying installations and eroding vendor margins. Multi-layer approval pathways for new procedure codes slow clinical adoption of advanced modalities such as photon-counting CT. Smaller facilities lack dedicated procurement staff, handing bargaining power to large university hospitals. The resulting inertia reduces near-term revenues in the Italy diagnostic imaging equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: X-Ray Dominance Faces MRI Innovation Challenge

X-ray retained 30.32% share in 2025, underpinned by universal clinical use and economical operating costs. Digital radiography upgrades continue to replace film systems, securing steady replacement demand within the Italy diagnostic imaging equipment market. Advanced detectors and dose-reduction algorithms enhance image quality while easing regulatory compliance.

MRI, however, is set to grow at a 7.17% CAGR as open-bore systems reduce claustrophobia and 3 T platforms shorten scan times. Esaote’s Magnifico Open drove a 3.3% sales increase in 2023. Neuro-oncology, musculoskeletal sports injuries, and cardiac viability studies widen clinical indications, elevating the MRI slice of the Italy diagnostic imaging equipment market size for hospital and private settings alike.

By Portability: Fixed Systems Stability Challenged by Mobile Innovation

Fixed units held 81.12% of 2025 revenues, anchored by high-throughput CT, MRI, and angio suites that integrate with PACS and hospital information systems. PNRR budgets prioritize like-for-like replacements, ensuring short-term stability in this segment of the Italy diagnostic imaging equipment market.

Mobile and handheld devices are scaling at 6.79% CAGR. Wireless ultrasound probes and wheeled DR carts support surge capacity in ICUs and emergency departments. Their flexibility aligns with evolving care models such as hospital-at-home, expanding the Italy diagnostic imaging equipment market share for vendors that optimize weight, battery life, and image quality.

By Application: Oncology Leadership Meets Cardiology Growth Surge

Oncology accounted for 26.05% of total revenue in 2025. Multi-modality protocols spanning CT, MRI, PET/CT, and mammography underpin precision staging and therapy monitoring. Photon-counting CT at San Raffaele enhances lesion conspicuity and reduces follow-up scans, entrenching oncology’s command of the Italy diagnostic imaging equipment market.

Cardiology is projected to accelerate at 7.15% CAGR, propelled by calcium-scoring CT, stress perfusion MRI, and 3-D echocardiography. Reimbursement expansion for non-invasive ischemia testing and aging demographics drive hospitals to add advanced cardiac imaging suites, enlarging the Italy diagnostic imaging equipment market size allocated to heart care.

By End User: Hospital Dominance Faces Diagnostic Center Disruption

Hospitals contributed 68.92% of 2025 revenue, leveraging integrated care pathways, emergency coverage, and PNRR-funded upgrades. Clinical engineering departments align equipment cycles with risk-management protocols, supporting steady procurement within the Italy diagnostic imaging equipment market.

Diagnostic imaging centers, however, are rising at 6.78% CAGR. They offer rapid scheduling, subspecialty reading, and patient-friendly environments, siphoning elective volumes from public hospitals. Franchise models achieve scale economies in equipment leasing and teleradiology, tilting future demand in the Italy diagnostic imaging equipment industry toward outpatient settings.

Geography Analysis

Northern regions such as Lombardy, Veneto, and Emilia-Romagna command the largest portion of the Italy diagnostic imaging equipment market, buoyed by dense hospital networks, higher disposable income, and home-grown manufacturers like Esaote in Genoa. Early adoption of AI-enabled PACS and 3 T MRI supports procedure growth and keeps waiting lists below national averages. Cross-border patients from Switzerland and Austria add incremental volumes.

Central Italy, anchored by Rome and Florence, benefits from a balanced mix of university hospitals, military medical facilities, and private diagnostics hubs. The region hosts flagship installations of photon-counting CT and hybrid PET/MR, reinforcing its role as a clinical research corridor. Public-private partnerships enable joint investment in high-field MRI and advanced ultrasound laboratories, expanding the Italy diagnostic imaging equipment market for both sectors.

Southern Italy and the Islands historically lag in modality density, yet PNRR allocations now finance core replacements, RIS/PACS roll-outs, and mobile fleets that service rural catchments. Vendor strategies here emphasize lower-cost configurations, extended warranties, and workforce training that collectively enlarge the Italy diagnostic imaging equipment market base while narrowing the national care gap.

Competitive Landscape

The Italy diagnostic imaging equipment market shows moderate concentration. Siemens Healthineers, GE HealthCare, and Philips jointly supply most multi-modality tenders, leveraging full-line portfolios, local service hubs, and financing arms. Siemens posted 7.6% imaging revenue growth in fiscal Q1 2025, while GE spearheads the EU-funded Thera4Care theranostics project, embedding SPECT-CT scanners with AI.

Philips invested EUR 1.7 billion in R&D and topped the 2024 European Patent Office league table with 594 medical technology filings. Its cloud-based enterprise imaging suite launched in Europe in 2025, bundling AI workflow tools that lock clients into subscription ecosystems. Canon Medical and Fujifilm compete in ultrasound and CT niches, often pairing with local distributors to penetrate community hospitals.

Domestic champion Esaote excels in dedicated MRI and premium ultrasound. Italian X-ray specialists Italray and Gilardoni supply cost-competitive DR rooms, while Bracco ramps contrast-agent output by USD 86 million to safeguard supply chains. Competitive levers increasingly revolve around AI-assisted interpretation, life-cycle service contracts, and sustainability credentials rather than raw hardware specifications, shaping procurement priorities across the Italy diagnostic imaging equipment market

Italy Diagnostic Imaging Equipment Industry Leaders

Fujifilm Holdings Corporation

Siemens Healthineers

Koninklijke Philips N.V.

Esaote SpA

GE HealthCare

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Mindray launched the Resona A20 premium radiology ultrasound system featuring Acoustic Fusion Matrix transducers and AI tools in Italy.

- June 2024: Esaote unveiled the MyLab E80 ultrasound platform for complex cases.

- November 2023: Vein Clinic Brescia deployed MGI Tech’s Imabot X for remote ultrasound scanning.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Italian diagnostic imaging equipment market as all new capital-equipment systems that produce in-vivo anatomic or functional images, namely X-ray, CT, MRI, ultrasound, nuclear imaging, fluoroscopy, and mammography units, sold to hospitals, imaging centers, ambulatory surgical centers, and other clinical users across Italy.

Scope exclusion: accessory software sold separately, contrast media, post-sale service contracts, and imaging services are not counted within the revenue base.

Segmentation Overview

- By Modality

- MRI

- Computed Tomography

- Ultrasound

- X-Ray

- Nuclear Imaging (PET/SPECT)

- Fluoroscopy

- Mammography

- By Portability

- Fixed Systems

- Mobile and Hand-held Systems

- By Application

- Cardiology

- Oncology

- Neurology

- Orthopedics

- Gastroenterology

- Gynecology & Obstetrics

- Other Applications

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Ambulatory Surgical Centers

- Other End Users

Detailed Research Methodology and Data Validation

Primary Research

Interviews with radiology department heads, biomedical engineers, procurement managers, and modality specialists across Lombardy, Lazio, Emilia-Romagna, and Sicily helped us stress-test utilisation assumptions, replacement cycles, and average selling prices. Short online surveys with private imaging-center owners validated growth pockets that were invisible in desk data.

Desk Research

We began with publicly available datasets from ISTAT, the Ministry of Health medical-device registry, Eurostat trade statistics, and OECD Health Data, which supplied baseline shipment, procurement, and procedure volumes. Additional insight came from Radiology and Imaging Societies in Italy, peer-reviewed journals such as European Radiology, and tender notices captured through the Tenders Info paid feed. Company filings on CONSOB, press releases, and import filings on Volza offered price and competitive context. These examples illustrate, rather than exhaust, the secondary sources consulted; numerous other public and paid references informed our view.

Market-Sizing & Forecasting

We reconstructed national demand through a top-down model that links installed-base inventories, average replacement age, and new NRRP-funded purchases to annual equipment flows, which are then value-scaled by verified ASP curves. Targeted bottom-up checks, supplier roll-ups for CT and MRI, and channel checks for ultrasound served as guardrails. Key variables include: 1) NRRP capital outlay by modality, 2) population aged >=65, 3) oncology and cardiology imaging procedure growth, 4) modality-specific ASP deflation, and 5) euro-dollar exchange paths. A multivariate regression of unit demand against demographic and spending indicators underpins the forecast, with scenario analysis cushioning policy or currency shocks. Data gaps on private-sector volumes were bridged with moderated extrapolations from sample clinics and ISTAT service-output indices.

Data Validation & Update Cycle

Outputs pass variance checks against historical trade and production lines, peer review by a senior analyst, and a cross-tool anomaly screen. Models refresh annually, with interim updates triggered by material events such as major tenders or reimbursement changes. Before release, an analyst reruns the latest data pull to ensure clients receive the freshest baseline.

Why Our Italy Diagnostic Imaging Equipment Baseline Commands Reliability

Published figures often diverge because firms choose differing modality baskets, price conventions, and refresh cadences.

Key gap drivers include: some studies bundle only digital hardware, omit handheld ultrasound, or apply global ASP curves without Italian tender discounts; others freeze assumptions from pre-NRRP purchase plans, whereas Mordor's base case embeds the EUR 1.18 billion upgrade budget and the 24 percent geriatric share that pushes multi-modality demand.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.43 B (2025) | Mordor Intelligence | - |

| USD 0.98 B (2024) | Regional Consultancy A | excludes mobile X-ray and handheld ultrasound; uses list prices not tender prices |

| USD 0.88 B (2024) | Trade Journal B | projects only digital modalities and ignores NRRP-funded backlog replacement |

In sum, by anchoring revenues to verified tenders, triangulating with expert insight, and revisiting models every year, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What government measure is most influential in refreshing Italy’s diagnostic imaging fleet?

The National Recovery and Resilience Plan is funneling dedicated funds into public hospitals, prompting rapid replacement of aging scanners with digitally connected, AI-ready systems.

Which imaging technologies are seeing the quickest clinical adoption because of artificial intelligence?

MRI and CT platforms integrated with automated post-processing and triage algorithms are gaining traction, as radiology departments seek to shorten report turnaround times and boost diagnostic confidence.

How are mobile and handheld imaging units changing day-to-day patient management?

Portable ultrasound and mobile X-ray carts let clinicians conduct exams at the bedside or in emergency bays, cutting patient transfers, easing infection-control protocols, and enabling faster treatment decisions.

Why are private diagnostic centers expanding their footprint across Italy?

Shorter appointment lead times, flexible opening hours, and tailored patient experiences are drawing referrals away from crowded hospital radiology suites, encouraging private operators to open additional sites.

In what way is the shortage of radiologists shaping equipment purchases?

Hospitals favor scanners with embedded automation, remote reading compatibility, and decision-support software to maximize productivity and help overextended clinicians handle rising exam volumes.

What impact do uniform national tariffs have on regional imaging access?

Standardized reimbursement rates are leveling the playing field between northern and southern provinces, prompting providers in underserved areas to invest in modern equipment and expand service capacity.

Page last updated on: